=

Key Takeaways

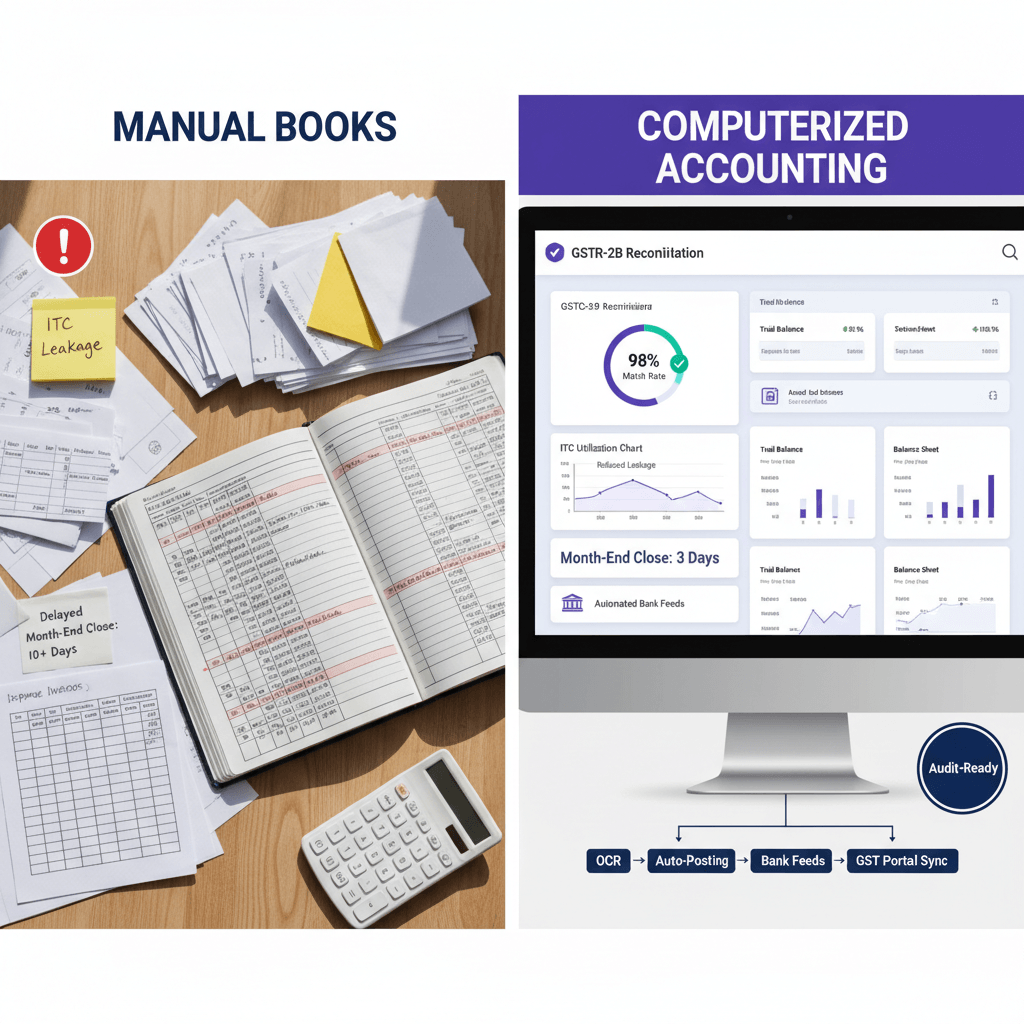

- Manual accounting relies on human entry and checks, computerized accounting automates data capture, validation, and posting. The real gap shows up when invoice volume rises, error rates compound, and ITC mismatches grow.

- GSTR-2B governs ITC availment, not 2A, and interest at 18% per annum under Section 50 of the CGST Act applies on wrongly availed credit from the date of availment.

- ITC leakage of even 1–2% on monthly purchases quietly erodes margin, and the interest on reversals increases the cost further, especially when reconciliations lag.

- Audit readiness demands transaction level trails, vendor wise ITC mapping, and edit histories that spreadsheets do not capture by default.

- The pragmatic move is a layer, not a rip and replace: keep Tally as the ledger, automate the chokepoints like AP bill ingestion, daily bank reconciliation, and GSTR-2B matching.

Computerized Accounting vs Manual Accounting: The Short Answer

Bank reconciliation and GSTR-2B matching together consume 60% of an Indian finance team’s month-end close.

Computerized accounting automates data capture, validation, and posting, while manual accounting relies on human entry at every step. The difference is most consequential on three dimensions: ITC accuracy, close speed, and audit defensibility.

