Key Takeaways

- GSTR-2B is the static, period-locked ITC control for each month, generated on the 12th and used to decide what you can claim in GSTR-3B.

- GSTR-2A is dynamic and rolls in real time, useful for chasing vendor filings, not for booking monthly ITC.

- If an invoice is in 2A but missing in 2B, the ITC is ineligible for that month, claiming and utilising it risks 24% per annum interest under Section 50(3).

- Late GSTR-1 filing pushes the invoice to the next month’s 2B, the 12th is a hard cut-off.

- Rule 37A can force reversal even after 2B confirmation if the supplier fails to file GSTR-3B by 30 September of the following financial year, you can re-avail after they file.

2A vs 2B GST: The Difference, Explained

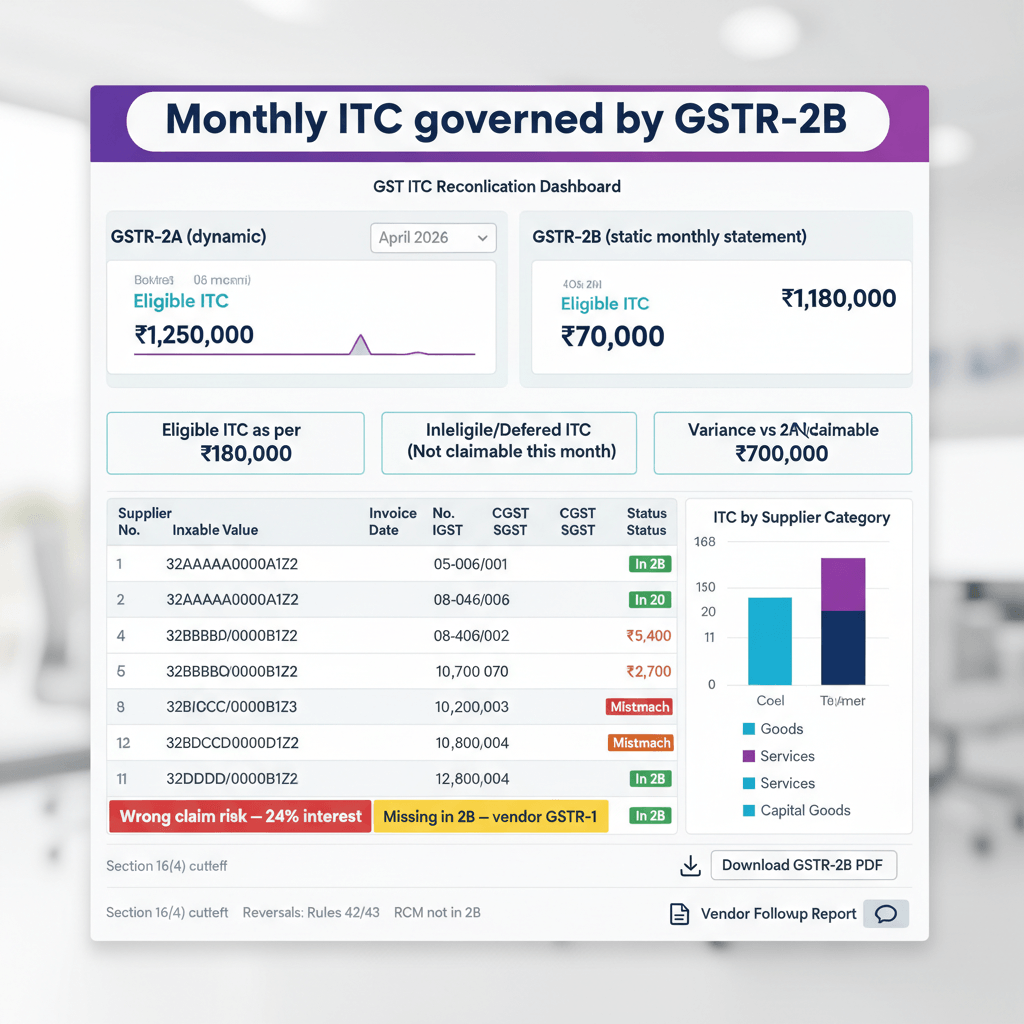

GSTR-2B is your locked, period-specific statement for Input Tax Credit availment, while GSTR-2A is a continuously updating mirror of supplier filings. Treat 2B as the monthly truth for GSTR-3B and 2A as your vendor follow-up dashboard.

- Nature: 2A is dynamic and updates whenever a supplier files or amends, 2B is static after the 12th.

- Use case: 2A for chasing vendors, 2B for booking ITC.

- Cut-off: Only filings up to the 12th feed into that month’s 2B, as explained in GSTN Help — GSTR-2B.

