Key takeaways

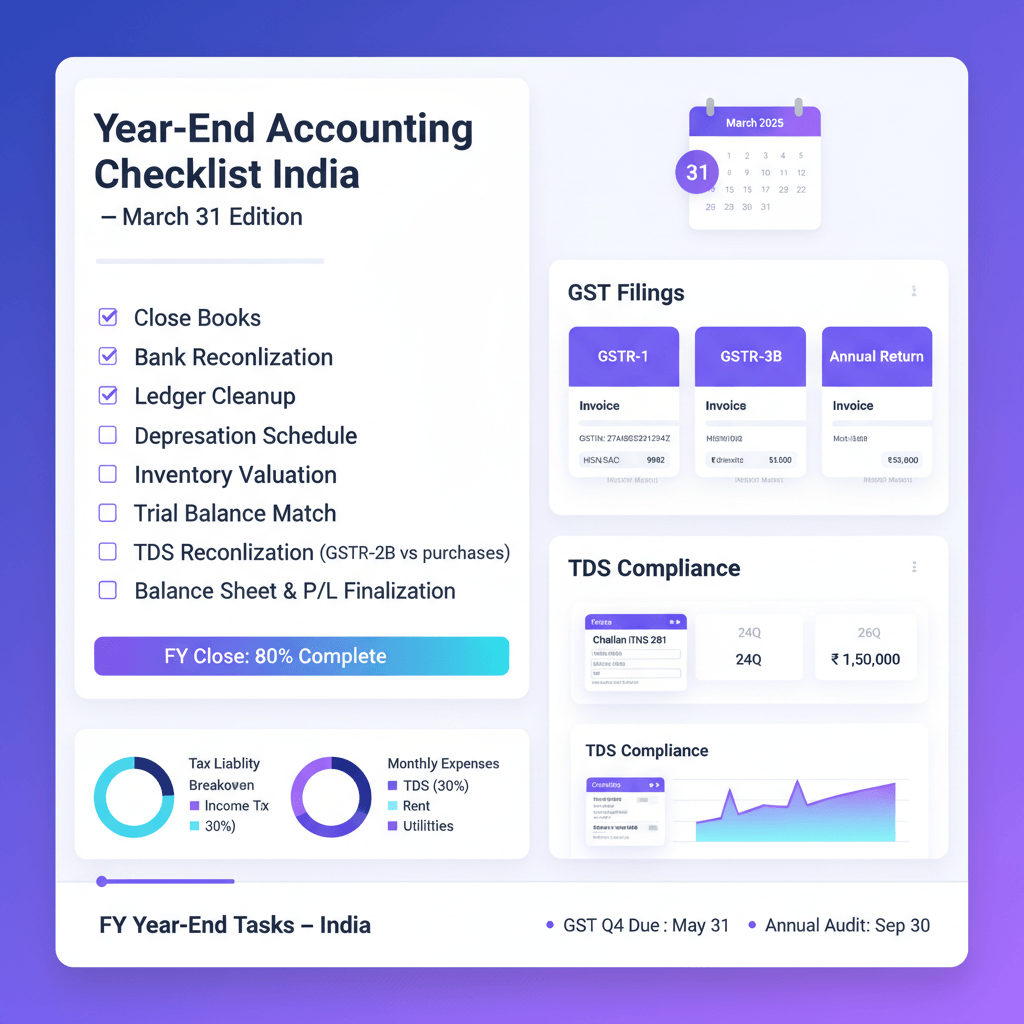

- Start the year end close two weeks before March 31, lock periods, clean masters, and circulate cut off memos.

- Prioritize MSME dues, provision unbilled expenses, and validate GSTIN and HSN to avoid ITC and tax pitfalls.

- Issue March e invoices early, confirm balances with key customers, and assess expected credit losses conservatively.

- Finish bank reconciliations, cash counts, and inventory verification on March 31, document all variances immediately.

- Reconcile GSTR 2B with purchase registers, apply Rule 42 and 43 reversals, and park ineligible ITC until supplier compliance.

- Compute depreciation under Companies Act and Income Tax separately, review deferred tax, and finalize accruals.

