Key takeaways

- Indian SMEs are uniquely exposed to vendor payment fraud due to manual processes, informal vendor onboarding, and mixed payment rails like cheques, NEFT, and UPI.

- Common schemes include ghost vendors, Duplicate invoicing, invoice manipulation, and kickbacks that exploit approval gaps and threshold limits.

- Red flags span vendor master anomalies, invoice irregularities, and payment pattern outliers, for example similar addresses, round number bills, and repeated just-below-limit payments.

- Controls that work: Three way matching, segregation of duties, robust Vendor verification, and continuous transaction monitoring.

- AI and ML can learn your company’s normal patterns, then flag anomalies across invoices, approvals, and GST data, reducing manual review without slowing AP.

- Start with quick wins like duplicate payment sweeps and vendor master cleanups, then scale to automated matching, risk scoring, and advanced analytics.

- Measure ROI using detection rates, loss reduction, faster detection times, and improved vendor master data quality.

Understanding vendor payment fraud patterns in Indian SMEs

What makes Indian businesses vulnerable

Heavy reliance on manual approvals, Excel trackers, and email based invoice flows creates blind spots that fraudsters exploit. Informal vendor relationships, seasonal vendors, and WhatsApp based onboarding increase the risk surface. With mixed payment modes and GST complexity, gaps appear that criminals turn into siphons.

When process speed is prioritized over verification discipline, small gaps become expensive pipelines. Tighten data, not just deadlines.

Most common vendor fraud schemes

Ghost vendors and shell companies

Fake suppliers are added to the vendor master, often with convincing PAN and GST details, then drip-feed small invoices under approval limits.

Duplicate invoicing and inflated billing

Duplicates slip through during busy cycles, while subtle quantity or rate inflation accumulates into large overpayments.

Invoice manipulation

PDFs are altered to change bank accounts or amounts, with faked supporting documents like challans and GRNs to create a convincing trail.

Kickbacks and collusion

Employees steer business to favored vendors, approve inflated rates, or bypass procurement norms in exchange for personal benefits.

Red flags and warning signs across vendor data

Vendor master file anomalies

- Incomplete KYC, missing GST or PAN, personal email domains, or residential addresses.

- Multiple vendors sharing addresses, phones, or bank accounts.

- Vendors created during month end rushes, or created, used briefly, then dormant.

- Names mimicking legitimate suppliers, for example “ABC Traders” versus “ABC Trading”.

Invoice level indicators

- Round number invoices like Rs. 50,000 or Rs. 99,999, or number sequences that jump and reset.

- Weekend or holiday invoice dates, inconsistent logos or formats, vague descriptions.

- Delayed submissions, clusters of same-day invoices, or invoices raised just after PO creation.

Payment data irregularities

- Frequent bank account changes or multiple accounts per vendor.

- Repeated just-below-approval-limit payments, or unusually fast payments to specific vendors.

- Geographic mismatches between service locations and vendor bases.

- Spikes during audits, quarter close, or employee exit periods.

