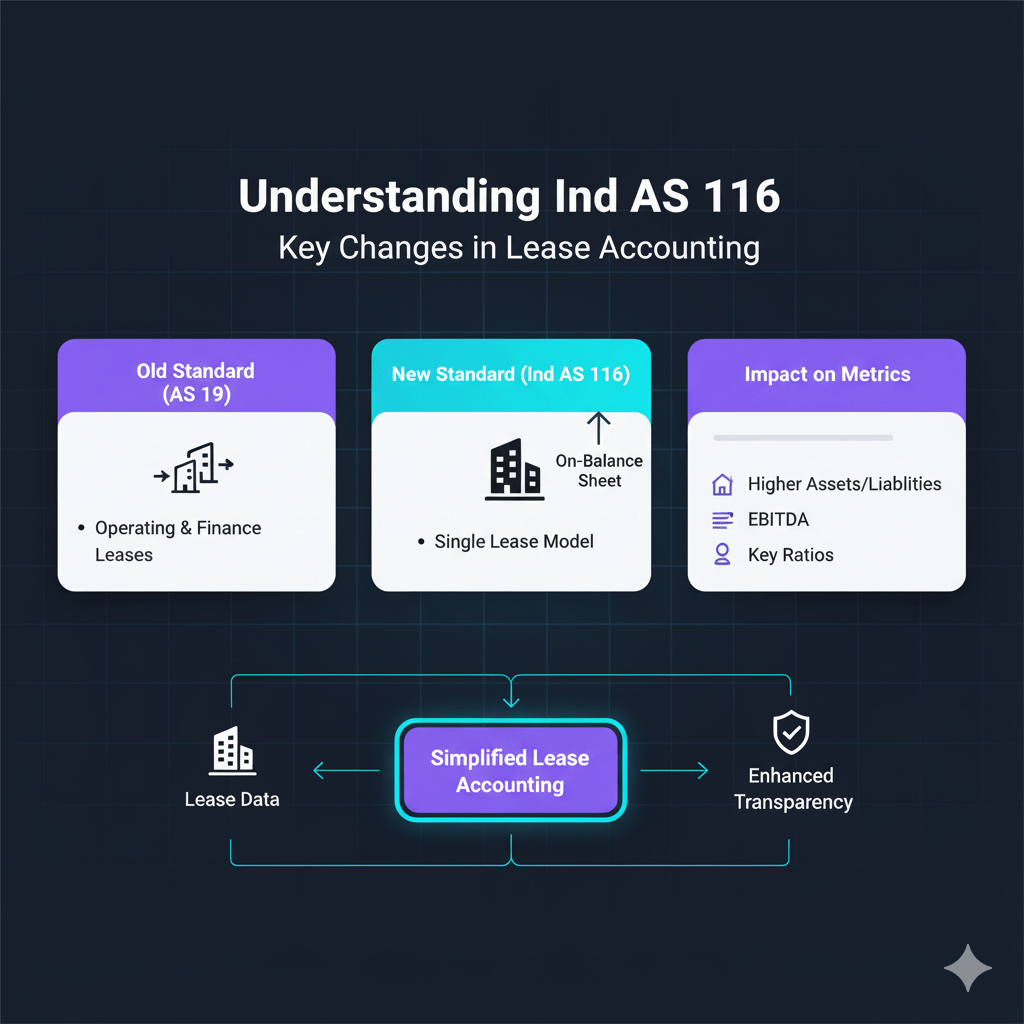

Ind AS 116, Leases, is the Indian Accounting Standard, that defines the principles relating to recognition, measurement, presentation, and disclosure of leases. The standard mandates a single lessee accounting model, which entails the recording of most leases on the balance sheet by the recognition of a Right-of-Use (ROU) asset and a corresponding lease liability.

Simply put, Ind AS 116 alters the reporting of leased assets and rented properties by companies, thereby increasing the transparency of financial statements.

Why was Ind AS 116 introduced?

