Key takeaways

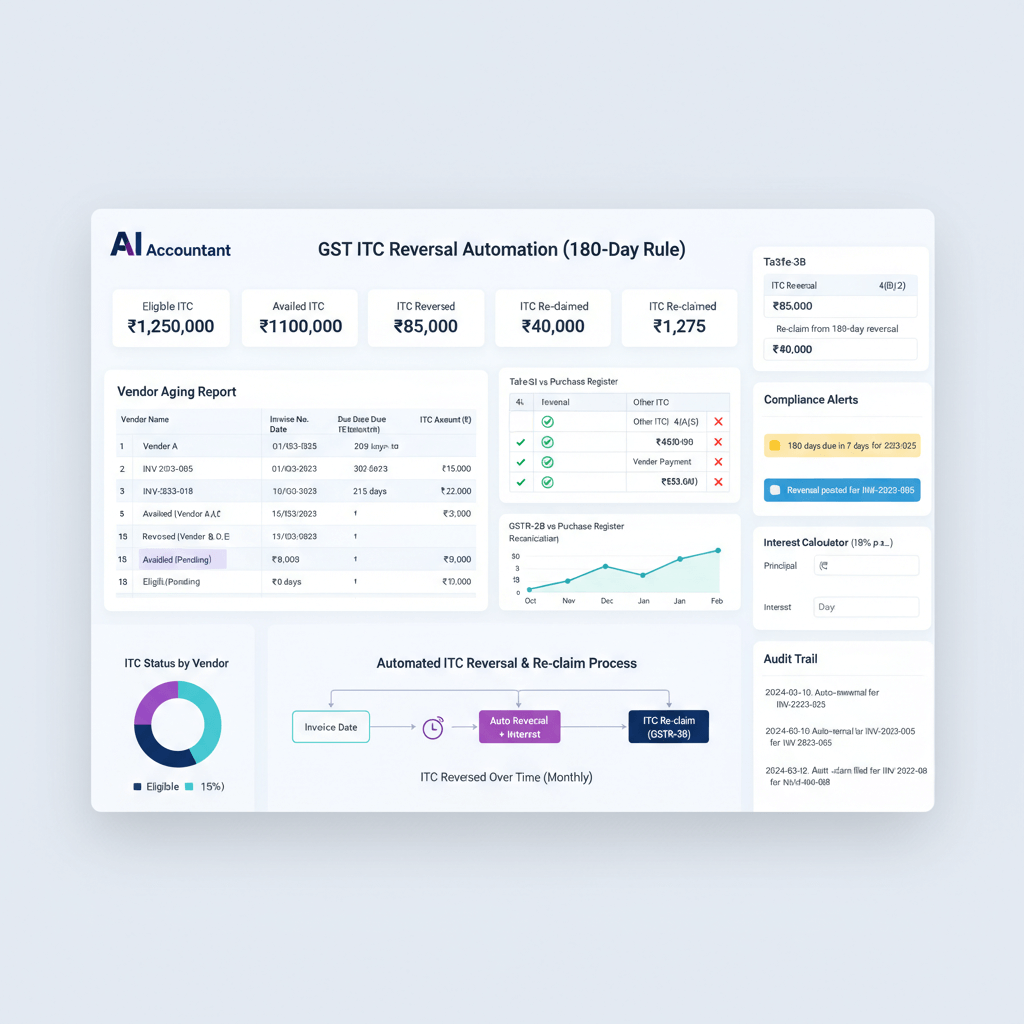

- The 180-day payment condition under Rule 37 is the primary trigger for ITC reversal in India: if you do not pay your supplier (invoice value plus tax) within 180 days, you must reverse ITC proportionately on the unpaid portion, plus 18% interest from the date of availment.

- Re-claim is allowed in the return period of actual payment, with no Section 16(4) time limit for re-availment, as long as you maintain payment proof and working papers.

- Supplier defaults under Rule 37A require reversal by November 30 if the supplier has not deposited tax by September 30 of the following financial year, even if you have paid them in full.

- Accurate reporting matters: use GSTR-3B Table 4(B)(2) for reversals and Table 4(A)(5) for re-claims, then reconcile annually in GSTR-9 Table 8.

- Proactive vendor-level controls (ageing dashboards, compliance scoring, payment tagging) prevent reversals and protect cash flow.

- Automation eliminates manual errors and missed deadlines. AI Accountant's GST reconciliation engine auto-flags 180-day breaches, computes proportionate reversals with interest, and nudges re-claims the moment payments clear.

