-01%201.svg)

Key takeaways

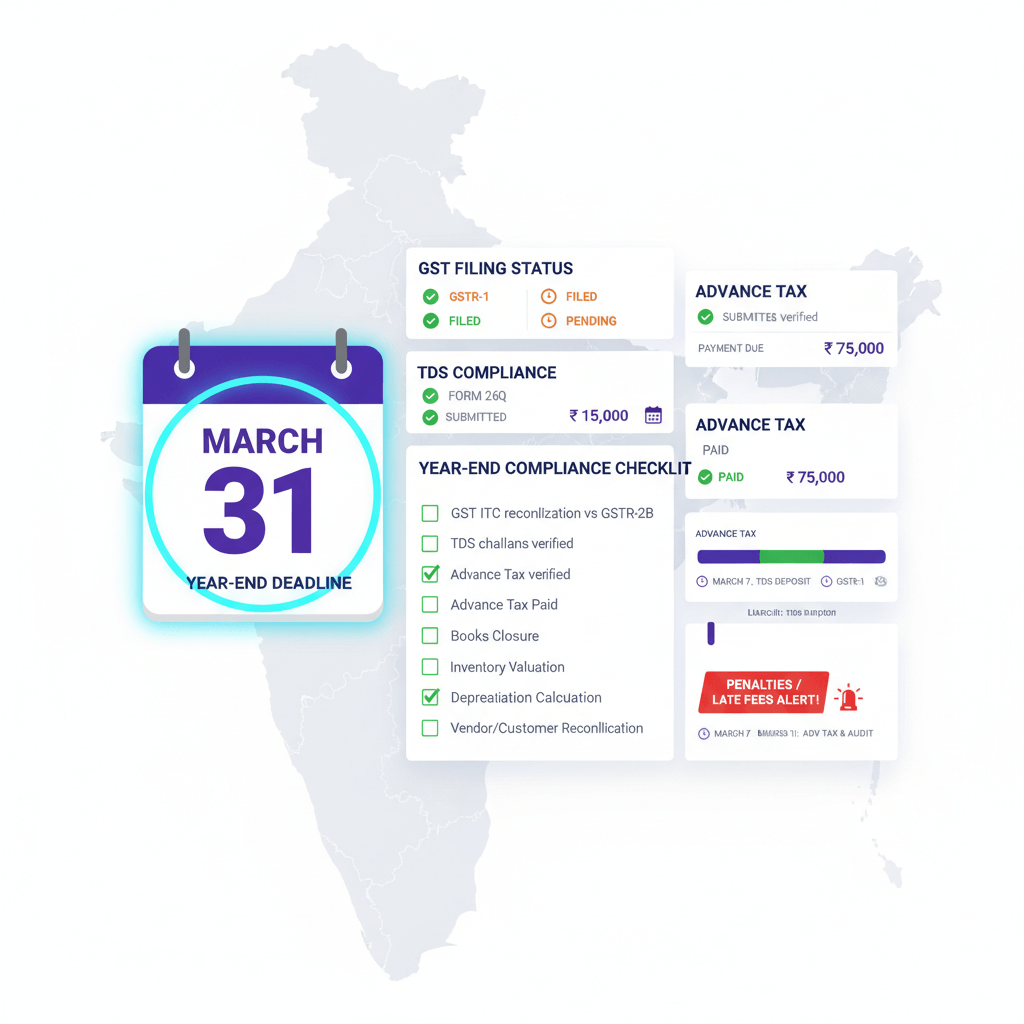

- Missing the April 30 TDS deposit deadline triggers ₹200 daily late fee under Section 234E, plus 1.5% monthly interest, March TDS enjoys an extended timeline but the penalty clock is unforgiving.

- Section 43B(h) disallows unpaid MSME vendor invoices unless cleared before your ITR filing date, a single slip can inflate tax by lakhs.

- Advance tax shortfalls below 90% attract 1% monthly interest from April 1, making the June 15 first instalment critical for cash flow planning.

- GST ITC claims for FY 2023-24 expire on November 30, 2024, or the annual return date, reconciliation after March 31 becomes harder to fix.

Body

What are the critical tax deadlines for Indian SMEs with a March 31 year-end?

