Key takeaways

- A KPI data dictionary India gives every team one shared source of truth, locking definitions, formulas, and data lineage so Tally, GST returns, and dashboards always agree.

- India specific rules (GST exclusive revenue, TDS timing, April to March fiscal year) must be baked into every formula to prevent metric drift and audit surprises.

- Governance principles, data quality checks, and benchmark ranges let CAs, CFOs, and founders compare performance across periods and act with confidence rather than guesswork.

- Dashboard mapping converts raw AR, AP, GST, and cash data into visual insights, cutting decision time and boosting accountability across the finance team.

- Manual reconciliation and inconsistent definitions are the root cause of reporting errors. Automating bookkeeping and reconciliation workflows reduces rework, improves accuracy, and keeps compliance on track.

- Start with five to seven core metrics (revenue, cost, cash, DSO, GST match rate), validate on one fiscal quarter, then scale. Waiting for a "perfect" dictionary delays every downstream decision.

KPI Data Dictionary India: What's New in 2026

The compliance landscape around financial metrics has shifted noticeably since FY 2024 25. Two changes matter most for anyone building or maintaining a KPI dictionary.

First, the GST e invoicing turnover threshold dropped from ₹5 crore to ₹1 crore effective August 2023, and the GST portal now enforces stricter schema validations on IRN generation. By early 2026, businesses below ₹5 crore that had never dealt with e invoicing are well inside the mandate. Their KPI dictionaries must now include e invoice success rate and IRN rejection rate as standard compliance metrics, fields that simply did not exist for them two years ago.

Second, GSTR 2B reconciliation expectations have tightened. The CBIC's recent circulars clarify that ITC claims unsupported by GSTR 2B data face reversal with interest at 18 percent per annum. In practice, this means your GSTR 2B Match Rate KPI is no longer a nice to have dashboard tile. It is a financial risk metric. Firms below 95 percent match rates now carry measurable interest exposure every month they delay vendor follow ups.

The operational shift is real. Finance teams must now reconcile ITC monthly (not quarterly), tag unmatched invoices by vendor within seven days of the GSTR 2B release, and escalate chronic mismatches before the filing deadline. Ignoring this workflow risks blocked ITC, penalty notices, and cash flow surprises during assessment.

What to do now:

- Add e invoice success rate and IRN rejection rate to your dictionary if your turnover crosses ₹1 crore.

- Set your GSTR 2B Match Rate alert threshold at 95 percent, with vendor escalation triggered at 90 percent.

- Review ITC reversal exposure monthly, not at year end.

Teams already using GST reconciliation automation can run 2B matching within hours of the statement release, flagging gaps before they become penalties.

What Makes a KPI Dictionary Essential for Indian Businesses

Understanding the India specific context

Indian SMBs operate in a complex environment. GST inclusive invoicing inflates the top line. TDS leads to timing differences. Bank statements include UPI and NEFT references. Systems like Tally follow their own ledger conventions.

Without a KPI dictionary, revenue definitions drift. DSO calculations differ across teams. Monthly results lose comparability.

Standardization turns ambiguity into clarity. You decide once how to define and compute, then every team follows the same playbook.

Who benefits from standardized KPIs

- Chartered Accountants reduce rework when formula standards are common across ledgers and dashboards.

- CFOs track benchmark ranges consistently. When DSO moves from 45 to 60 days, they know exactly why.

- Founders get transparent dashboard mapping. Revenue means revenue, not a shifting definition.

Shared definitions, standardized formulas, benchmark ranges, dashboard mapping, and sample visuals make data actionable and discussions productive.

Building Governance Principles for Your KPI Dictionary

Establishing naming conventions and standards

- Define short name, long name, and aliases. For example: DSO, Days Sales Outstanding, DRO.

- Specify periodicity and units (daily or monthly, INR, percentages, or counts).

- Align to April to March fiscal year. Document FX treatment and rounding rules.

Identifying source of truth fields

Map each metric to its origin system. Sales from Tally Sales group, bank reconciliation via IFSC and UPI references. Document lineage end to end: invoice creation, GST computation, final ledger postings.