Ind AS 116 was put in place to get rid of discrepancies as well as off-balance-sheet financing that were still present under the previous standard. Under Ind AS 17, a large number of leases, mainly operating leases, were not reflected in the balance sheet even though the companies had long-term payment commitments.

This most of the time led to:

- understated liabilities

- overstated profitability metrics (like EBITDA)

- comparability problems between companies

Ind AS 116 brings Indian accounting standards to the level of international norms and makes sure that the users of the financial statements receive a true and fair view of the entity’s leasing obligations.

Who must comply to Ind AS 116?

Ind AS 116 is applicable to all entities that follow Ind AS as per the Companies (Indian Accounting Standards) Rules.

This includes:

- Listed companies

- Unlisted companies meeting net worth thresholds prescribed by MCA

- Subsidiaries, associates, and joint ventures of Ind AS–compliant companies

- Companies voluntarily adopting Ind AS

Basically, any company that is required to follow Ind AS has to comply with Ind AS 116, unless there are specific scope exceptions or recognition exemptions.

Ind AS 116 Summary (For Quick Reading)

Major changes introduced

Ind AS 116 dramatically alters the way leases are accounted for, primarily by lessees. It supersedes Ind AS 17 and eliminates the separations of lessees’ operating and finance leases. As a result, most leases are accounted for off-balance-sheet operations through the recognition of a right-of-use asset and a lease liability. The new method thus increases the disclosure level and makes it easier to compare different entities.

New model for lessees

The lessee model involves the recognition of a right-of-use asset at cost and the measurement of a lease liability at the present value of the future lease payments. The right-of-use asset is normally charged to the income statement over the lease period, while the lease liability is accounted for using the effective interest method. Hence, the rent expense is substituted by the depreciation and the interest, thus, there is a change in the pattern of expense recognition in the financial statements.

Key principles at a glance

Ind AS 116 applies to contracts that transfer the right to control the use of an identified asset for a period of time in exchange for consideration. Entities need to assess:

• whether the contract contains an identified asset

• whether the customer obtains substantially all economic benefits from use of the asset

• whether the customer has the right to direct the use of the asset

The standard includes exceptions for short-term leases and low-value assets, allowing lessees to opt out of recognising these on the balance sheet.

Effective date and applicability

Ind AS 116 is effective for annual reporting periods beginning on or after 1 April 2019. Entities transitioning to the new standard may apply it either fully retrospectively or using a modified retrospective approach without restating comparatives. The standard applies to all entities required to follow Ind AS, subject to specific scope exclusions and optional exemptions.

What contracts come under Ind AS 116

Ind AS 116 applies to all leases, including subleases, that provide the right to control the use of an identified asset for a period of time in exchange for consideration. A contract contains a lease when it conveys the right to use an identified asset and the customer has the ability to obtain substantially all economic benefits from its use and the right to direct its use. The standard applies to both leases of tangible assets and right-of-use assets recognised by lessees. It covers arrangements that explicitly or implicitly specify an asset and provide the customer with control over the asset’s use during the lease term.

Scope exclusions

Ind AS 116 does not apply to certain types of arrangements even if they involve the use of assets. The following are specifically excluded from the scope of the standard:

• leases to explore for or use minerals, oil, natural gas, and similar non-regenerative resources

• leases of biological assets within the scope of Ind AS 41

• service concession arrangements within the scope of Appendix D to Ind AS 115

• licences of intellectual property granted by a lessor within the scope of Ind AS 115

• rights held by a lessee under licensing agreements such as motion picture films, video recordings, plays, manuscripts, patents, and copyrights

These exclusions ensure that industries with specialised accounting requirements follow their respective standards.

Optional exemptions for lessees

Ind AS 116 provides two optional recognition exemptions that lessees may elect to apply. These exemptions allow lessees to avoid recognising a right-of-use asset and lease liability for certain leases.

Short-term leases

A short-term lease is a lease that, at the commencement date, has a lease term of 12 months or less and does not include a purchase option. Lessees may elect, by class of underlying asset, not to apply the recognition and measurement requirements of Ind AS 116 to short-term leases. Instead, lease payments are recognised as an expense on a straight-line or other systematic basis over the lease term.