Every ₹1 lakh of ITC you miss reconciling with GSTR-2B costs you ₹18,000 in interest at the statutory 18% per annum rate under Section 50 of the CGST Act CGST Act, Section 50 – GST Council. Most finance teams running manual processes do not catch these gaps until they are 60 days old.

DimensionManual AccountingComputerized AccountingData CaptureKeyed per transaction, error proneAuto ingested from bills, bank feeds, statementsITC ReconciliationPeriodic spreadsheet match, lags GSTR-2BReal time match against GSTR-2B line by lineAudit TrailManual notes or absentTimestamped edit log per transactionMonth End Close10–20 days post period3–5 days with automated matchingError RateHigh at volume, duplicates and wrong codesValidation rules flag mismatches before postingBank PostingManual narration and matchingStatement ingestion with auto reconciliationGST Interest ExposureHigh, gaps caught lateLow, mismatches surfaced at entryScalabilityDegrades with volumeScales with rules, not headcount

The most common misconception is that computerized means a new ERP. For most Indian SMBs on Tally, it means automating three manual chokepoints, bills, bank, and GSTR-2B, while Tally stays the ledger.

Manual Accounting vs Computerized Accounting: Impact On Close And ITC

The gap shows up first in close duration and ITC leakage, not in abstract capability comparisons. Fully manual teams often close 15–25 days after period end. Bottlenecks are bill entry backlogs, bank statement matching, and GSTR-2B reconciliation done in sequence rather than in parallel.

ITC Leakage Is The Biggest Rupee Consequence

CBIC Circular No. 237/31/2024-GST mandates that ITC availment be strictly as per GSTR-2B. If your process reconciles monthly or quarterly, you risk availing ITC on invoices your supplier has not filed, or missing invoices that are in 2B but not in your register. Wrongly availed ITC attracts 18% per annum interest under Section 50 of the CGST Act from the date of availment CGST Act, Section 50 – GST Council. Missed eligible ITC is lost if not claimed within the statutory limit.

Close Duration Is A Cash Flow Problem

A 20 day close means April MIS is ready around 20 May. Decisions in May, vendor payments, working capital draws, advance tax, are then based on March. Automated ingestion of bills and bank statements compresses close to 3–5 days because matching happens daily, not retrospectively.

Bank Reconciliation Is The Hidden Time Sink

Manual bank reconciliation means downloading statements, pasting into spreadsheets, and matching each line by narration. For 300 bank lines per month across two accounts, that is 4–6 hours before exception investigation. Computerized ingestion removes paste and match, your team reviews exceptions only. See the practicals in our internal guide: bank reconciliation statement automation guide.

Difference Between Computerized And Manual Accounting: A CFO-Level Comparison

Data Capture And Entry Error Rates

Manual entry introduces wrong GST codes, wrong vendor mapping, transposed amounts, and duplicates. In a 200 invoice per month AP process, even a 2% error rate means four invoices posted incorrectly, which then ripple into ITC mismatches, vendor disputes, and rework. Computerized capture reads the bill, maps fields against master data, and reduces input errors to exception review.

Approval Workflow And Duplicate Payment Risk

Manual email approvals do not enforce uniqueness checks, so the same invoice can enter twice. Computerized systems enforce invoice number level uniqueness before entry, duplicates become a flag, not a posting.

Audit Trail And GST Assessment Readiness

Assessments require transaction level traceability, vendor wise ITC reconciliation, amendment histories, and credit note mapping. Spreadsheets do not carry timestamped edit logs. Computerized systems log every edit with a timestamp and user ID by design.

AiA addresses the data capture and audit trail gap directly. AP and bills automation ingests invoices, validates GST fields, maps to Tally masters, and prepares a clean posting entry. Bank and card ingestion applies the same controls to bank lines, auto match, flag exceptions, and post confirmed entries. Your team focuses on judgement, not keystrokes.

The Break-Point: When Manual Starts Costing You

Volume Triggers By Invoice And Vendor Count

Below 75 purchase invoices per month with fewer than 30 active vendors, a disciplined weekly entry and monthly 2B reconciliation can suffice. Above 150 invoices per month, chokepoints compound, and something always slips. Above 300 invoices, manual cannot close in time to inform monthly decisions.

The ITC Leakage Math

Assume ₹10 lakh in monthly purchases at a 12% average GST rate, ₹1.2 lakh in monthly ITC. A 1.5% mismatch rate means ₹1,800 per month at risk as wrongly availed or missed. Wrongly availed ITC reversed 60 days later attracts 18% per annum interest under Section 50 of the CGST Act. Across 12 months, leakage, interest, and staff time typically exceed ₹25,000–₹30,000 even at modest volumes.

