Key takeaways

- A revenue recognition dashboard for India gives CFOs, controllers, and CA firms a single source of truth that separates billed from recognised revenue across subscriptions, milestones, and hybrid contracts, fully aligned with the Ind AS 115 five step model.

- Real time deferred revenue waterfalls, contract asset tracking, and automated schedules eliminate month end scrambles and cut close cycles from 15 days to under 7.

- Hybrid billing (milestone, percentage of completion, straight line) coexists cleanly in one dashboard when performance obligations are classified at the line level with proper SSP allocation.

- NFRA's increased scrutiny of SME revenue in 2025 and 2026 audits makes audit ready evidence (version history, policy memos, immutable logs) non negotiable, not optional.

- Subscription metrics like MRR, ARR, churn, and cohort retention reconcile back to your general ledger without manual rework when the underlying data is normalised and mapped correctly.

- AI Accountant's MIS reporting engine solves the foundational data problem: it normalises invoices and contracts from Tally, maps lines to performance obligations, and feeds audit ready datasets into your BI layer.

Revenue Recognition Dashboard India: What's New in 2026

Until late 2024, NFRA audit inspections flagged revenue overstatement primarily in listed entities. From 2025 onwards, NFRA expanded sample queries to SMEs, with roughly 20% of inspection samples now targeting SSP evidence and variable consideration estimates. If your firm lacks documented SSP catalogs and estimation policies, expect extended audit procedures and potential qualification risks.

Operationally, the shift is tangible. CBIC's December 2025 circular now mandates GSTIN wise revenue splits in GSTR 9C reconciliations. Finance teams must tag every revenue line by GSTIN before filing, a step that did not exist in the 2024 workflow. For multi GSTIN entities (common in CA firms managing 10+ clients), this creates a new reconciliation layer between your recognition schedules and GST returns.

Who does this hit hardest? Mid size SaaS and services firms with hybrid billing (₹5 to ₹50 crore turnover) that previously relied on spreadsheets for revenue schedules. These firms now face three pressures simultaneously: NFRA scrutiny, GSTIN wise filing requirements, and auditor demands for immutable change logs on contract modifications.

The cost of inaction is concrete: NFRA can impose penalties up to ₹10 lakh on auditors who fail to evidence revenue testing, and companies face ITC reversals if GSTN reconciliations don't match recognition records. Deadlines are annual (GSTR 9C filing by December 31), but the data preparation is monthly.

What to do now:

- Audit your SSP catalogs and update them with Q1 2026 pricing data before your next statutory audit.

- Implement GSTIN tagging at the invoice ingestion stage, not as a year end exercise.

- Ensure your recognition schedule tool produces immutable logs acceptable under automated GST reconciliation workflows.

Platforms that normalise Tally data and maintain structured MIS outputs are well suited to handle this new GSTIN wise reconciliation layer without adding manual steps to the close process.

Who this guide is for and what you will learn

This guide is written for CFOs, controllers, CA partners, and SME finance heads who need a reliable, Ind AS 115 compliant revenue truth that runs at the speed of business.

You will learn buying criteria, feature checklists, implementation steps, pricing benchmarks, and how AI Accountant complements Tally to deliver a working, audit ready solution.

Stretch Tally with BI, buy specialised revenue recognition software, or use AI Accountant as a middle path. This guide helps you choose, price, and implement.

For deeper context on the standard, see the ICAI Ind AS standards page, the Grant Thornton overview on Ind AS 115, and the MCA portal for the latest Ind AS notifications.

Why revenue recognition in India is uniquely challenging

The hybrid billing reality

Indian companies juggle multiple billing models. Subscriptions with upgrades or downgrades, retainers plus time and material, and milestone or percentage of completion projects all coexist.

Under Ind AS 115, recognition follows performance obligations, not invoices. Excel schedules quickly break under this volume and complexity. The Ind AS 115 complexity grows exponentially when a single customer contract bundles software licenses, implementation services, and ongoing support.

Regulatory and tax overlay

Recognition requires identification of distinct performance obligations, transaction price determination, SSP allocation, and recognition timing aligned to control transfer.

