Key takeaways

- Since April 1, 2023, every company in India must maintain unalterable audit trails for all AP activities, including invoice edits, approvals, and payments, with logs preserved for statutory retention periods.

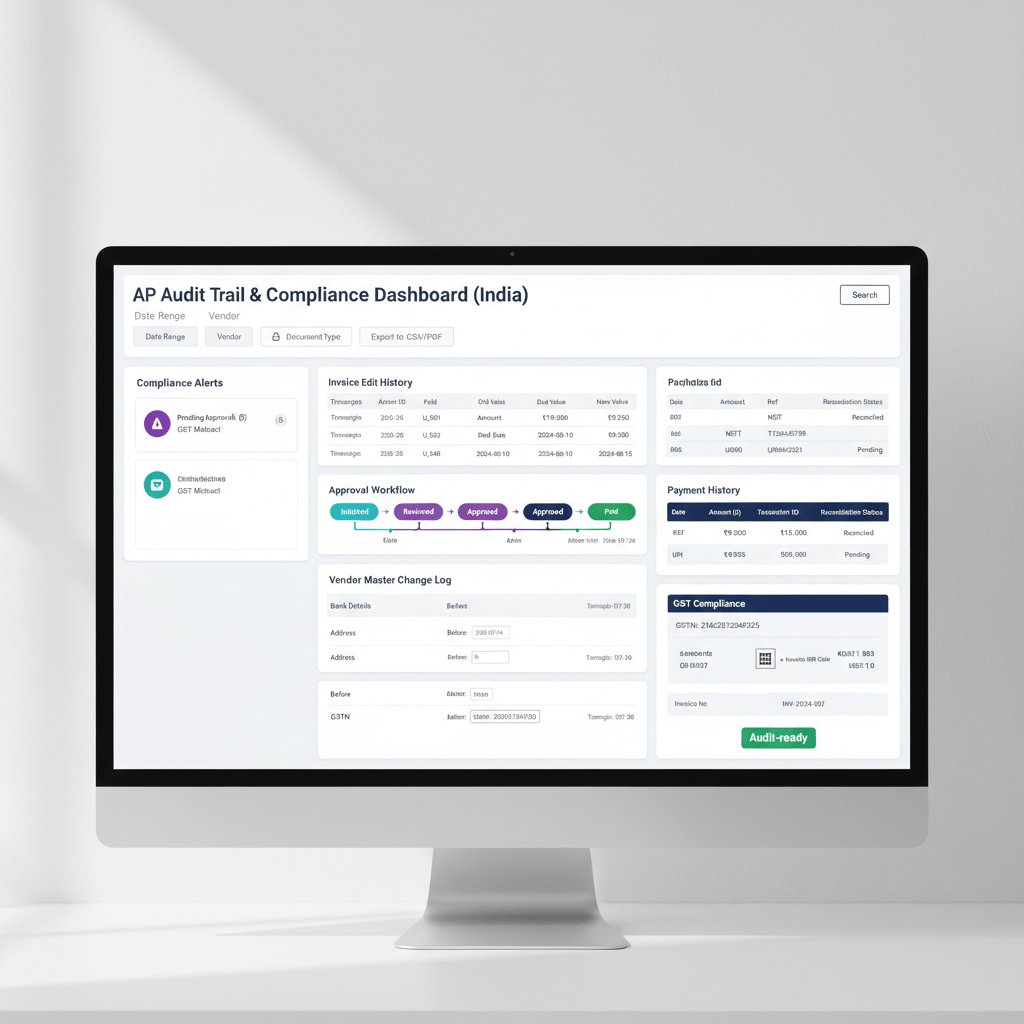

- AP audit trails should capture who did what, when, and why, including user ID, timestamp, IP, old and new values, reason codes, and references to supporting documents, creating an end to end evidence chain.

- Well defined approval workflows, backed by a Delegation of Authority matrix and enforced maker-checker controls, are essential to demonstrate separation of duties.

- High risk vendor master changes, such as bank account or GSTIN updates, must follow change request and verification workflows, with clear approval evidence and before or after snapshots.

- Payment processing documentation should link each invoice to fund transfer references, partial or advance adjustments, reversals, and bank reconciliations, ensuring audit ready traceability.

- Automation platforms like AI Accountant can automatically capture granular AP audit trails, integrate with Tally and Zoho Books, and generate audit evidence packs.

