-01%201.svg)

Key takeaways

- GSTR-2B is the anchor for compliant ITC, accurate reconciliation prevents cash leaks and notice risks.

- Great tools ingest 2B and purchase registers, normalize vendors, apply tolerance rules, and automate vendor follow-ups.

- Two-way gap analysis finds PR-not-in-2B and 2B-not-in-PR, reason codes and aging make follow-up actionable.

- An eligibility engine prevents blocked or premature ITC claims, optimises carry-forward, and boosts working capital.

- Dashboards give real-time visibility into eligible, ineligible, and deferred ITC, vendor risk, and audit readiness.

- AI-led platforms like AI Accountant deliver scale, accuracy, and ERP sync for CA firms and SMEs.

Why GSTR 2B reconciliation matters now

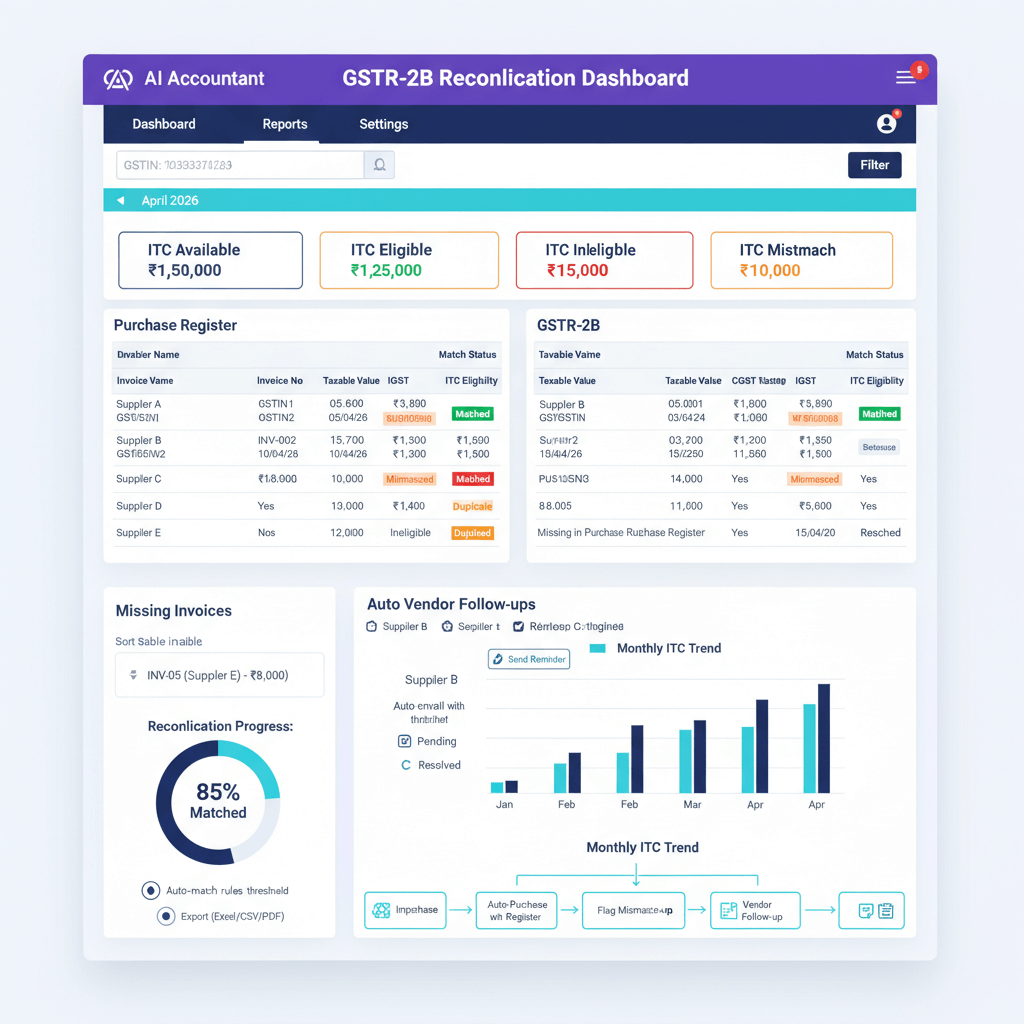