The operating rule: Claim what is in 2B, chase what is in 2A but not in 2B, block everything else.

Which Document Controls Your ITC Each Month?

GSTR-2B controls monthly ITC. Section 16(2)(aa) links ITC to supplier-reported invoices communicated to the recipient, operationalised via 2B. Booking ITC from 2A without 2B confirmation exposes you to 24% per annum interest under Section 50(3) if the credit is availed and utilised.

The 2B vs 2A rule in one line

Claim what is in 2B, chase what is in 2A but not in 2B, block everything else.

Example: You purchase ₹10 lakh of goods in October. The supplier files GSTR-1 on 15 November. October’s 2B, generated on 12 November, does not include this invoice. 2A shows it from 15 November. Claiming ₹1.8 lakh IGST in October is premature. Wait for November’s 2B, then claim.

Why the interest makes this non-negotiable

Wrongly availed and utilised ITC attracts 24% per annum under Section 50(3). On ₹10 lakh of ineligible ITC for 60 days, interest is roughly ₹40,000, before penalties. Waiting one cycle is cheaper than funding interest.

Does 2A have any role in close?

Yes, a single role. Run a post-12th comparison to escalate vendors for invoices visible in 2A but missing in 2B. Map each gap to a root cause, late GSTR-1, skipped IFF, import timing, or data error. Most will land in the next 2B.

What Exactly Shows Up In 2A And 2B, And When?

2B is generated monthly on the 12th, pulling all supplier filings up to that cut-off, as per GSTN Help — GSTR-2B. 2A updates as and when suppliers file, amend, or upload invoices.

What feeds into GSTR-2B

- GSTR-1 filed by monthly suppliers on or before the 11th.

- IFF from QRMP taxpayers for the first two months of a quarter, window closes on the 13th, as outlined in GSTN Help — QRMP Scheme.

- GSTR-5 for non-resident taxable persons.

- GSTR-6 for ISD distributions.

- ICEGATE import data for IGST on Bills of Entry.

If any of the above are filed after the 12th, the entries move to the following month’s 2B. This next-month rule for late GSTR-1 was confirmed in GSTN Advisory — August 2020.

A worked example for a ₹2 crore monthly ITC pool

October’s 2B shows ₹1.8 crore eligible ITC, while 2A shows ₹2.1 crore. The ₹30 lakh gap breaks down as ₹18 lakh from vendors who filed GSTR-1 on 13–15 November, hence next month’s 2B, ₹8 lakh from a QRMP vendor who skipped IFF, waiting for quarterly GSTR-1, and ₹4 lakh from import BoEs still syncing from ICEGATE. Book ₹1.8 crore, park ₹30 lakh, and escalate vendors.

Operational Rulebook: Claiming, Reversing, And Re-Availing ITC Using 2B

Your month-end ITC close has three moves, claim what 2B confirms, block what 2B excludes, and track reversals under Rule 37 and Rule 37A.

Step 1 — Claim only what is in 2B

After the 12th, download 2B and match it to your purchase register line by line. Post only matched, eligible entries to GSTR-3B Table 4(A). Nothing else. If five invoices are missing from 2B, park those credits.

Step 2 — Block and track missing credits

Maintain a pending ITC ledger for invoices absent from 2B, capturing vendor name, invoice details, tax amount, and reason for absence. Monitor the Section 16(4) cut-off of 30 November after the FY close. If an invoice never hits any 2B before that date, the credit is permanently lost.

Step 3 — Apply Rule 37 and Rule 37A reversals

- Rule 37, 180-day payment condition: If you have not paid the supplier within 180 days, reverse ITC in Table 4(B)(2) and pay interest under Section 50(3). Re-avail once you pay.

- Rule 37A, supplier GSTR-3B default: If the supplier fails to file GSTR-3B by 30 September following the FY of availment, reverse in October’s GSTR-3B. Re-avail after they file.

Edge Cases That Create 2A vs 2B Gaps

QRMP suppliers and IFF timing

IFF invoices appear in your 2B only if uploaded by the 13th. If your QRMP supplier skips IFF, invoices wait until quarterly GSTR-1, as per GSTN Help — QRMP Scheme. For the third month of a quarter there is no IFF, invoices always wait for quarterly GSTR-1.

Late GSTR-1 and the next-month rule

Monthly suppliers who file GSTR-1 after the 11th push invoices to the next month’s 2B. The 12th cut-off is binary, see GSTN Advisory — August 2020.

Imports of goods via ICEGATE

IGST on imports comes via ICEGATE and appears in 2B in the month the BoE is processed. Port or volume delays often shift entries to the next month, so reconcile BoE numbers against 2B and ICEGATE acknowledgements.