GST treatment, GSTIN wise reporting, and the flow into contract assets or liabilities adds a demanding overlay. CBIC's 2025 circular on GSTIN wise splits in GSTR 9C makes this even more granular.

Use the Ind AS 115 five step model as your reference. The Grant Thornton overview provides practical examples of how bundled offerings are unbundled.

Operational pressure

Month end close deadlines tighten. Auditors demand evidence for each step. Management needs recognised versus billed visibility.

Sales reports from Tally do not satisfy recognition or audit needs. Finance teams must upgrade process and systems. With NFRA now sampling SME revenue in 20% of inspections, the pressure is no longer theoretical.

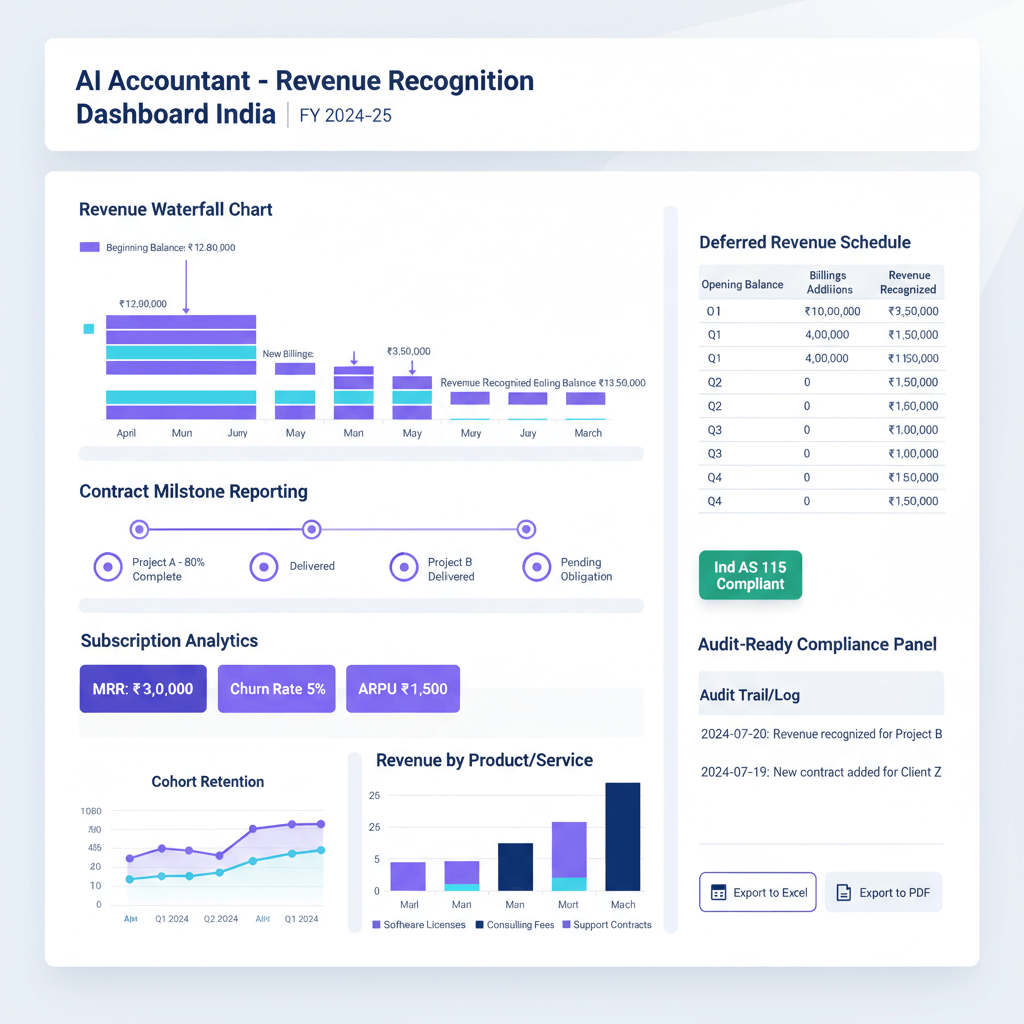

What is a revenue recognition dashboard for India

Core definition

A revenue recognition dashboard is a connected set of reports and models that converts contracts and invoices into Ind AS 115 compliant schedules.