GSTR-2B is a monthly, static statement of inward supplies, it reflects suppliers’ GSTR-1 filings and defines what you can lawfully claim as ITC. Reconciliation matters because a bill must exist in both your purchase register and GSTR-2B, otherwise ITC gets delayed or denied. Every unreconciled invoice is either money left on the table, or a compliance risk waiting to surface.

Typical problem patterns include delayed amendments and credit notes, Reverse-charge mechanism (RCM) supplies excluded from 2B, SEZ or exempted supplies appearing differently, import IGST via ICEGATE requiring special mapping, and the 180-day payment rule affecting blocked or deferred credits.

What great GSTR 2B reconciliation tools should include

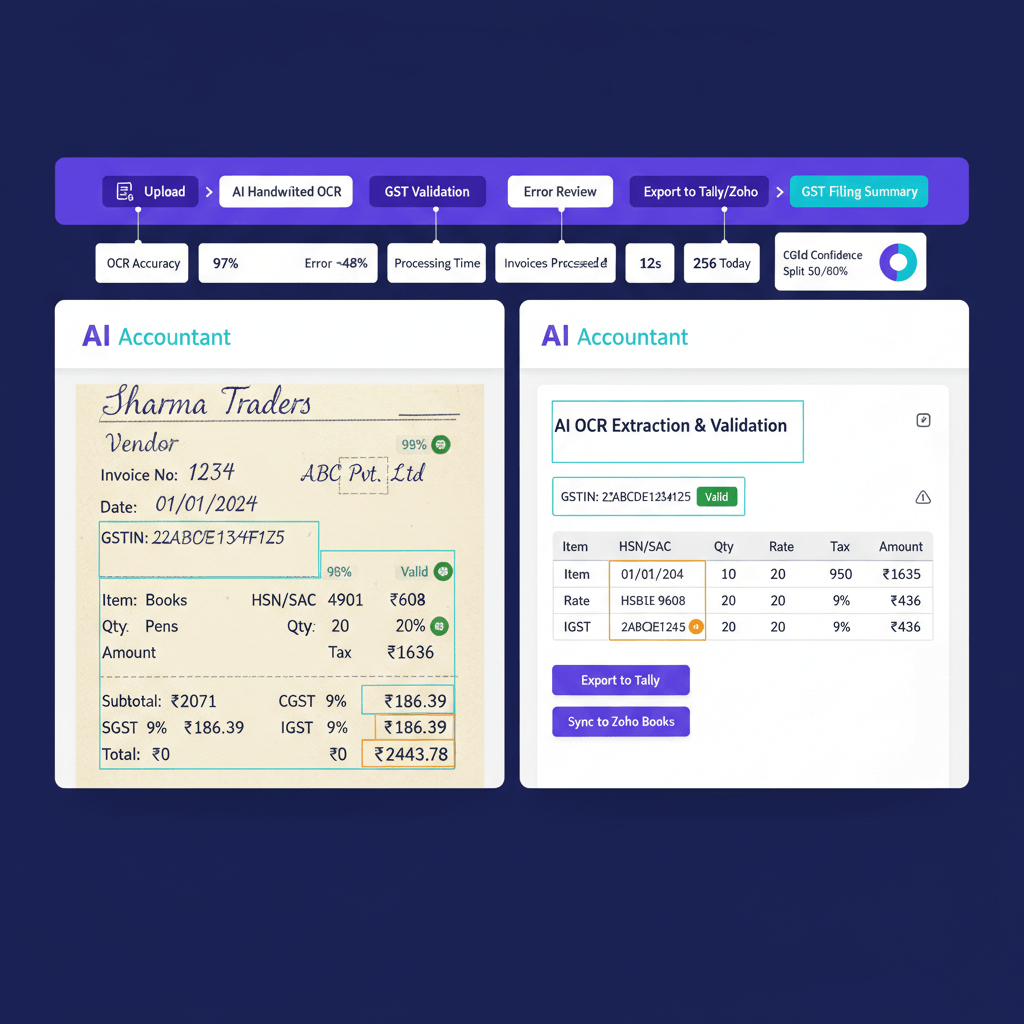

- Ingestion: Read 2B JSON or Excel, purchase registers, credit or debit notes, journal vouchers.