RCM supplies in 2B

RCM entries in 2B are informational. You must first pay the RCM tax in cash through GSTR-3B Table 3.1(d). Only then can you claim the corresponding ITC in Table 4(A)(3).

ISD credits

ISD allocations flow through the ISD’s GSTR-6, subject to the same 12th cut-off. Late GSTR-6 shifts credit to the next 2B. Match ISD allocation memos to 2B before booking.

Month-End Close Checklist To Make 2B Your Single Source Of Truth

Lock your process to calendar dates published on the GSTN Portal, and keep internal cut-offs one day tighter than statutory ones.

- 12th, download 2B and export the purchase register for the month.

- 13th–15th, match 2B against the register, tag each variance by cause.

- 15th–17th, post only matched, eligible ITC to your 3B draft.

- By the 18th, move unmatched invoices to a pending ITC ledger and issue vendor follow-ups, apply Rule 37 reversals crossing 180 days.

- File GSTR-3B by the due date, monthly filers by the 20th, QRMP by the 22nd or 24th, depending on state.

Build a September–October calendar for Rule 37A. Before 30 September, check whether suppliers whose ITC you availed in the prior FY have filed GSTR-3B. Reverse in October if they have not, re-avail after they file.

References

- GSTN Advisory — August 2020, treatment of late GSTR-1 and 2B generation.

- GSTN Help — GSTR-2B, generation schedule, sources including ICEGATE and ISD.

- GSTN Help — QRMP Scheme, IFF timelines and impact on recipient 2B.

- CBIC Circular 246/03/2025 — 30 January 2025, additional compliance references.

FAQ

What is the main difference between GSTR-2A and GSTR-2B for monthly ITC?

GSTR-2A is dynamic and updates whenever suppliers file or amend, GSTR-2B is static and generated on the 12th. For ITC booking in GSTR-3B, 2B is the controlling statement each month, while 2A is best used to chase vendor filings.

Can I claim ITC shown in 2A if it is not yet in 2B for the same month?

No. Section 16(2)(aa) requires communication of invoice details to the recipient, which GSTN implements through 2B. Claiming and utilising such ITC before it appears in 2B can trigger 24% per annum interest under Section 50(3). Wait for the invoice to land in a future 2B, then claim.

What interest applies if I wrongly avail and utilise ITC not reflected in 2B?

Section 50(3) levies 24% per annum on ITC wrongly availed and utilised, calculated from the date of utilisation. For example, on ₹5 lakh for 90 days, interest is about ₹30,000, exclusive of any penalty.

How do QRMP suppliers change my 2A vs 2B reconciliation?

QRMP suppliers can upload invoices through IFF by the 13th for the first two months of a quarter. If they skip IFF, those invoices only appear after quarterly GSTR-1, which can be up to three months later. Expect timing gaps in 2B and plan cash flows accordingly.

When must I reverse ITC under Rule 37A, even if the invoice appeared in my 2B?

If the supplier fails to file GSTR-3B by 30 September following the FY in which you availed the ITC, you must reverse the credit in October’s GSTR-3B. You can re-avail once the supplier files their GSTR-3B. This check is calendar driven, not 2B driven.

How should I treat RCM entries that show up in 2B?

They are informational. You can claim ITC on RCM only after paying the RCM tax in cash through GSTR-3B. Do not book RCM ITC merely because the supply appears in 2B.

What should I do if a vendor insists they filed GSTR-1, but the invoice is not in my 2B?

Request the ARN and filing date. If they filed after the 12th, the invoice will appear in next month’s 2B. If they filed before the 12th and it is still missing, ask them to check for errors in GSTIN, invoice number, or period, and file an amendment.

Does filing GSTR-3B late affect ITC already visible in my 2B?

ITC eligibility remains, but late filing attracts late fees. Ensure you still meet the Section 16(4) deadline of 30 November after the FY, otherwise the ITC is lost permanently.

How do I reconcile import IGST in 2B with my books?

Match each Bill of Entry number against ICEGATE acknowledgements and your purchase register. Expect timing shifts when ICEGATE processing crosses month end, the entry will land in the 2B of the processing month, not necessarily the BoE date.

What is a practical way to operationalise these rules with an AI accounting tool?

Upload your GSTR-2B and purchase register to an AI reconciliation workflow, have it auto-categorise gaps into late GSTR-1, QRMP IFF misses, import timing, or data errors, generate the journal entries for booked, blocked, reversed, and re-availed ITC, and create vendor follow-up queues so your 2B claim is clean by the 20th. This cuts interest risk and prevents Section 16(4) write-offs.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.