Key takeaways

- ITC validation in accounts payable is a cash protection discipline, done right it can unlock 5 to 8% of working capital otherwise stuck in reversals and notices.

- Anchor your checks on Sections 16, 17(5), and Rule 46, pair them with GSTR 2B reconciliation for airtight eligibility.

- Use a practical, line level checklist for supplier hygiene, transaction logic, 2B linkage, blocked credits, special cases, and timing rules.

- Build a Tally centric workflow, tag each line as eligible, ineligible, deferred, or RCM, then post only after reconciliation.

- Track KPIs like 2B hit rate, deferred ITC aging, 180 day exposure, and exception resolution time to drive continuous improvement.

- Prepare for hard validations in GSTR 3B via ECRS, automate now to avoid system level ITC blocks later.

- Tools like AI Accountant deliver bulk extraction, line level eligibility checks, and one click validation with Tally and Zoho Books.

Why ITC Validation Accounts Payable India Matters More Than Ever

Picture this, you close the month and realize 8% of working capital is stuck due to denied ITC. That is not theoretical, it is cash your business needs. ITC validation accounts payable India is now the highest ROI control point for finance teams, get it wrong, and you invite cash leakage, reversals, interest, penalties, and audit heat. Get it right, and you recover real money, fast. For a policy background, see this detailed explainer on ITC rules and pitfalls and this concise industry insights ITC checklist eBook.

Finance leaders who operationalize ITC validation at source typically recover 5 to 8% of working capital that would otherwise leak through compliance cracks.

What ITC Validation in AP Really Covers

Think of ITC validation as an AP journey, ingestion, validation, posting, reconciliation, close. Invoices must comply with Rule 46, match master data, and pass place of supply logic, then meet GSTR 2B eligibility, only then should they hit your ITC ledgers. Sections 16 and 17(5) govern eligibility and blocked credits, Rule 46 prescribes invoice particulars, and time limits matter, including the 180 day payment rule for proportionate reversal.

Get ready for a 2026 shift, CBIC hard validations in GSTR 3B via ECRS will auto block non 2B matched credits, learn more about handling these changes in this practical note on ITC reclaim with hard validations in GSTR 3B. For ground level eligibility lists, see this ITC eligibility criteria checklist and this GST ITC claim checklist.

ITC Eligibility Check Vendor Bill: A Practical Checklist

Use this step by step, itc eligibility check vendor bill routine before you post anything to your books.

Supplier and Document Hygiene

- Validate vendor GSTIN and registration status on the GST portal, inactive or cancelled means no ITC.

- Verify Rule 46 particulars, invoice number and date, both GSTINs, HSN or SAC, tax rate, place of supply, value and CGST, SGST, IGST split, supply type.

- Match invoice to PO and GRN, no receipt evidence, no ITC. Good reference, ITC claim documentation essentials and this invoice standards checklist.

Transaction Logic Verification

- Check tax rate versus HSN or SAC, a 12% rate on an 18% code is a red flag.

- Verify inter state versus intra state logic, IGST for inter state, CGST plus SGST for intra state, place of supply must align. See this quick logic refresher.

GSTR 2B Linkage

Confirm the invoice appears in the latest period’s 2B, for tooling context read this GSTR 2B reconciliation tools overview. If missing, defer the credit and follow up with the vendor. For methodical reconciliation steps, see this reconciliation deep dive and a pragmatic filing and documents checklist.

Blocked Credits Under Section 17(5)

- Motor vehicles, food and beverages, club memberships, works contracts for immovable property, and personal use items are typically blocked.

- Handle mixed use with proportionate reversals, and treat capital goods with care. A crisp summary is available in this ITC restrictions note.

Special Cases That Need Extra Care

- Reverse charge mechanism transactions require tax payment first, then ITC claim, common items include freight, legal services, director remuneration.

- Imports need Bill of Entry, advances allow ITC only when invoiced, credit notes trigger reversals.

- ISD credits and SEZ supplies require precise documentation, see these practical checklists, ITC reconciliation guide and GST filing checklist.

Payment and Timing Rules

The 180 day payment rule is critical, see how teams automate this in ITC reversal automation. If unpaid after 180 days, reverse proportionately. Defer credits until 2B reflects, the upcoming hard validations will block out of sync claims. A handy perspective, ITC reclaim with hard validations and ITC eligibility criteria.

