-01%201.svg)

Key takeaways

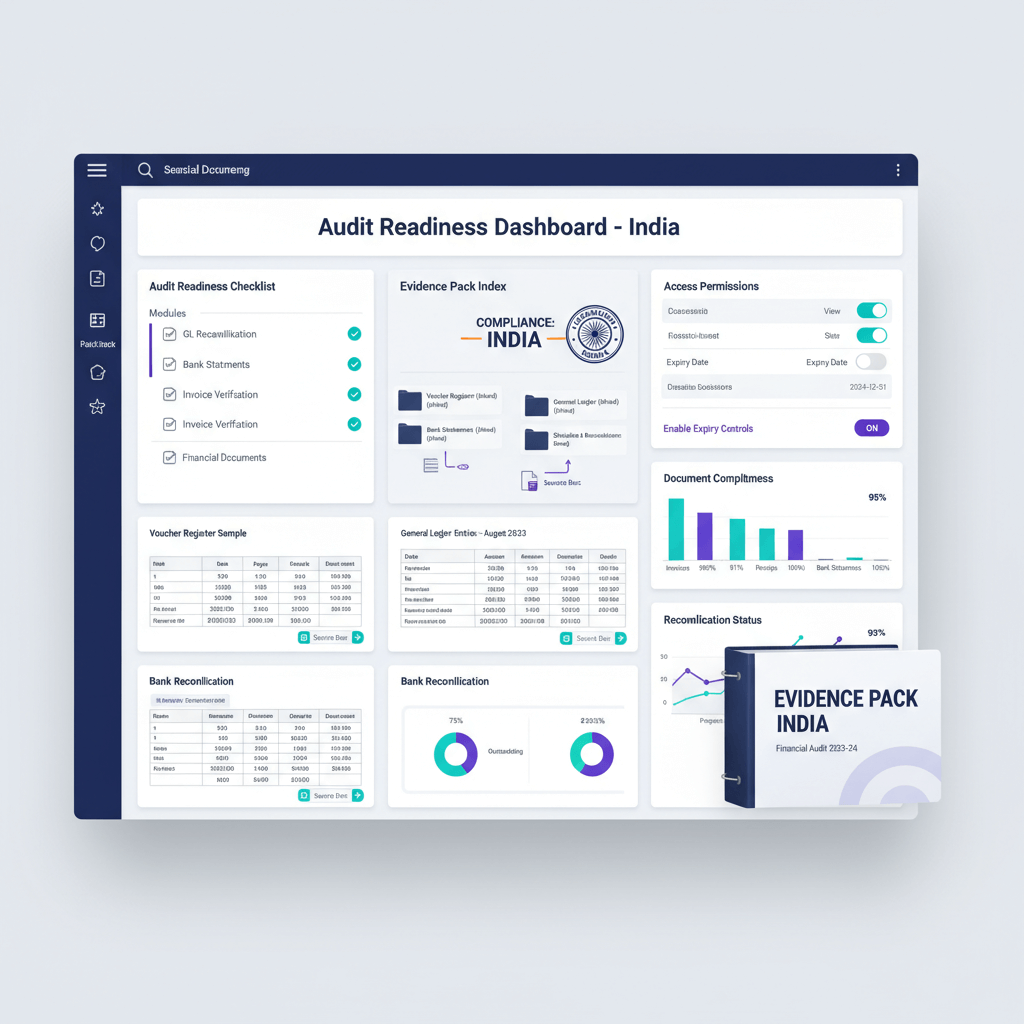

- Audit readiness in India means delivering a complete, cross referenced audit pack with vouchers tied to ledgers, reconciled schedules linked to trial balance, and a secure data room for auditor access, all prepared at least 90 days before audit week.

- Your audit pack must prove completeness, existence, accuracy, cut off, rights, and obligations, mapped to Ind AS or AS, GST, and TDS requirements, including GSTR-2B matches, 26AS proofs, and e-invoice IRNs.

