-01%201.svg)

Key takeaways

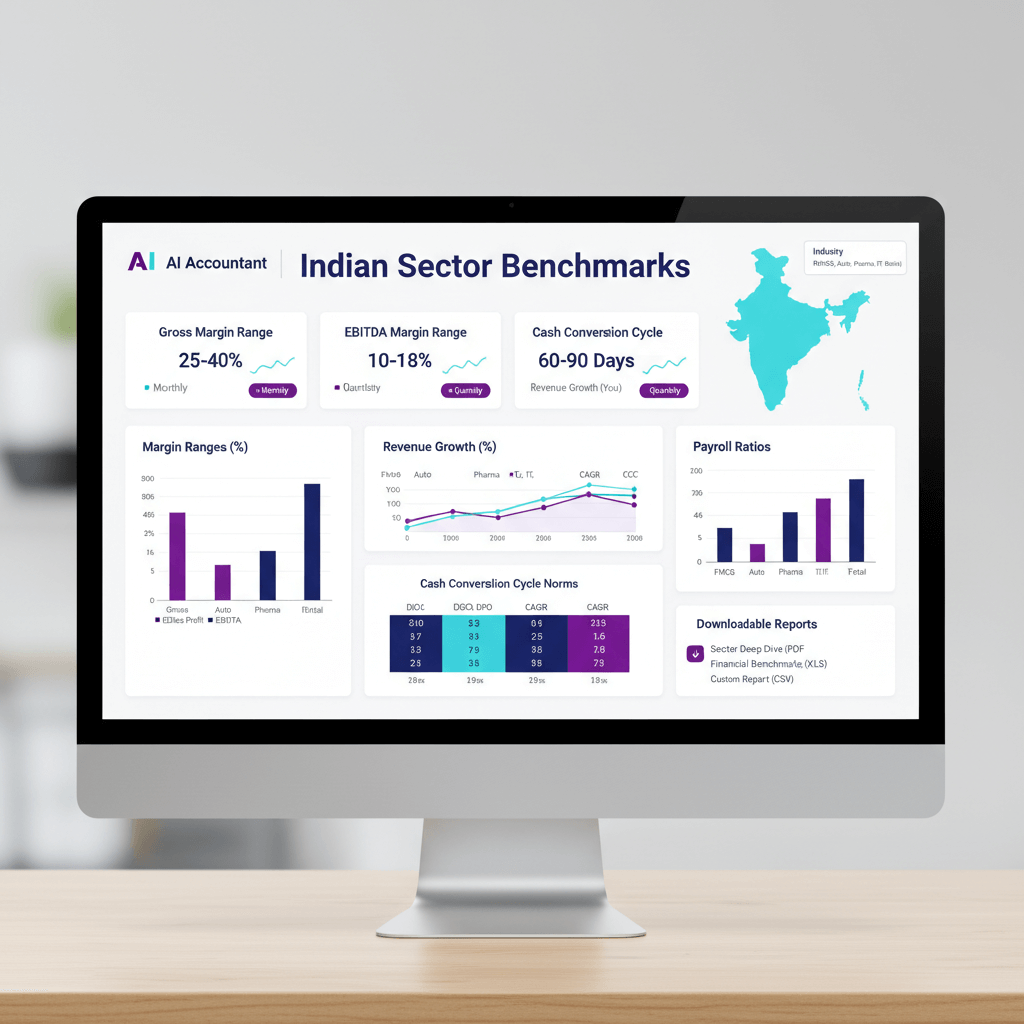

- Benchmark Library India gives India first ranges for margins, cash cycles, growth, and payroll ratios, built from real ledgers, bank data, and GST filings.

- Sector, city tier, and maturity segmentation lets CAs and finance teams compare like with like, then set realistic targets quarter by quarter.

- Use it during budgeting, lender conversations, vendor negotiations, pricing reviews, and cash flow troubleshooting, so decisions are grounded in data, not guesswork.

- Quartiles, not averages, show healthy ranges, with outlier trimming, reconciliation checks, and clear treatment rules for clean comparisons.

- Red flags like Rising DSO, payroll creep, and CCC drift are paired with practical levers you can execute now.

- Monthly, quarterly, and annual refreshes keep the benchmarks current, with transparency on last updated dates and coverage.

- Privacy and compliance standards ensure only aggregated, anonymised insights, never firm level data.

