-01%201.svg)

Key takeaways

- A year end close plan is an integrated framework (calendar, owners, deadlines, blackout periods, audit pack) that turns the March scramble into a repeatable, predictable process for CA teams and SMB finance departments.

- Starting at T-45 with ledger hygiene and enforcing blackout dates from T-7 to T+5 prevents last minute surprises, protecting reconciliation accuracy when it matters most.

- Staffing by functional lanes with a RACI matrix, shift coverage, and daily standups reduces burnout and cuts rework, the silent delay multiplier during close.

- Disciplined reconciliations (bank, AP/AR, GST, inventory, fixed assets) with linked evidence shorten audit cycles and satisfy auditor queries on day one.

- Firms tracking KPIs like days to close, journal rework rate, and query ageing see compounding efficiency gains year over year, often shaving two to five days off their close timeline.

- Repetitive execution work (ingesting statements, categorizing transactions, matching invoices, reconciling GST) is where automation delivers the biggest time savings. AI Accountant's bookkeeping automation handles this so your team focuses on judgment and decisions, not data entry.

Year End Close Planning: What's New in 2026

If you ran your March 2025 close on spreadsheets and manual uploads, the 2026 landscape demands a rethink. Several regulatory and operational shifts directly affect how CA teams plan their year end.

GST e-invoicing thresholds have tightened. Until March 2025, the mandate covered businesses with turnover above ₹5 crore. From April 2025, the threshold dropped further, pulling a larger share of SMEs into the e-invoicing net. For close planning, this means more clients generating IRNs, more data to validate during your T-14 to T-1 window, and more ITC mismatches to catch before GSTR-2B reconciliation. The CBIC's e-invoicing notifications detail the phased rollout.

Auditors now expect AI generated PBC packs with embedded evidence. Query SLAs have tightened to 48 hours for Schedule III disclosures in many mid tier audits. If your team still emails zip files with inconsistent naming, expect day one friction. A structured approach using automated GST reconciliation and statement ingestion cuts prep time significantly.

On the Ind AS and ICDS front, deferred tax computations increasingly require monthly roll forwards rather than year end bulk calculations. Firms maintaining a living tax book reconciliation throughout the year, tagging timing differences as transactions hit, are closing faster and with fewer adjustments. The ICAI's technical guidance on Ind AS implementation continues to be the reference point for complex areas like revenue recognition and financial instruments.

What to do now:

- Confirm which clients crossed the latest e-invoicing threshold and update your IRN validation checklist before T-45.

- Shift deferred tax computation to a monthly cadence this quarter, so March is a review, not a build from scratch exercise.

- Pilot bulk statement ingestion and auto categorization for at least two clients before the close window opens.

What is a Year End Close Plan?

Every March, the same pattern repeats for Indian SMBs and CA firms. GST rushes, bank recs stack up, TDS mismatches crop up, auditors ask for documents at the worst time. A smart year end close plan turns that chaos into clockwork.