For FY 2023-24, your immediate deadlines include: TDS deposit for March deductions by April 30, Q4 TDS returns, Forms 24Q and 26Q, by May 31, and Form 16 issuance by June 15. First advance tax instalment of 15% is due June 15, with subsequent instalments on September 15, 45% cumulative, December 15, 75%, and March 15, 100%. GST ITC claims expire November 30, 2024 or by annual return date. Virtual Accounting by AI Accountant tracks these deadlines automatically and sends alerts 7 days before each due date.

You are three weeks away from year-end, surrounded by invoices, wondering which ones you can still claim and which deadlines will hit you with penalties if missed. The difference between getting your March 31 tax planning right and wrong is not just money, it is the cascading effect of one missed deadline triggering penalties, interest charges, and disallowed deductions that compound into the next financial year.

This guide walks you through every critical deadline, penalty threshold, and last-minute tax move for Indian SMEs, with exact dates, penalty amounts, and what you can still fix before March 31.

Understanding March 31 Tax Implications for Indian SMEs

March 31 is not just a date on the calendar, it is the moment when every financial decision you made in the past year crystallizes into either a tax deduction or a disallowed expense. For SMEs operating on thin margins, the tax implications of year-end decisions can mean the difference between reinvesting profits and scrambling for working capital to pay unexpected tax bills.

The complexity comes from multiple overlapping compliance systems. Income tax follows one set of rules with advance tax, TDS, and deduction timelines. GST operates on its own monthly cycle with annual reconciliations. Add statutory compliances like PF and ESI, and you are juggling three different deadline calendars, each with its own penalty structure.

What makes March 31 different for SMEs vs large companies?

SMEs face three unique challenges at year-end. First, you likely do not have a full-time CFO tracking every compliance date, the founder or a part timer manages it. If you are exploring online bookkeeping services to close year-end cleanly, compare options that can own deadlines and reconciliations end to end. Second, your cash flow timing matters more because you cannot absorb penalties the way larger companies can. Third, many SME specific benefits like Section 44AD presumptive taxation or composition schemes have year-end elections that cannot be changed mid year.

The stakes are higher because errors compound. Miss your advance tax payment and you face both interest under Sections 234B and 234C. Delay vendor payments to manage cash flow and Section 43B(h) disallows the entire expense. File GST returns late and you lose input tax credit permanently after the November cutoff.

How do tax year-end timelines intersect with GST obligations?

Your income tax year ends March 31, but GST continues its monthly march. GSTR-3B for March is due April 20, with late fees of ₹50 per day for non nil returns, ₹25 CGST plus ₹25 SGST, capped based on turnover, ₹2,000 maximum if your turnover is below ₹1.5 crore. Miss this and you cannot file subsequent returns, creating a cascade effect.

The real complexity emerges in reconciliation. Your GST credits claimed throughout the year must match your books for the income tax return. Any mismatch discovered after March 31 requires amendments in both systems, triggering interest charges and potential scrutiny from both departments.

Warning: GST ITC reversals discovered after March 31 create double jeopardy, you lose the GST credit and potentially face income tax additions if expenses are disallowed due to missing GST compliance.

The trick is understanding that while these are separate systems, they watch each other’s data.

Critical Tax Deadlines and Compliance Requirements, April to June

The 90 days following March 31 contain more compliance deadlines than any other quarter, and missing even one can trigger a domino effect of penalties that extends into the next financial year.

Your immediate priority is the April 30 deadline for March salary TDS deposits. Unlike other months where TDS is due by the 7th, March gets special treatment with an extended timeline. But this apparent grace period is deceptive, any delay beyond April 30 attracts ₹200 per day under Section 234E, capped at the TDS amount, plus 1.5% monthly interest under Section 201(1A).

Following close behind are your Q4 TDS returns. Forms 24Q, salaries, 26Q, non salary, and 27Q, NRI payments, must be filed by May 31, with Form 16 issuance to employees required by June 15. Missing these dates attracts penalties from ₹10,000 to ₹1 lakh under Section 271H for incorrect returns.

When are advance tax instalments due for FY 2024-25?