It separates billed from recognised revenue by period, customer, contract, and performance obligation. It tracks deferred revenue, contract assets and liabilities, and backlog in real time. Think of it as an audit ready revenue waterfall generation tool that updates itself as contracts evolve.

How it differs from sales and billing dashboards

Sales dashboards focus on invoice values and collections. Revenue recognition dashboards focus on the timing of recognition under the standard.

They show recognised versus billed with reconciliations, waterfalls, and milestone progress. The difference is fundamental: sales answers "what was billed," revenue recognition answers "what can be recognised."

Essential features checklist for audit ready revenue waterfall generation tools

Ind AS 115 logic built in

- Support for contract identification, performance obligations, transaction price, SSP allocation, and recognition timing.

- Variable consideration (discounts, rebates, and performance adjustments) fully modelled with audit ready calculations.

- Contract modification handling: create new contracts or reallocate within existing, with transparent version history.

Deferred revenue tracking

- Automated schedules per contract line, aging analysis, and monthly or quarterly waterfalls.

- Period wise releases and closing balances, available for operational reviews and audits.

Milestone revenue reporting

- Contract and project level visibility into milestone definitions, dates, and acceptance status.

- Recognised versus milestones achieved, change order impacts, and exception alerts.

Subscription revenue analytics

- MRR, ARR, churn, expansion, contraction, and cohort analysis, including proration for mid term changes.

- Recognised versus billed reporting for prepaid plans, with clear reconciliation lines.

Audit trail and documentation

Version history for schedules and assumptions is non negotiable. Auditors need change logs and context.

Use Audit Trail and Documentation features. Store policy notes and recognition memos per contract. Maintain user activity logs for accountability. Under NFRA's 2025 and 2026 inspection standards, immutable logs are the minimum expectation for revenue evidence.

Data input capabilities

- Contracts, orders, invoices, credit notes, debit notes, receipts, adjustments, and journal vouchers: all ingested and tagged.

- Native pull from Tally, CRM, and project systems. Minimise manual uploads, maximise accuracy.

Controls and approvals

Enable maker checker workflows and role based access. See role based access patterns for multi org setups.

Include reconciliation panels comparing subledger to Tally control accounts. This is where your revenue recognition dashboard earns its keep during audits.

Integration capabilities

- Connectors to Tally: import invoices and export journals to reduce manual effort and error.

- Exports to Power BI and Excel for custom analysis and board reporting.

Scalability requirements

- Handle thousands to millions of schedule lines with reliable performance.

- Multi org, multi entity support for CA firms and corporate groups. Entity isolation with consolidated visibility.

Reporting and drill down

- Slice by customer, contract, PO, product or service, region, GSTIN, and channel.

- Drill from summary to detail. Answer audit questions quickly. Resolve variances without switching tools.

For standards alignment, revisit the ICAI Ind AS standards repository and the Grant Thornton paper.

Data model and architecture fundamentals

Master data requirements

Customer data must include GSTIN and region. Products and services need revenue attributes, SSP, and default recognition methods.

Contracts and orders require clear identifiers. Performance obligations must be linked to specific contract lines. Without clean master data, no revenue recognition dashboard can produce trustworthy outputs.

Transaction data flow

Invoices, receipts, credit notes, debit notes, and adjustments: each flow through mapping rules to recognition schedules.

Contract modifications are tagged distinctly. True ups are tracked carefully. Every transaction (or ledger entry) must carry enough metadata to route correctly into the right schedule line.

Revenue schedules table structure

- Contract ID, line ID, obligation ID, start and end dates, recognition method, allocated transaction price, recognised to date, and remaining amounts.

- Transparent calculations, auditable fields, clear linkage to GL accounts for revenue, deferred revenue, and contract assets.

Critical linkages

Map billed lines to performance obligations. Allocate transaction price at SSP. Maintain GL account mapping that posts correctly to financial statements.

Practical expedients and policy choices

Support expedients like ignoring significant financing components under one year. Document policies. Link memos to affected schedules.