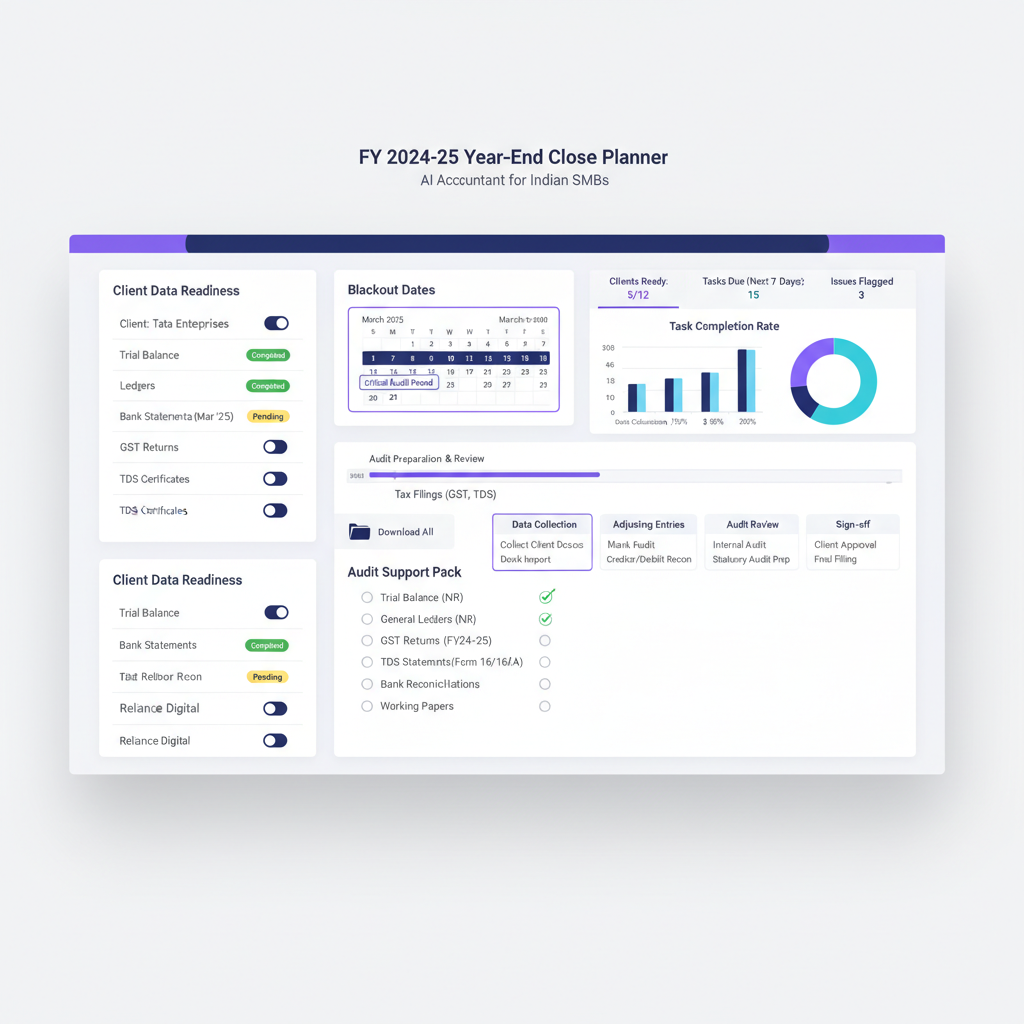

At its heart, a year end close plan is an integrated framework, not just a checklist. You get a calendar with clear owners and deadlines, staffing and shifts for peak days, defined blackout dates to prevent last minute system changes, client data readiness criteria, a standard journal checklist, stepwise reconciliations, and a bulletproof audit support pack.

Success looks like on time close, zero orphan tasks, minimal rework, and fast audit query resolution.

Your year end close becomes a repeatable process, not an annual emergency.

For a practical overview, see this helpful ICAI guidance on accounting standards and close procedures and the MCA's Schedule III requirements for presentation and disclosure.

Creating Your Year End Close Timeline Blueprint

Timing is everything. Your timeline blueprint breaks work into phases, from pre close hygiene to audit support.

T-45 to T-15: Build momentum

- Clean up ledgers and sub ledgers. Update master data, send balance confirmations, check GRNs and IRNs.

- Finalize request lists to clients. Communicate blackout dates early. Lock scope creep before it starts.

- Verify vendor invoice matching for top counterparties and clear pending disputes.

T-14 to T-1: Data completeness

- Run a soft close dry run. Complete physical inventory counts. Verify fixed asset registers.

- Document with memos. Align provisions logic. Queue standard journal entries for posting.

- Flag any ledger entry anomalies or unreconciled transactions now, not during T0.

T0 to T+5: Execution window

- Post all journals. Complete reconciliations. Freeze trial balance, no exceptions.