Advance tax instalments follow a rigid schedule that starts just 15 days into the new financial year. The threshold is ₹10,000 in estimated tax liability, if your total tax exceeds this after TDS credits, you must pay:

| Instalment | Due Date | Cumulative Amount |

|---|---|---|

| First | June 15 | 15% of annual tax |

| Second | September 15 | 45% of annual tax |

| Third | December 15 | 75% of annual tax |

| Fourth | March 15 | 100% of annual tax |

Missing these triggers two types of interest. Section 234B charges 1% monthly on shortfalls where less than 90% of assessed tax is paid. Section 234C charges 1% monthly on specific instalment shortfalls, for example if you pay only 10% by June 15, you owe interest on the 5% shortfall for three months until the next instalment.

Which GST obligations continue after March 31?

GST deadlines do not pause for your income tax year-end. For businesses exceeding the threshold, e-invoicing continues without interruption. The system watches for any gap in sequential invoice numbers, and missing entries can trigger automated notices months later.

Exporters must file their Letter of Undertaking, LUT, renewal by July 31 for the new financial year. This annual requirement allows zero rated exports without paying IGST, miss the deadline and you are forced to pay IGST on all exports until renewed, locking up working capital.

For composition dealers, the April 30 deadline to opt in or opt out using Form CMP-02 is absolute. Once you miss this window, you are locked into your current status for the entire year. With limits of ₹1.5 crore for traders and ₹50 lakh for service providers, crossing these thresholds mid year without proper planning can force you out of the scheme retrospectively.

But here is what keeps founders up at night, you have done all this correctly, yet one more rule change could still disallow your deductions.

Section 43B(h) and MSME Payment Requirements

Section 43B(h) is the single most expensive compliance trap for SMEs, effective from FY 2023-24, any amount payable to MSME vendors gets disallowed as a deduction if not paid within statutory timelines.

The rule is brutal in its simplicity. If your vendor is registered as an MSME and you have not paid them within 45 days, or 15 days without a written agreement, you cannot claim that expense as a deduction unless you clear it before filing your income tax return. The law does not care if you have been doing business with them for years, if there is a commercial dispute, or if your own customers have not paid you.

Here is what catches SME owners off guard, the timeline starts from delivery or acceptance, whichever is earlier. A vendor who delivered goods on February 15 but whose invoice you received on March 1 still has a due date of April 1, 45 days from February 15. Miss this date and that entire purchase amount becomes non deductible until paid.

How to verify if a vendor qualifies as MSME

A vendor is an MSME only if they have valid Udyam Registration. The thresholds are investment up to ₹10 crore and turnover up to ₹50 crore for small enterprises, and investment up to ₹1 crore with turnover up to ₹5 crore for micro enterprises. What matters is having the Udyam Registration Number, not the old Udyog Aadhaar Memorandum.

You can verify any vendor's MSME status on the Udyam portal using their registration number. Print these verification reports for every MSME vendor and file them with your purchase invoices.

Critical Documentation Checklist:

- Udyam Registration Certificate showing valid URN

- Written payment terms agreement, to extend to 45 days

- Proof of delivery or acceptance date for each invoice

- Payment bank statements showing clearance date

Without this documentation trail, tax officers can disallow the entire expense during assessment, even if you paid within time.

What are the penalties under MSMED Act Section 16?

Beyond the tax disallowance, the MSMED Act Section 16 imposes interest at three times the bank base rate, commonly around 24% annually, on delayed payments. This compounds monthly until payment.

The interest becomes payable from the day after the due date. For a ₹10 lakh pending payment, you are looking at significant MSME interest, plus the entire ₹10 lakh becoming non deductible for tax purposes. This double whammy can effectively cost you lakhs on a single invoice, lost tax deduction at 30% rate plus additional interest charges.

This is where Virtual Accounting by AI Accountant proves invaluable, tracking all MSME vendor payment due dates in real time, flagging purchases approaching the 45 day threshold before they become non deductible. The system pulls Udyam verification automatically and creates audit trails for every MSME transaction. Use our buyer’s checklist to compare providers.

Want to see how it works? Watch this short video.

Automate Your Year-End Tax Planning

Track all MSME payment deadlines. Get alerts before Section 43B(h) disallowances. Never miss a statutory payment again.

Start Your Free Tax Review →

Advance Tax Planning and Interest Calculations

Advance tax is where most SME owners first encounter Section 234B and 234C interest, not because they intentionally delayed tax but because they miscalculated income projections or did not understand the instalment schedule.