- Monthly reconciliations of bank BRS, GSTR-2B to purchases, GSTR-1 to sales, and 26AS to TDS ledgers catch mismatches early and prevent last minute firefighting during audit season.

- A well structured folder system with systematic voucher numbering, predictable file names, and tested hyperlinks lets you answer any auditor query in seconds rather than hours.

- Secure, read only auditor access with role based controls, link expiry set to 30 days post audit, and encrypted backups protects sensitive data while meeting Companies Act and GST retention requirements.

- Automating repetitive audit prep tasks like voucher compilation, ledger code prediction, document linking, and schedule generation can cut preparation time substantially. AI Accountant's bookkeeping automation handles these workflows so your team focuses on analysis and decisions.

Audit Readiness India: What's New in 2026

The 2025 to 2026 transition brought several changes that directly affect how CA firms and finance teams prepare audit packs. Until March 2025, GST e-invoicing applied to businesses with turnover above ₹5 crore. From April 2025, the threshold dropped to ₹1 crore under CBIC Notification No. 17/2025, pulling a much larger pool of SMEs into mandatory e-invoicing. If you are a CA firm managing multiple clients on Tally, this means more IRN generation, more e-invoice validation steps, and more data points to reconcile during audit.

On the income tax side, the updated Form 26AS now includes high value transaction reporting under the Statement of Financial Transactions (SFT). Auditors in 2026 are cross verifying SFT entries against your books, not just TDS credits. Missing or mismatched SFT items will raise red flags during Section 44AB tax audits. The Income Tax Department portal now surfaces these details more prominently, so quarterly downloads and verification are essential.

The operational shift is clear. Monthly reconciliation is no longer optional for businesses above ₹1 crore turnover. Your workflow now includes validating IRNs on every invoice, matching SFT data to ledger entries, and ensuring GSTR-2B reconciliation covers the expanded supplier base. Firms that skip this face blocked ITC claims, penalty notices under Section 122 of the CGST Act, and delayed audit sign offs.

What to do now:

- Verify all clients above ₹1 crore are generating e-invoices correctly. Audit existing invoices for missing IRNs before the auditor does.

- Download and reconcile Form 26AS with SFT data quarterly, not just at year end.

- Automate GSTR-2B matching and vendor invoice reconciliation to handle the increased volume. Platforms offering automated GST reconciliation make this manageable without adding headcount.

What "Audit Readiness India" Really Means

Indian audit readiness is more than clean books. It is a complete audit pack with vouchers tied to ledgers, reconciled schedules linked to trial balance and financial statements, and a secure data room for auditor access.

Auditors evaluate completeness, existence, accuracy, cut off, rights, and obligations, mapped to Ind AS or AS, GST, and TDS. You will be asked for perfect GSTR-2B matches, 26AS TDS proofs, and e-invoice IRNs. Cash expenses over statutory limits, or unapproved vouchers, will be flagged quickly.

Think of audit readiness as a system, not a checklist. When every transaction has a source document, every ledger entry has a cross reference, and every schedule ties to the trial balance, the audit becomes a verification exercise rather than a discovery exercise.

Pro tip: Start audit prep 90 days early. This separates smooth sign offs from last minute firefighting. The ICAI guidance on audit documentation reinforces this timeline for statutory audits under the Companies Act.

How to Compile Vouchers and Ledgers Like a Pro

Begin by gathering every source document: purchase bills, sales invoices, expense receipts, bank statements, and credit card statements. Ensure vendor or customer masters carry GSTIN or PAN for every party. No exceptions.

Step 1: Number Everything Systematically

Adopt clear sequences. Use PV-2026-001 for payment vouchers, SV-2026-001 for sales vouchers. Record approvals for each transaction so you can trace any payment when questioned months later.

Consistent voucher numbering is the backbone of a reliable audit trail. Without it, auditors spend time hunting for documents instead of verifying them.