- Normalization: Clean GSTIN formats, standardize vendor names, normalize invoice numbers and prefixes.

- Tolerances: Configurable date variance, rounding, and amount thresholds to avoid false mismatches.

- Duplicate and partial-match detection: Prevent over-claims, catch data-entry errors.

- Missing invoice flags: PR-not-in-2B and 2B-not-in-PR mapped with reason codes for fast action.

- ITC eligibility engine: Auto-tag eligible, ineligible, deferred, and time-barred credits.

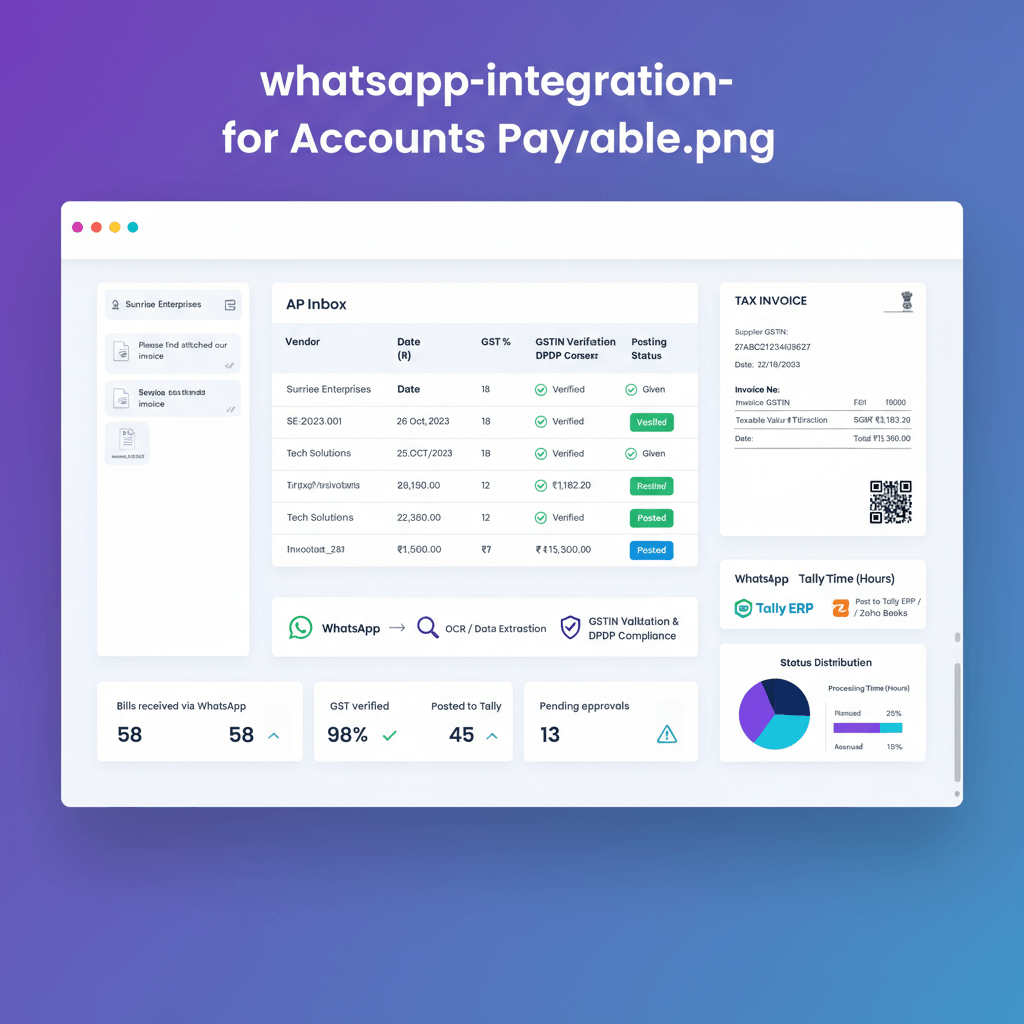

- Vendor follow-up automation: Bulk WhatsApp or email outreach, acknowledgements, and reminders.

- Monthly dashboard: Eligibility snapshot, deferred credits, vendor risk, trends, and drill-downs.

- Audit trail, maker-checker: Logged actions, approvals, and controlled corrections.

- ERP integration: Sync statuses back to Tally or Zoho Books to close the loop.

- Scale and security: 100K plus invoices monthly, ISO and SOC-2 controls, encrypted data.

- Support and templates: Pre-built validations, live onboarding, configurable rules.

Match purchase register at scale

Robust matching is the foundation, without it, everything else slips. Leading tools normalize vendor names and GSTINs, validate PAN-based deduplication, and clean invoice numbers so “INV 2026 001” matches “INV-2026-001.” Tolerance rules allow a couple of days’ date variance, small rounding differences, and minor amount differences to reflect reality without spurious flags.

Bulk exception handling runs through a maker-checker review, the system proposes, humans approve, and the engine learns. Duplicate detection protects against accidental double claims, and a persistent vendor master remembers that “ABC Pvt Ltd” equals “ABC Private Limited” next month.

Identify missing invoices fast

- PR-not-in-2B: Likely supplier non-filing or delayed GSTR-1, action is vendor follow-up and deferred ITC tagging.

- 2B-not-in-PR: Often unbooked bills, wrong vendor mapping, or duplicate suppression, action is GRN check and timely booking.