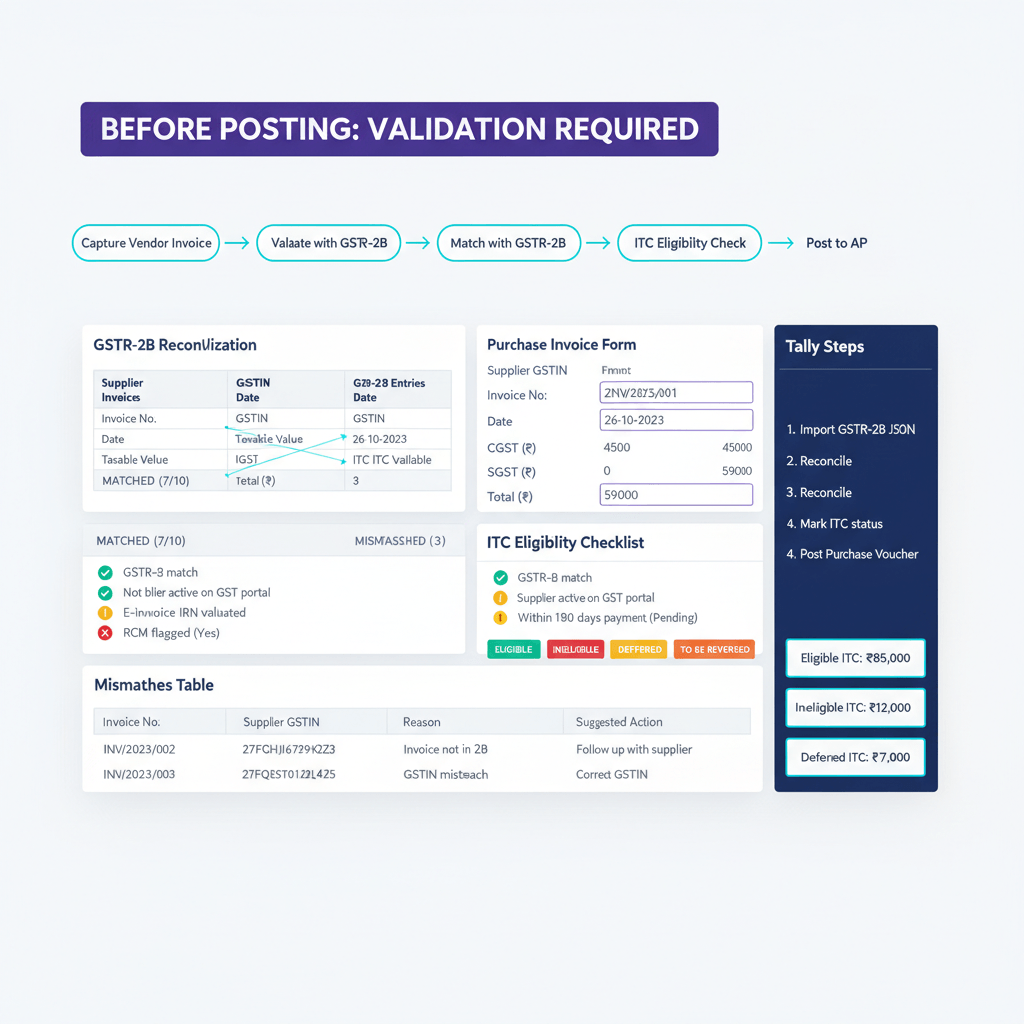

Validate ITC Before Posting Invoice Tally: Step by Step Workflow

Here is how to validate itc before posting invoice tally, saving hours at close and avoiding painful reversals later.

Prerequisites in TallyPrime

- Enable GST, set state and registration, create supplier ledgers with correct GSTIN and state.

- Maintain separate purchase ledgers for supply types, plus specific ledgers for ineligible and deferred ITC. See AP audit readiness fundamentals and this GST setup checklist.

Voucher Entry Best Practices

- Map IGST or CGST plus SGST by place of supply, verify Tally calculations, do not assume.

- Tag lines as eligible, ineligible, deferred, or RCM, attach invoice, PO, GRN for audit trail, reinforced here, prepare AP for audit.

Reconciliation and Posting Logic

- Run 2B reconciliation pre posting, investigate mismatches first.

- Post eligible to ITC ledger, park deferred in a separate ledger, auto release when 2B matches.

- Book ineligible straight to expense, process RCM with liability first, then ITC after payment. See this reconciliation deep dive and filing checklist.

Control Reports You Need

- Exception reports for missing GSTINs, rate mismatches, wrong place of supply, and 2B gaps.

- Run weekly, not monthly, and maintain deferred ITC aging with escalations. Useful primer, AP controls that withstand audits.

GST ITC AP India: End to End Workflow and Controls

Ingestion and Standardization

Create a central repository, deduplicate, and extract key fields consistently. See intake and standardization best practices for AP.