Step 2: Export and Verify Your Ledgers

Export ledgers from Tally, then verify opening and closing balances tie to the trial balance. This is a simple check that prevents major downstream reconciliation pain.

Pay special attention to ledger entries that span multiple accounting periods. These are common sources of cut off errors that auditors flag.

Step 3: Fix the Gaps Now, Not Later

Identify missing bills, remove duplicates, reclassify misposted expenses, and correct GST codes. Do this while you have time, not when the audit clock is running.

Common gaps include vendor invoices without matching purchase orders, expense entries lacking supporting receipts, and journal entries without narration. Fix them proactively.

The Perfect Folder Structure

Use a predictable, scannable structure so retrieval is instant during audit queries.

AuditPack_2026/

├── Vouchers/

│ ├── Purchases/PV-2026-001_BillNo_ABC.pdf

│ ├── Sales/SV-2026-001_InvNo_XYZ.pdf

│ └── Expenses/EXP-2026-001_Receipt_UPIREF.pdf

├── Ledgers/

│ └── TallyExport_Jan-Dec2026.xlsx

└── Masters/

└── VendorMaster_GSTIN.xlsx

Name files as [Type]-[YYYY]-[Seq]_[Ref].pdf. Any auditor request can be answered in seconds with this naming convention.

Creating Bulletproof Cross Links to Source Documents

Every ledger entry needs clear cross links to source. This proves existence and accuracy to auditors and forms the backbone of your audit evidence.

Step 1: Build Your Cross Reference Register

Include these columns: Ledger Entry ID, Voucher Number, Document ID, Link Path, and UTR or IRN. This becomes your master map that auditors use to navigate the entire audit pack.

Step 2: Set Up Your Digital Data Room

Store artefacts in read only rooms using Google Drive, OneDrive, or Box. Use hyperlinks rather than embedded files. This keeps the pack light and accessible.

A well organized digital data room reduces back and forth with auditors by 50% or more. When they can self serve documents through clear links, queries resolve faster.

Step 3: Attach the Must Haves

TDS certificates, GSTR-2B proofs, e-invoice QR codes, purchase orders, and contracts must be attached for every entry. These are the supporting artefacts that auditors check first.

Sample Cross Reference Index

Ledger EntryVoucher NoDoc IDLinkSupporting ArtefactSundry Creditors, ABCPV-2026-001Bill-ABC123/Vouchers/PV-2026-001.pdfGSTR-2B Match, IRN

Test for broken or inaccessible links and non standard names. Fix these before sharing with auditors. A single broken link can stall an entire audit query thread.

Building Schedules and Reconciliations That Actually Work

Your schedules and reconciliations tell the story behind numbers. Build them thoroughly so auditors can verify without guessing.

The Essential Schedules

- Fixed asset register and depreciation schedules

- Receivables and payables ageing analysis (0 to 30, 30 to 60, 60+ day buckets)

- Loans and advances, provisions, accruals

- GST payable or ITC, TDS or TCS

Critical Reconciliations You Cannot Skip

- Bank BRS monthly with sign offs

- GSTR-2B matched to purchase register

- GSTR-1 aligned to sales ledger

- 26AS verified against TDS ledger, including SFT entries for 2026

- Vendor statement reconciliation performed regularly

Cut off Testing Matters

Focus on revenue and expense cut off at financial year end. Handle post year entries correctly and document FX or rounding differences.

Sample invoices issued in the last 7 days of March and the first 7 days of April. Verify that revenue recognition follows the correct period. This is one of the most common audit adjustments.

The Sign off Flow

Preparer creates, Reviewer checks, Approver signs. Ensure each schedule ties to trial balance and financial statements. No schedule should exist without this three step sign off.

Your Reconciliation Coverage Checklist

- Bank reconciliations: monthly, with signatures

- GST reconciliations: 2B and 1 matched to books

- TDS reconciliations: 26AS aligned perfectly, including SFT cross checks

- Ageing analysis: 0 to 30, 30 to 60, 60+ day buckets

- Inter company reconciliations (if applicable): balances confirmed quarterly

Pre sign off verification eliminates gaps. Run the checklist before the auditor does.

