Key Takeaways

- The Composition Scheme under GST lets small businesses pay tax at a fixed rate (1% to 6%) on turnover instead of standard GST slabs, with quarterly payments and one annual return instead of monthly filings.

- Eligibility hinges on aggregate annual turnover calculated on a PAN-India basis: up to ₹1.5 crore for goods suppliers, ₹75 lakh for North-Eastern states and Himachal Pradesh, and ₹50 lakh for service providers or mixed suppliers.

- The biggest trade-off is losing Input Tax Credit (ITC). You pay GST on your purchases but cannot recover it, and your B2B customers cannot claim credit on your supplies either.

- Composition dealers are restricted to intra-state sales only. If your business plans to sell across state borders or through e-commerce platforms, this scheme is not an option.

- Before opting in, evaluate your customer base. If most buyers are GST-registered businesses, the lack of ITC on your invoices may push them toward other vendors.

- Staying compliant under the Composition Scheme still requires accurate transaction mapping and GST reconciliation. Tools like AI Accountant's GST reconciliation can automate this process, saving hours of manual matching every quarter.

Composition Scheme Under GST: What's New in 2026

The core structure of the Composition Scheme (turnover thresholds, tax rates, filing cadence) has remained largely unchanged heading into FY 2026-27. The turnover limits still stand at ₹1.5 crore for goods dealers and manufacturers, ₹75 lakh for special category states, and ₹50 lakh for service providers. However, the compliance environment around the scheme has tightened in ways that matter operationally.

Until March 2025, GST e-invoicing applied only to businesses with turnover above ₹5 crore. Starting April 2025, the threshold dropped significantly, pulling more SMEs into the digital compliance net. While composition dealers themselves remain exempt from e-invoicing, their regular-regime suppliers and buyers now generate more structured digital data. This means any mismatch between your purchase records and your supplier's e-invoices can trigger notices faster. Maintaining clean, reconciled books is no longer optional, even for small composition dealers.

The GST Network has also improved auto-population of data in GSTR-4 (the annual return for composition taxpayers). Purchase details from your suppliers' filings now flow into your return more accurately. The flip side: discrepancies between what your suppliers report and what you have recorded are easier for the department to spot. Businesses that still reconcile manually risk missing these gaps. Automated bookkeeping workflows can flag mismatches before the return due date, keeping you ahead of potential queries.

For existing composition taxpayers planning to continue in FY 2026-27, no fresh CMP-02 filing is needed. But if you are a regular taxpayer looking to switch, the deadline to file Form GST CMP-02 on the GST portal is March 31, 2026, followed by ITC-03 within 60 days. Missing either deadline locks you into the regular regime for the entire year.

What to do right now:

- Verify your aggregate turnover for FY 2025-26 is within the applicable limit before March 31.

- Reconcile all purchase data against supplier GSTR-1 filings to avoid auto-populated mismatches in your GSTR-4.

- If switching from the regular regime, file CMP-02 before March 31 and calendar the ITC-03 deadline (May 30, 2026).