Who should use this benchmark library India

Indian finance teams need answers fast, not another spreadsheet rabbit hole. Benchmark Library India delivers a living, India first reference for Chartered Accountants, SMB finance leads, and founder CFOs, standardising margin ranges, cash cycle norms, growth metrics, and payroll ratios for small and mid size businesses.

Why do India specific benchmarks matter more than global decks you have been referencing? GST complexities, UPI adoption, marketplace dynamics, TDS and TCS quirks, festival seasonality, and our unique credit culture make generic benchmarks unhelpful for Indian businesses.

Who benefits

- Chartered Accountants use the ranges for client reviews, tax planning, and quarterly health checks, so the question, are we doing okay, is answered with data.

- Finance leads at SMBs lean on benchmarks for budgets, board decks, lender discussions, and performance reviews.

- Founder CFOs and operator founders pull up benchmarks before vendor negotiations, pricing changes, hiring decisions, and cash flow troubleshooting.

When to use

- Annual and quarterly budgeting, lender applications and renewals, board and investor reviews.

- Vendor and landlord negotiations, pricing and discount policy changes.

- Hiring plans and payroll sanity checks, plus cash flow troubleshooting when runway feels tight.

Sometimes the problem is not revenue, it is the time it takes to hit your bank.

Scope, sectors, maturity tiers, and city tiers

Sectors covered

Retail spans grocery, fashion, and electronics, with distinct inventory turns and margin profiles. D2C and e commerce covers own site, marketplaces, and ONDC linked platforms, where RTO rates and fees hit margins. Services includes IT, consulting, agencies, and professional services, where utilisation and billable hours drive results. Manufacturing spans light assembly, job work, and contract setups, where raw material volatility and wastage matter. Logistics and transport includes line haul, last mile deliveries, and fleet owners, driven by fuel and utilisation. Healthcare spans clinics, diagnostics, and day care. F and B and QSR covers cloud kitchens, dine in, and quick service chains.

Business maturity tiers

- Early stage, less than three years, shows high variance and erratic growth.

- Scaling, three to seven years, shows stabilising patterns and meaningful benchmarking.

- Mature, over seven years, prioritises efficiency, cash generation, and margin improvement.

City tier impact

- Metros carry higher rent and payroll, but faster UPI and card adoption, plus better credit access.

- Tier two has lower fixed costs, but longer receivable cycles and more cash heavy sales.

- Tier three runs hyperlocal, with higher variance and informal practices.

Methodology and data hygiene

Data sources

- Bank statement aggregates via secure feeds, capturing real cash flows.

- Accounting systems like Tally and Zoho Books, syncing ledger level details.

- AP and AR ledgers for precise receivable, payable, and CCC calculations.

- Cross checks with GST filings validate turnover and input credits, with seasonality overlays for festivals and monsoons.

Key definitions used consistently

- Gross margin equals revenue minus cost of goods sold, divided by revenue.

- Contribution margin equals revenue minus variable costs, divided by revenue.

- EBITDA margin equals EBITDA divided by revenue.

- Net margin equals net profit after tax divided by revenue.

- Cash Conversion Cycle, CCC, equals inventory days plus receivable days minus payable days.

- Growth rates include year over year growth and three year CAGR bands.

- Payroll ratios include payroll cost as percent of revenue, and revenue per FTE.

Segmentation approach

- Sector first, then revenue bands, under five crores, five to twenty five, twenty five to one hundred, and over one hundred crores.

- City tiers, Metro, Tier two, and Tier three, for cost differences.

- Formalisation level, GST registered versus unregistered.

- Sales mix splits, cash, UPI, card, marketplaces, and exports.

Treatment rules

- Outlier trimming removes first and ninety ninth percentiles.

- Reports show quartiles, P25, median, P75, not simple averages.

- Both fiscal year and rolling 12 month views are available.

- GST inclusive versus exclusive figures are clearly labelled and normalised by sector where relevant.

- One off items like exceptional gains and subsidy income are adjusted out.

Compliance and privacy standards

Infrastructure aligns with SOC 2 Type 2 and ISO 27001 standards. Only aggregated, anonymised benchmarks are visible.

No firm level data, no reversibility, just clean, comparable ranges.

Core benchmark sections

Margin ranges by sector

For each sector, maturity, and city tier combination, the library presents typical gross, contribution, EBITDA, and net margin ranges by quartile, with commentary on drivers. Commodity volatility affects manufacturers, discounts and promotions compress retail margins, marketplace take rates and RTO costs pressure e commerce, and freight impacts everyone, especially low ticket items.