Essential fraud detection techniques and controls

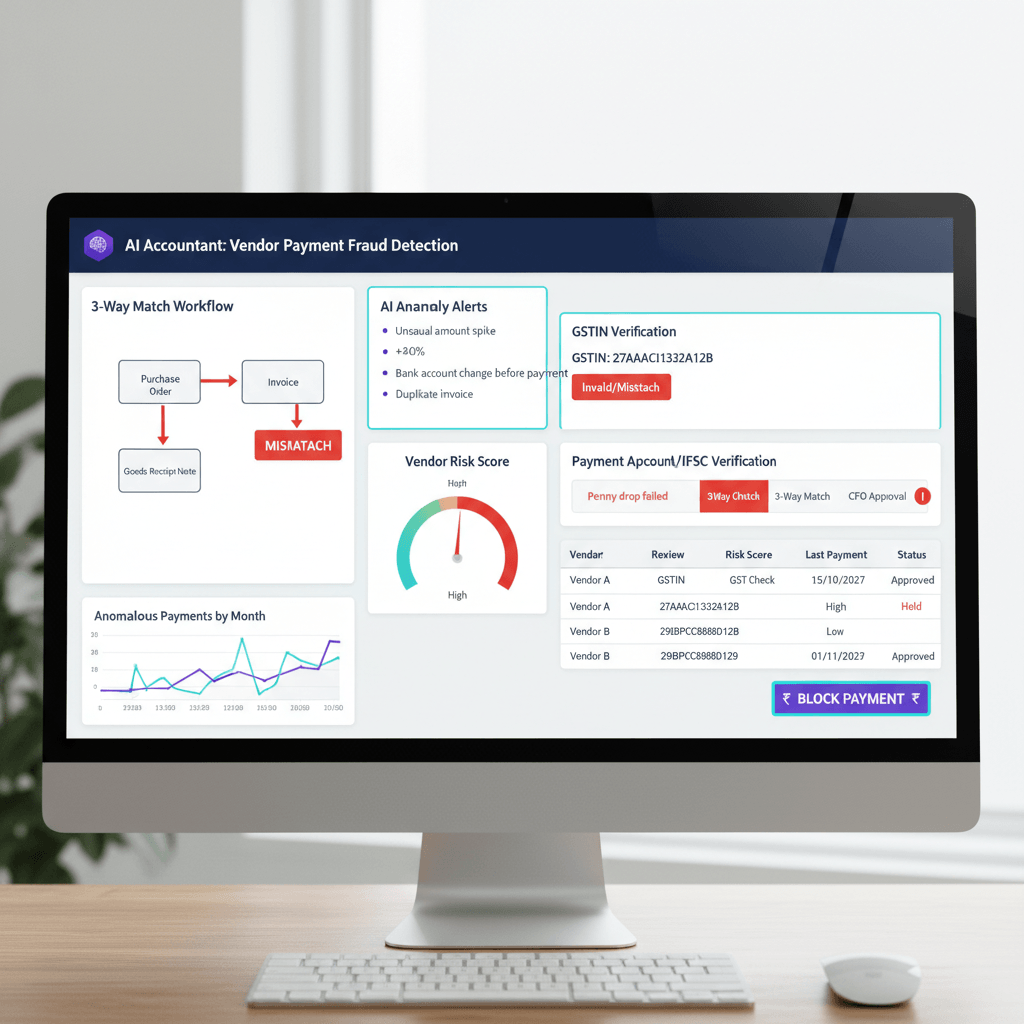

Three way matching implementation

Make matching mandatory above a defined threshold, compare PO, GRN, and invoice systematically, and adapt for services using completion certificates or approved timesheets. Use checklists to confirm quantities, rates, and terms before payment, then automate wherever possible to reduce manual fatigue.

Segregation of duties framework

Split vendor creation, invoice entry, approval, and payment across different people. In small teams, use maker checker, owner approvals for high risk actions, surprise audits, and rotation of duties to mitigate collusion risks.

Vendor verification protocols

Standardize onboarding with GSTIN and PAN verification, bank account penny-drop checks, and site or video verification for significant vendors. Confirm GST activity status and filing history, and validate entity type alignment between documents and registrations.

Transaction monitoring systems

Set alerts for velocity spikes, dormant vendor reactivation, and payment timing anomalies. Apply Benford’s Law to detect unnatural number patterns, and build vendor scorecards that track returns, complaints, and override frequency.

Automated payment reminders and approval notifications also help strengthen payment controls by ensuring invoices move through the right workflow instead of relying on manual follow-ups. A structured reminder system reduces last-minute approvals, rushed payments, and the risk of bypassing established verification checks.

Technology solutions for automated fraud prevention

AI powered anomaly detection

AI models learn normal behaviors across vendors, amounts, invoice formats, and approval paths, then flag deviations early. They spot subtle, cross month patterns that humans miss, and adapt as your volumes and seasonality change.