- Freeze the trial balance by April 7, back up ledgers, and send final balance confirmations to vendors and customers.

- Use automation like AI Accountant to compress close cycles from a week to 2 3 days, with fewer errors and better audit trails.

Year end accounting checklist India March 31: quick view

Print this at a glance schedule, assign owners, and track completion rigorously.

| Priority | Action | Owner | Due Date |

|---|---|---|---|

| 1 | Lock accounting periods, freeze masters, verify GSTIN and HSN codes | Finance Head | Mid March |

| 2 | Process all vendor bills, check MSME status, create provisions | AP Team | Mid March |

| 3 | Issue customer invoices, send balance confirmations, assess bad debts | AR Team | Mid March |

| 4 | Complete bank reconciliations, count cash, clear old entries | Cashier | March 31 |

| 5 | Conduct physical inventory, apply valuation methods, check NRV | Warehouse | March 31 |

| 6 | Update fixed asset register, calculate depreciation | FA Custodian | March 31 |

| 7 | Process final payroll, create provisions, prepare TDS data | HR Team | March 31 |

| 8 | Reconcile GSTR 2B, check ITC eligibility, verify e invoices | Compliance | March 31 |

| 9 | Review Section 43B disallowances, calculate deferred tax | Tax Lead | March 31 |

| 10 | Freeze trial balance, prepare schedules, create backup | CFO or CA | April 1 7 |

Why it matters: Missing March 31 advance tax can trigger interest under Sections 234B and 234C, unresolved GSTR 2B differences can lead to GST notices, and unbooked accruals invite audit qualifications.

Source: ClearTax year end tasks

Pre close, by mid March: set up to year end close books India smoothly

Data hygiene and cut offs

Begin two weeks before March 31. Lock your chart of accounts in Tally or Zoho Books, verify every GSTIN against the portal, and refresh HSN and SAC mappings. Clear old suspense and rounding differences now, not on March 31 night.

Create a cut off memo for warehouse, procurement, and sales. For example, no goods receipts after 5 PM on March 31 without finance approval, all March sales invoices to be posted by March 30, and courier expenses through March 31 to be accrued.

Vendor bills and AP

Compile pending bills across email, trays, and Excel. Match to POs and GRNs, flag GSTIN or HSN mismatches instantly. Check MSME status for each vendor, then prioritize payouts because unpaid MSME dues beyond 15 or 45 days risk disallowance under Section 43B(h). Accrue for services received but unbilled, for example, March portion of an annual AMC or quarterly freight bills.

Time saver: AI Accountant bulk bill extraction reads hundreds of PDFs, validates GSTIN, and prevents duplicates, which turns days of typing into a short review.

Customer invoices and AR

Raise March e invoices before the 30th, then send balance confirmations to your top customers by March 20. Review aging deeply, apply expected credit loss percentages based on history, and provision for stress cases such as NCLT exposures. Allocate March receipts to specific invoices so advances do not distort revenue.

AI Accountant auto links bank receipts to open invoices and visualizes aging, so collectors focus on the hardest buckets first.

Banking and cash

Download statements for banks, credit cards, gateways, and wallets through March 31. Start your bank reconciliation early, clear old reconciling items, and split consolidated settlements correctly. Audit trails are stronger when differences are fixed before close.

Source: ClearTax checklist

March 31 day of checklist

Inventory and COGS

Count high value items fully, document variances, and close any open GRNs. Apply your valuation policy consistently, verify NRV for slow movers, and capture work in progress cleanly for materials, labor, and overhead.

Fixed assets and depreciation

Move CWIP to fixed assets for items commissioned before March 31, update the asset register for additions and disposals, and compute depreciation under both Companies Act Schedule II and Income Tax Section 32. For assets used for less than 180 days, apply the half year convention for tax depreciation.

Accruals and provisions

Accrue utilities, professional fees, bonuses, and statutory charges, then defer prepaid portions like rent or insurance. Translate foreign currency balances using March 31 RBI reference rates, recognize unrealized gains or losses, and update deferred tax for timing differences.

GST and indirect tax cut offs

GSTR 2B reconciliation should not wait. Match every purchase line with your registers, mark ineligible ITC where suppliers have not filed GSTR 1, and compute reversals under Rule 42 and 43. RCM for GTA and legal services should be accrued and paid on time.