ITC Reversal Rules India: What's New in 2026

The core mechanics of Rule 37 and Rule 37A remain stable heading into 2026, with no fresh CBIC notifications altering the 180-day threshold or the 18% interest rate. However, the operational environment has shifted meaningfully from 2025.

Until mid-2025, many CA firms handled Rule 37A reversals manually by checking GSTR-2B once a quarter. From FY 2025-26 onwards, the GST portal's improved GSTR-2B generation (with supplier-level filing status flags) means taxpayers are expected to identify non-compliant suppliers monthly and reverse ITC by the November 30 deadline without waiting for department notices. The CGST Rules on the CBIC tax repository continue to reflect this timeline.

Who does this hit hardest? CA firms managing 20+ clients and SME finance teams on Tally with 200+ vendor invoices per month. If you lack automated ageing alerts, you are likely missing reversals or over-reversing due to partial payment mismatches.

Cost of inaction: 18% interest accumulates from the ITC availment date (not day 181). On a ₹50,000 reversal missed for six months, that is roughly ₹4,500 in avoidable interest, plus potential show-cause notices during assessments.

What to do now:

- Run a full 180-day ageing scan on all open AP invoices before your next GSTR-3B filing.

- Cross-check GSTR-2B supplier filing status monthly, not quarterly, to preempt Rule 37A reversals due by November 30.

- Adopt automated vendor bill matching to link payments to invoices at source, eliminating manual re-claim tracking.

Body

Introduction

Picture this: you are reviewing last month's GST workings, and a few vendor invoices have quietly crossed the 180-day mark. Suddenly, that Input Tax Credit feels uncertain.

The good news? With a clear grip on ITC reversal rules India, you can turn anxiety into a controlled routine.

At its core, ITC lets registered taxpayers offset input taxes on business purchases against output tax liability. When eligibility conditions fail (non-payment within 180 days, use in exempt supplies, or supplier non-compliance), you must reverse credit, then re-claim when the issue is rectified.

This guide explains the triggers, computations, re-claim mechanics, vendor controls, reporting, and audit readiness. Your compliance stays tight and your cash flow remains predictable.

Quick primer: legal basis and scope

Section 16 lays the foundational eligibility to claim ITC. Fail any condition and reversal follows.

Section 17(5) blocks credits permanently for specific expenses, such as personal consumption or free samples.

Rule 37 mandates reversal if you do not pay the supplier within 180 days from the invoice date.

Rules 42 and 43 govern apportionment where inputs serve both taxable and exempt supplies.

Reverse charge supplies are outside Rule 37 since the recipient directly pays tax. Schedule I deemed supplies carry special treatment.

Spot reversal risks early, and you will save interest, effort, and notices.

For deeper reading on reversal triggers and methods, see the CBIC official text of Rule 37 and ClearTax's Rule 37 explainer with examples.

Core trigger deep dive: reversal for non-payment beyond 180 days

Under Rule 37, if payment of invoice value and tax is not made within 180 days from the invoice date, you must reverse ITC proportionate to the unpaid portion.

Book adjustments count as payment. Partial payments cause proportionate reversals. Interest at 18 percent per annum applies from the date of availment till the date of reversal, then until payment when you re-claim.

Worked examples to clear the confusion

- Full non-payment: Invoice ₹1,00,000 plus ₹18,000 GST, full unpaid beyond 180 days. Reverse ₹18,000 plus interest.

- Partial payment: Pay ₹60,000 out of ₹1,00,000. Reverse ITC on unpaid ₹40,000. Proportionate reversal = 40,000 ÷ 1,00,000 × 18,000 = ₹7,200 plus interest.

- Subsequent payment and re-claim: After reversing, you pay the supplier. Re-avail the relevant ITC in the return for the period of payment.

Interest example: If you availed ₹9,000 ITC in April and reverse in October (184 days later), interest = ₹9,000 × 18% × 184 ÷ 365 = approximately ₹817. Use exact day counts for precision.

For illustrations and FAQs, see ClearTax's ITC reversal calculator and examples.

Other common ITC reversal scenarios

Apportionment under Rules 42 and 43: If inputs serve both taxable and exempt supplies, reverse the exempt portion using the notified formula. This ensures ITC benefit aligns with taxable turnover only.

Blocked credits under Section 17(5): Credits on personal consumption, motor vehicles for personal use, goods lost or disposed, and similar items remain permanently blocked. No re-claim is possible here.