Machine learning applications

ML assigns fraud probability scores using many signals, improves from feedback, and predicts high risk vendors for preemptive controls. NLP can scan descriptions and emails for vague wording or sudden communication shifts that often precede fraud.

Automation tools and platforms

AI Accountant automates matching, monitors vendor patterns, reconciles GST data, and integrates with Tally and Zoho Books to surface anomalies natively. QuickBooks adds audit trails and duplicate detection, Xero strengthens approval workflows, SAP Concur excels in expense and invoice controls, FreshBooks supports basic verification for small teams, and Tally Prime pairs well with add-ons for reconciliation and alerts.

Integration with existing systems

Use API based sync so vendor additions and invoices are risk scored instantly, standardize data formats for reliable comparisons, and maintain complete audit trails of changes, approvals, and overrides across ERP and accounting systems.

Building a comprehensive fraud prevention framework

Risk assessment methodology

Document the end-to-end process, identify high frequency and high value risk points, quantify exposure, and evaluate collusion risks through relationship mapping and duty overlaps.

Internal controls implementation

Design approval matrices by risk, not just amount. Enforce documentation for overrides and emergency payments, build redundancy for critical checks, rotate duties, and communicate that monitoring is active and continuous.

Continuous monitoring strategies

Daily scans for high risk actions, weekly pattern reviews, monthly deep dives on vendor concentration and duplicates, and quarterly control effectiveness assessments. Dashboards make exceptions visible at a glance.

Team training and awareness

Provide role based training, clear escalation paths, anonymous reporting, and recurring refreshers. Promote healthy skepticism that protects the company, not finger pointing that stalls work.

Vendor fraud case studies and examples

Indian SME fraud incidents

Ghost vendors siphoned Rs. 67 lakhs by exploiting approval limits, invoice manipulation diverted payments through edited PDFs in a Pune firm, and a kickback scheme inflated prices by 20 to 30 percent for years in a retail chain until analytics exposed the pattern.

Lessons learned from real cases

- Approval thresholds alone do not stop split invoices, automated similarity checks on vendor names and periodic audits help.

- Start small is the norm for fraudsters, continuous monitoring catches escalation early.

- Manual and disconnected systems are prime targets, even basic automation closes critical gaps.

- Always verify changes with the vendor directly, especially bank details and addresses.

- Leadership tone matters, visible commitment reduces incidents and increases reporting.

Implementation roadmap

Quick wins and immediate actions

- Run a six month duplicate payment sweep, investigate matches by number, date, or amount.

- Enforce a vendor KYC checklist immediately, with GST, PAN, and bank verifications.

- Track all vendor master changes in a single log, require callback confirmation for bank updates.

- Deactivate dormant vendors and clean obvious anomalies from the master.

- Enable payment alerts above a chosen threshold to widen oversight.

- Hold a weekly 30 minute exceptions meeting to review unusual items.

Short term enhancements

- Deploy automated or template based three way matching above set thresholds.

- Implement maker checker and duty segregation across onboarding, entry, approval, and payment.

- Introduce vendor risk scores and tailor approval rigor by risk tier.

- Start a monthly vendor audit program with documentation and call backs.

- Integrate accounting, ERP, and fraud tooling for unified oversight.

- Train the finance team using your live data to spot red flags.

Long term strategic initiatives

- Adopt a company wide fraud risk framework for all disbursements.

- Scale analytics and ML to detect evolving schemes without adding headcount.

- Define and rehearse a fraud response plan, from investigation to recovery.

- Build structured vendor relationship management and performance scorecards.

- Invest in culture, communication, and insurance to mitigate residual risk.

Measuring success and ROI

Key performance indicators

- Monthly suspicious transaction detections and confirmed cases.

- Fraud loss rate as a share of total payments, target below 0.5 percent.

- Average time to detect and contain incidents, aim within 30 days.

- Vendor master completeness rates and dormant vendor counts.

- Override and exception processing rates to gauge control health.