- Run final bank rec and GST tie outs. Escalate any open items immediately.

T+6 to T+15: Audit preparation

- Compile audit support pack. Conduct management reviews. Brief the board if required.

- Ensure all evidence is linked, named consistently, and mapped to the PBC tracker.

Blackout dates are your guardrails. Freeze policy changes, ERP modifications, and SKU master updates from T-7 to T+5. This keeps reconciliations stable when accuracy matters most.

For additional context, refer to the GST portal for filing deadlines that overlap with your close window.

Managing Staffing and Shifts During Close

Your team can make or break the close. Capacity plan by functional lanes: AP and AR, GST and TDS, fixed assets, revenue, inventory, intercompany. Assign primary owners with backups. Pair preparers with reviewers.

- Design shifts for coverage. Early shifts gather and process data. Late shifts review and escalate. Weekends and holidays are pre planned, not afterthoughts.

- Use a RACI for every task. Clarify who is responsible, accountable, consulted, and informed.

- Protect people. Cap hours. Enforce handoffs. Run short daily standups to clear blockers fast.

Remember: a tired accountant makes avoidable mistakes. Rework during close is a silent delay multiplier.

Here is a practical RACI snapshot for common close workstreams:

| Task Area | Responsible (Preparer) | Accountable (Lead) | Consulted (Reviewers) | Informed (Stakeholders) |

|---|---|---|---|---|

| Bank Recs | Junior Accountant | Sr. Accountant | Tax Lead | Client CFO |

| GST Matches | AR/AP Team | Compliance Mgr | Auditor | Operations Head |

| Journal Postings | FA Specialist | Engagement Mgr | Board (if material) | Full Team |

| Audit Pack | All Preparers | Firm Partner | External Auditor | Client |

Adapt this to your firm's size and engagement complexity.

Ensuring Client Data Readiness

Define "ready to post." Files complete, naming conventions followed, formats accepted, approvals documented.

Issue comprehensive request lists early:

- Bank statements (all accounts, full year)

- GST returns and reconciliations (GSTR-1, GSTR-3B, GSTR-2B)

- TDS certificates and Form 26AS / AIS

- Payroll registers and leave encashment data

- Inventory count sheets with valuation basis

- Balance confirmations for top counterparties

Validate upon receipt. Check OCR readability. Deduplicate. Maintain version control. Update a shared dashboard daily so nothing slips through.

For setup ideas, explore a digital client portal.

Modern automation changes the game. Tools like AI Accountant bulk ingest documents, structure statements, match transactions, and flag gaps early, so your team focuses on analysis, not typing.

Mastering Reconciliations and Tie Outs

Reconciliations verify that books reflect reality. Each one is a control point that auditors rely on.

- Bank: Cover every account. Chase items older than 30, 60, 90 days. Document provisions for stale items.

- AP and AR: Use aging reports. Focus on top counterparties and related parties. Confirm balances. Document disputes or payment plans.

