-01%201.svg)

Key takeaways

- TDS on salary under Section 192 is based on estimated annual income, employers must apply slab rates, factor in the employee’s chosen tax regime, and deduct on payment, not accrual.

- The new tax regime is the default from FY 2023 to 24, employees must explicitly opt for the old regime, standard deduction of ₹50,000 applies to both regimes.

- Collect declarations early, compute average monthly TDS, include other income and house property loss up to ₹2 lakh, and adjust for bonuses, arrears, and job changes.

- Deposit TDS by the 7th of next month, file Form 24Q quarterly, issue Form 16 by June 15, manage perquisites, PAN, and TRACES reconciliation carefully.

- Non compliance triggers interest, late fees, and penalties, avoid common errors like wrong regime, ignoring Section 87A rebate, or mismatching challans.

- Professional support, for example Virtual Accounting by AI Accountant, streamlines calculations, filings, and audits with automation and CA oversight.

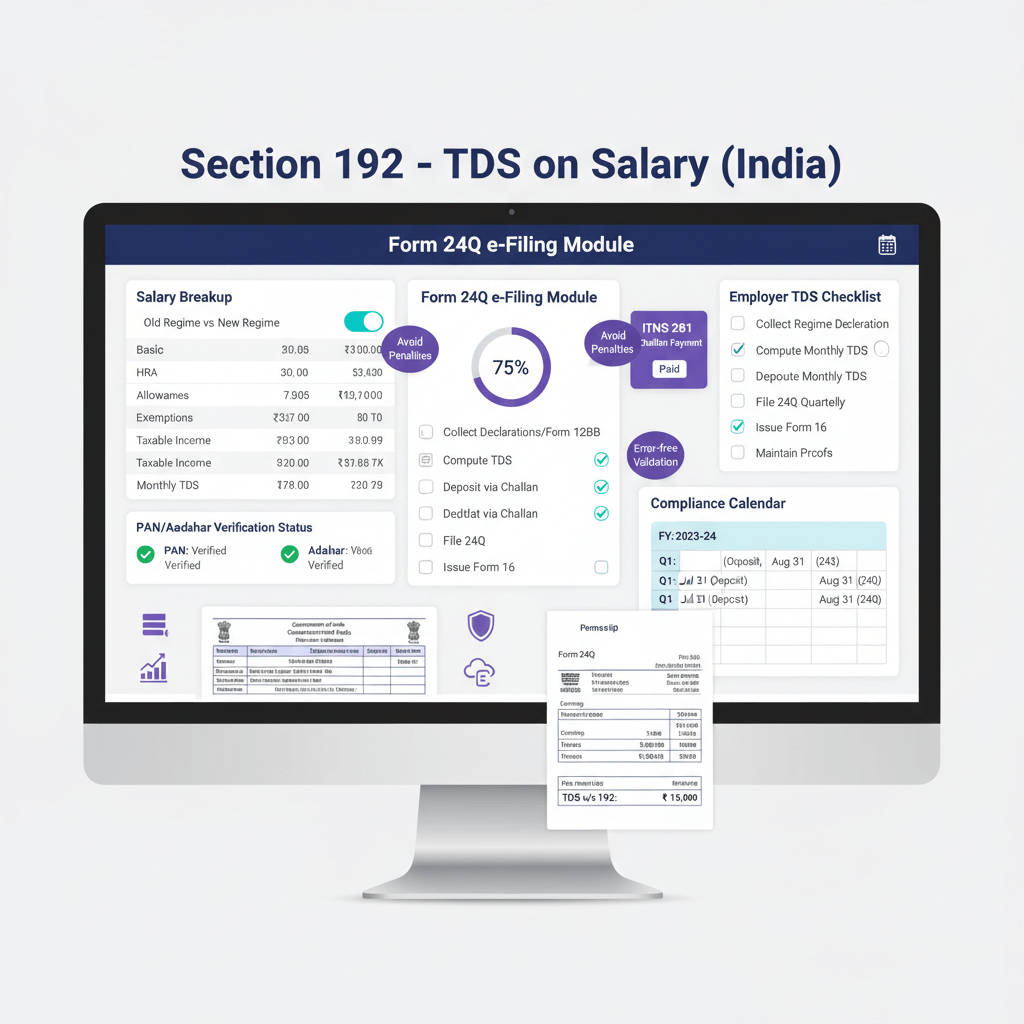

Quick refresher, what is TDS on salary under Section 192

TDS on salary is advance tax collection on employee income, deducted by the employer at the time of payment. You estimate each employee’s annual income, apply applicable slab rates based on the chosen regime, then spread the tax across remaining months. No TDS is required if estimated income is below ₹2.5 lakh in the old regime, or below ₹3 lakh in the new regime. A clear, practical primer is available in this Section 192 overview, this Kotak Life explainer on TDS Section 192, this BondScanner guide to Section 192, and this PNB MetLife article on TDS.

Remember, TDS applies when you pay the salary, not when it accrues in your books, advance salary, arrears, and bonuses are all covered on payment.

Two quick rules matter a lot. First, PAN is mandatory, without PAN, Section 206AA forces a 20 percent TDS. Second, employees choose the tax regime, if they do not submit a declaration, the new regime applies by default from FY 2023 to 24.

Applicability and scope for employers in India

Section 192 covers any employer employee salary relationship in India, this includes Indian and foreign companies, partnerships, HUFs, and individuals who employ staff. If salary is paid in India, TDS rules apply. Salary is a broad term, it includes basic pay, allowances, perquisites, bonuses, commissions, arrears, advance salary, and previous employer salary disclosed by the employee. For deeper coverage, review this ClearTax guide on applicability and this Kotak Life reference.