Low-value leases

Lessees may also elect not to apply Ind AS 116’s recognition and measurement principles to leases where the underlying asset is of low value when new. This exemption is applied on a lease-by-lease basis. Assets that typically qualify as low value include items such as small office equipment or telephones. The assessment of low value is independent of the lessee’s size or financial condition; it is based solely on the value of the underlying asset itself.

How to Identify a Lease under Ind AS 116

Definition of a lease

A contract contains a lease when it conveys the right to control the use of an identified asset for a period of time in exchange for consideration. To assess whether a contract contains a lease, an entity must determine whether the customer has the right to obtain substantially all the economic benefits from use of the asset and the right to direct the use of the asset throughout the period of use. This assessment is made at the inception of the contract.

Identified asset

A contract contains a lease only if it relates to an identified asset. An identified asset can be explicitly specified in the contract or implicitly specified at the time it is made available for use. An asset must be physically distinct or must represent substantially all of the capacity of the asset to be considered an identified asset. A portion of an asset that is physically distinct, such as a floor of a building, is an identified asset. A capacity portion that is not physically distinct, such as part of a fibre optic cable, is not an identified asset unless it represents substantially all of the asset’s capacity.

Substantive substitution rights

Even if an asset is specified, a customer does not have the right to use an identified asset if the supplier has substantive substitution rights throughout the period of use. Substitution rights are substantive only when the supplier has the practical ability to substitute the asset and would benefit economically from doing so. If substitution is only for repairs, maintenance, or malfunction, the right is not substantive. When substitution rights are not substantive, the asset remains an identified asset.

Right to control the use of an asset

To control the use of an identified asset, the customer must have the right to obtain substantially all of the economic benefits from using the asset and the right to direct how and for what purpose the asset is used. A customer directs the use when it can change how and for what purpose the asset is used throughout the period of use. If decisions about how and for what purpose the asset is used are predetermined, the customer still directs the use if it has the right to operate the asset without the supplier’s right to change those instructions, or if the customer designed the asset in a way that predetermines its use.

Decision tree explanation

The standard provides a decision framework to determine whether a contract contains a lease. The assessment proceeds as follows:

- Determine whether there is an identified asset.

- Assess whether the customer has the right to obtain substantially all economic benefits from the asset.

- Determine whether the customer has the right to direct the use of the asset.

If all three conditions are met, the contract contains a lease. If any condition fails, the contract does not contain a lease.

Lessee Accounting Under Ind AS 116

1. Initial Recognition

Under Ind AS 116, a lessee is required to recognise both a Right-of-Use (ROU) asset and a lease liability at the commencement of the lease.

Right-of-Use (ROU) Asset

The ROU asset is initially measured at cost, which includes:

- The initial measurement of the lease liability

- Lease payments made at or before the commencement date

- Initial direct costs incurred by the lessee

- Estimated costs of dismantling, restoring or removing the underlying asset

- Less any lease incentives received

The standard clearly states that the ROU asset is not measured at fair value; it is measured based on the lease liability plus adjustments.

Lease Liability

The lease liability is measured at the present value of lease payments that are not paid at the commencement date. These include:

- Fixed lease payments (including in-substance fixed payments)

- Variable payments linked to an index or rate

- Amounts expected to be payable under residual value guarantees

- Exercise price of purchase options (if reasonably certain)

- Termination penalties (if lease term reflects exercising termination option)

Discount Rate

Lease payments must be discounted using:

- Interest rate implicit in the lease, if readily determinable, or

- Lessee’s incremental borrowing rate, if the implicit rate cannot be determined.

This discounting model ensures that lease liabilities reflect the financing nature of leasing transactions.

2. Subsequent Measurement

Once initially recognised, lessee accounting under Ind AS 116 consists of two separate processes:

Depreciation of ROU Asset

The ROU asset is depreciated in accordance with Ind AS 16.