The mathematics of advance tax interest penalizes both procrastination and poor estimation. Under Section 234B, if you pay less than 90% of your assessed tax, you pay 1% monthly interest on the entire shortfall from April 1 until you rectify it. This continues even if you file your return on time, the interest keeps accruing until full payment.

Section 234C operates differently. It penalizes specific instalment shortfalls. Miss the 15% requirement by June 15 and you pay 1% monthly for three months on just that shortfall, not your entire liability. But compound this across all four instalments and a founder who pays the entire tax in March faces interest charges on multiple fronts, the early instalments for nine months, middle instalments for six months, and so on.

How to calculate if you need to pay advance tax

The ₹10,000 threshold seems straightforward until you factor in deductions. Take your projected gross income, subtract legitimate business expenses, factor in any Section 80 deductions, then reduce TDS already paid. If the net tax payable exceeds ₹10,000, advance tax applies.

Common Calculation Errors:

- Forgetting to exclude agricultural income, which is exempt

- Not factoring in quarterly TDS certificates from clients

- Missing presumptive taxation benefits under 44AD or 44ADA

- Incorrectly estimating final profits mid year

The challenge for SMEs operating under Section 44AD presumptive taxation is different, you are required to pay the entire advance tax in the March 15 instalment. Miss this unique rule and you face full interest charges despite choosing the simpler tax regime that aims to reduce compliance burden.

What happens if income projections change mid year?

Income volatility is standard for SMEs, a large contract in December can throw off all advance tax calculations made in June. The law recognizes this through a concept called reasonable cause but defines it narrowly.

If a single transaction or event substantially changes your income, document it immediately. A major client contract signed in January, a business pivot in November, or an unexpected insurance claim can qualify. The remedy involves recalculating at each instalment date. If your June projection showed ₹10 lakh tax liability but December contracts push it to ₹15 lakh, pay the catch up amount in the December 15 instalment. This minimizes interest even if perfect prediction was impossible.

Here is the critical insight most advisors miss, paying excess advance tax is usually better than underpayment because interest on shortfall compounds while refunds earn minimal or no interest.

Employee Benefit Deductions and Deadlines

Employee related statutory deductions operate under overlapping rules that can disallow the same expense twice if handled incorrectly, once under Section 36(1)(va) for late deposits and again under Section 43B for accrual issues.

Your employees' contribution to PF or ESI must reach EPFO by the 15th of the following month. Deposit employees' PF on the 16th instead of 15th and the entire employee contribution becomes disallowed, even though it is their money.

The disallowance is permanent. Unlike other sections where late payments fix the default, employee contributions deducted but deposited late never regain deductibility. A ₹50,000 employee PF contribution deposited a day late means ₹15,000 additional tax, at 30% rate, that continues forever.

Employee Benefits Timeline:

- Bonus payments: 8 months from year end, November 30

- Gratuity funding: Before filing ITR for deduction

- Leave encashment: Paid or provisioned by March 31 with evidence

- PF or ESI: 15th of following month consistently

When must employee bonuses be paid for deduction?

The Payment of Bonus Act mandates payment within eight months of year end, by November 30 for March year ends. For tax deduction under Section 43B, paying before filing the return of income, typically July 31 or October 31 depending on audit requirements, secures deduction in the current year. Smart planning can save material tax and improve employee morale.

How do leave encashment provisions work?

Leave encashment requires careful documentation. Merely showing a provision in books is not enough, you need evidence of the leave policy, employees' actual cumulative leave balances, and calculation methodology showing how the encashment amount was derived. The critical evidence includes employee wise leave cards, a written leave policy clearly defining encashment rules, and actuarial valuation for larger teams. Without this, the entire provision risks disallowance regardless of actual liability.

GST Considerations for Financial Year-End

Your GST year-end intersects with income tax in three critical areas, input tax credit reconciliation, revenue recognition timing, and expense classification, all of which must align or you face additions.

The November 30 deadline for claiming prior year ITC is absolute. Any credits from FY 2023-24 not claimed by November 30, 2024, or annual return date, expire permanently, regardless of having valid invoices.

Timing differences create mismatches. An invoice booked in March but uploaded to GSTR-1 by your vendor in April creates reconciliation gaps. The window to fix these discrepancies narrows rapidly after March 31 as both GST and income tax timelines move forward.