Under the new regime, most exemptions and deductions are unavailable, except standard deduction and specific employer NPS contributions, which simplifies computation but can be less beneficial for highly invested employees.

How to deduct TDS on salary in India, step by step

Step 1, collect employee declarations

Obtain regime choice at the start of the year, collect Form 12BB, rent receipts and landlord PAN where rent exceeds ₹1 lakh, home loan certificates, and for new joiners, Form 12B with prior salary and TDS. See foundational guidance in this ClearTax Section 192 walkthrough and this Department of Revenue circular.

Step 2, calculate gross salary

Add basic, DA, allowances, perquisites as per rules, bonuses, advance salary, arrears, and any employer contributions that are taxable beyond thresholds.

Step 3, apply exemptions

Old regime allows HRA exemption, LTA, and others within limits, both regimes allow the standard deduction of ₹50,000. New regime mostly allows only standard deduction and specific employer NPS contribution.

Step 4, include other income and losses

Add interest income and rental income declared by the employee, permit set off of house property loss up to ₹2 lakh.

Step 5, claim deductions

Under the old regime, consider Section 80C, 80D, 80E, 80G, and more, the new regime largely limits this to 80CCD(2) for employer NPS and the standard deduction.

Step 6, compute tax and monthly TDS

Apply slab rates as per chosen regime, check rebate under Section 87A, add cess at 4 percent, include surcharge where applicable, then divide annual tax by remaining months and adjust as facts change.

Step 7, handle special situations

For arrears from earlier years, obtain Form 10E and apply relief under Section 89(1) to avoid bunching impacts.

Step 8, manage multiple employer cases

Use Form 12B to incorporate previous employer salary and TDS, ensuring correct annual computation. Additional clarity is available in this Kotak Life explainer and the official circular.

Practical examples with numbers

Example 1, software engineer in Bangalore

Rahul earns ₹12 lakh annually, opts for old regime, and has 12 months remaining. Gross salary ₹12,00,000, standard deduction ₹50,000, Section 80C ₹1,50,000, taxable income ₹10,00,000. Tax before cess ₹1,12,500, cess ₹4,500, total ₹1,17,000, monthly TDS ₹9,750. Under the new regime, with standard deduction only, tax may be lower or even nil subject to rebate thresholds.

Example 2, mid year joiner

Priya’s package is ₹10 lakh, previous employer paid ₹6 lakh with ₹20,000 TDS. Full year tax assumed ₹75,000, after credit of ₹20,000, remaining ₹55,000 spread across October to March, monthly TDS ₹9,167.