The depreciation period is:

- The useful life of the underlying asset, if ownership transfers or the lessee is reasonably certain to exercise a purchase option; or

- The lease term, in all other cases.

If the underlying asset belongs to a class for which the entity uses the revaluation model, Ind AS 116 allows a lessee to apply the same revaluation approach to ROU assets of that class.

Impairment of the ROU asset is assessed in accordance with Ind AS 36.

Interest Expense

The lease liability is measured using the effective interest method.

Each period, the lessee recognises:

- Interest expense, and

- A reduction in lease liability for lease payments made.

Remeasurement of Lease Liability

The lease liability must be remeasured when:

- There is a change in lease term

- There is a change in the assessment of purchase/termination options

- There is a change in amounts expected to be payable under residual value guarantees

- Future lease payments change due to index or rate adjustments

- In-substance fixed payments change

Revised lease payments are discounted using:

- A revised discount rate, when lease term or purchase option assessment changes

- The original discount rate, when only expected cash flows change (e.g., residual value guarantees, variable index-linked payments)

Corresponding adjustments are made to the ROU asset unless it has been reduced to zero.

3. Presentation and Disclosure

Balance Sheet

Lessees present:

- ROU assets either in a separate line item or within the same class of underlying assets (e.g., PPE)

- Lease liabilities separately from other liabilities

Short-term and low-value leases are not capitalised and therefore no ROU asset is recognised.

Statement of Profit and Loss

Lease-related expenses appear as:

- Depreciation expense (for the ROU asset)

- Finance cost (interest on lease liability)

- Lease rental expense for short-term and low-value leases

- Variable lease payments not included in the lease liability (disclosed separately)

This creates a front-loaded expense pattern, unlike straight-line operating lease rentals under Ind AS 17.

Statement of Cash Flows

Ind AS 116 prescribes the following classification:

- Financing activities: principal portion of lease payments and interest payments

- Operating activities: variable lease payments, short-term lease payments, low-value lease payments

- Non-cash disclosures: initial recognition of ROU asset and lease liability

Disclosure Requirements

Lessees must disclose qualitative and quantitative details to help users assess:

- Nature of leasing activities

- Future cash outflows not reflected in lease liabilities

- Exposure to variable lease payments

- Extension or termination options

- Residual value guarantees

- Leases not yet commenced

- Sale-and-leaseback arrangements

These disclosures provide a comprehensive view of the entity’s lease obligations and risks.

Lease Modifications

What Is a Lease Modification?

A lease modification is a change in the scope or consideration of a lease that was not part of the original terms and conditions. Under Ind AS 116, a modification occurs when the parties to a lease agree to alter elements such as the lease term, the leased space, or the lease payments.

Modifications may include:

- Adding or removing the right to use underlying assets

- Extending or shortening the lease term

- Increasing or decreasing lease payments

- Changing the consideration structure

A modification is accounted for from the effective date—the date on which the modification is agreed and becomes enforceable.

When Does a Modification Become a Separate Lease?

A lease modification is treated as a separate lease only when both of the following conditions are met:

- The modification increases the scope of the lease by adding the right to use one or more underlying assets, and

- The consideration increases by an amount commensurate with the stand-alone price for the added scope (with appropriate adjustments for contract-specific circumstances).

If both conditions are met, the modification is accounted for as a new, separate lease. In all other cases, the modification is accounted for by adjusting the existing lease.

Accounting Guidance for Lessees

For a modification that is not treated as a separate lease, Ind AS 116 requires the lessee to:

- Reallocate consideration in the modified contract,

- Determine the revised lease term, and

- Remeasure the lease liability using a revised discount rate at the modification date.

The revised lease liability is calculated using the updated payment schedule and the revised rate (either the implicit rate if readily available or the incremental borrowing rate).

Once the revised lease liability is determined:

- If the modification decreases the scope of the lease (e.g., reduction in leased area or shortened lease term), the lessee must:

- Reduce the carrying amount of the right-of-use (ROU) asset proportionately, and

- Recognise any gain or loss relating to the partial termination in profit or loss.