Setting Up Secure Access for Auditors

Create proper access for auditors via a secure audit data room. Use least privilege, read only permissions. Never share login credentials directly.

Role Based Access Control

Define roles clearly. Auditors get view and download only. Preparers upload. Approvers handle sign offs. Document the access matrix and share it as a one page reference.

Establish Clear Protocols

Publish a request list upfront. Set 24 to 48 hour SLAs for document delivery. Version control files as v1.0_2026-01-02. Keep naming consistent across all documents.

A well published protocol note builds trust. It tells auditors exactly how to access documents, who to contact for queries, and what response times to expect.

Handle Sensitive Information Properly

Mask PAN or Aadhaar before sharing. Log all access activity. Maintain a Q and A trail. Share via invitation only links.

Publish a one page note on roles and access to build trust with the audit team. This small step prevents most access related delays during audit week.

Implementing Smart Expiry Controls

Time bound expiry controls protect data after audits end. This is essential for governance and regulatory compliance.

Set Clear Expiration Dates

Configure links to expire 30 days post audit completion. This balances auditor access with long term data protection.

Maintain Revocation Trails

Track who accessed what, when, and how often. Create logs, review patterns, and investigate anomalies when required.

Post Audit Cleanup Process

Revoke access systematically after sign off. Retain documents per the Companies Act, 2013 requirement of 8 years. Note the GST document retention requirement of 72 months under Section 36 of the CGST Act.

Backup Strategy

Maintain encrypted backups. Test restores periodically. Document each review cycle and store backup verification logs.

Your India Specific Audit Pack Readiness Checklist

Use this checklist to track completion for audit readiness India.

Document Preparation

- Compile vouchers and ledgers: completed and indexed

- Tally exports tied to trial balance

- Supporting documents gathered and organized

- Vendor and customer masters verified with GSTIN or PAN

Linking and Verification

- Cross links to source verified and tested

- All hyperlinks live and accessible

- Master register fully updated

- Broken links identified and fixed

Reconciliation Completion

- Schedules and reconciliations prepared and signed off

- Bank reconciliation statements completed monthly

- GSTR matching completed (2B to purchases, 1 to sales)

- 26AS verification done, including SFT entries

Access Management

- Access for auditors configured with read only permissions

- Read only data room established

- Roles documented in access matrix

- Protocol note published for auditor team

Security Measures

- Expiry controls set for shared links

- Links expire 30 days post audit

- Revocation procedures documented

- Encrypted backups tested and verified

Common Pitfalls and How to Dodge Them

GST Mismatches Between 2B and Books

Run monthly reconciliations so differences are resolved early. With the expanded e-invoicing mandate covering businesses above ₹1 crore, the volume of mismatches has increased. Catch them monthly, not annually.

Missing TDS Certificates

Automate TRACES downloads quarterly. This removes March panic and ensures 26AS alignment well before audit season.

Unsupported Cash Expenses

Keep cash transactions under ₹10,000 per transaction to avoid disallowances. Insist on vouchers always. Prefer UPI or bank transfers for any amount that approaches the limit.

Unlinked Entries and Outdated Masters

Schedule weekly ledger scans. Update vendor and customer masters monthly. Outdated GSTIN data causes cascading reconciliation failures.

Uncontrolled Document Links

Apply expiry controls to every shared document for sustained security. An open link from a previous audit cycle is a governance risk waiting to happen.

Tools That Make Audit Preparation Less Painful

Essential Accounting Automation Tools

- AI Accountant: automates voucher compilation from Tally, predicts ledger codes, builds audit ready dashboards, and handles GSTR-2B reconciliation at scale

- QuickBooks: comprehensive bookkeeping with audit trails

- Xero: cloud accounting with strong reconciliation capabilities

- FreshBooks: user friendly expense tracking and invoicing

- Tally Prime: widely used in India with robust statutory compliance features

How Automation Helps with Audit Readiness

Compile vouchers and ledgers becomes automated via imports, predictions, and structured organization. What used to take days of manual data entry now happens in hours.