Reason codes like “Supplier Non-Filing,” “Unbooked,” “Possible Duplicate,” and “Amendment Pending” convert vague mismatches into task lists. Aging analysis surfaces 30, 45, and 60 plus day gaps, so teams tackle what is closest to becoming time-barred first. A visual workflow moves each gap from awaiting confirmation, to under review, to booked, to resolved.

ITC claim optimisation that stands up in audit

- Blocked credits under Section 17(5) get auto-flagged, including personal consumption, motor vehicles, food, fuel, and non-business use.

- RCM invoices are separated to prevent premature claims.

- 180-day payment rule: The 180-day payment rule defers ITC until paid, then re-credits automatically when conditions are met.

- Place of supply checks catch interstate POS mismatches and related exceptions.

- Time-bar checks prevent claims beyond 24 months from invoice date.

The engine computes eligible versus ineligible or deferred ITC, suggests partial claims for mixed invoices, and carries forward deferred credits. What-if simulations let you plan cash flow before month-end. When amendments or credit notes arrive, recalculations ensure neither under-claiming nor over-claiming persists.

Vendor follow-up automation that actually works

Automation turns chasing into a calm cadence. Vendors receive discrepancy sheets listing their invoice numbers, requested actions, and due dates via WhatsApp or email, responses and filing statuses are logged automatically. Escalation sequences nudge non-responders at set intervals. A vendor performance view highlights repeat offenders to inform procurement decisions and relationship management.

Monthly dashboard your CFO will open

A best-in-class monthly dashboard surfaces eligible ITC, ineligible and deferred amounts, missing invoice counts with aging, top at-risk vendors, and historical trends. Drill-downs go from tile to invoice in a click, audit readiness indicators confirm approvals and trails, and exports create tidy working papers. Real-time refresh means you spot leakage early, not at close.

Tool categories and trade-offs

- Spreadsheets with VLOOKUP: Free and flexible, yet error-prone, slow, and audit-light, fine for tiny volumes.

- GST portal downloads: Native and free, limited analytics and no automation, suited to low volumes.