- Ongoing monitoring with KPIs, monthly spot checks, and quarterly access reviews keeps AP audit trail compliance effective and exam ready for statutory audits.

Understanding India’s Audit Trail Requirements for Accounts Payable

The Ministry of Corporate Affairs requires that all companies using accounting software maintain uneditable, continuous audit trails across financial transactions. For AP teams, this extends to vendor bill creation, edits, approvals, payments, and even views of sensitive data. Your software must prevent anyone from disabling these logs, and your organization must retain them for the prescribed period, typically eight years.

AP is collaborative by design, which means multiple roles, many touchpoints, and more compliance risk if actions are not tracked comprehensively. Each step should be auditable, from data entry to CFO sign off, with consistent timestamps and version history that cannot be overridden.

Think of audit trails as a permanent security camera on your books, always on, never tampered with, and ready to replay the complete story of any transaction.

For a quick policy context, refer to this helpful explainer on India mandates audit trail compliance.

Essential Components of AP Audit Trail Documentation

Build your AP evidence so it answers four questions instantly, who acted, what changed, when it happened, and why it was necessary. Auditors expect to see a consistent pattern across all AP transactions.

- User identity, user ID, role, and where possible, IP or device metadata for high risk actions.

- Time context, system timestamp of action, business date on document, and any approval date differences.

- Value history, old value, new value, field level change log, and version snapshots at each approval step.

- Reason and reference, mandatory reason codes, narrative notes for exceptions, links to POs, GRNs, contracts, and email or memo artifacts.

- GST context, link invoice to GSTR 2B reconciliation results, discrepancy notes, credit reversals, and approvals.

- Retention and integrity, evidence that logs cannot be disabled or deleted, backed by periodic backups and access controls.

For perspective on what auditors look for, review this note on auditors’ reporting for audit trail.

Setting Up Compliant Invoice Approval Workflows

Start with a clear, written Delegation of Authority matrix. For example, invoices under ₹10,000 require one approver, ₹10,000 to ₹50,000 need two approvers, above ₹50,000 require CFO sign off. Configure this in your system so rules are enforced automatically.

- Capture the invoice version approved at each stage, a later edit must not alter what was originally approved.

- Enforce maker-checker controls, the entry user cannot approve the same invoice, and system rules must block conflicts.

- Handle delegation with clarity, when approvers are on leave, log the delegated authority and duration, then restore normal routing after return.

- Use standing approval templates for recurring bills, while ensuring each payment still creates a fresh approval and payment log.

- Import email approvals into your system with attachments and timestamps, mobile approvals should record device or session metadata.

Approvals that live only in inboxes do not satisfy AP audit evidence, the system of record must contain the official trail.

Managing Vendor Master Data Changes and Audit Evidence

Vendor master governance is central to fraud prevention. Treat additions, bank changes, and GSTIN updates as controlled changes, not casual edits.

- Vendor onboarding, capture KYC verification steps, documents reviewed, and independent approval before activation.

- Bank account changes, require a two step process, requester uploads proofs, verifier independently confirms, approver signs off, with a full timestamped trail.

- GSTIN updates, record old and new GSTIN, reason, and auto flag open invoices for review to protect input credit claims.

- Periodic reviews, circulate change logs, who changed what and when, to detect anomalies early.

- Deactivation or blacklisting, document reason, approving authority, and outstanding payables status at the point of action.

For baseline context, see this concise audit trail overview.

Best Practices for Payment Processing Documentation

Payments are the moment of risk, so your trail must be airtight from invoice to bank statement.

- Payment initiation, log the batch creator, included invoices, payment schedule adherence, and reasons for any exceptions.

- Bank references, store NEFT or RTGS or IMPS identifiers and map them to individual invoices for one click traceability.

- Two person verification, after initiation, a verifier cross checks amounts, beneficiaries, and approvals, recording discrepancies and resolutions.

- Partial and advance payments, document rationale, dispute notes, quality holds, and later adjustments to close the loop.

- Reversals or cancellations, capture reason, authorizer, and follow up actions, whether reprocessed or method switched.

- Bulk runs, maintain invoice level detail even when paying hundreds together, do not sacrifice granularity.

- FX payments, record rate source, applied rate, and approvals for large variances, post gain or loss entries with references.