Cross links to source are created automatically when bills and UTRs match, reducing manual effort and human error in the linking process.

Schedules and reconciliations are generated via dashboards, including ageing, cash flow, and variance views. These update in real time as new transactions flow in.

Bi directional sync keeps books live, enabling seamless access for auditors. Expiry controls safeguard access windows. The net result is substantially reduced audit prep time and fewer last minute surprises.

The Timeline That Actually Works

90 Days Before: Foundation Phase

Gather source documents. Set folder structure. Start voucher numbering. Update vendor and customer masters with current GSTIN and PAN details.

60 Days Before: Building Phase

Complete cross reference register. Run reconciliations for available months. Fix gaps in documentation. Start building schedules for material balances.

30 Days Before: Verification Phase

Test all links for accessibility. Finish remaining reconciliations. Obtain preparer, reviewer, and approver sign offs. Configure audit data room access.

15 Days Before: Final Prep

Run the complete checklist. Brief team on auditor interaction protocols. Set expiry controls on all shared links. Publish the audit pack index.

Audit Week: Execution Phase

Share access credentials through the secure data room. Maintain fast responses within SLA timelines. Document every query and answer. Keep audit trails updated in real time.

Making It Through Your First Audit

Prioritize fundamentals. Vouchers first, ledgers second, then systematic cross references.

Start schedules with material balances. Perfect those, then move to smaller accounts. Do not try to build everything at once.

For access, keep it simple early on. A well organized Drive with clear names beats an unmanageable complex system. You can always upgrade your data room setup for the next audit cycle.

Implement expiry controls from day one for predictable security. This habit compounds over time.

Beyond Compliance: Building a Culture of Readiness

Monthly Disciplines

- Close books monthly, do not defer closings to quarter end

- Reconcile bank statements within five days of month end

- Review and approve journal entries monthly

- Maintain fixed asset register with every addition or disposal

Quarterly Reviews

- Run mini audits on high risk areas

- Review reconciliation processes for efficiency

- Update documentation standards based on recent queries

- Train team members on audit requirements and new regulations

Annual Improvements

- Document lessons learned from each audit cycle

- Incorporate auditor feedback into process design

- Invest in better tools and training

- Build institutional knowledge so readiness survives team changes

The Hidden Costs of Poor Audit Readiness

Poor preparation leads to penalties, interest, extended audit fees, lost focus on growth, and strained auditor relationships.

Hidden costs include team burnout, attrition, and reputational damage with lenders or investors. When your team spends weeks scrambling for documents, they are not working on business advisory, tax planning, or client relationships.

Good readiness avoids these costs. It delivers smoother operations, better morale, and faster audit completion. The ROI of proper preparation is measured not just in fees saved, but in capacity freed up for higher value work.

Special Considerations for Different Audit Types

Statutory Audit Under Companies Act

Focus on board resolutions, related party transactions, internal controls, secretarial records, and detailed notes to accounts. The Companies Act, 2013 specifies documentation requirements that auditors must verify.

Tax Audit Under Section 44AB

Emphasize cash transactions, disallowed expenses, and capital gains computations. Prepare Form 3CD details early. Document all assumptions behind each disclosure.

With the updated 26AS now including SFT data, auditors will cross verify high value transactions more rigorously in 2026.

GST Audit

Perfect GSTR reconciliations. Document ITC reversals with clear reasoning. Prepare state wise turnover breakups. Maintain e-way bill registers with dispatch and delivery details.

Internal Audit

Strengthen process documentation, control testing, compliance tracking, and statutory registers. Record deviations and corrections with timestamps and responsible parties.

When Things Go Wrong: Damage Control Strategies

Missing Documents

Be transparent with your auditor. Offer alternative evidence like bank statements, email confirmations, or supplier acknowledgements. File FIRs if documents are genuinely lost. Never recreate documents from memory.