Implementing data quality checks

Set reconciliation standards at 100 percent for critical metrics. Build duplicate detection on invoice and bill numbers. Ensure dates align to fiscal calendar. Validate HSN or SAC codes for GST.

The ICAI's guidance on accounting standards provides a useful reference for documentation and internal control expectations that apply directly to KPI governance.

Core Financial Metrics with India Specific Formula Standards

Revenue metrics and calculations

Gross Revenue equals total invoice value including GST and advances. Net Revenue equals Gross Revenue minus returns minus GST output tax.

Example: a bill of ₹1,18,000 at 18 percent GST yields net revenue of ₹1,00,000. Always strip GST before computing margin or growth metrics.

Cost and profitability metrics

- COGS equals Opening Inventory plus Purchases minus Closing Inventory.

- Operating Expenses include non COGS items like rent and salaries. Capitalize consistently where policy requires.

- Gross Profit equals Net Revenue minus COGS. Gross Margin equals Gross Profit divided by Net Revenue times 100.

- EBITDA equals Net Revenue minus COGS and OpEx plus Depreciation and Amortization. EBITDA Margin is the percentage view.

- Net Profit follows EBITDA minus Interest, Tax, and Depreciation. Net Margin reflects the bottom line.

Liquidity and cash flow metrics

- Cash in Bank uses reconciled balances, not book estimates.

- Operating Cash Flow aggregates core inflows and outflows. Negative OCF becomes Operating Cash Burn.

- Runway equals Cash divided by Monthly Burn.

- Current Ratio equals Current Assets divided by Current Liabilities. Include GST receivables and payables.

- Quick Ratio equals Cash plus AR divided by Current Liabilities. Inventory is excluded.

- Track bank charges and FX differences with proper realization and unrealization classification.

Working Capital Metrics: AP, AR, and Collections Formula Standards

Accounts receivable management

Age AR into 0 to 30, 31 to 60, 61 to 90, and beyond 90 day buckets. Anchor aging to GST invoice date for compliance alignment.

DSO or DRO equals Average AR divided by Credit Sales times 365. Define credit sales clearly. Exclude advances and cash sales.

Accounts payable optimization

Age AP similarly. Analyze vendor wise patterns. DPO equals Average AP divided by Credit Purchases times 365. Balance cash efficiency with vendor relationships.

Vendor invoice (also called a bill) aging helps identify which suppliers consistently send late documentation, a common cause of ITC mismatch.

Collection efficiency metrics

- Collection Efficiency equals Collections divided by Billed Amount times 100.

- Write off Percentage equals Write offs divided by Total Billed. Target under 2 percent.

- Dispute Percentage equals Disputed Amount divided by Total AR.

Compliance Metrics Specific to Indian Regulations

GST compliance tracking

GST Payable equals Output Tax minus ITC. Net GST Position shows payable versus credit.

GSTR 2B Match Rate equals Matched ITC divided by Eligible ITC times 100. Target above 95 percent. Below 90 percent should trigger immediate vendor follow ups (2026 update).

GSTR 1 Accuracy equals Posted Invoices divided by Reported Invoices times 100. Track On time Filing Percentage monthly. The GST Council's latest recommendations continue to tighten return filing timelines and ITC claim windows.

TDS compliance measurements

TDS Compliance Rate equals Amount Deducted and Deposited divided by Required Amount times 100. Monitor Mismatch Resolution Time. Reconcile Form 26AS and books frequently.

The Income Tax Department's portal now provides near real time 26AS updates, making monthly reconciliation practical for most firms.

Industry Specific Metric Definitions and Formulas

D2C and retail metrics

- Contribution Margin per Order equals Net Revenue per Order minus Variable Costs.

- Return Rate Percentage equals Returns divided by Total Orders. Festive seasons can spike returns significantly.

- Marketplace Commission Percentage captures platform fee variability.

- Logistics Cost per Order typically ranges ₹40 to ₹100 depending on city tier.

SaaS and subscription business metrics

- MRR and ARR provide recurring revenue lenses.

- Churn Rate equals Lost MRR divided by Starting MRR. NRR incorporates expansion revenue.

- CAC equals acquisition spend divided by new customers. LTV equals ARPU multiplied by Customer Lifetime.