Implementing Technology Solutions for AP Audit Compliance

Manual logging does not scale, automation is your ally. Evaluate whether your accounting platform can prevent audit log deletion, capture field level changes, and produce auditor friendly reports.

- AI Accountant, automated, field level audit trails across invoice capture, approvals, and payments, with Tally and Zoho Books integrations and exportable evidence packs.

- QuickBooks, built in change logs and audit trail reports, Indian specific controls may need configuration.

- Xero, activity tracking with cloud backups, supports user action history and retention.

- Zoho Books, audit trails with GST aligned features, useful for Indian SMBs and mid market teams.

- FreshBooks, basic logs for small teams, workflows may require add ons for complex approvals.

- Enable role based access, log attempted violations, and minimize super user privileges.

- Automate three way matching, PO, invoice, and receipt, to generate evidence without extra work.

- Use real time alerts for high risk actions, vendor bank changes or edits on paid invoices.

- Prefer cloud backups for long term retention, disaster recovery, and scalability.

- Track bank and GST integrations through APIs, so cross system actions are auditable end to end.

Training Your Team on Audit Trail Compliance Procedures

People complete the control environment. Teach the why, then the how, reinforce with scenarios, and keep it practical.

- Explain that strong logs protect the company and protect honest employees during disputes.

- Share visual guides for common tasks, including which fields are mandatory and how notes translate into the audit log.

- Role play exceptions, for example, a vendor bank change request or an urgent out of cycle payment, and show correct documentation.

- Onboard new hires with audit trail essentials from day one, then schedule refreshers after system updates.

- Publish compliance metrics, completion rates, exception counts, and celebrate steady improvement.

When teams see audit trails as a shield, not a spotlight, adherence becomes habit and quality rises.

Common AP Audit Trail Mistakes and How to Avoid Them

- Mistake 1, Backdating entries, use current system dates, log original invoice date separately, and note reasons for delays.

- Mistake 2, Shared user IDs, issue unique credentials to preserve accountability, even for temps.

- Mistake 3, Offline approvals, move to mobile or in app approvals, import legacy email approvals with attachments and time context.

- Mistake 4, Bulk deletions, reverse or adjust, do not delete, maintain the full correction trail.

- Mistake 5, Inconsistent notes, standardize reason codes and mandatory fields to reduce ambiguity.

- Mistake 6, Ignoring system timestamps, business dates matter, system timestamps matter more for actual action time.

- Mistake 7, Poor exception documentation, use quick templates for urgent cases to keep evidence complete.

- Mistake 8, Vendor verification gaps, enforce KYC checklists and dual verification on critical fields.

Preparing for Statutory Audits, AP Documentation Checklist

Be ready with evidence packs, user access proofs, and exception narratives before auditors walk in. For a structured approach, see this guide to audit readiness and evidence pack.

- Run completeness reports on audit logs for the period, fix gaps and document remediation.

- Provide AP policy documents and show how configurations enforce them in your system.

- Share user access histories, role changes, and approvals for privilege escalations.

- Produce DoA matrices, then cross reference to workflow settings.

- Prepare samples across vendor onboarding, invoice edits, payment runs, reversals, and advances, each with full trails.

- Compile exception registers, urgent payments, hierarchy overrides, and high value approvals, with supporting evidence.

- GSTR 2B reconciliation logs, show discrepancy handling, credit reversals, and approvals.

- Vendor master change reports, before and after snapshots, and review meeting notes.

- Payment batch maker and checker evidence, bank confirmations, and reconciliation trails.

- Assign a response team, rehearse navigation of logs, and keep prior year remediation evidence handy.

Measuring and Monitoring AP Audit Trail Effectiveness

Compliance is continuous. Define clear KPIs, schedule reviews, and keep improving with each cycle.

- Completeness rate, percentage of AP transactions with full logs and notes.

- Timeliness, lag between decision and in system approval, large gaps signal offline behavior.

- User adherence, track users who consistently miss notes or reason codes, coach with targeted refreshers.

- Exception ratio, if exceptions rise, your standard process needs an update, not just more notes.

- Monthly spot checks, random pulls must tell the story without extra context.

- Quarterly access reviews, prune inactive users and remove leavers immediately.

- Semi annual process walkthroughs, test if a neutral reviewer can understand a transaction using only logs.

- Regulatory watch, update configurations as MCA and GST norms evolve, adopt new features that enhance traceability.