- Fashion retailers in metros often see gross margins of 45% to 60%, median around 52%, but EBITDA margins of 8% to 15%, median around 11%, given rentals and staff costs.

- IT services firms show gross margins of 35% to 50%, median around 42%, with EBITDA margins of 15% to 25%, median around 19%, driven by utilisation and bench.

Rule of thumb: if gross margins are stable but EBITDA compresses, overheads, wastage, or operating discipline need attention.

Cash cycle norms

Inventory days, receivable days, payable days, and the resulting CCC are tracked by sector and maturity, with India specific nuances called out. Distributor and dealer credit cultures extend receivables, festive stock builds push inventory, marketplace remittances and TDS or TCS deductions delay cash, and GSTR-2B reconciliation lags tie up working capital.

- D2C fashion often runs 60 to 90 days of inventory, 30 to 45 days of receivables including marketplace delays, and 45 to 60 days of payables, resulting in a CCC of 45 to 75 days.

- Manufacturers often run 45 to 60 days of raw material inventory, 60 to 90 days of receivables, and 30 to 45 days of payables, producing CCCs of 75 to 105 days.

Growth metrics that matter

- Early stage bands frequently span 50% to 200% annually, with high variance.

- Scaling bands stabilise to 20% to 50% with less quarter to quarter volatility.

- Mature bands target 5% to 15% with emphasis on margins and cash generation.

The library flags overheated growth patterns, for example, 80% revenue growth while CCC deteriorates from 45 to 90 days, which signals working capital stress ahead.

Payroll ratios and productivity

- Payroll as percent of revenue, roughly 8% to 15% in manufacturing, 15% to 30% in retail, 40% to 65% in services.

- Revenue per FTE ranges help calibrate hiring, IT services target 15 to 25 lakhs per FTE, retail stores aim for 8 to 15 lakhs per employee.

- Services teams monitor billable versus non billable mix and utilisation, manufacturing tracks shop floor versus office splits.

Guidance: services firms often wait for revenue per FTE to cross 20 lakhs before expanding teams, retailers target 12 lakhs per employee before adding headcount.

Red flags and practical levers

Common red flags

- Rising DSO despite revenue growth, hinting at collections strain or customer quality issues.

- Margin compression from freight, discounts, or marketplace fees, indicating pricing power erosion.

- CCC drifting above sector median for multiple quarters, showing working capital management breakdown.

- Payroll creep without productivity gains, a sign of inefficiency.

- High growth with negative operating cash flow over multiple periods, model stress in plain sight.

Practical levers for improvement

- Renegotiate vendor terms, add 15 to 30 days to payables without burning bridges.

- Offer 1% to 2% early payment discounts when cash allows, the ROI is often compelling.

- Tighten inventory policies, reorder points, ABC classification, and liquidate dead stock.

- Apply price increases or enforce discount discipline, lift margins by 2 to 5 percentage points.

- Restructure commissions and incentives to align with profitability.

- Adopt automation, tools like AI Accountant streamline AP or AR, reconciliations, and invoice discounting. Alternatives include QuickBooks, Xero, FreshBooks, and Tally.

India first nuances throughout

GST and reconciliation complexities

GST and GSTR 1, 3B, and 2B reconciliation affects both apparent and real margins. Input credit delays can make profitable months look loss making on a cash basis. TDS or TCS mismatches and delayed refunds trap working capital for months. A 2% TDS on a 10% margin business locks up 20% of profit.

Seasonal patterns unique to India

Festival peaks and monsoon cycles shape rhythms. Diwali can be 30% to 40% of annual sales for retailers and brands. Monsoons affect logistics costs, construction activity, and procurement cycles, creating predictable cash crunches.

Digital payment evolution

UPI versus cash changes float and reconciliation complexity. UPI settles instantly, but creates micro transactions to track. Cards carry MDR of 1% to 2%, and exporters face forex charges of 1% to 3%.

Marketplace and platform dynamics

Platform settlements deduct commissions, shipping, returns processing, and storage. RTO rates of 5% to 25% can flip unit economics. ONDC reduces commissions, but adds technology integration work.

Credit and lending patterns

EMI seasonality, balloon repayments, moratoriums, and top ups affect free cash flow. Working capital limits often ignore seasonal peaks, creating artificial constraints.