What is the ITC reversal rule impact?

Common reversals include personal use assets claimed as business expenses, inputs used for exempt supplies, and credit notes not reflected promptly. An SME that claimed ITC on a company car must reverse proportionate credit for personal usage, and that calculation requires detailed logbook maintenance throughout the year.

The blocked credit list under Section 17(5) creates additional issues. Your year-end audit list should include standard disallowances:

- Employee facilities and housing benefits

- Membership fees for clubs and gyms

- Outdoor catering beyond statutory requirements

- General insurance except where mandatory

Missing these reversals invites adjustments under GST and potential income tax disallowance of the same expense.

When should you opt for composition scheme?

The composition scheme option for FY 2024-25 must be exercised by April 30 using Form CMP-02. Once chosen, you are locked in for the entire year. The ₹1.5 crore turnover limit for traders and ₹50 lakh for services covers all divisions, you cannot segregate activities. Composition dealers cannot claim input credits, which is viable only if your input costs are minimal. To get audit ready, see how to prepare your books for a GST audit.

Inventory and Bad Debt Adjustments

Year-end inventory valuation under ICDS II requires documentation many SMEs overlook until assessment notices arrive. Physical verification on or near March 31 is mandatory, not just counting but reconciling book quantities with physical stock, identifying damaged or obsolete goods, and computing net realizable value where market prices have dropped below cost.

The documentation trail should include dated photos or videos of inventory, third party inspection certificates for high value items, aging analysis showing time periods stock has been unsold, and comparable market pricing data supporting write down valuations.

How to correctly identify non moving stock

Inventory over 180 days without movement typically qualifies as slow moving. Use system generated reports showing the last sales date, original cost, current market price comparison, and specific reasons for the value decline. The quantum of write down depends on recovery expectations. Document any scrap sales or donation receipts from prior disposals to establish precedent values.

Bad debts recovery and provision considerations

Bad debt write off requires proving non recoverability. Prior recovery attempts should include account statements showing follow ups, legal notices sent with delivery proof, and reasonable attempts at settlement. Government and PSU receivables need different treatment, they rarely become genuinely unrecoverable and arbitrary write offs attract scrutiny.

Common Pitfalls:

- Writing off related party balances without formal proceedings

- Round figure provisions instead of account specific analysis

- Recovery after write off not offered to income

- GST credits not reversed on bad debt write offs

Convert Year-End Chaos to Clarity

Real time inventory valuations. Automated bad debt tracking. Documentation that stands up to scrutiny. Stop scrambling every March.

Get Your Free Tax Assessment →

Last-Minute Tax Strategies

The final weeks before March 31 offer specific opportunities to optimize tax position through strategic payment timing and documentary cleanup that become impossible after year-end.

Strategic timing of payments in the last week of March versus early April can swing tax liability significantly. A ₹10 lakh capital goods purchase completed March 30 allows depreciation for the year even with just one day of use. The same purchase on April 2 provides zero deduction this year. Similarly, prepaying certain expenses like insurance or AMC can create immediate deductions while spreading the benefit across the next year.

Documentation is key. Prepaid expenses need clear contracts showing the service period, capital equipment needs installation or put to use certificates, and professional fees need actual work commencement proof. Without these, shifting expenses risks disallowance.

Tax saving investments under Section 80

The ₹1.5 lakh Section 80C limit fills quickly with employee PF, but gaps often remain. Life insurance premiums, ELSS investments, PPF contributions, and permitted children's tuition all qualify. The key is paying before March 31.

Section 80D health insurance provides a separate ₹25,000 deduction, ₹50,000 for senior parents. Similar opportunities exist under 80G charitable donations with the ₹2,000 cash limit and 80GG rent deduction for non HRA proprietors.

Capital expenditure timing strategies

Additional depreciation at 20% applies to eligible new plant and machinery, excluding used goods and buildings, even if used for under 180 days in the acquisition year. For March purchases, this often creates a strong first year deduction on eligible costs. The put to use criterion matters, get an engineer's certificate, dated photos showing operational status, and first production run evidence to support the claim.

Post Year-End Actions

April 1 begins the timeline for capturing all FY 2023-24 benefits and avoiding irreversible errors.