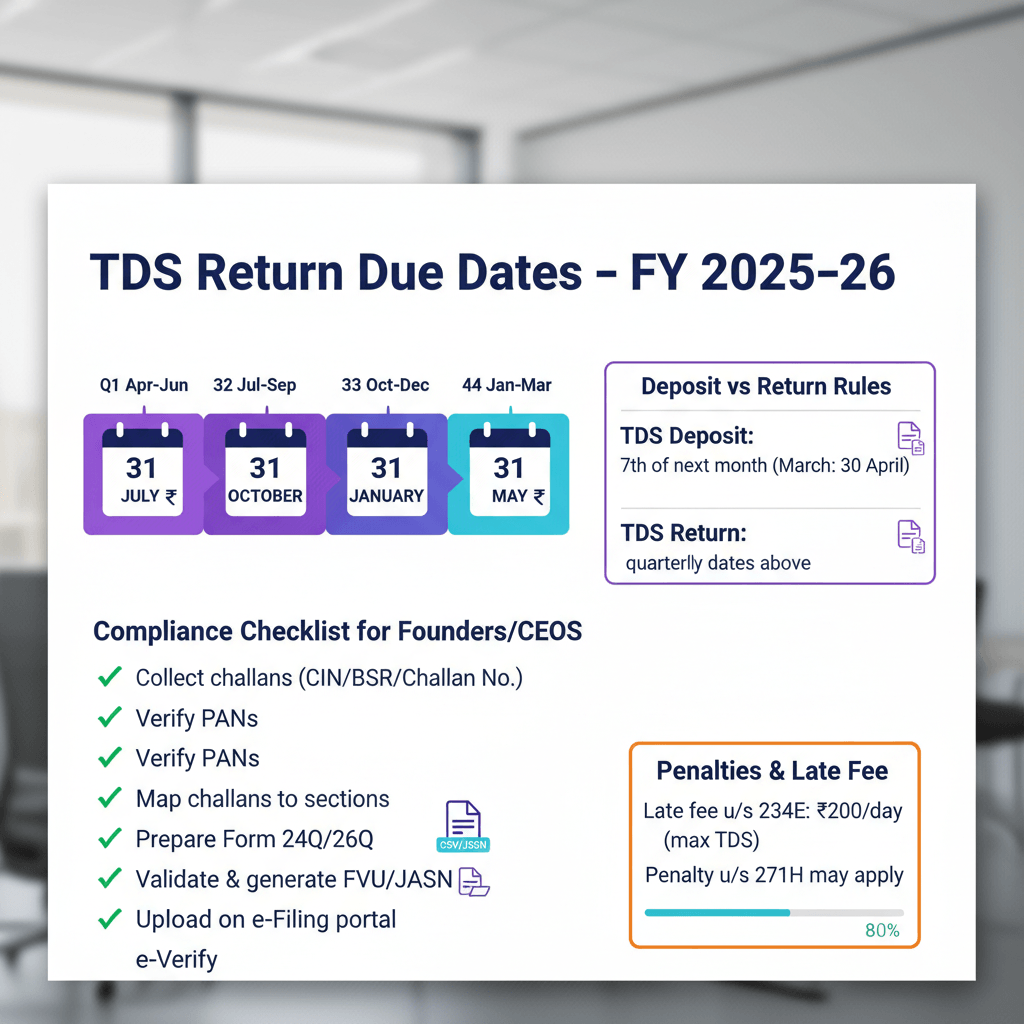

- GST: Match GSTR-2B reconciliation to purchase book. Identify ITC reversals and ineligible credits. Reconcile TDS payable with Form 26AS and the Annual Information Statement (AIS).

- Loans and FX: Match interest to statements. Revalue monetary items. Document exchange rate sources using RBI reference rates consistently.

- Inventory: Tie physical counts to system records. Mark WIP. Compute obsolescence and write downs for damaged goods.

- Fixed assets: Confirm capitalization cutoffs. Remove disposals. True up depreciation. Review for impairment triggers.

Each reconciliation needs proof: screenshots, calculations, variance explanations, and approved adjustments. Link every recon to your PBC index.

For additional best practices on tax compliance before 31 March, refer to the Income Tax Department portal for Form 26AS verification and TDS filing deadlines.

Building Your Standard Journal Checklist

A strong journal checklist prevents last minute surprises. Think of it as your close playbook for recurring entries.

- Accruals: Utilities unbilled, audit fees, bonus provisions, straight line rent adjustments.

- Provisions: ECL for doubtful debts, warranty obligations, stock obsolescence, asset impairment.

- Prepaids and deferrals: Insurance, AMCs, advance rentals, unearned revenue for incomplete services.

- FX revaluation: Unrealized gains and losses on monetary assets and liabilities. Use RBI reference rates consistently.

- GST adjustments: Rule 42 and 43 reversals, clear GSTR-2B mismatches, annual reconciliations and true ups.