Reconciliation Differences

Quantify the impact immediately. Explain variances clearly by classifying them as timing, classification, or data entry issues. Propose fixes with timelines. Document everything.

System Access Issues

Maintain backup access methods. Keep PDF exports of critical reports ready. Have admin contacts on hand. Use proper access management instead of sharing passwords.

Auditor Disputes

Stay professional. Document disagreements clearly. Escalate appropriately through the engagement partner. Seek second opinions when needed, and focus on resolution rather than blame.

Conclusion: Your Audit Success Roadmap

Audit readiness in India is about robust processes, not last minute sprints. Systematically compile vouchers and ledgers, create cross links to source, build schedules and reconciliations, configure secure access for auditors, and apply expiry controls.

Use automation wisely. Let tools like AI Accountant handle repetitive workflows while your team focuses on analysis and decisions.

Consistency wins. Daily practices, monthly closes, quarterly reviews, and continuous improvements will turn audit season into a smooth routine. The best time to start was three months ago. The next best time is today.

FAQ

How should a CA compile vouchers for Section 44AB tax audit with evidence trails?

Start with a numbered sequence for each voucher type (PV-2026-001 for payments, SV-2026-001 for sales). Attach source documents like purchase bills, sales invoices, receipts, and UTRs to each voucher. Map vouchers to ledger entries via a cross reference register that includes Voucher No, Document ID, Link Path, and UTR or IRN. Store everything in a read only audit data room and test every hyperlink before sharing access with auditors.

What documentation satisfies existence and cut off assertions for revenue at financial year end?

Tie each revenue entry to the issued invoice, dispatch evidence, and e-invoice IRN where applicable. Align GSTR-1 with the sales ledger and ensure no post year invoices are recorded within the reporting period. Perform cut off testing by sampling invoices from the last 7 days of March and first 7 days of April, validating revenue recognition per Ind AS or AS.

How can I reconcile GSTR-2B and purchase register monthly?

Match supplier GSTINs, invoice numbers, taxable values, tax components, and ITC eligibility line by line. Flag exceptions like missing invoices in 2B, mismatched invoice numbers, credit notes not adjusted, and ineligible ITC categories. Document reconciliation comments for each exception and create an action plan to fix or defer ITC claims, then sign off monthly. With the e-invoicing threshold now at ₹1 crore (2026 update), the volume of supplier invoices requiring 2B matching has increased significantly.

What is the ideal folder structure for audit packs?

Use AuditPack_YYYY as the root folder with Vouchers, Ledgers, and Masters as sub folders. Name files as [Type]-[YYYY]-[Seq]_[Ref].pdf, for example SV-2026-001_InvNo_XYZ.pdf. Keep supporting artefacts like TDS certificates and IRNs alongside related vouchers, and maintain a cross reference register linking ledger entries to file paths.

What access controls should I set for external auditors?

Provide read only, least privilege access via invitation only links to your audit data room. Set 24 to 48 hour SLAs for document requests, maintain version control, and mask PAN or Aadhaar before sharing any documents. Keep an access log and publish a one page protocol guide that defines roles for preparer, reviewer, and approver.

How do I implement link expiry controls after audit sign off?

Set link expiries to 30 days post audit completion, maintain logs of all link creation and usage, then revoke access systematically. Retain records per Companies Act (8 years minimum) and for GST (72 months under Section 36 of the CGST Act). Keep encrypted backups and test restores periodically to ensure document recoverability.

What is the minimum viable audit pack for a first time audit?

Deliver numbered vouchers with evidence, verified ledgers tied to trial balance, a cross reference register with tested links, core schedules (fixed assets, ageing, bank BRS for all months, GST, TDS), a secure data room with documented roles, and link expiry settings. Keep a simple index and a one page protocol note for the auditor team. Build on this foundation with automation as your processes mature.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.