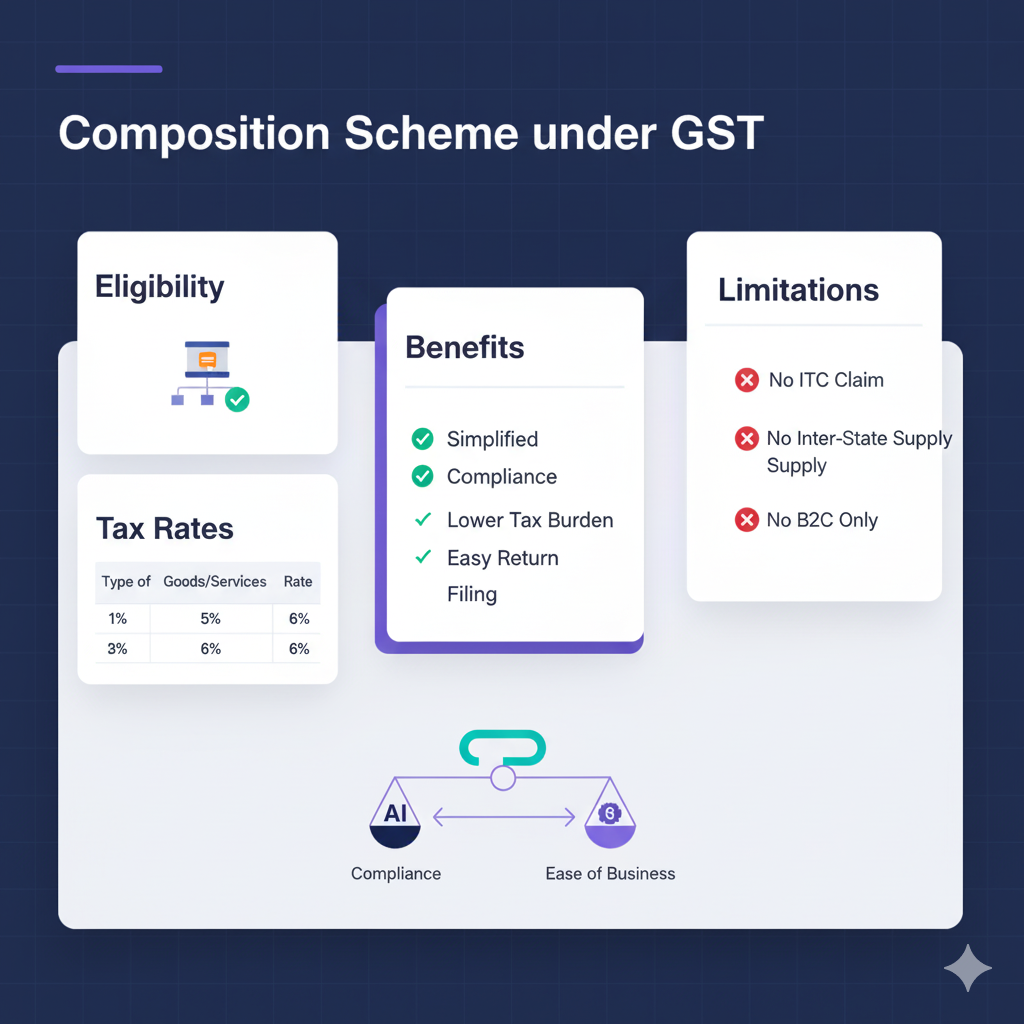

Eligibility Criteria for Composition Scheme under GST

The Composition Scheme under GST may be availed of only by small taxpayers that satisfy certain turnover and business criteria. It is intended to offer comfort to small enterprises by making the compliance process easier and lessening the tax burden.

Nevertheless, eligibility is determined by well-defined limits and requirements in Section 10 of the CGST Act, 2017, and the corresponding GST Rules.

1. Turnover Limits for Goods and Services

To opt into the scheme, the taxpayer's aggregate annual turnover in the preceding financial year must not exceed the prescribed limits:

Type of BusinessTurnover LimitApplicable GST Law ReferenceSuppliers of goods / manufacturers / tradersUp to ₹1.5 croreSection 10(1) of CGST ActSuppliers in North-Eastern States, Himachal Pradesh & UttarakhandUp to ₹75 lakhSection 10(1) ProvisoSuppliers of services or mixed suppliers (goods + services)Up to ₹50 lakhSection 10(2A) of CGST Act

Note: These limits are calculated on a PAN-India basis, not state-wise. That means if a business operates branches in multiple states, their combined turnover will determine eligibility.

2. Conditions for Eligibility

To qualify under the Composition Scheme, the business must also satisfy the following operational and compliance-based conditions:

- The taxpayer must deal only in intra-state supplies (no inter-state supply of goods or services).