Conclusion

AP audit trail compliance in India is a mandate, and a strategic safeguard. Document actions comprehensively, automate wherever possible, train your team, and monitor relentlessly. The gains are tangible, faster audits, fewer penalties, reduced fraud risk, and stronger trust in your numbers. Whether you process ten invoices or ten thousand, the winning formula remains the same, complete evidence, controlled workflows, and continuous improvement, turning compliance into a durable advantage.

FAQ

How do I evidence that audit trails cannot be disabled in my AP system for MCA compliance?

Export a system configuration report that shows audit logging is mandatory, include screenshots of settings where applicable, add vendor documentation that states logs are immutable, and demonstrate a sample change log for an invoice edit. Tools like AI Accountant show a permanent toggle in the on state with no user override, plus field level histories to prove immutability.

What exact fields should my AP audit trail capture to satisfy a statutory auditor?

Capture user ID, role, timestamp, action type, old and new values at field level, document linkages like PO or GRN, approval step identity and version snapshot, IP or device info for high risk actions, and a reason code with narrative where exceptions occur. AI Accountant populates these automatically during data entry, approval, and payment posting.

How can I implement maker checker in a small finance team where resources are tight?

Split duties by workflow, for example, AP executive creates bills, accountant validates and tags, finance manager approves, and a separate user runs payments. Enforce this in software rules so conflicts are blocked. If headcount is minimal, assign part time reviewers with restricted roles and use AI Accountant to auto block self approval and log any attempted violations.

What documentation do auditors expect for vendor bank account changes?

Auditors want the requestor identity, supporting proofs like a signed letter and canceled cheque, independent verification evidence, approver identity, timestamps for each step, and before or after bank details snapshots. The change should sync to subsequent payments, creating a complete chain. AI Accountant’s change request workflow generates this evidence with one export.

How should I document partial payments or short settlements on vendor invoices?

Record the reason code, quality hold, disputed quantity, pricing variance, or SLA penalty, attach or reference the approval, and show the residual balance. When the issue is resolved, link the closing entry to the original short pay record. A good system will expose this as a single narrative across entries, AI Accountant does this natively.

Is email based approval acceptable for AP if we store the emails?

Only if the approval is imported into the accounting system with the email artifact, approver identity, and timestamp. Pure inbox evidence is weak. Use in app or mobile approvals that write directly to the audit trail. As a fallback, import emails into AI Accountant so the approval lives with the invoice version that was approved.

What KPIs should I track monthly to prove strong AP audit trail hygiene?

Track audit completeness rate, documentation timeliness, exception ratio, user adherence to reason codes, vendor master change count with approvals, and closure time for discrepancies. AI Accountant’s dashboard surfaces these KPIs and flags outliers in real time.

How do I reconcile GSTR 2B with AP and preserve the evidence for audits?

Perform a periodic 2B match, record matched status, discrepancies, credit blocks, and reversals with approver notes, then attach vendor communications. Keep the reconciliation report and change logs for eight years. AI Accountant links invoice records to reconciliation outcomes, creating traceability from bill to GST credit.

What is the right way to correct a wrong AP entry without breaking the audit trail?

Never delete, post an adjustment or reversal with a clear reason, then rebook correctly. The trail must show the original, the correction, and the final, with timestamps and users at each step. Systems like AI Accountant guide users through compliant reversal flows and prevent destructive edits.

How do I show that approvals were based on the exact version of the invoice presented at the time?

Use versioned approvals where each approval stores a snapshot of the invoice fields as seen by the approver. Later edits must create a new version and, if necessary, trigger reapproval. AI Accountant preserves versioned approvals by default, which auditors can verify quickly.

What evidence is needed for payment runs to prove segregation of duties and control?

Provide the batch creation log, included invoices with approvals, the verifier’s checklist and sign off, bank reference IDs, and post payment reconciliation entries. Show that the initiator and verifier are different users, and that exceptions were approved. AI Accountant produces a payment packet with all linked artifacts.

How should I prepare an AP evidence pack before the statutory audit begins?

Compile policy documents and DoA, user access and role change logs, vendor master change reports, invoice modification samples, payment run packets, GSTR 2B reconciliation logs, and exception registers. Run a completeness scan to fix gaps proactively. AI Accountant’s audit readiness export creates this evidence pack in minutes.