Post-supply adjustments: Supplier credit notes reduce taxable value. Reverse the proportionate ITC. If invoices are cancelled, reverse the entire ITC claimed.

Supplier non-compliance under Rule 37A: If the supplier fails to deposit tax by September 30 of the financial year following the year of supply, you must reverse ITC by November 30, even if you have paid them in full. Re-avail when the supplier complies and appears in your GSTR-2B.

Monitor GSTR-2B closely each month to preempt these reversals.

More context on these scenarios is available in Grant Thornton India's analysis of the 180-day ITC reversal rule.

Compute and re-claim: step-by-step playbook

Step 1: compute the reversal

For 180-day breaches:

Unpaid portion ITC = Original ITC × Unpaid value ÷ Total invoice value.

Interest = Reversed ITC × 18% × Days ineligible ÷ 365.

Track month-wise to avoid understatement. A day-count method is more precise than monthly approximation.

Step 2: process the re-claim

Upon payment, re-avail in the next period through GSTR-3B Table 4(A)(5). Keep invoice copies, bank statements, adjustment notes, and approvals handy. Partial payments allow proportionate re-claims.

Example with journal entries

On reversal: Debit Output Tax Liability, Credit ITC Ledger.

On re-claim: Debit ITC Ledger, Credit Output Tax Liability.

Make your ledgers mirror your returns, and your audits will be smoother.

Vendor-level ITC control: processes and controls

Build a live vendor dashboard to track invoice due dates, 180-day ageing, GSTR-2B filing status, and link payments to invoices. During onboarding, validate GSTINs, check filing discipline, and align payment terms well within 180 days.

- Segregate ITC on hold versus available credits.

- Automate alerts for invoices nearing the 180-day threshold (set triggers at day 150).

- Integrate AP ageing with ITC tracking and approvals.

- Review vendor compliance periodically, and contractually nudge timeliness.

- Assign vendor compliance scores based on GSTR-1 and GSTR-3B filing regularity.

A proactive approach turns compliance into cash flow optimization. Paying the right vendor at the right time protects your ITC without straining working capital.

Reporting in returns: where and how

GSTR-3B

Report reversals in Table 4(B)(2). Report re-claims in Table 4(A)(5). Split by IGST, CGST, and SGST. Keep working papers for each amount.

GSTR-9

Reconcile annual reversals and re-claims with books and the electronic credit ledger. Use Table 8 for detailed ITC adjustments. Ensure that classifications (Rule 37 versus Rules 42 and 43) are distinctly presented.

Invoice mapping

Maintain a reversal register with invoice number, supplier GSTIN, original ITC, reversal amount, date, interest computed, and re-claim reference. This is essential during assessments and helps bridge your ledger to your filed returns.

Audit trail: evidence and documentation

- Reversal log capturing availment date, breach date, computation sheet, and 18 percent interest calculation (day-count method).

- Approval trail with maker-checker segregation.

- Payment proofs for re-claims, including bank statements or book adjustment notes.

- Version control for any corrections, with clear explanations.

Digitize everything. Tag by invoice ID. Conduct periodic internal audits to catch issues early. Assessors expect clean linkage from reversal register to GSTR-3B to bank proof.

Checklists and templates

180-day payment tracker

Columns: Invoice ID, date, supplier GSTIN, value, tax, due date, actual payment date, unpaid percentage, ITC to reverse, interest, status.

Monthly close checklist

- Scan invoices crossing 180 days.

- Compute proportionate reversals and interest (use day-count formula).

- Reconcile with GSTR-2B and flag non-compliant suppliers for Rule 37A.

- Review Rules 42 and 43 apportionment.

- Document all re-claims with proofs.

- Verify reversed ITC pending re-claim register for cleared payments.

Interest worksheet

Formula: Reversed_ITC × 0.18 × Days ÷ 365. Automate from the tracker to reduce manual errors. Cross-check interest periods carefully against availment dates.

Audit log

Fields: action type, date, user, invoice reference, amount, document link, approval status, return period.

Common pitfalls and how to avoid them

Over or under reversal on partial payments

Always apply the proportionate formula. Never reverse the whole amount if only a part is unpaid. Example: ₹40,000 unpaid on ₹1,00,000 invoice means only 40% of ITC gets reversed.

Ignoring supplier mismatches

Monitor GSTR-2B monthly, not quarterly. Prepare for Rule 37A driven reversals if suppliers default. The November 30 deadline catches many firms off guard.

Weak payment linking

Always tag payments to specific invoices. Bulk or pooled payments without invoice-level allocation make re-claim tracking nearly impossible during audits.