- The taxpayer cannot supply non-taxable goods (e.g., petroleum, alcohol for human consumption).

- The taxpayer cannot supply goods through e-commerce operators required to collect TCS under Section 52 of the CGST Act.

- The taxpayer must not be a casual or non-resident taxable person.

- The taxpayer must display the words "Composition Taxable Person" on all signboards and documents.

- The taxpayer must issue a Bill of Supply, not a Tax Invoice, since GST cannot be charged from customers.

If any of these conditions are violated, the taxpayer becomes ineligible and must withdraw from the scheme immediately.

3. How to Calculate Aggregate Annual Turnover

The aggregate annual turnover (AATO) determines eligibility for the Composition Scheme and is computed on an all-India basis using the same Permanent Account Number (PAN).

AATO includes:

- Taxable supplies (sales on which GST is payable)

- Exempt supplies (zero-rated or nil-rated)

- Exports of goods or services

- Inter-state supplies made from all business locations using the same PAN

AATO excludes:

- Taxes and cess paid under GST (CGST, SGST, IGST, UTGST)

- Value of inward supplies liable to reverse charge

- Interest or discount earned from loans, deposits, or advances

Example:

If a Delhi trader has the following turnover in FY 2024-25:

- Taxable sales: ₹90 lakh

- Exempt sales: ₹5 lakh

- Export sales: ₹10 lakh

Then, Aggregate Annual Turnover = ₹90 lakh + ₹5 lakh + ₹10 lakh = ₹1.05 crore,

which is within the ₹1.5 crore limit — making the business eligible for the Composition Scheme in FY 2025-26.

A taxpayer can opt for the Composition Scheme only if the total turnover across India remains below the prescribed threshold, and all eligibility conditions are satisfied. Once the turnover crosses the limit or any condition is violated, the taxpayer must switch to the regular GST regime and comply accordingly.

Who Cannot Opt for the Composition Scheme under GST

While the Composition Scheme under GST offers simplified tax compliance and reduced rates for small businesses, not every taxpayer is allowed to opt in. The GST law clearly specifies certain categories of persons who are ineligible to register under the scheme.

This ensures that only small, local, and low-risk businesses benefit from the simplified tax system while keeping large or complex operations under the regular GST structure.

1. Casual Taxable Persons

A casual taxable person is someone who occasionally undertakes supplies in a State or Union Territory where they do not have a fixed place of business.

Example: A trader from Delhi participating in a trade fair in Maharashtra.

Since such persons are temporary suppliers with no fixed business base, they cannot opt for the Composition Scheme.

2. Non-Resident Taxable Persons

A non-resident taxable person (NRTP) is an individual or entity making supplies in India but without a fixed place of business or residence in India.

GST rules exclude NRTPs from the Composition Scheme since they operate on a short-term basis and are not considered small domestic taxpayers.

3. Businesses Engaged in Inter-State Supplies

A key restriction is that a Composition Dealer cannot make inter-state supplies of goods or services.

This means all sales and purchases must happen within the same state (intra-state). If a business makes or plans to make inter-state transactions, it must register under the regular GST scheme.

Example:

A textile wholesaler in Gujarat selling fabric to a retailer in Maharashtra cannot opt for the Composition Scheme.

4. Suppliers of Non-Taxable Goods

Businesses dealing in goods that are not taxable under GST are automatically excluded.

Common examples include:

- Petroleum crude

- High-speed diesel (HSD)

- Motor spirit (petrol)

- Natural gas

- Aviation turbine fuel (ATF)

- Alcoholic liquor for human consumption

Since GST does not apply to these products, suppliers of such goods are not eligible for the Composition Scheme.

5. Businesses Selling through E-Commerce Operators

Any business that sells goods or services through an e-commerce operator (ECO) required to collect Tax Collected at Source (TCS) under Section 52 of the CGST Act cannot opt for this scheme.

For example, sellers operating on Amazon, Flipkart, or Zomato are ineligible because these platforms collect GST at source.