India specifics: GST on advances, FIRC for foreign customers.

Professional services metrics

- Utilization Rate equals Billable Hours divided by Available Hours. Target 70 to 80 percent.

- Realization Rate equals Billed Amount divided by Billable Amount.

- WIP tracks accrued but unbilled revenue. Watch the cash flow impact carefully.

Benchmark Ranges for Indian SMBs

Understanding industry standards

Benchmarks provide context, not rules. Services often show DSO 45 to 60 days and gross margins 40 to 60 percent. Manufacturing cycles run longer with margins 20 to 40 percent. D2C operates faster. SaaS margins of 70 to 90 percent offset acquisition costs.

Adjusting for Indian context

Festive seasonality, regional payment behaviors, and GST compliance thresholds all matter. A GSTR 2B match rate above 95 percent is a healthy target.

Cash runway targets work well as a traffic light system: under 6 months is red, 6 to 12 months is yellow, 12 plus months is green. These thresholds help founders and investors align on risk tolerance quickly.

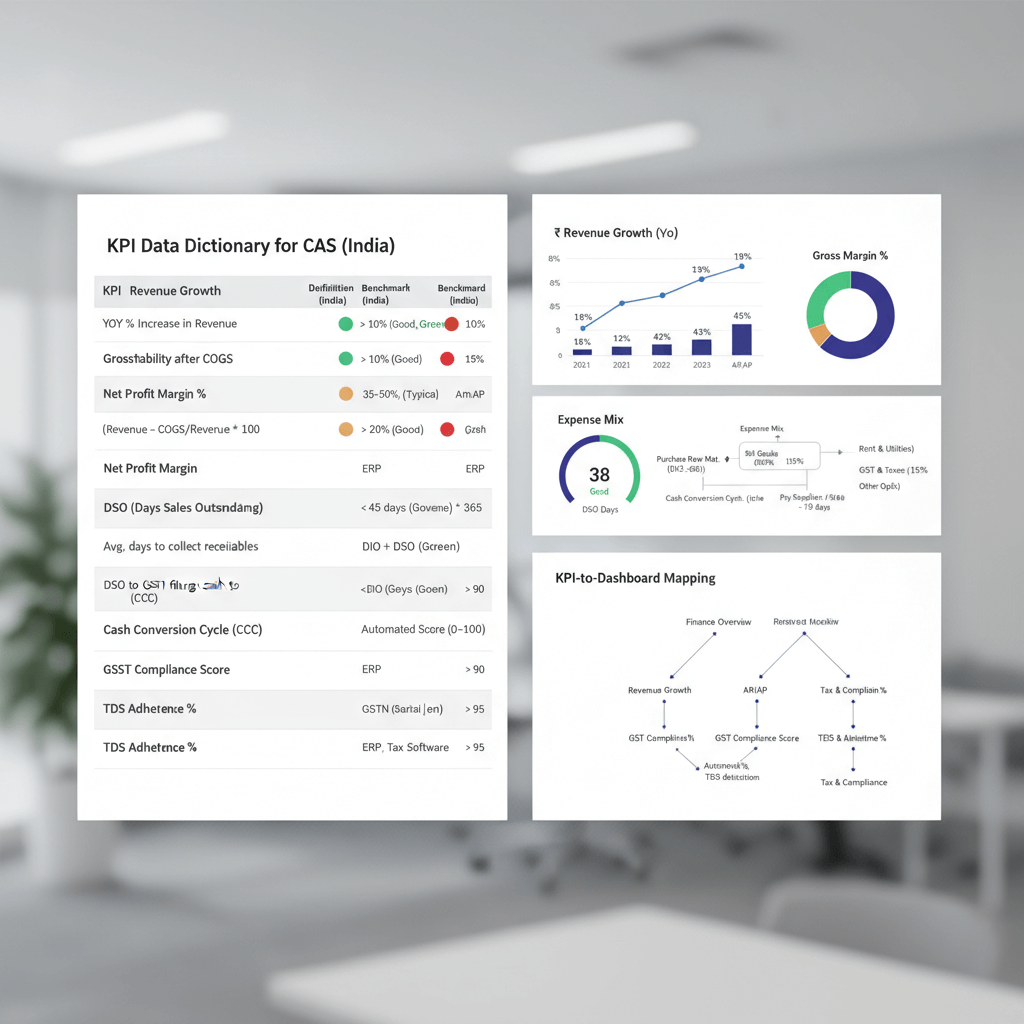

Dashboard Mapping: From Raw Data to Visual Insights

Connecting metrics to data sources

Map Net Revenue to Tally Sales. Include credit notes and GST output tax. Align to fiscal months.