- Accounting software add-ons: Close to the books, basic matching and follow-ups, limited optimisation rules.

- Dedicated 2B tools: Strong matching, vendor portals, and compliance features, separate data flows to manage.

- AI-led accounting platforms: End-to-end automation, scale, and ERP sync. Example: AI Accountant; also options from QuickBooks, Xero, FreshBooks, and Zoho Books.

Mid-market firms typically recover 1 to 3 percent more ITC, save 5 to 10 hours monthly, and reduce notice risk with dedicated or AI-led solutions.

Evaluation checklist: 15-point buyer framework

- Ingestion capabilities, real files tested.

- Vendor normalization and fuzzy accuracy, sample 100 invoices.

- Tolerance configurations, per client or org.

- Missing invoice detection, both PR-not-in-2B and 2B-not-in-PR with reason codes.

- ITC rule coverage, 17(5), RCM, 180-day, POS, time-bar.

- Vendor follow-ups, bulk sends, tracking, reminders.

- Dashboard depth, drill-downs and exports.

- ERP integration, push-back to Tally or Zoho Books.

- Audit trail and maker-checker, user and timestamp logs.

- Batch speed, 100K plus invoices without slowdown.

- Security, ISO and SOC-2, encryption.

- Multi-org support, role-based access.

- Onboarding and support, go-live speed and quality.

- Pricing and ROI clarity, payback within six months.

- India-specific edge cases, ISD, SEZ, e-invoice, amendments, imports.

Implementation guide: prep, pilot, rollout, and success metrics

Phase 1: Preparation, weeks 1 to 2

Collect six months of 2B files, purchase registers, notes, and JVs, clean vendor masters with GSTIN mapping, and document today’s ITC process with roles and approval steps. This reveals gaps before tooling begins.

Phase 2: Pilot, weeks 3 to 6

Run a parallel month, compare eligible ITC, check every flagged gap, measure hours saved, and tune tolerances. Bring auditors in early to validate trails and controls.

Phase 3: Rollout, weeks 7 to 12

Train power users, set follow-up cadences, finalize dashboard views, document approvals and retention, go live for one GSTIN, then expand after two stable cycles.

Phase 4: Measure success, month 3 to 6 onwards

Track close-time reduction, additional ITC recovery, notice reduction, vendor follow-up time saved, and audit readiness. Publish a monthly scorecard to sustain momentum.

How AI Accountant maps to your needs

Match Purchase Register via bulk ingestion, fuzzy matches, and duplicate or partial detection. Identify Missing Invoices with two-way gaps, reason codes, and workflow states. ITC Claim Optimisation through a rules engine, carry-forward, and simulations. Vendor Follow-Up Automation using WhatsApp or email, schedules, and escalations. Monthly Dashboard across entities, with drill-downs and exports. Integration that syncs to Tally and Zoho Books. Scale and Security backed by ISO and SOC-2. Firms report faster closes and higher compliant ITC recovery within weeks.

India-specific edge cases and best practices

- ISD credits allocated correctly across branches and categories.

- SEZ or exempt supplies flagged as ineligible to avoid accidental claims.

- Import IGST via ICEGATE reconciled to 2B with customs data mapping.

- Amendments and credit notes linked back to original invoices with smart matching.

- Composition vendors auto-excluded from ITC.

- E-invoice IRNs normalized alongside legacy invoice numbers.

- POS mismatches handled through precise rule checks.

Close the year with a complete audit pack, include reconciliation logs, approved exceptions, and section-wise ITC summaries. Review monthly, not just at filing, so issues never snowball.

Next steps

Map your pain points to the buyer checklist, shortlist two or three tools, and insist on a 20-minute demo with your real data. Pilot one GSTIN for four weeks, validate eligible ITC and hours saved, and compute ROI on time plus ITC recovered, then scale with confidence.

FAQ

How do I reconcile GSTR-2B with my purchase register without manual VLOOKUP, and what accuracy should I expect?