- TDS provisions: Compute by category. Gross up if contracts require. Verify with Form 26AS.

- Intercompany eliminations: Remove intra group sales and purchases. TP adjustments. Eliminate unrealized profit in inventory.

- Payroll accruals: Leave encashment, gratuity, bonuses per agreements.

- Financial instruments: Interest accruals, EIR amortization, fair value changes where applicable.

Use a standard template for every journal: date, description, policy reference, linked workings, and reviewer signoff with timestamp.

Implementing Controls Reviews and Documentation

Controls reduce errors and audit friction. Start by creating workstream checklists with owners and due dates.

Set materiality thresholds to focus reviews on what matters. Define evidence standards by area: bank statements for cash, confirmations for receivables, count sheets for inventory, board minutes for provisions.

Run three way sign offs: preparer, reviewer, approver. Track all signoffs with timestamps. Organize documentation so auditors can follow the narrative with minimal queries.

A well structured control environment means fewer back and forth emails during audit fieldwork.

Creating Your Audit Support Pack

A great audit support pack shortens audits dramatically. Build an index covering: trial balance, GL details, lead schedules, bank recs, confirmations, payroll summaries, GST and TDS reconciliations, loan statements, board minutes, key contracts, and memos.

Use a standard folder tree with consistent file names. Map everything to your PBC tracker.

Protect data. Restrict access. Watermark sensitive files. Align with ISO 27001 or SOC 2 where tools are involved. Define query SLAs (aim for 48 hours or less), manage versions, and maintain a query log.

When your pack is clean and complete on day one, the entire audit moves faster.

Meeting India Specific Compliance Requirements

- Schedule III presentation: Correct classification between current and non current. Proper disclosures per MCA guidelines.

- MSME disclosures: Track payment delays, interest obligations, and reporting requirements. This is a high scrutiny area in audits.

- Related parties: Identify all parties. Document terms. Compare with arm's length. Ensure comprehensive disclosures.

- CSR: Compute average net profits. Track spends. Disclose unspent amounts and set asides.

- CARO: Review internal controls, statutory dues, loan utilizations, going concern considerations.

- ICDS: Manage tax book differences, deferred taxes, and reconciliations. Monthly roll forward of deferred tax is now best practice (2026 update).

- UDIN: Ensure generation and verification. Maintain records per ICAI requirements.

- Management representation letters: Include Indian regulatory confirmations and get proper signoffs.

Tracking Continuous Improvement Metrics

What gets measured gets better. Track these KPIs after every close:

- Days to close (target reduction of one to two days per cycle)

- On time task completion percentage

- Journal rework rate

- Audit query volume and average age

- Reconciliation backlog age

- Exception turnaround time

Run retrospectives. Find root causes. Implement targeted fixes. Track per client and per workstream to find your real constraints.

Look for automation wins: direct bank feeds, AI driven reconciliations, and predictive alerts on risk areas. Small gains compound. A day saved, an exception prevented, a query avoided.

Selecting the Right Tooling Workflow

Your tooling can accelerate quality and speed.

- AI Accountant, a quiet AI assistant that auto ingests bank statements, categorizes transactions, flags exceptions, and syncs with Tally, especially strong with Indian bank formats and GST workflows.

- QuickBooks, user friendly, rich integrations, may need localization for GST workflows.

- Xero, clean bank recs and real time collaboration.

- FreshBooks, simple invoicing and expenses for smaller teams.

- Tally Prime, the Indian backbone with native GST and TDS compliance.

Let Tally be your backbone. Layer intelligent automation for ingestion, categorization, reconciliation, and exception reporting. The goal is not replacement, it is leverage. Your accountants spend time on analysis and decisions, not repetitive keystrokes.

Essential Templates and Downloads

- Year end close master plan: calendar, RACI, escalations, and success criteria.

- Client data readiness checklist: accepted formats, quality thresholds, deadlines, and escalation triggers.