Compute DSO and DPO from AR and AP aging. Present heatmaps and ratio tiles. Compare GSTR 2B downloads with book entries to produce match rates. Use compliance panels for visibility.

Calculate runway using bank cash and operating burn.

Implementing dimensional analysis

Slice by customer, vendor, SKU, GSTIN, state, or channel. Map UPI and POS transactions correctly. Exclude non cash items from OCF.

Highlight FX gains, bank charges, refunds, and loan principals in detail tables. This level of dimensional analysis (also called multi dimensional reporting) turns a flat ledger entry into a navigable data set.

Creating Effective Visual Representations

Revenue and expense visualizations

Use stacked monthly bars for net revenue versus costs. Add dual axis charts with lines for profit and percentages for margins. Provide captions like MoM trends post GST adjustment for clarity.

Cash flow and liquidity displays

Plot OCF and cash balance. Add runway gauges with clear color logic.

Include dotted forecast projections for optimistic and pessimistic scenarios. This helps founders communicate burn context to investors without ambiguity.

Working capital heatmaps

AR and AP aging heatmaps reveal bottlenecks. Summarize DSO and DPO with tiles and 6 month sparklines.

Compliance status panels

Use gauges for GSTR 2B match and TDS compliance. Calendar heatmaps show filing timeliness at a glance.

Transaction detail tables

List highlights: date, amount, and type. Include bank charges, FX adjustments, refunds, and loan principals. Add filters and export options for deeper analysis.

Implementation Checklist for Your KPI Dictionary

Phase 1: Inventory and documentation

- List systems. Mark source of truth per metric.

- Document definitions and formulas. Obtain CA sign off.

- Create a master sheet with metric owner, source, and refresh cadence.

Phase 2: Customization and testing

- Adjust benchmarks by sector and scale.

- Set alert thresholds. For example, DSO above 60 days.

- Map data to calculations and visuals. Validate on historical fiscal data.

Phase 3: Automation and maintenance

- Automate reconciliation, bank feeds, and transaction matching where possible.

- Adopt monthly review cycles: collect, validate, analyze, act.

- Version control your dictionary. Add, modify, or retire metrics as needed.

Common Pitfalls in Indian Financial Metrics

GST related mistakes

Using GST inclusive revenue for margin calculation distorts results. Reconcile against GSTR 2A and GSTR 2B. Track unclaimed ITC separately.

Payment platform complications

Classify marketplace settlements correctly. Payouts count as revenue. Processing fees count as OpEx. Model settlement timing in your cash flow projections.

Foreign exchange handling

Separate realized and unrealized FX. Stabilize P&L and balance sheet presentation. Track exposure per currency.

Accrual adjustments

Amortize prepayments monthly. Capitalize assets consistently by policy.

Bank statement reconciliation

Normalize bank formats. Map IFSC and UPI IDs properly. Prefer daily reconciliation to avoid month end surprises. This is especially important as UPI transaction volumes continue to grow, with RBI data showing consistent year on year increases in digital payment processing.

Leveraging Technology for KPI Management

Automation tools and solutions

- AI Accountant, built for Indian SMBs. Automatic bank statement processing for 50 plus formats, GST aware ledger mapping, and direct Tally integrations. Strong classification predictions and compliance ready dashboards.

- QuickBooks India, GST features with basic dashboards. Manual bank reconciliation effort remains.

- Xero, strong multi currency and cash flow forecasting. Requires customization for GST in India.

- FreshBooks, simple for services. Limited Indian compliance depth.

- Tally Prime, the most widely used accounting software in India. Excellent for ledger management. Dashboard and automation capabilities require add ons or integrations.