Your first 30 days involve gathering full documentation. TDS certificates from each deduction, final bank statements showing March 31 balances, credit card statements with business transactions, purchase invoices awaiting entry, and confirmations for PF or ESI deposits. Missing documents spotted in April can usually be obtained, by June the trail runs cold.

Form 26AS and AIS downloads typically become available from mid April. These show all TDS credits, high value transactions reported by banks, and other filed information. Cross checking early highlights potential mismatches and allows correction before notices.

Critical Documentation checklist

- Monthly GST reconciliation, GSTR-2B versus purchases, with differences noted

- Fixed asset physical verification and insurance coverage aligned with block values

- Stock statements matching bank reported figures for secured loans

- Related party agreements and minutes approving terms

- Auditor communication letters highlighting significant observations

Advance tax estimation for new year

Your first quarter assessment for FY 2024-25 advance tax requires projection by June 15. Use prior year actuals adjusted for known contract changes, discontinued operations, new customer agreements, or regulatory impacts. Document assumption changes, these notes become your defense if projections prove incorrect and interest is levied.

Common Mistakes to Avoid

Mixing personal and business expenses remains the largest category, mobile bills with heavy personal use fully claimed, car running costs without logbooks, foreign travel where conferences represent two days of ten day trips. These attract additions and penalties.

Inadequate contract documentation follows closely. Oral agreements with regular vendors work until assessments demand proof. Related party transactions at non market rates without support. Sub contracts without PAN or GST details triggering higher TDS rates. Missing rental agreements resulting in 30% TDS instead of 10%.

Then comes statutory non compliance, GST credits claimed without valid invoices in GSTR-2B, TDS certificates not reflected in Form 26AS, Aadhaar linkage issues, return acknowledgments missing. These technical failures disallow genuinely valid claims.

The biggest mistake, viewing compliance as yearly instead of continuous. March 31 planning starts April 1, not February.

Conclusion

March 31 feels like the goal for tax planning but is really just the midpoint, between the decisions you have made all year and the consequences that crystallize over the coming months. The deadlines do not pause, April 30 TDS, May 31 returns, June 15 advance tax, November 30 GST credit expiry. Miss one and the dominoes fall.

Understanding Section 43B(h) MSME payment requirements can save more tax than all Section 80 investments combined. Properly timing capital equipment at year-end can be worth whole percentage points of profit. Those wins require continuous tracking, not March scrambles. The winners set up systems that drive compliance daily rather than fixing crises quarterly.

FAQ

What happens if I miss the TDS deposit deadline by just a day?

Missing the TDS deadline by even one day triggers automatic late fee of ₹200 per day under Section 234E, capped at the TDS amount, plus interest under Section 201(1A) at 1.5% per month from the original due date. For a ₹50,000 TDS payment due April 7 but paid April 10, you face ₹600 in late fees plus interest. The online TDS payment system also logs demands in your portal. To avoid slip ups, consider outsourcing to Virtual Accounting by AI Accountant that auto schedules these payments and reconciles challans.

Can I still claim deduction if I pay MSME vendors in April instead of March?

You cannot claim the deduction for FY 2023-24 if you pay after March 31 and beyond the MSME timeline. Section 43B(h), effective from AY 2024-25, disallows unpaid MSME dues older than 45 days, or 15 days without written agreement, as deductions in the year of accrual. If you pay before filing your ITR, typically July 31 or October 31, the expense becomes deductible in the year of payment. Virtual Accounting by AI Accountant tracks MSME due dates and nudges payments in the right order.

How much penalty do I face for late GST return filing as an SME?

GST late fees are ₹50 per day, ₹25 CGST plus ₹25 SGST, for non nil returns and ₹20 per day for nil returns, with caps based on turnover. Additionally, you pay 18% annual interest on net tax liability from the original due date. The real cost is the cascade, you cannot file subsequent returns until clearing previous defaults, and ITC expires after November 30 following the financial year. Virtual Accounting by AI Accountant prevents this by reconciling 2B to books and scheduling filings on time.

What if my advance tax calculations are wrong due to sudden income changes?