Misreporting in returns

Map reversals to Table 4(B)(2), re-claims to Table 4(A)(5), and reconcile to GSTR-9. Consistency between monthly returns and annual return is what assessors check first.

Poor documentation

Keep digital logs. Avoid verbal approvals. Preserve all payment proofs with date stamps.

Manual calculation errors

Use standardized templates or automation. Cross-check interest periods carefully. A one-month error in the start date changes the interest amount significantly.

Missed re-claims

Maintain a separate register for reversed ITC pending re-claim. Set reminders aligned to payment runs. Many firms lose lakhs annually simply by not re-claiming after payment.

India-context best practices

- Negotiate payment terms of 120 to 150 days to preserve a buffer before the 180-day deadline.

- Perform monthly GSTR-2B reconciliation, not just year-end true-up.

- Institutionalize maker-checker for all reversals, given the 18% interest impact.

- Run quarterly clean-ups for small unpaid invoices. Decide: pay and claim, or reverse and close.

- Educate vendors on filing discipline. Offer better payment terms to compliant suppliers.

- Plan for festival season cash stretches. Anticipate potential reversals and queue re-claims.

- Track the Rule 37A November 30 deadline separately in your compliance calendar.

How technology and automation help

Tools that transform ITC management

AI Accountant auto-syncs vendor masters, validates GSTINs, flags 180-day breaches, links AP invoices to payments, computes reversals, and nudges re-claims once payments clear. Other tools that support GST compliance include QuickBooks, Tally Prime, SAP, and FreshBooks, although complex reversals involving proportionate calculations and interest may need careful oversight in any system.

Automation benefits that matter

- Real-time vendor-level ITC control with ageing and compliance scores.

- Error-free compute and re-claim with proportionate reversal and interest logic.

- Smoother reporting in GSTR-3B and rolling logs for GSTR-9.

- Automatic audit trail with user stamps and document links.

Dashboards surface overdue ITC, cash flow impact, and 2B alignment, so you pay the right supplier at the right time.

Conclusion

ITC reversal does not have to be a monthly scramble. Know the 180-day rule, reverse proportionately, factor in 18 percent interest, and re-claim with proof.

Build vendor-level controls, keep tight documentation, and report accurately. The Rule 37A November 30 deadline adds another layer, so monthly GSTR-2B monitoring is non-negotiable.

Automation with tools like AI Accountant can streamline computations, alerts, and audit trails. Start now, and your next audit will feel like a checklist, not a crisis.

FAQ

How do I compute interest on a Rule 37 reversal, monthly or daily?

Interest is calculated at 18% per annum using a day-count method: Reversed ITC × 0.18 × actual days ÷ 365. The period runs from the date of ITC availment until the date you reverse it. For re-claim scenarios, interest continues until payment. While some CAs use monthly approximation, the day-count method is more precise and defensible during assessments.

From which date is 18% interest calculated for 180-day breaches?

The clock starts from the date of ITC availment on that invoice, not from day 181. If you availed ITC in April and hit the breach in October, compute interest from April up to the date of reversal. Interest continues until payment if you re-claim later.

Is there any time limit under Section 16(4) for re-claiming ITC reversed due to 180-day non-payment?

No, re-claim on payment is allowed without the Section 16(4) cut-off, provided the original availment was within time and you maintain robust payment proof. File the re-claim in GSTR-3B Table 4(A)(5) in the period of payment, with clear working papers.

Do book adjustments qualify as payment for the 180-day rule?

Yes, valid book adjustments (such as netting receivables against payables with the same supplier) count as payment under Rule 37. Keep properly authorized journal entries and a clear offset note as evidence.

Does reverse charge (RCM) come under the 180-day payment condition?

No, RCM supplies are outside Rule 37 because the recipient pays tax directly to the government. However, ensure you pay the self-assessed tax correctly and report it in your return before claiming ITC.

What is the Rule 37A deadline for supplier default reversals?

You must reverse ITC by November 30 of the financial year if your supplier has not deposited the relevant tax by September 30 of the following financial year (2026 update). Monitor GSTR-2B monthly to identify non-compliant suppliers early. Re-avail when the supplier files and the invoice appears in your GSTR-2B.

How should retention money or staggered contractual payments be treated?

Reverse ITC proportionately for the unpaid retention portion once 180 days pass, and re-claim upon actual payment. Keep the contract terms, milestone approvals, and payment schedules as evidence. Auditors expect a clear linkage between retention clauses and the ITC reversal timeline.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.