Sources: ClearTax, ApkiReturn

First week of April: post close hygiene

Close entries and reviews

Compile your journal voucher pack, include accruals, depreciation, forex revaluation, and tax provisions. Run a month on month and year on year variance review, investigate spikes or drops, and document explanations for audit files. Freeze the trial balance by April 7 and back up data locally and to cloud.

Banking, AR and AP finalization

Complete final BRS by April 5, list reconciling items clearly, and lock subledgers to avoid accidental changes during audit. Send final vendor and customer balance confirmations with a reconciliation statement, then target responses by April 15.

April and May statutory calendar, India specifics

TDS obligations:

- March TDS deposit: April 30, government deductors until May 7

- Q4 TDS return: May 31

- Form 16 and 16A issuance: June 15

TCS requirements:

- March TCS deposit: April 7

- Q4 TCS return: May 15

GST filings:

- GSTR 3B for March: April 20, ITC eligibility impacted if claimed after September 30

- GSTR 1 for March: April 11 for monthly filers

- Annual returns and audit: timelines as per turnover

Other critical dates:

- PF and ESI for March: April 15

- Professional tax: state specific, typically April 15 to 30

- Advance tax final installment: March 15 for FY 2024 25

Do not miss LUT renewal for exporters, CMP 02 for composition, and QRMP selection changes by March 31. Check Schedule III disclosures, CARO 2020 applicability, related party reporting, and Section 44AB audit thresholds.

Sources: ClearTax, ApkiReturn

Compliance hot spots in India to not miss

MSME payment tracking

Map MSME status and agreed credit terms, then run weekly aging. Section 43B(h) can disallow expenses if dues cross 15 or 45 days, so prioritize those payments and record clear justifications.

E invoicing thresholds

If turnover crosses Rs. 5 crore in FY 2024 25, e invoicing becomes mandatory from April 1, 2025 for B2B. Test API integration, print formats, and IRN workflows before go live.

Related party scrutiny

Maintain agreements, board approvals, and pricing documentation. For domestic transactions above thresholds, ensure arm’s length support because auditors and tax officers will examine these closely.

TDS narration errors

Mis tagging sections, for example 194C versus 194J, creates Form 26AS mismatches. Review March vouchers, correct sections, and prepare for timely return filing.

Capex versus repairs classification

Assess nature and benefit period, not only per item value. Batch purchases of small individual items that create a capital unit should be capitalized with a consistent policy.

How AI Accountant accelerates your financial year closing India checklist

AP automation: Upload PDFs or images, extract vendor, GSTIN, invoice detail, and taxes automatically. Duplicates and GSTIN mismatches get flagged before posting.

Bank reconciliation: Ingests multi bank statements, normalizes formats, and auto matches ledger entries, including splits and consolidated receipts, which reduces manual work drastically.

Transaction mapping: Learns your patterns, categorizes recurring narrations, and suggests mappings for new entries with high accuracy.

GST reconciliation: Scales from 100 to 10,000 invoices, categorizes mismatches, and converts chaos into manageable exception queues.

Tally and Zoho Books integration: Sync masters and transactions both ways, keep a single source of truth, and eliminate re entry.

Multi organization support: CAs can switch clients quickly, maintain segregated learning, and enforce role based access across teams.

Result: Most companies compress the close from 5 to 7 days to 2 to 3 days, with fewer queries during audit and better compliance hygiene.

Download the march 31 accounting checklist India, printable

Get a one page PDF with tasks, owners, and dates, including:

- Pre close activities timeline starting mid March

- Day of tasks for March 31

- Post close tasks for the first week of April

- Statutory calendar through June

- Department wise responsibility matrix

- Audit document preparation checklist

Wrap up and next steps

Your year end accounting checklist India March 31 journey is smoother when you start early, fix data hygiene, finish reconciliations on time, and automate the repetitive work. AI Accountant handles bulk bills, reconciliations, and GST matching so your team can analyze, not enter data.

Book a short demo, then run this financial year closing India checklist with confidence. The March 31 deadline does not need to be a scramble.