Deloitte's 2026 Ind AS Roadmap confirms that AI assisted schedules are acceptable if audit trails remain immutable. This validates automated approaches, provided version history and approval workflows are in place.

Dashboard design: key views and reports

Executive summary view

Show current month and quarter recognised revenue versus plan. Track deferred revenue movement and backlog remaining. These views anchor performance reviews and give leadership instant visibility into revenue recognition Ind AS 115 compliance.

Deferred revenue visualisations

Waterfall charts by month or quarter reveal timing patterns. Release schedules for the next 12 to 24 months provide forward visibility. Aging buckets flag old balances that may indicate stale contracts or recognition errors.

Milestone revenue reporting views

Project and contract level milestone status. Recognised versus milestones achieved. Variance analysis to catch revenue without acceptance or unrecognised completed milestones.

Subscription analytics dashboards

MRR and ARR trends, cohort analysis, recognised versus billed reports for prepaid plans, and upgrade or downgrade proration.

These insights separate growth quantity from growth quality, a vital distinction for leaders and investors.

Reconciliation panels

GL versus revenue subledger reconciliation. Invoice totals versus recognition schedules. GST adjustments that impact net revenue recognition.

These panels reduce close time and audit friction. They also satisfy the GSTIN wise reconciliation now required under GSTR 9C.

Exception views

Missing terms, negative balances, inconsistent schedules, and unmapped performance obligations: all surfaced without delay. Exception views are your early warning system against misstatement.

Aligning with Ind AS 115 compliance requirements

Five step model operationalised

Step one: identify contracts with commercial substance and approval status.

Step two: identify distinct performance obligations with point in time or over time tagging.

Step three: determine transaction price including variable consideration.

Step four: allocate price to obligations based on relative SSP.

Step five: recognise revenue when or as obligations are satisfied.

Reference the ICAI's Ind AS standards page and the Grant Thornton guide for worked examples.

India specific edge cases

Bundled offerings combining software, implementation, and support must be unbundled and allocated at SSP. Discounts and free goods must be allocated systematically.

Modifications and usage based fees need estimation and true ups. ICAI's April 2026 study circle confirmed that hybrid SaaS plus services contracts should unbundle at SSP and true up variables quarterly.

Documentation requirements

Policy memos by revenue stream. Assumptions libraries for estimates. Audit ready evidence for each contract and schedule.

Documentation is the difference between smooth audits and extended procedures. With NFRA's 2025 and 2026 focus on SME revenue, this is not aspirational. It is survival.

Period close checklist

- Tie subledger detail to GL control accounts for revenue, deferred revenue, and contract assets.

- Review deferred revenue releases. Investigate large or unusual movements. Validate exceptions.

- Spot check high risk contracts and disclosures. Produce Ind AS 115 statements efficiently using your dashboard data.

- Verify GSTIN wise splits match between recognition schedules and GSTR 9C data.

Further reading: MCA's latest Ind AS notifications, and the EY India insights on Ind AS 115 practical expedients.

Implementation pathways: comparing your options

Option 1: specialised revenue recognition SaaS

Deep Ind AS logic, strong audit trails, and purpose built dashboards. Pros include compliance coverage and vendor support. Cons include higher subscription costs (typically ₹5 to ₹15 lakh per year for SMEs), integration effort, and change management.

Works best for high volume, complex contracts, and listed entities.

Option 2: ERP or Tally modules plus BI

Leverage your existing stack with add ons and BI. Pros include familiarity and flexible reporting. Cons include heavy configuration and custom logic.

TallyPrime 5.0 (January 2026) improved deferred tracking, but still lacks full hybrid dashboard capabilities. Suits mid size firms with strong IT or CA partner support.

Option 3: Excel plus BI plus process controls

Lowest cash cost and quick setup for simple cases. Pros include flexibility. Cons include manual error risk, weak audit trails, scaling challenges, and key person dependency.

Use only for very low volumes and simple contracts. Upgrade as you grow.

Key decision factors

- Contract volume and complexity, audit intensity, budget, and IT bandwidth all drive your choice.