E-Invoicing And IRN Compliance

Where e-invoicing applies, invoices without valid IRN are invalid under Rule 48(5) of the CGST Rules, ITC cannot be claimed. Spreadsheet tracking is one missed update away from an ITC block. Computerized AP ingestion validates IRN at entry.

Penalties For Delayed Returns

Slow closes delay GSTR-1 and GSTR-3B, blocking buyers’ ITC and incurring late fees and interest on unpaid tax. The manual versus computerized decision is therefore a compliance risk decision, not just an efficiency choice.

Already On Tally? What Computerized Should Look Like Without A Rip And Replace

Tally Prime remains the ledger of record. The question is where to stop feeding it manually. The three highest leakage processes are AP bill entry, bank statement posting, and GSTR-2B reconciliation. Automate these layers, keep Tally intact, and eliminate the points where data quality degrades.

The Tally First Automation Workflow

Stage one, sync Tally masters, ledgers, cost centres, GST rates, into the automation layer. Stage two, ingest purchase invoices from PDFs, emails, portals, extract and validate against masters. Stage three, ingest bank and card statements and auto match. Stage four, push clean vouchers back into Tally. Your role shifts to exception review and approval, the books stay in Tally, the pre work happens outside.

GSTR-2B Reconciliation At Scale

Manual 2B reconciliation means downloading JSON, extracting to a sheet, and VLOOKUPs line by line. At 200 invoices, this takes hours and creates a backlog. Computerized reconciliation auto matches every 2B line, classifies mismatches by type, and generates a vendor wise exception queue. CBIC Circular No. 237/31/2024-GST confirms ITC eligibility is governed by 2B, structured reconciliation is the only way to enforce this at volume.

AiA is built for this workflow. Tally sync in, clean vouchers out, and 2B reconciliation that categorises every mismatch, surfacing a vendor wise queue without replacing Tally.

Controls And Review Steps To Maintain

- Exception approval: invoices that fail matching, GSTIN mismatch, duplicate flags, rate variance, must be reviewed before posting.

- Supplier follow up: mismatches surfaced by the system need vendor communication and correction.

- Bank reconciliation sign off: finance head signs off on unmatched items before close.

Rollout And ROI: A 30–60–90 Plan

Days 1–30: Pilot On One Entity

Connect Tally masters, enable AP ingestion for purchase invoices, run 2B reconciliation in parallel with your current process, and compare outputs.

KPIs at Day 30

- Invoice entry time, manual hours versus automated, target 60% reduction

- GSTR-2B mismatches identified, manual count versus automated count

- Exceptions needing human review, under 10% of invoice volume

Days 31–60: Add Bank Ingestion And Expand

Turn on bank and card ingestion, run the full month end close using the automated workflow, standardise rules for recurring exceptions.

KPIs at Day 60

- Close duration, under 7 days

- Bank reconciliation time, under 30 minutes per account per month

- Duplicate invoice flags, count and value of duplicates caught

Days 61–90: Scale And Measure ROI

Extend to all GSTINs, enable vendor wise 2B mismatch tracking, and begin supplier follow up. Calculate ITC recovered and interest avoided, add staff hours saved, subtract platform cost.

Simple ROI formula: Monthly ITC recovered + interest avoided + staff hours saved at cost rate, minus monthly platform cost. For ₹15 lakh monthly purchases at a 1.5% historical mismatch rate, ITC recovery alone is roughly ₹2,250 per month, staff time saved at 20 hours per month at ₹400 per hour is ₹8,000 per month, payback is typically under 60 days.

KPIs at Day 90

- ITC recovery rate, target 100% of eligible 2B credits availed

- Close duration, 5 days or fewer

- GSTR-2B mismatch aging, none older than 30 days

- Posting accuracy, error rate under 0.5%

Related Reading

- 2A vs 2B GST: Which One Controls Your ITC Each Month

- AI assisted audit trail: Immutable logs that auditors love

- Month-End Payables Close Checklist for CA Firms: Proven India Playbook

References

- CGST Act, Section 50 – GST Council

- CBIC Circular No. 237/31/2024-GST – cbic-gst.gov.in

FAQ

What is the fundamental difference between manual and computerized accounting for an Indian SMB?

Manual accounting records transactions through human data entry with minimal system validation, while computerized accounting captures, validates, and posts using software rules. The most material differences are higher GSTR-2B reconciliation accuracy, faster month end close, and better audit trails in computerized workflows.

If my business is on Tally Prime, does that already count as computerized accounting?

Yes as a ledger, but if purchase bills, bank lines, and GSTR-2B are still keyed and reconciled in spreadsheets, your process is effectively manual. The real shift is where automation handles data capture and matching while Tally remains the system of record.