How to use this benchmark library India step by step

Getting started

- Pick your sector and sub niche, do not force fit categories.

- Match revenue band and city tier, a ten crore Tier two retailer should not benchmark against hundred crore metro chains.

- Pull your margins, CCC, growth, and payroll ratios for the last four to eight quarters, keep calculation consistent.

- Compare against quartiles to see where you sit versus P25, median, and P75.

Identifying improvement areas

- Spot gaps, below median margins, above median CCC, outlier payroll ratios.

- Map gaps to red flags and levers, then select proven remedies.

- Set targets, track quarterly, celebrate compounding wins.

Reading quartiles correctly

Treat the median as a healthy baseline, not a minimum. Use P75 as a two to three quarter target for well run businesses. P25 is not always bad, sometimes it reflects growth or share capture trade offs.

Setting realistic targets

- Margin improvement of 2 to 3 percentage points over two to three quarters.

- DSO and CCC reductions of five to ten days per quarter via focused collections.

- Inventory turns can move from 4x to 6x with disciplined buying and markdowns.

- Payroll productivity gains of 10% to 15% annually through training and process improvement.

Real world scenarios

Retail fashion brand case

A metro fashion brand sits at median margins, 52% gross, 11% EBITDA, but CCC is 30 to 40 days worse than peers. Diagnosis shows 120 days inventory versus 75 day median, and generous franchisee credit. Actions, stretch payables from 45 to 60 days, enforce open to buy discipline, and markdown slow movers. Two quarters later, CCC improves from 95 to 70 days, freeing two crores of working capital.

Small IT services transformation

A Tier two early stage services firm shows payroll at 68% of revenue, versus 55% median, and growth at 5%, versus 35% median. Root causes, 35% bench, 60% utilisation, below market rate cards. Actions, lift utilisation to 75% via pipeline management, lift new project rates by 15%, trim bench to 20%, enforce monthly project profitability. Six months later, payroll is 58%, growth 25%, EBITDA rises from 5% to 14%.

Light manufacturing efficiency drive

A Tier three mature unit runs EBITDA at 6%, below P25 of 9%, while gross margin holds at 31%, near median. Diagnosis points to overheads and efficiency, not pricing. Findings, 8% material wastage versus 4% benchmark, overtime overruns, low utilisation. Actions, tighter quality checks, renegotiate power and rent, add a second shift, prune low margin SKUs. Year end EBITDA recovers to 11%, above median.

When gross is okay but EBITDA lags, chase wastage, utilisation, and fixed cost absorption.

Update cadence and roadmap

Monthly updates

- Rolling refresh of leading indicators and cash cycle norms from bank and ledger data.

- High frequency growth indicators, orders, store count, customer adds, refresh monthly.

Quarterly deep dives

- Margin and payroll updates incorporate filings and audited numbers.

- Sector adjustments reflect regulatory changes and GST rate shifts, with trend commentary.

Annual rebenchmarking

- Full recalibration of sectors, definitions, and ranges.

- Method upgrades and new data sources, plus multi year trend reviews.

Roadmap enhancements coming

- GSTN integration for refined purchase and input tax benchmarks.

- Bank feeds via Account Aggregator for near real time CCC.

- Sub sector granularity, diagnostics versus clinics, cloud kitchens versus dine in, SaaS versus services.

Transparency standards

- Every sector page shows last updated date.

- Sample sizes and coverage by city tier and revenue band are disclosed.

- Method notes and caveats prevent misinterpretation.

Quiet integration benefits

With modern automation, your live metrics plot against Benchmark Library India ranges inside dashboards. AP or AR systems nudge collections and payment runs toward benchmarked norms. Reconciliations flag anomalies like DSO spikes or payroll drift early. Consistent ledger mapping standardises COGS versus overhead, enabling apples to apples comparisons.

Limitations and important caveats

Micro enterprise variations

Very small and cash heavy businesses show wide variance, treat ranges as indicative, not prescriptive. Hyperlocal businesses run on different fundamentals than city wide operations.

Platform business volatility

Marketplace fees, ads, and returns drive short term swings that smooth over quarters. Algorithm changes can shift unit economics overnight, so avoid point in time overreactions.

Sub niche structural differences

Diagnostics versus clinics, SaaS versus body shopping IT, cloud kitchens versus dine in, all need separate treatment. Where samples are thin, confidence flags suggest caution.