- Standard journal entry checklist: recurring entries, methods, policy references, PY comparatives.

- Blackout calendar: freeze periods, restricted actions, exception approvers, and communication plan.

- Staffing and shift roster: coverage by function, hours, rotations, and backups.

- Audit support pack tracker: schedule list, prep status, reviewer notes, and auditor queries.

Visualizing Your Close Process

Visuals make complex processes simple. Build:

- A close timeline with milestones and blackout overlays

- A RACI snapshot for a typical engagement

- A data flow from client upload to audit pack

- Dashboards for progress, rec exceptions, and query ageing

When everyone can see the flow, everyone can improve the flow.

Taking Action on Your Year End Close Plan

Knowledge without action changes nothing.

Start by adopting comprehensive templates. Customize for your context. Run a dummy close before year end to test your process. Use your monthly close to refine handoffs and communication.

If you are ready to accelerate, pilot an automation layer: bulk ingestion, auto categorization, AI reconciliations, and seamless sync into Tally.

A proper plan replaces panic with process, chaos with control, and late nights with predictable workflows.

FAQ

How should a CA structure a T-45 to T+15 close calendar for Indian SMB clients?

Start at T-45 with ledger cleanup, master data updates, balance confirmations, and GRN/IRN checks. From T-14 to T-1, run a soft close dry run, complete inventory counts, verify fixed assets, and queue standard journals. T0 to T+5 is the execution window: post all journals, finish reconciliations, and freeze the trial balance. T+6 to T+15 is for compiling the audit support pack and management reviews. Enforce blackout dates from T-7 to T+5 to keep the data stable.

What is a practical RACI model for close tasks that CAs can hand to staff and article assistants?

Assign Responsible to preparers by workstream (AP, AR, GST, TDS, FA, inventory). Accountable should be the team lead or engagement manager. Consulted includes tax and audit reviewers. Informed includes client finance heads. Keep the RACI inside your close tracker and pair each task with clear evidence standards and deadlines.

How do I enforce blackout dates with clients who keep changing masters in Tally during close?

Communicate freeze dates one month in advance with a clear list of restricted actions: policy changes, master data updates, SKU edits, and backdated entries. Provide a named exception approver and a cut off time. If an exception is approved, log the change, re run impacted reconciliations, and capture revised evidence immediately.

What reconciliation evidence do auditors typically accept without pushback?

Bank reconciliations with bank statements, recon sheets, and proof for outstanding items. AP and AR aging with top party confirmations and dispute notes. GST tie outs matching GSTR-2B to purchase registers with ITC reversal workings. TDS matched with Form 26AS and AIS (2026 update). Inventory count sheets with valuation workings. Fixed assets with FA register, capitalization memos, and depreciation schedules. Link every recon to your PBC index with consistent naming.

How can I cut journal entry rework during close for multi entity groups?

Standardize journal entry templates with policy references, computation sheets, and clear review checkpoints. Lock calculation methods for provisions and FX revaluation. Maintain prior year comparatives for sanity checks. Use maker checker workflows with defined materiality thresholds. For intercompany, run a pre close netting and confirmation loop to catch mismatches early.

What KPIs should a CA firm track to prove close efficiency improvements to clients?

Days to close, on time task completion percentage, journal rework rate, audit query count and average age, reconciliation backlog age, and exception turnaround time. Track per client and per workstream to pinpoint your real bottlenecks. Share a post close dashboard in your management review to demonstrate measurable improvement cycle over cycle.

How do I align ICDS and Ind AS differences at year end without last minute fire drills?

Maintain a living tax book reconciliation throughout the year, tagging transactions that create timing differences as they occur. Compute deferred tax monthly rather than in a single year end batch (2026 update). Keep a disclosure ready template for complex areas like revenue recognition, FX, provisions, and financial instruments. Run a tax technical review at T-14 to catch issues before the execution window.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.