Use a reconciliation tool that normalizes vendor names and GSTINs, cleans invoice numbers, and applies date and amount tolerances. With fuzzy matching, maker-checker approvals, and learned mappings, CA firms typically achieve 95 percent plus auto-match accuracy within the first cycle. Platforms like AI Accountant deliver sub-minute processing for large datasets.

What tolerance settings do CAs usually configure for dates and values to minimize false mismatches?

Common starting points are two to three days for date variance, small paise rounding, and one to two percent for amount differences when partial shipments occur. Tune by client vertical, for instance, pharma may need tighter tolerances than construction. Validate on a 100-invoice sample before go-live.

How should RCM invoices be treated during GSTR-2B reconciliation and ITC claim?

RCM supplies generally do not populate in 2B for ITC in the usual manner, so the tool must tag them separately, prevent premature claims, and reclassify once payment and conditions are met. A rules engine, as in AI Accountant, isolates RCM flows so they never inflate eligible ITC.

What is the operational workflow for the 180-day payment rule, including reversal and re-credit?

At 180 days from invoice date, the engine defers ITC automatically and posts a reversal JV if integrated to books, then upon payment, it re-credits in the next cycle and updates the audit trail. Using an automated tracker avoids missed reversals and ensures timely re-credit without manual spreadsheets.

How do I handle 2B-not-in-PR invoices that appear after close, and avoid double booking?

First, verify GRN or receipt evidence, then book the invoice with correct vendor mapping. A duplicate detector should scan for same GSTIN, invoice number, and date variations to avoid double entries. Tools like AI Accountant keep a persistent vendor and invoice signature to suppress duplicates reliably.

What is the best approach to reconcile import IGST via ICEGATE with GSTR-2B?

Load ICEGATE data alongside 2B, map Bill of Entry numbers to the corresponding 2B entries, and use a dedicated import reconciliation view. The engine should flag missing or unmatched imports with reason codes like “Pending Supplier Declaration” or “Data Entry Variation,” then route for review.

How do auditors evaluate reconciliation quality, and what evidence should I retain?

Auditors look for completeness, accuracy, and controls. Provide a monthly dashboard snapshot, invoice-level match logs, maker-checker approvals, reversal or re-credit entries for 180-day cases, and communications with vendors for non-filing. An AI Accountant style audit trail satisfies these checkpoints efficiently.

What tool category fits a CA firm managing 50 plus GSTINs with high invoice volumes?

Dedicated or AI-led platforms are best, since they combine high-accuracy matching, automated vendor follow-ups, and multi-org dashboards. They cut manual hours per GSTIN and standardize controls across clients. Evaluate ingestion breadth, rule coverage, ERP sync, and security certifications.

How do I quantify ROI on a GSTR-2B reconciliation tool for client proposals?

Add monthly hours saved by the tax team, multiplied by blended hourly cost, plus incremental eligible ITC recovered, typically one to three percent, then include reduced notice management time. Most firms see payback within six months, AI Accountant users often report faster closes and tangible cash benefits.

Can an AI tool reliably detect duplicates across amended invoices, credit notes, and vendor naming variations?

Yes, with multi-key signatures, fuzzy name logic, normalized invoice numbers, and amendment linking, AI engines detect duplicates and partial overlaps with high precision. The system proposes merges or exclusions, and maker-checker approval finalizes decisions for a clean audit trail.

How does maker-checker work in practice for reconciliation exceptions?

The engine flags potential matches or exceptions, a preparer reviews and proposes actions, and a checker approves or rejects with reasons. All steps are timestamped, creating a defensible control environment. This is essential for CA firms managing multiple client entities.

What is the simplest path to integrate reconciliation outputs back to Tally or Zoho Books?

Choose a platform that maps vendors and ledger codes, then posts cleaned invoices, statuses, and JVs via native connectors or export-import templates. AI Accountant, for example, supports push-back to Tally and Zoho Books, reducing manual corrections and keeping books aligned with 2B outcomes.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.