Taking action with Benchmark Library India

Download a quarterly checklist, subscribe for updates, map your metrics to the library template, and schedule recurring reviews. Build an improvement roadmap that targets specific metrics, then track progress visibly.

Stop guessing, start benchmarking, and compound small wins every quarter.

FAQ

As a CA, how do I present quartile ranges to a board without triggering panic?

Lead with the median as the healthy baseline, then show gaps by metric, for example EBITDA margin and CCC, and map each gap to a lever and a two quarter target. Position P75 as an aspirational range, not an overnight expectation. A simple one page bridge, current to target with levers and timing, keeps conversations calm and action focused.

How reliable are these ranges if my client straddles multiple channels, own site, marketplaces, and offline?

Use the sector primary, D2C or retail, then apply sales mix overlays, for example marketplace share and cash versus UPI or card splits. The library’s quartiles remain directionally correct. Where the mix is unusual, add a sensitivity note and track channel level margins separately for clarity.

Do the margins use GST exclusive revenue, and how are input credits treated?

Yes, revenue and margins are shown GST exclusive for comparability. Input credits are netted in COGS where relevant, so gross and contribution margins reflect true economics. If a sector’s GST treatment materially alters optics, a special note accompanies the ranges.

What is a sensible cadence for monitoring DSO and CCC for a manufacturing client?

Track DSO weekly on a rolling 13 week view during tight liquidity, otherwise monthly is fine. Review CCC monthly, then deep dive quarterly. Set five to ten day improvement targets per quarter. Use an AI tool like AI Accountant to automate reminders, escalation rules, and customer level risk flags.

How should I normalise payroll ratios for a services firm with a large bench and seasonal projects?

Report payroll as percent of revenue monthly and quarterly, split by billable versus non billable. Track utilisation weekly. Use revenue per FTE and project margin dashboards for quarterly reviews. Tools like AI Accountant can surface team level profitability and bench trends automatically.

My retail client has strong gross margin but weak EBITDA, what diagnostics should I run first?

Start with rent to revenue, staff cost to revenue, shrinkage or wastage, and discount leakage. Compare each to median and P75. Review stock turns and ageing, because slow movers inflate overhead absorption. Implement open to buy, markdown calendars, and incentive redesign. Expect two to three percentage point EBITDA recovery across two to three quarters if discipline holds.

For D2C, how do marketplace deductions and RTO affect CCC and margin benchmarking?

Treat marketplace settlements as receivables with embedded delays and deductions. Model RTO as negative volume with full landed cost. Align CCC by adding settlement lag days to receivable days. Benchmark against D2C quartiles that explicitly include marketplace effects, then pursue levers, packaging changes, address verification, and prepayment incentives.

What evidence should I carry into a lender renewal meeting to validate working capital needs?

Bring 12 month CCC trend with P25 to P75 sector range overlays, AR ageing with collection cohorts, inventory ageing, vendor term history, and a forward 13 week cash flow. Showing variance versus sector medians, plus actions in flight, strengthens the case for limits aligned to seasonal peaks.

How do I reconcile seasonality, for example Diwali, without misreading quarter on quarter changes?

Use year over year comparisons by month or quarter, and maintain a rolling 12 month view to smooth spikes. For festival quarters, compare against the same festival period last year, not the prior quarter. This avoids false alarms and aligns with how benchmarks are constructed.

What hiring guardrails should a scaling IT services firm use?

Wait for revenue per FTE to cross 20 lakhs, sustain 75% utilisation, and show two consecutive quarters of positive operating cash flow. If those hold, expand cautiously. An AI tool like AI Accountant can alert you when guardrails are met and simulate the impact of new headcount on project margins and cash.

Can I trust the library for niche healthcare, for example diagnostics versus clinics, with smaller samples?

Yes, directionally. Quartiles reduce outlier impact. Where samples are light, confidence flags advise additional judgment. Use the ranges as guardrails, then overlay your client’s unit economics, device utilisation, and payor mix to refine targets.

What quick wins typically move CCC by 10 to 20 days within two quarters?

Renegotiate vendor terms by 15 to 30 days, enforce invoice completeness for faster approvals, implement AR dunning with weekly touchpoints, shift slow movers with targeted markdowns, and automate GSTR 2B matching to release input credits faster. With AI Accountant, many of these workflows become autopilot, accelerating impact.