Mapping and Master Management

Maintain clean vendor masters, HSN and SAC mapping, periodic GSTIN status checks. A legal controls refresher, ITC legal foundation.

Eligibility Assessment at Scale

Apply Section 17(5) uniformly, verify place of supply, and tag at line level. For quick guardrails, use this ITC eligibility checklist.

GSTR 2B Reconciliation Process

Download 2B on the 14th, match with purchase register, and queue claims versus deferrals. Read, mastering ITC reconciliation and filing checklist.

Clean Posting to Accounting Systems

Post to Tally or Zoho Books only after validation, link to PO and GRN, test bulk posting in small batches. Guidance, prepare AP for audit.

Month End Procedures

Roll forward deferred ITC with aging, process 180 day reversals and interest, publish ITC utilization reports. Create a tight month end checklist, supported by this compliance checklist and ITC controls explainer.

Get sign offs from AP, tax, and CFO, consistency prevents surprises.

Real World Examples: ITC Validation in Action

Scenario 1: Inter State Service Invoice

A digital marketing invoice from Mumbai to your Delhi registration shows 18% IGST, appears in 2B, and has documentation, this is eligible ITC, post full IGST to input credit. For a crisp checklist, see ITC eligibility criteria.

Scenario 2: Hotel Stay for Business Travel

Hotel bill for an employee, even with GST and valid GSTIN, is blocked under 17(5), post entire amount to travel expense, no ITC. Reference, blocked credits summary.

Scenario 3: Freight Under RCM

Freight from an unregistered transporter, pay GST under RCM, then claim ITC after payment, retain challan as audit proof. Steps align with ITC reconciliation guide and filing checklist.

KPIs and Dashboards for ITC Management

Core ITC Metrics

- Claimed versus potential ITC, the delta is recoverable opportunity.

- Deferred ITC aging, focus on 30 to 60 day buckets for recovery.

- GSTR 2B hit rate on first attempt, below 80% indicates vendor education gaps.

Compliance and Risk Metrics

- Ineligible ITC by 17(5) code, informs procurement policy.

- 180 day exposure with alerts at 150 days.

- Exception resolution time, faster closure equals better working capital.

Dashboard Design for Decision Making

Show deferred aging, current 2B compliance rate, 180 day at risk, and six month recovery trend. Use green, yellow, red cues, and drilldowns from total deferred to vendor to invoice. For context, review this ITC checklist eBook and ITC controls explainer.

Automation Tools for ITC Validation

Essential Automation Capabilities

- Bulk extraction from PDFs and images, automatic GSTIN validation and mismatch detection.

- Line level eligibility checks on Section 17(5), place of supply logic, and RCM applicability.

- Automated GSTR 2B reconciliation with match, mismatch, and missing statuses.

Top Tools for Indian Businesses

- AI Accountant offers bulk bill extraction, automatic itc eligibility check vendor bill at line level, instant GSTIN mismatch detection, and one click validate itc before posting invoice tally workflows, with Tally and Zoho Books integrations.

- QuickBooks, GST features with basic ITC tracking and GSTR reports.

- Xero, GST support and basic reconciliation capabilities.

- Zoho Books, native GST and return preparation features.

- FreshBooks, GST invoicing and basic ITC tracking for small teams.

- Tally Prime, comprehensive GST and ITC functionality widely adopted in India.

Integration Requirements

Ensure clean sync with your accounting system, maintain full audit trails, and surface real time dashboards. For audit readiness and systems design tips, see this AP audit playbook and the industry checklist.

Getting Started with ITC Validation

What You Need Before Starting

- Access to Tally or Zoho Books, 6 to 12 months of purchase data, corresponding GSTR 2B files.

- Updated vendor master with GSTINs, pick a pilot group from your top 20% vendors by volume.

- Document your current flow, approvals, and bottlenecks to benchmark improvements.

Implementation Approach

- Pilot with 10 to 20 vendors, run the checklist in Excel for a week, refine using actual exceptions.

- Track recovered ITC and error rates from day one, numbers will drive adoption.

Training Your Team

- Use one page guides and visual flowcharts, run weekly 15 minute exception huddles, celebrate wins.

- Adopt a buddy system to speed up on the job learning. Helpful references, GST filing checklist and the ITC checklist eBook.

Common Mistakes to Avoid

Claiming ITC on Blocked Categories

Classic 17(5) traps include food and beverages, club memberships, and personal use vehicles, even with valid invoices, no ITC.

Ignoring Place of Supply Rules

Mis coding IGST versus CGST plus SGST leads to rework, verify place of supply for each transaction, especially services.