- Do not underestimate hidden labour costs, controls, and documentation needs.

- Factor in NFRA scrutiny: if your firm handles 50+ contracts with variable consideration, spreadsheets will not survive an inspection.

Vendor evaluation: critical questions to ask

Ind AS 115 and audit support

Ask how the system supports the five step model, variable consideration, and modifications. Request a demonstration on a complex contract. Verify GST integration and multi GSTIN handling.

Functional coverage

Confirm that both milestone and subscription models are handled in one system. Ensure deferred tracking and reconciliation to Tally. Probe treatment for exceptions and contract modifications.

Implementation and support

Request realistic timelines. Understand data migration plans and error handling. Review support SLAs and escalation paths.

Security and multi org capabilities

Seek ISO 27001 and SOC 2 certifications. Require role based access and change logs. Evaluate multi org setups for CA firms or groups, with isolation and consolidation.

India pricing benchmarks and ROI considerations

Typical cost bands

DIY Excel plus BI has low licences but high labour. ERP add ons require moderate licences with significant consultancy. Specialised SaaS charges per entity or volume: ₹5 to ₹15 lakh per year is the current market range for mid size deployments in India. Implementation varies by complexity.

Hidden costs to consider

- Data cleanup and master data normalisation (often 40 to 50% of total implementation time).

- Change management and training across finance, sales, and delivery teams.

- Extended audit work without strong evidence trails.

- Ongoing maintenance of rules and mappings as contracts evolve.

ROI drivers

Faster closes, fewer post close adjustments, better forecasts from backlog and ARR visibility, stronger governance and audit outcomes.

Reducing close time from 15 to 7 days transforms finance capacity for analysis and decision support.

Real world example: India SME with hybrid billing

Company profile

A Bangalore based HR SaaS plus services firm sells annual and quarterly subscriptions. It delivers implementation projects through milestones. It processes change orders and discounts, and occasionally issues credits.

Building the recognition schedules

Subscriptions allocate at SSP and recognise time based straight line. Prorate upgrades and downgrades mid term.

Projects define milestones with acceptance criteria. Recognise at achievement. For long contracts, use percentage of completion based on input costs.

Dashboard outputs

Deferred revenue waterfalls predict future releases and renewal risks. Milestone revenue reports show recognised versus remaining value per project. Subscription analytics track MRR and ARR growth with expansion insights.

Close and audit process

Automated journals post to Tally. Reconciliation dashboards resolve variances before close. Audit ready schedules and policy references shorten audit time significantly.

The firm passed its 2025 statutory audit without extended procedures, a direct result of immutable logs and documented SSP catalogs.

How AI Accountant fits in your stack

Data ingestion and normalisation

AI Accountant pulls invoices, contracts, and notes directly from Tally. It normalises customer names and IDs, standardises product or service codes with revenue attributes, cleans contract identifiers and line items, and flags mismatches up front.

Structured revenue data preparation

Builds clean transaction tables for scheduling. Maps invoice lines to performance obligations and recognition methods. Computes simple time based schedules. Feeds complex scenarios into specialised engines.

Clean data is the foundation for trustworthy recognition.

Pushing results back

Summarised journals flow to Tally. Curated datasets feed Power BI. Bi directional sync keeps source systems and analytics aligned.

Current capabilities and roadmap

AI Accountant excels at cash, receivables, and payables dashboards, powered by robust pipelines. See data pipelines from books to dashboards.

The platform now includes native five step mapping, GSTIN normalisation, and Power BI exports for MRR and ARR (2026 update). It is extending to full revenue recognition dashboards, partnering for deep Ind AS logic where needed, while remaining the integration and data quality backbone.

Multi org support with 500+ CA firms and 300 million plus processed transactions demonstrates scalability and reliability.

Common risks and pitfalls to avoid

- Inconsistent contract IDs and customer codes across Tally and Excel. Establish a single source of truth early.

- Missing contract modifications and variable consideration updates. Build change tracking into process from day one.

- Mixing billed and recognised views. Label dashboards clearly and reconcile rigorously.

- GST and posting errors. Validate the split between GST and revenue in journal entries. GSTIN wise tagging must happen at ingestion, not at year end.