6. Manufacturers of Notified Goods

The government has notified certain categories of manufacturers who are not eligible for the Composition Scheme under Section 10(2)(e) of the CGST Act.

These typically include manufacturers of:

- Ice cream and other edible ice

- Pan masala

- Tobacco and manufactured tobacco substitutes

These goods attract higher tax rates and are excluded to prevent misuse of the simplified scheme.

7. Input Service Distributors (ISDs) and Agents

Entities acting as Input Service Distributors or agents on behalf of another taxable person are not eligible.

They function primarily as intermediaries, not independent small businesses, and hence must follow the regular GST model.

8. Taxpayers Who Have Opted but Become Ineligible

Even after opting in, a taxpayer may lose eligibility for the scheme if:

- The aggregate turnover exceeds ₹1.5 crore or ₹50 lakh in a financial year.

- They start inter-state trade or export goods or services.

- They violate any conditions (e.g., issue a tax invoice instead of a Bill of Supply).

In such cases, the taxpayer must immediately withdraw from the scheme by filing FORM GST CMP-04, and begin paying tax under the regular GST regime.

The Composition Scheme under GST is designed to be used by small, local, and simple businesses only.

In case your business is doing inter-state trade, selling through e-commerce, or dealing in high-tax products, you must get a registration under the normal GST system.

It is a good practice to analyze your business model thoroughly before choosing to participate. An incorrect selection may lead to fines, interest, and revocation of tax benefits.

Registration and Intimation Process under the Composition Scheme

A taxpayer willing to take advantage of the Composition Scheme under GST has to go through the steps of registration and intimation by filing certain forms. Though the procedure is straightforward, it should be carried out only before the start of the financial year for which the taxpayer intends to avail the scheme.

By doing this, the taxpayer is accorded the status of a composition dealer and can commence the payment of tax at the predetermined fixed rate.

For New Taxpayers

When an individual is procuring GST registration for the very first time and intends to take the Composition Scheme, they are required to file an application through Form GST REG-01 on the GST portal. It is in Part B of the form where they should mark the choice of tax payment under the Composition Levy Scheme.

After the sanction of the registration, the Composition Scheme shall be in effect from the very date of registration.

For Existing Registered Taxpayers

A taxpayer under the normal GST regime willing to change to the Composition Scheme has to electronically submit the application in Form GST CMP-02 on the GST common portal before the beginning of the financial year.

Along with the filing of CMP-02, the taxpayer should within 60 days from the financial year commencement file Form GST ITC-03. This form is for declaring and reversing any Input Tax Credit (ITC) on the stock, semi-finished, and finished goods in possession on the date of transition.

It is very significant to point out that the Composition Scheme is not available if one is in the middle of a financial year. The option is only valid when it is exercised prior to the start of the financial year.

Timeline and Renewal Rules

Form CMP-02 must be filed before the beginning of the financial year, usually by March 31. Form ITC-03 must be filed within 60 days from the commencement of the new financial year.

Once opted, there is no need to reapply every year. The scheme remains valid as long as the taxpayer continues to meet all eligibility conditions, such as turnover limits and intra-state supply requirements.

If the taxpayer's turnover exceeds the limit or any eligibility condition is violated, they must withdraw from the scheme by filing Form GST CMP-04.

Key GST Forms for Composition Scheme

Here is a quick reference of the forms involved in the composition scheme registration and withdrawal process:

- GST CMP-01: Tax payment notification for provisional registrations

- GST CMP-02: Opt for the Composition Scheme (filed before the financial year)

- GST CMP-03: Details of stock and inward supplies on the date of opting in

- GST CMP-04: Withdraw from the Composition Scheme

- GST ITC-01: Claim ITC on stock held when exiting the scheme

- GST ITC-03: Reverse ITC on stock held when entering the scheme

Validity and Effective Date of the Scheme

The effective date of the Composition Scheme depends on whether the taxpayer is newly registered or already registered under GST.