Missing the 180 Day Payment Deadline

Track payment aging diligently, reverse proportionately after 180 days, with interest from original claim date.

Poor Documentation Practices

No document, no ITC, keep invoice, proof of payment, receipt evidence, and 2B proof together. Auditors reward discipline.

Conclusion and Next Steps

ITC validation accounts payable India is not just compliance, it is working capital protection. With a robust itc eligibility check vendor bill, a Tally first posting routine, and vigilant KPIs, you create a resilient gst itc ap india engine that scales. Improve recovery by even 2% on 10 crores of purchases, that is 20 lakhs in additional working capital. Start with the checklist, implement the workflow for your top vendors, then automate as volume grows. Explore this comprehensive ITC explainer and the eligibility checklist for immediate action.

If you want a fast baseline, run last month’s purchase register through a rigorous validation pass. Teams ready to scale can ask AI Accountant to analyze a sample month and pinpoint recovery opportunities. The best time to fix ITC validation was yesterday, the second best is today.

FAQ

Can I claim ITC if an invoice is missing in GSTR 2B but I have a valid tax invoice and GRN?

Defer the claim, do not book ITC until it appears in your 2B. Follow up with the supplier to ensure timely GSTR 1 filing. Once the invoice flows into your 2B within the statutory window, claim it in that period. For a practical process, see this ITC eligibility checklist.

How should a CA handle credit notes and corresponding ITC reversals in Tally?

Reconcile the credit note against the original invoice, verify GSTINs and tax amounts, then reverse ITC in the month of receipt of the credit note. Link the reversal to both documents to avoid double action. A refresher on documentation is here, GST filing checklist.

What is the correct approach for multiple GST registrations when invoices span states?

Each GSTIN is a separate person under law, only the registration that receives the supply can claim ITC. Use place of supply for apportionment, split multi location deliveries accordingly, and maintain separate ITC registers per GSTIN. Legal grounding here, ITC legal foundation.

How do I treat vendor uploads made after my intended claim period, especially near November 30?

Claim in the period when the invoice appears in 2B, ensuring you are within the final eligibility cutoff, November 30, or annual return due date, whichever is earlier. For 2026 hard validations, see this note on ITC reclaim with hard validations.

What controls help avoid reversals under the 180 day payment rule?

Start a payable aging watch at 120 days, trigger alerts at 150 days, and auto compute proportionate reversal at 180 days. After payment, reclaim in the month of payment. Learn about automating this in ITC reversal automation.

How should RCM on freight and legal services be captured for seamless audit trails?

Raise a liability entry for RCM tax, pay it with your return, then book the corresponding ITC post payment, attach challans and workings to the voucher. A concise overview of RCM accounting is here, RCM accounting in India.

For mixed use expenses, what is the CA recommended basis for proportionate reversal?

Adopt a rational, consistently applied basis, for instance square footage for facilities, headcount for certain services, or usage logs for shared subscriptions. Document the basis and review quarterly. See blocked credit principles in this ITC restrictions explainer.

How do I structure Tally ledgers to separate eligible, ineligible, deferred, and RCM ITC?

Create distinct ledgers for input IGST, CGST, SGST, ineligible ITC expense, deferred ITC control, and RCM tax liability, tag lines accordingly at voucher entry. Pre posting 2B reconciliation is non negotiable. For AP audit readiness, review this audit readiness guide.

What reconciliation cadence is ideal for minimizing ITC leakage for mid market clients?

Weekly exception sweeps for GSTIN validity, rate mismatches, place of supply errors, and 2B gaps, plus a full 2B reconciliation by the 16th. Keep a deferred ITC aging dashboard with escalations beyond 60 days. Method steps here, ITC reconciliation deep dive.

How does an AI tool like AI Accountant reduce month end firefighting for AP and tax teams?

AI Accountant automates OCR based bill extraction, runs line level 17(5) checks, validates GSTINs, and performs one click GSTR 2B reconciliation, then syncs clean postings to Tally or Zoho Books. Teams report fewer reversals, faster close, and clearer dashboards. Explore AI Accountant for a working demo.

What documentation packet should I maintain per invoice to survive scrutiny?

Maintain the tax invoice, PO and GRN or service receipt evidence, proof of payment, 2B match proof or defer note, and, if applicable, RCM challan. Follow the mantra, no document, no ITC. Cross check with this GST documentation checklist.

What KPI thresholds indicate vendor education or policy changes are needed?

2B hit rate below 80% suggests supplier filing issues, deferred ITC over 15% of potential ITC indicates follow up gaps, and more than 5% of ITC reversed under 180 day rules points to payables discipline issues. For structured KPI design, see the ITC checklist eBook.