Reference: ClearTax resource

FAQ

What documents should a CA compile to year end close books India efficiently?

Collect vendor bills and credit notes, customer invoices and debit notes, bank and wallet statements, GSTR 2B and 3B downloads, fixed asset register with additions and disposals, inventory count sheets and valuation working, payroll registers with bonus and leave provisions, board approvals for write offs or policy changes, and key contracts for accrual estimates. Many CAs use AI Accountant folders to auto tag and store PDFs against ledgers.

How should I reconcile ITC if vendor invoices are missing in GSTR 2B at year end?

Do not claim ITC that is absent in GSTR 2B. Park it in an “ITC Pending” ledger, follow up with suppliers weekly, and transfer to eligible ITC only after the invoice surfaces in 2B. If the supplier does not file by September 30, reverse permanently. AI Accountant’s 2B match report highlights vendor wise gaps with reminders.

How do CAs differentiate Companies Act depreciation and Income Tax depreciation during close?

Compute book depreciation per Schedule II based on useful life, then compute tax depreciation per Section 32 block rates, with the half year rule where applicable. Maintain separate ledgers or schedules and calculate deferred tax on timing differences. AI Accountant can export dual depreciation schedules for audit files.

What is the clean way to book unbilled services and goods received not invoiced, GRNI, on March 31?

Accrue by debiting the expense or inventory and crediting a provision or GRNI liability with substantiation such as contracts, delivery challans, and GRNs. Reverse the entry in April when the actual bill arrives. AI Accountant templates let you post standard accrual JVs in bulk.

How should a CA compute Section 43B(h) disallowance for MSME dues at year end?

Identify MSME registered vendors, map agreed credit terms, then compute outstanding beyond 15 days for goods or 45 days for services as of March 31. Amounts unpaid within the permissible window become non deductible. AI Accountant’s MSME tracker tags vendors and auto ages dues with exception flags.

What is the best practice for March 31 inventory valuation, especially NRV tests?

Apply the chosen method, FIFO or weighted average, consistently, then test NRV for slow moving or obsolete items using current selling price less costs to complete and sell. Document write downs with SKU level evidence. Service firms should value unbilled WIP hours at realizable rates. AI Accountant can export SKU aging for NRV reviews.

How can I streamline March bank reconciliation for multiple banks and gateways?

Ingest statements for all banks, cards, and gateways, standardize columns, clear historic reconciling items, and document reasons for any residual differences. Complex splits for consolidated settlements should be broken into invoice wise mappings. AI Accountant auto matches narrations and learns split rules over time.

What is the recommended approach to expected credit loss provisioning on overdue receivables?

Segment aging buckets, apply historical recovery rates, overlay current customer risk intel, then provision at a conservative rate for 180 plus day buckets and special cases such as NCLT. Support with customer communication logs. AI Accountant’s aging dashboards and notes help justify ECL percentages.

Which GST reversals must I close by March 31, and how do I evidence them?

Compute Rule 42 reversals for exempt supplies, Rule 43 for capital goods, and RCM liabilities for notified services. Keep working papers with formulae, turnover ratios, and invoice lists. AI Accountant produces rule wise reversal sheets that tie back to registers.

How do I handle foreign currency revaluation and its tax impact on March 31?

Revalue receivables and payables using RBI reference rates on March 31, recognize unrealized gains or losses per AS 11 or Ind AS 21, and assess taxability per prevailing guidance. Capture exchange differences in a dedicated account and disclose policy notes. AI Accountant can fetch reference rates and post standard JVs.

What close controls should a CA enforce after posting year end entries?

Freeze the trial balance, lock subledgers, archive backups, circulate a period lock memo, and maintain a change log for audit adjustments only. Send final balance confirmations and start audit PBC tracking. AI Accountant provides a close checklist with owner and due dates for each control.

Can AI tools like AI Accountant actually reduce year end close timelines for multi entity CA firms?

Yes, with bulk OCR for bills, auto bank matching, GST 2B reconciliations at scale, template based accrual JVs, and one click exports to Tally or Zoho Books, most firms cut close time to 2 or 3 days per entity while improving accuracy and audit readiness. Multi organization switching also reduces context loss for partners and staff.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.

.png)