- Overreliance on uncontrolled spreadsheets. Add maker checker workflows and version history immediately, even for interim solutions.

- Over optimistic variable estimates in projects. MCA alerts in 2026 highlight this as a common misstatement driver.

Step by step implementation roadmap

Phase 1: discovery

- Map contract types and billing models. Document current Ind AS 115 policies and gaps. Assess data quality.

- Identify GSTIN wise reporting requirements and current gaps in your filing workflow.

Phase 2: data preparation

- Use AI Accountant ingestion for Tally. Clean master data for customers, products, and contracts.

- Define mapping rules from invoice lines to performance obligations.

Phase 3: schedule design

- Choose recognition methods for each obligation type.

- Configure SSP allocation and variable consideration.

- Set exception handling for unusual contracts.

Phase 4: dashboard build

- Start with the most critical views: deferred waterfalls, milestone status, subscription analytics.

- Include reconciliation and exception reports from day one.

Phase 5: controls and go live

- Implement maker checker and approvals.

- Run parallel periods to resolve variances.

- Go live with close monitoring and scheduled reviews.

Taking the next step

Begin with a no obligation assessment. Identify your contract types and Ind AS 115 gaps. Evaluate data readiness in Tally. Select the approach that matches your volume, complexity, and audit intensity.

Share anonymised samples for realistic estimates. Get a demo of AI Accountant ingestion and mapping with your data. Agree scope, integrations, and timeline.

The path to compliance and operational visibility is practical and achievable, with the right dashboard and data engine.

Helpful references: the ICAI Ind AS standards page, the Grant Thornton paper, and the MCA Ind AS notifications portal.

FAQ

Can Tally alone meet Ind AS 115 requirements for hybrid contracts?

For simple straight line subscriptions at small volumes, yes. But once you add modifications, milestones, variable consideration, and disclosure needs, native billing views fall short. TallyPrime 5.0 improved deferred tracking but still lacks full SSP and variable logic (2026 update). Combine Tally with a data engine such as AI Accountant plus BI, or adopt specialised revenue recognition software for comprehensive compliance.

How do subscriptions and milestone recognition coexist within a single dashboard without misstatement risk?

Classify obligations at the line level and maintain separate recognition methods per obligation, then roll up into unified schedules and summary views. Clear mapping rules, SSP allocation, and exception handling ensure coherent aggregation. AI Accountant helps structure the data so BI can present both models accurately.

What is the minimum data set a CA should demand before designing revenue schedules?

Contracts with terms and approval status, identified performance obligations, transaction price including variable consideration, SSP allocation basis, and schedule parameters (dates and methods). Without these, the five step model cannot be evidenced. Insist on master data cleanup before schedule design.

What realistic implementation timeline should a CA advise for an SME with mixed subscriptions and projects?

Four to twelve weeks, depending on data quality and complexity. Discovery and data cleanup often take half the time. Parallel runs for one or two periods are essential to validate recognition and reconciliations before go live.

How do we estimate and true up variable consideration such as performance bonuses or penalties under Ind AS 115?

Document estimation policies, maintain assumptions libraries, and post true ups when outcomes crystallise. ICAI's 2026 study circle recommends quarterly true ups for hybrid SaaS plus services contracts (2026 update). Build audit trails that show original estimates, revisions, and final outcomes.

What makes a revenue waterfall "audit ready" under current NFRA expectations?

An audit ready revenue waterfall must include version history for every schedule change, user activity logs with timestamps, linked policy memos, and immutable records that cannot be edited after period close. NFRA's 2025 and 2026 inspections specifically test for these attributes in SME revenue samples (2026 update). Without them, expect extended procedures or qualification.

How do GSTIN wise requirements in GSTR 9C interact with revenue recognition dashboards?

Revenue is recognised net of GST, but CBIC's December 2025 circular requires GSTIN wise revenue splits in GSTR 9C reconciliations (2026 update). Your dashboard must tag each revenue line by GSTIN at the point of ingestion, then reconcile between recognition schedules and GST returns. Multi GSTIN entities need entity level dashboards that roll up cleanly.