Example 3, junior employee

Amit earns ₹7 lakh under the new regime, after standard deduction taxable income is ₹6.5 lakh, Section 87A rebate applies, TDS is nil.

| Component | Old Regime | New Regime |

|---|---|---|

| Gross Salary | ₹12,00,000 | ₹12,00,000 |

| Standard Deduction | ₹50,000 | ₹50,000 |

| Other Deductions | ₹1,50,000 | Nil |

| Taxable Income | ₹10,00,000 | ₹11,50,000 |

| Tax Before Cess | ₹1,12,500 | ₹1,95,000 |

| Less Rebate | Nil | ₹1,95,000 |

| Net Tax | ₹1,17,000 | Nil |

| Monthly TDS | ₹9,750 | Nil |

For reference on computations and relief, see this Department of Revenue circular and the ClearTax Section 192 explainer.

Deduction, deposit, and return filing workflow

Monthly deposit

Deposit TDS via Challan 281 by the 7th of the next month, for March, government employers by April 30, others by May 7. Use correct TAN, assessment year, and Section 192 code. Online payment on the income tax portal provides instant acknowledgments.

Quarterly returns

File Form 24Q quarterly, Q1 due July 31, Q2 due October 31, Q3 due January 31, Q4 due May 31. Validate with FVU, map challans accurately, and reconcile with Form 26AS. Guidance, Form 24Q and TRACES essentials.

Annual certificates

Issue Form 16 by June 15, Part A from TRACES, Part B prepared with salary breakup, issue Form 12BA for perquisites where required.

Proactive TRACES monitoring prevents mismatches, download 26AS, cross check challans, and respond to notices quickly.

Employer TDS obligations, a complete compliance checklist

Beginning of financial year

- Verify TAN and employee PANs, collect regime choice declarations and KYC.

- Obtain Form 12BB, and for new joiners, Form 12B with prior salary and TDS.

Monthly routine

- Compute gross salary including perquisites, add other income, apply house property loss cap of ₹2 lakh.

- Calculate TDS using the average rate, adjust for changes like bonuses or revised declarations.

Deposit and compliance

- Pay via Challan 281 by the 7th, map challans correctly, and retain acknowledgments.

Quarterly tasks

- Prepare and file Form 24Q before due dates, validate with FVU, and rectify errors promptly.

Annual requirements

- Issue Form 16 by June 15, provide Form 12BA where applicable, preserve records for seven years, and respond to tax notices in time.

Useful primers, ClearTax on Section 192 and Kotak Life guide to TDS on salary.

Penalties, interest, and common mistakes

Interest and fees

Failure to deduct invites 1 percent per month interest, failure to deposit after deduction invites 1.5 percent per month, late Form 24Q filing triggers ₹200 per day under Section 234E, subject to the TDS cap. Incorrect returns can draw penalties from ₹10,000 to ₹1,00,000 under Section 271H, willful non deposit can lead to prosecution under Section 276B.

Common pitfalls

Applying the wrong regime when no declaration is received, not capturing previous employer TDS, missing Section 87A rebate, using flat rates instead of the average rate, accepting HRA without landlord PAN where rent exceeds ₹1 lakh, or mismapping challans. A practical roundup of common mistakes to avoid is helpful, also, do not miss March salary timelines, see this year end accounting checklist for India.

Special scenarios every employer faces

Perquisites and grossing up

Company car, rent free accommodation, and memberships are valued per Income Tax Rules and added to salary. If the company bears the tax on perquisites, use gross up under Section 192(1A), tax on tax must be computed.

Mid year joiners and leavers

Collect Form 12B for joiners and incorporate prior income and TDS, for exits, compute cumulative tax to date and adjust in final settlement.

Advance salary and arrears

Deduct TDS when paying, not when due, for arrears, apply Section 89 relief with Form 10E.

Missing PAN

Apply 20 percent under Section 206AA until PAN is furnished, this applies even to foreign nationals starting work in India.

International assignments

Check residential status, residents are taxed on global income, non residents on Indian income, DTAA claims are typically for return filing, employers compute TDS per Indian law. For structured references, see the ClearTax guide, the Kotak Life explainer, the BondScanner overview, and the official circular.

How professional services help with TDS compliance

Running payroll and meeting Section 192 timelines is a process discipline, not a one time task. Consider these models:

- Virtual Accounting by AI Accountant, comprehensive TDS management with regime tracking, monthly calculations, automated challans, Form 24Q and Form 16, proof workflows, TRACES reconciliation, dashboards, and CA oversight. Explore the virtual accounting services included.