- For a new registrant, the scheme becomes effective from the date of registration approval, as per Form GST REG-01.

- For an existing taxpayer, the scheme becomes effective from the first day of the financial year in which Form GST CMP-02 is filed.

Once the scheme becomes effective, the taxpayer is treated as a Composition Dealer from that date onward and must comply with specific requirements. They must issue a Bill of Supply instead of a Tax Invoice and mention the phrase "Composition Taxable Person – not eligible to collect tax on supplies" on all such bills.

The taxpayer must also display the words "Composition Taxable Person" at all their business premises.

Withdrawal from the Composition Scheme

A taxpayer may need to withdraw from the Composition Scheme if they no longer meet eligibility criteria or if they wish to shift to the regular GST regime.

In such cases, the taxpayer must file Form GST CMP-04 before the intended date of withdrawal. They must also submit Form GST ITC-01 within 30 days to claim Input Tax Credit on stock, semi-finished, and finished goods held on the date of withdrawal.

From that point onward, the taxpayer will issue tax invoices and comply with normal GST filing requirements, such as monthly or quarterly returns.

Tax Rates under the Composition Scheme

The Composition Scheme under GST provides a fixed and simplified rate of tax that varies depending on the nature of the business. Instead of paying tax at regular GST slab rates of 5%, 12%, 18%, or 28%, composition taxpayers pay a nominal percentage of their turnover.

The rates are prescribed under Section 10 of the CGST Act, 2017, and corresponding state GST provisions. These rates have been effective since April 1, 2019.

Composition Scheme GST Rate Table

- Manufacturers of Goods

Eligible manufacturers are required to pay tax at the rate of 1% of their turnover in the state or union territory. This includes 0.5% CGST and 0.5% SGST. - Traders or Dealers

Traders engaged in the supply of goods are also liable to pay 1% of their taxable turnover. This is split equally between CGST and SGST at 0.5% each. - Restaurant Service Providers

Businesses providing restaurant services that do not serve alcohol are taxed at 5% of their turnover. This rate consists of 2.5% CGST and 2.5% SGST. The rate is applicable only to restaurants not eligible for input tax credit. - Service Providers and Mixed Suppliers

The GST law was later amended to extend the Composition Scheme to small service providers and mixed suppliers (those dealing in both goods and services). Such entities can opt to pay tax at 6% of their turnover (3% CGST and 3% SGST), provided their aggregate annual turnover does not exceed ₹50 lakh in the preceding financial year.

Why Composition Scheme May Not Be Ideal For You

The Composition Scheme under GST is often seen as a small business "miracle": simple, predictable, and without a lot of trouble. However, while it certainly facilitates compliance, the scheme is not altogether without its trade-offs.

It blocks businesses from several areas that may directly affect their competitiveness, potential to grow, and profit margins. It is still a good idea to know what you might be giving up in exchange for the simplicity.

No Access to Input Tax Credit

The most limiting feature of the Composition Scheme is the prohibition of Input Tax Credit (ITC). In other words, the GST you paid on business purchases (raw materials, equipment, or services) is not refundable.

What this really means is that your business costs increase because you are in effect paying the same tax twice: once on your purchases and the other when you pay your composition levy.

Besides, your customers are also not allowed to claim ITC on your supplies. This may make your goods or services less attractive to GST-registered buyers who prefer vendors offering input credits, especially if your business is B2B.

Restricted to Local Sales Only

One of the most significant restrictions is that composition dealers are limited to making intra-state sales only. They are not allowed to sell goods or provide services across state boundaries, nor can they export.

It might not be an issue for a small shop or a service provider that is solely focused on local customers. However, for any business that has the intention of growing or taking orders from other states, this limitation can become a barrier very quickly.

Once a dealer engages in inter-state trade, they have to exit the Composition Scheme and switch to the regular GST regime.