If my GSTR-2B shows less ITC than my purchase register, which number controls?

GSTR-2B controls your availment. CBIC Circular No. 237/31/2024-GST mandates ITC strictly as per 2B. If your register shows ₹5 lakh and 2B shows ₹4.2 lakh, you can avail ₹4.2 lakh, the gap needs supplier filing or amendment.

Does interest start from the date I file GSTR-3B or the date I avail the ITC?

Interest under Section 50 applies from the date the tax was due or the ITC was wrongly availed or utilised, not the GSTR-3B filing date. See CGST Act, Section 50 – GST Council.

Can I use a spreadsheet for GSTR-2B reconciliation instead of accounting software?

You can at low volumes, but error and version control risk compound quickly. Above 100 invoices per month, manual extraction and VLOOKUPs miss matches and create reversals later. Tools like AI Accountant can auto match every 2B line, surface exceptions by type, and push only reconciled entries into Tally, reducing interest exposure and rework.

What happens if I avail more ITC than what GSTR-2B shows?

The excess is wrongly availed and must be reversed with interest at 18% per annum from the date of availment per Section 50 of the CGST Act, and CBIC guidance confirms 2B governs ITC availment.

What is the practical close-time difference for a ₹10 crore turnover business?

Manual teams typically close 15–20 days post period. With automated bill, bank, and 2B matching, close compresses to 4–7 days. The time saved comes from eliminating batch entry and sequential reconciliations.

At what turnover or volume does manual become risky for GST compliance?

Risk correlates with transaction volume, not turnover alone. Above ~150 purchase invoices per month, manual 2B reconciliation becomes unreliable. Businesses above ₹5 crore often cross this threshold, and those under can still face risk if invoice counts are high.

How does missing GSTR-2B reconciliation for one month affect my annual ITC position?

That month’s availed ITC may not align with 2B. Wrongly availed portions are reversed with 18% per annum interest from the date of availment. Missed eligible ITC can be permanently lost if time limits pass. A single miss is recoverable, repeated misses become material.

How does computerized accounting help in a GST audit versus manual?

Computerized systems produce vendor wise ITC tie outs, invoice trails, and edit histories on demand, whereas manual processes require reconstruction from emails and sheets, which introduces gaps. Auditors prefer structured, timestamped logs that systems generate by default.

If I automate AP and bank in a third-party tool, are my Tally books still the official records?

Yes. As long as approved entries are posted into Tally and filings draw data from Tally, it remains the book of record. The automation layer pre processes and reconciles, it does not replace the ledger.

Can GSTR-2B reconciliation be handled for multiple GSTINs in one place?

Yes. Modern tools reconcile per GSTIN while presenting a consolidated exception queue. Manual multi GSTIN spreadsheets are error prone and slow to audit.

What is the difference between GSTR-2A and GSTR-2B, and why does it matter?

2A is dynamic and updates with supplier filings, 2B is a static monthly statement generated on a cut off date. CBIC guidance makes 2B the basis for ITC availment, so entries visible in 2A but not yet in 2B cannot be availed that month.

How do credit notes and debit notes affect 2B reconciliation in practice?

Supplier credit notes reduce ITC and appear as negative lines in 2B. In manual setups, matching them to purchase returns and reversal entries is often delayed. Computerized reconciliation flags these as a separate queue so you reverse in the same GSTR-3B cycle.

Is data loss risk higher in computerized systems than in manual records?

System risks exist, outages and corruption, but reputable platforms maintain backups, access logs, and version histories that paper or ad hoc spreadsheets lack. The net risk, with standard controls, is lower than a person dependent manual setup.

How do I measure if my automation pilot is working before full rollout?

Track three numbers: reconciliation coverage above 85%, exception rate under 15% with genuine mismatches, and time to close under 7 days. If you miss these, fix master data quality first, then re test. With AI Accountant, most pilots exceed these thresholds in month one.

How do I build an ROI case for the founder or board?

Use a single monthly figure: purchases × mismatch rate × 18% annualised interest risk, plus staff hours × cost rate, minus platform fee. Present it as monthly leakage stopped, not generic productivity.

What data do I need to start an AP automation pilot?

A Tally master export, 30–50 recent purchase invoices in PDF or image format, and the latest GSTR-2B JSON. With these, a tool like AI Accountant can demonstrate extraction accuracy, match rates, and exception queues within days.

Do I need to replace my ERP to get the benefits of computerized accounting?

No. For most Tally users, layering AP ingestion, daily bank matching, and line by line GSTR-2B reconciliation delivers the benefits, while Tally stays the book of record. Rip and replace is unnecessary for these outcomes.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.