- Traditional CA firms, suitable for stable setups, more manual coordination.

- Payroll software, good automation, you still handle filings and notices.

- Big 4 consulting, comprehensive, premium pricing for larger enterprises.

- DIY, workable for micro teams, higher risk of errors and missed deadlines.

As teams cross ten employees, automation for proof collection, challan mapping, and reminders becomes essential.

Your next steps

Set up a compliance calendar, mark deposit dates, Form 24Q deadlines, and the Form 16 issuance date, and share it with finance and HR. Review your computation workflow, ensure other income and house property loss are considered, confirm the correct regime for each employee, and compute TDS early each month. Organize employee folders with PAN, regime choice, proofs, and rent details. Stay updated with budget changes and official circulars, and when in doubt, lean on expert support, for example Virtual Accounting by AI Accountant, to keep your TDS process consistent and audit ready.

FAQ

How do I pick the right tax regime for my team, and what if someone forgets to submit a declaration

The new regime is the default from FY 2023 to 24, if no declaration is submitted, apply the new regime. Encourage employees to submit their choice in April, and allow changes once if needed, then recalculate TDS for remaining months and document the change. A managed workflow through a service like Virtual Accounting by AI Accountant helps you track and evidence regime choices.

We are a startup hiring mid year, how do we handle previous employer salary and TDS

Collect Form 12B from the joiner, include previous salary and TDS in your annual estimate, then compute monthly TDS for the remaining months. This avoids year end shortfalls and employee grievances about excess deduction.

Do I deduct TDS on bonuses, incentives, or advance salary when paid, or at year end

Deduct on payment, not accrual, apply the average rate method based on updated annual estimates. For large bonuses, recast the projection that month so you do not under deduct.

What if an employee’s estimated tax becomes zero because of Section 87A rebate, should I still deduct TDS

No, if projected taxable income after deductions and standard deduction is within the rebate threshold, TDS is not required. Retain working papers and declarations as evidence.

We missed the deposit deadline by a week, what interest and fees apply

If TDS was deducted but not deposited, interest is 1.5 percent per month or part thereof until payment. Also watch out for late filing fees of ₹200 per day under Section 234E if the quarterly return gets delayed.

How do we manage HRA claims above ₹1 lakh annual rent without the landlord’s PAN

Landlord PAN is required where annual rent exceeds ₹1 lakh, otherwise you cannot allow HRA exemption. Ask for a declaration and PAN copy, and keep rent receipts. Missing PAN leads to disallowance risk during scrutiny.

Do I need to consider employees’ interest income or rental income in TDS calculations

Yes, if employees declare such income, include it in the estimate, allow house property loss up to ₹2 lakh, and compute tax accordingly. This helps avoid short deduction and year end disputes.

How should I handle arrears or retrospective increments without shocking monthly TDS

Compute tax with arrears included, then apply relief under Section 89(1) if the employee furnishes Form 10E. Spread the adjusted TDS over remaining months to smooth deductions, and keep the working attached to payroll records.

We have foreign hires without PAN in their first month, what rate applies

Without PAN, apply 20 percent under Section 206AA, once PAN is allotted and furnished, recalculate prospectively, any earlier excess is adjusted in later months within the same financial year.

Which filings do I absolutely need to calendar so I do not get notices

Monthly TDS deposit by the 7th, Form 24Q quarterly by July 31, October 31, January 31, and May 31, and Form 16 issuance by June 15. Put reminders for challan mapping and TRACES reconciliation. A managed service like Virtual Accounting by AI Accountant automates these calendars and confirmations.

Is payroll software enough for TDS compliance, or do I still need a CA

Payroll software automates calculations, however you still handle proofs, challans, Form 24Q, TRACES mismatches, and notices. Many small teams pair software with expert oversight, for example Virtual Accounting by AI Accountant, to blend automation with accountability.

How do I prevent challan mismatches and Form 24Q errors that trigger TRACES notices

Use the correct TAN and assessment year, map challans accurately, validate with FVU, and cross check Form 26AS every quarter. Maintain a maker checker process, and keep challan receipts attached to the return working file for audits.