Revise your estimate at each instalment and pay catch up in the next due instalment. Document the specific event that changed projections, signed contracts, cancellations, or regulator notices. This reduces Section 234C interest, 1% per month on the shortfall, and demonstrates reasonable cause. Founders often pay an extra buffer in December or March to stay above 90% of final tax and minimize Section 234B interest.

Can I still claim FY 2023-24 purchases if the vendor uploads the invoice to GSTR-1 in April?

For income tax, purchases are deductible based on accrual and your accounting method, not GST upload month. For GST, if your vendor uploads the March invoice in April, you can usually claim ITC by November 30, 2024, or annual return date. Maintain delivery proof and invoice dating, and push vendors to include March invoices in their March GSTR-1 filed by April 20 to avoid mismatches.

Which employee benefits must be paid by March 31 for current year deduction?

Salaries are deductible on accrual, but employee PF or ESI must be deposited by the 15th of the following month to remain deductible, per judicial clarity. Bonuses can be paid up to November 30 under labor law, but for tax deduction ensure payment before ITR filing. Leave encashment and gratuity need actuarial or calculation support to be allowed as provisions. Virtual Accounting by AI Accountant maintains employee wise schedules and deposit trackers.

What capital equipment purchases make sense in the last week of March?

Eligible new plant and machinery, not furniture, buildings, or used assets, often deliver strong first year depreciation if installed and put to use by March 31. Technology hardware and manufacturing equipment are common examples. Keep commissioning evidence, installation certificate, test run logs, and dated photos. The documentation matters as much as the purchase date during assessment.

How does the GST Composition scheme election affect my tax planning?

Composition simplifies compliance and imposes a lower rate on turnover, but you lose all ITC and cannot issue tax invoices. The April 30 deadline to opt in or out via CMP-02 is hard. Model your next year turnover and input credits before you choose, a services SME with heavy GST paid inputs often loses more in credits than it saves in reduced rate. If many customers are B2B, losing their credit may cost you contracts.

What proof do I need for inventory write offs?

Prepare physical count sheets dated around March 31, item wise aging reports, market price evidence like supplier quotes or industry listings, and photos or videos of obsolete or damaged stock. Record disposal steps, scrap sale invoices, destruction memos with witnesses, or donation receipts. Reconcile any GST ITC reversals on written off items. Documentation should be SKU specific rather than round figure provisions.

Can old tax audit remarks affect my current year assessment?

Yes. Recurring issues like inventory valuation gaps, related party pricing, or cash handling draw intensified scrutiny. Address historical remarks proactively, file revisions where feasible, and prepare a memo showing corrections implemented. Demonstrating remediation reduces penalty risk for repeated defaults.

What happens if I miss the November 30 ITC deadline?

Missed ITC for the prior year is permanently forfeited after November 30, or the annual return filing date if earlier, no rectification later. This directly increases your cost of purchases. Persistent mismatches between books and GST returns may also invite income tax additions. Virtual Accounting by AI Accountant reconciles GSTR-2B monthly so no credits lapse.

Do I need auditor certification for advance tax estimation?

No formal certificate is required, but a reviewed working with assumptions, pipeline, margins, and known cost changes is your best defense if estimates deviate. Founders use CA reviewed projections each quarter, documenting why estimates moved and when, this establishes good faith during assessment.

Can GST credit adjustments impact income tax calculations?

Yes. GST credits reduce purchase cost for income tax. Any reversal increases expense for GST but can also force income tax adjustments if not mirrored in books. Ensure accounting entries reflect your GST position, especially blocked credits, time barred ITC, and credit notes. Consistency across systems avoids additions from both departments.

What if a high value March sale gets returned in April?

For GST, issue a credit note in April and report in April GSTR-1. For income tax under mercantile accounting, reduce March revenue with appropriate documentation of return date and reason. Maintain clear audit trails and ensure stock is accounted for on return. Patterns of frequent April returns after March spikes attract scrutiny, so keep explanations ready.

How should I organize March 31 documentation for assessment purposes?

Maintain a clean folder structure by transaction type then date, purchases, sales, expenses, capital. Include signed invoices with delivery proofs, bank statements with marked entries, TDS challans and returns, statutory deposit challans, email trails for key decisions, board or partner resolutions, and inventory count evidence. Virtual Accounting by AI Accountant automates this file structure, producing assessment ready packs in hours instead of weeks.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.