No Tax Invoice or GST Collection

You are not permitted to issue a tax invoice or collect GST from customers if you are operating under this scheme. What you have to do instead is provide a Bill of Supply indicating clearly "Composition Taxable Person – not eligible to collect tax on supplies".

While this may seem easy, it has its implications. Since you are not allowed to collect GST, you have to bear this cost out of your own pocket. Regardless of the fact that the rate is low, it still has a negative effect on your margins.

For trading businesses in price-sensitive markets, this can pose a challenge in competing with normal taxpayers who can recover their input tax through ITC.

Limited Room for Growth

The Composition Scheme is built around the idea of small taxpayers, and the advantages it offers are tied to your turnover. If your annual sales go beyond ₹1.5 crore (for goods) or ₹50 lakh (for services), you are required to move to the regular GST regime.

This implies new filing requirements, record keeping, and system upgrades, all at the halfway point.

If you are running a business that is growing rapidly, this changeover might be quite inconvenient. You may need to revise your invoice format, upgrade your accounting package, and notify your customers about the new tax changes. In many cases, the switch feels as tough as starting fresh.

Lower Credibility in B2B Markets

One more real limitation is perception. Since composition dealers are not allowed to collect GST, their invoices do not provide any input tax benefit to the buyers. Hence, big distributors, wholesalers, or corporate clients refrain from buying from them.

If the majority of your customers are other registered businesses, it might limit your potential client base. The Composition Scheme tends to be suitable for business-to-consumer (B2C) traders and service providers who sell directly to end customers.

Conclusion

The Composition Scheme delivers on its promise of simplicity: fewer returns, reduced rates, and less paperwork. Nevertheless, the simplicity comes with clear trade-offs.

It is an appropriate solution for small, locally focused businesses that are looking for a straightforward way to comply with GST without getting into complex tax procedures.

On the other hand, if you plan to expand beyond your state, serve B2B clients, or scale your business, the regular GST structure might be more beneficial in the long run. The main thing is to assess your business's future before deciding.

FAQ on the Composition Scheme under GST

1. Can I switch from the regular GST scheme to the Composition Scheme in the middle of a financial year?

No, a mid-year switch is not allowed. You can only opt for the Composition Scheme at the start of a new financial year by filing Form GST CMP-02 before March 31 on the GST portal.

2. Do I need to notify the GST department every year to stay in the Composition Scheme?

No, the scheme continues automatically each year once you have opted in, as long as you meet all eligibility conditions. A fresh notification is only needed if you had previously withdrawn and want to re-enter the scheme.

3. What happens if my turnover exceeds the prescribed limit during the year?

You must immediately switch to the regular GST regime by filing Form GST CMP-04. From the date your turnover crosses ₹1.5 crore (for goods) or ₹50 lakh (for services), you will need to start issuing tax invoices and filing regular returns.

4. Can a composition dealer purchase goods or services from another state?

Yes, a composition dealer can buy goods or receive services from other states. The restriction applies only to sales; you cannot make inter-state sales. Any GST due on reverse charge for such purchases must still be paid separately at regular GST rates, not at the composition rate.

5. How are reverse charge transactions handled under the Composition Scheme?

Composition taxpayers must pay GST on reverse charge supplies (such as notified goods or services from unregistered dealers) at the applicable regular GST rate, not the composition rate. This payment is made through the normal tax payment process on the GST portal.

6. What kind of invoice does a composition dealer issue to customers?

A composition dealer issues a Bill of Supply, not a tax invoice. This bill must clearly state: "Composition Taxable Person – not eligible to collect tax on supplies." No GST amount should be shown separately on the bill.

7. Can a composition dealer voluntarily exit the scheme?

Yes. A taxpayer can voluntarily withdraw by filing Form GST CMP-04. After exiting, they must file Form GST ITC-01 within 30 days to claim Input Tax Credit on stock held on the date of withdrawal. From that date onward, they operate under the regular GST regime with full ITC eligibility.