Integration capabilities

Prefer bidirectional sync to pull and push clean entries across Tally. Handle PDFs, CSVs, Excel, and scans with strong OCR built for Indian formats. Emphasize batch processing for scale.

Roadmap considerations

Adopt GSTR 2B auto matching, predictive cash flow, and multi entity capabilities. Prepare for account aggregator based direct bank feeds for frictionless ingestion.

Templates and Resources for Quick Implementation

Essential templates

- Master sheet with definitions, formulas, benchmarks, and mappings.

- Inventory of KPIs with owner, source, refresh frequency, and last update.

- Formula library with examples for product and services DSO.

Visual asset library

- Wireframes: revenue versus cost bars, cash flow trends, AR and AP heatmaps, compliance gauges.

- CSV sample files aligned to your structure. These ease vendor onboarding.

- Dummy data for realistic stress testing.

Maintenance documentation

- Version log for formula changes and rationale.

- Monthly validation checklist: reconciliation, formula audit, benchmark review.

- Troubleshooting guides for GST mismatch resolution and DSO spike investigation.

Moving Forward with Your KPI Dictionary

Starting small and scaling

Begin with revenue, cost, and cash metrics. Then layer in AP and AR. Add compliance metrics next. Finally, bring in industry specifics like MRR and contribution margin.

Building team alignment

Share the dictionary widely. Train on source systems and calculations. Create feedback loops for clarity and new visibility needs.

Measuring success

Track adoption, data quality improvement, and decision speed. Observe behavioral shifts from intuition to metric driven actions.

Your KPI data dictionary India becomes the foundation for data driven growth. The sooner definitions are locked, the sooner every conversation about performance starts from shared ground.

FAQ

As a CA, how do I define Net Revenue for Indian SMBs so Tally always matches my reports?

Use GST exclusive revenue consistently: Net Revenue equals Gross Revenue minus returns minus GST output tax. Reconcile to Tally Sales group totals, document lineage in the KPI dictionary, and automate checks to flag GST inclusive entries before they reach dashboards.

What is the correct DSO formula under Indian GST?

Age from GST invoice date to align with compliance. DSO equals Average AR divided by Credit Sales times 365. Define credit sales clearly by excluding advances and cash sales. Maintain a rule to exclude disputed invoices if your policy demands, and present both "all in" and "policy" DSO variants for transparency.

How should GST ITC mismatches be reflected in compliance KPIs?

Track GSTR 2B Match Rate (Matched ITC divided by Eligible ITC times 100) with a 95 percent target. Below 90 percent should trigger vendor follow ups immediately, as unmatched ITC now faces reversal with 18 percent interest under tightened CBIC enforcement (2026 update). Age unmatched ITC by month and escalate chronic gaps before filing deadlines.

How do I compute Runway and Burn for founders and reconcile it to bank statements?

Runway equals Cash divided by Monthly Burn, with burn derived from Operating Cash Flow excluding non cash items. Reconcile to bank statements via IFSC and UPI references. Use reconciled bank balances, not book estimates, as the cash numerator to keep the metric trustworthy.

What naming conventions and rounding rules should I enforce in a KPI dictionary?

Use short name, long name, and aliases where applicable. Define periodicity and unit, adopt INR as the base with documented FX rules, and set 2 decimal places for percentages with policy based rounding for amounts. Include worked examples for each rule so the dictionary is both audit ready and training friendly.

For manufacturing clients, what benchmark ranges should I publish for DSO, DPO, and gross margin?

Typical Indian manufacturing ranges are DSO 60 to 90 days, DPO 60 to 90 days, and gross margin 20 to 40 percent. Document sector context, credit terms, and production cycle length, then localize benchmarks using your client's historical data rather than relying on generic industry averages alone.

Do I need to add e invoicing metrics to my KPI dictionary now?

Yes, if your turnover crosses ₹1 crore. Since the e invoicing threshold dropped to ₹1 crore, businesses must track e invoice success rate and IRN rejection rate as standard compliance KPIs (2026 update). These metrics catch schema validation failures early and prevent downstream GST filing errors.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.