- For all other modifications, the lessee adjusts the ROU asset for the difference between the remeasured lease liability and the previous carrying amount.

Accounting Guidance for Lessors

Lessor accounting depends on whether the original lease is a finance lease or an operating lease:

Finance Lease

If the modification would have resulted in an operating lease had the new terms existed at the lease’s inception:

- The lessor accounts for the modification as a new lease from the effective date.

- The carrying amount of the underlying asset becomes the net investment in the original lease immediately before the modification.

Otherwise:

- The modification is accounted for under Ind AS 109 (Financial Instruments), because it represents a change in the financial asset (the net investment in the lease).

Operating Lease

For operating leases, modifications are accounted for as if they are new leases, with any prepaid or accrued rent recognized as part of the new lease’s accounting.

Conclusion

Ind AS 116 is probably the single biggest change to lease accounting in India over recent years. The standard has made a significant step forward in the openness and comparability of financial reporting by doing away with the concept of operating vs. finance lease for lessees and introducing a single, on-balance-sheet approach. Thus, the users of financial statements are in a better position to assess the contractual obligations of an entity, expected outflows of cash, and the economic effect of leases.

In short, Ind AS 116 is a step forward in the quality of financial reporting, as it commits to reflecting leasing arrangements more accurately on the balance sheet and in the performance metrics. Those companies which have a deep understanding of the standard and strong implementation of processes will become a source of reliable and relevant financial information to the users of their financial statements.

FAQs

1. How do you identify whether a contract contains a lease under Ind AS 116?

A contract contains a lease when it conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

You must assess:

• whether there is an identified asset

• whether the customer gets substantially all economic benefits

• whether the customer has the right to direct how and for what purpose the asset is used

If all three conditions are met, the contract contains a lease.

2. What counts as an identified asset?

An identified asset is one that is explicitly stated in the contract or implicitly understood to be used when the agreement begins. It must be physically distinct, such as a specific room or floor, or it must represent substantially all of the asset’s overall capacity. If the supplier can replace the asset freely and benefits economically from doing so, then the asset is not considered identified. In simpler terms, the customer must know exactly which asset they are receiving control over; otherwise, a lease does not exist.

3. What are substantive substitution rights?

Substantive substitution rights exist when a supplier can practically substitute the asset during its use and would benefit economically from the substitution.

If both conditions are met, the customer does not control the asset and the arrangement is not a lease. If substitution is allowed only for repairs or maintenance and not for economic benefit, then the rights are not substantive and the contract may still contain a lease.

4. How does Ind AS 116 treat capacity-based arrangements?

Capacity-based arrangements qualify as leases only when the customer controls a clearly identifiable and distinct portion of the asset. For example, if a customer receives exclusive use of specific rooms in a warehouse or a physically distinct section of a pipeline, then the arrangement may contain a lease. However, if the customer only receives a percentage of total capacity without exclusive control or without a physically distinct portion, such arrangements do not contain a lease. The key question is whether the portion being used is truly distinct or represents substantially all of the asset

5. What is a short-term lease under Ind AS 116?

A short-term lease is a lease with:

• a lease term of 12 months or less

• no purchase option

Lessees may elect not to recognise a right-of-use asset and lease liability for these leases and instead expense the lease payments over time.

6. Are service concession arrangements considered leases?

No. Service concession arrangements under Appendix D of Ind AS 115 are excluded from Ind AS 116.

In such arrangements, the grantor controls the infrastructure, so the operator does not have a lease.

7. What is a Right-of-Use (ROU) asset under Ind AS 116?

A ROU asset represents the lessee’s right to use the underlying asset during the lease term.

It is initially measured at cost, which includes:

• the initial lease liability

• payments made before commencement

• initial direct costs

• estimated restoration or dismantling costs

• minus any incentives received

The ROU asset is then depreciated and tested for impairment.

When was Ind AS 116 introduced?

Ind AS 116 became effective for annual reporting periods beginning on or after 1 April 2019.

On transition, entities could adopt it using:

• the full retrospective method, or

• the modified retrospective method without restating comparatives.