- Training coverage, reported concerns, and assessment scores.

Cost benefit analysis

Quantify direct loss reductions, add avoided legal and investigation costs, factor productivity gains from automation, include benefits from better vendor terms and fewer disputes, and compare annual spend on tools and training with prevented losses for a clear multiple on ROI.

Conclusion

Vendor payment fraud is preventable with disciplined processes, vigilant teams, and smart technology. Start with small, high impact steps, embed robust verification and matching, then layer continuous monitoring and AI to scale protection without throttling AP throughput. The cost of prevention is consistently lower than the cost of fraud, in rupees and in reputation.

FAQ

How can a small finance team in India detect duplicate invoices in Tally without slowing down payments?

Run periodic exports of the purchase register and use pivot or fuzzy matching to catch repeats by number, date, and amount, then add an automated layer by connecting Tally to an AI tool like AI Accountant that scans for near duplicates, vendor lookalikes, and just-below-threshold splits before payment.

What is three way matching and how do I automate it for services and GST scenarios?

Three way matching compares PO, GRN or service confirmation, and invoice. For services, replace GRN with a completion certificate or approved timesheets. Tools such as AI Accountant can auto-extract, align tax components, and flag mismatches in quantities, rates, and GST treatment.

How do I verify a vendor’s GSTIN and PAN quickly during onboarding?

Validate GSTIN against the GST portal to confirm legal name, address, and active status, then cross-check PAN entity type. Automate this using penny-drop bank checks and API lookups through AI Accountant so AP only approves vendors with clean, consistent KYC.

What red flags in the vendor master indicate ghost vendors or collusion?

Shared addresses or bank accounts across vendors, personal email domains, sequential vendor codes created in bursts, and vendors added during month end. An AI layer like AI Accountant scores such anomalies and pushes them for review.

How should I handle vendor bank account change requests securely?

Never accept changes via email alone, enforce a call back to a verified number on record, require a cancelled cheque and penny-drop verification, and log approvals. Integrations with AI Accountant can block payments until verification clears.

How do I detect invoice inflation when line items and rates look legitimate?

Benchmark current rates versus historical averages and market quotes, watch for gradual drifts, and track approver patterns that always clear the same vendor. ML models in AI Accountant compute anomaly scores for subtle overbilling.

Can Benford’s Law help catch manipulated invoices in Indian AP data?

Yes, natural financial data follow predictable leading digit distributions. Significant deviations suggest manual tampering or fabricated numbers. AI Accountant applies this test at scale and combines it with vendor behavior signals for stronger accuracy.

What controls can a two-person finance team implement for segregation of duties?

Use maker checker for vendor creation and payment runs, owner approval for high risk vendors and thresholds, weekly cross-review, and monthly surprise audits. Automations in AI Accountant enforce approvals and keep immutable audit trails.

How do I align AP fraud checks with GST compliance, for example GSTR-2B reconciliation?

Auto-match vendor invoices with GSTR-2B to confirm reporting, tax amounts, and vendor status. AI Accountant flags mismatches, inactive vendors, and ITC risks while simultaneously scanning for duplicate or manipulated invoices.

Which KPIs should a CFO track to measure the effectiveness of AP fraud prevention?

Monitor detection rate, confirmed loss rate, average time-to-detect, vendor master completeness, override frequency, and training participation. Dashboards in tools like AI Accountant consolidate these metrics for monthly reviews.

How do I integrate Tally or Zoho Books with an AI fraud tool without heavy IT lift?

Use plug-and-play connectors or APIs offered by platforms such as AI Accountant, sync vendor masters, invoices, and payments, then enable anomaly scoring and alerting directly within your existing workflow.

What is the fastest way to start catching fraud this month without buying new software?

Run a duplicate payment sweep, deactivate dormant vendors, enforce callback verification for bank changes, and set a weekly exceptions huddle. Then pilot a low-cost trial of AI Accountant to automate the highest value checks with minimal disruption.