-01%201.svg)

Key takeaways

- GSTR 9 is the annual return summarizing your entire year’s GST data, mandatory when aggregate turnover exceeds Rs 2 crore.

- The usual due date is December 31 following the financial year, late fees are Rs 200 per day with a cap at 0.25% of state turnover.

- GSTR 9C applies when turnover exceeds Rs 5 crore, it reconciles GST returns with audited financials and needs CA or CMA certification.

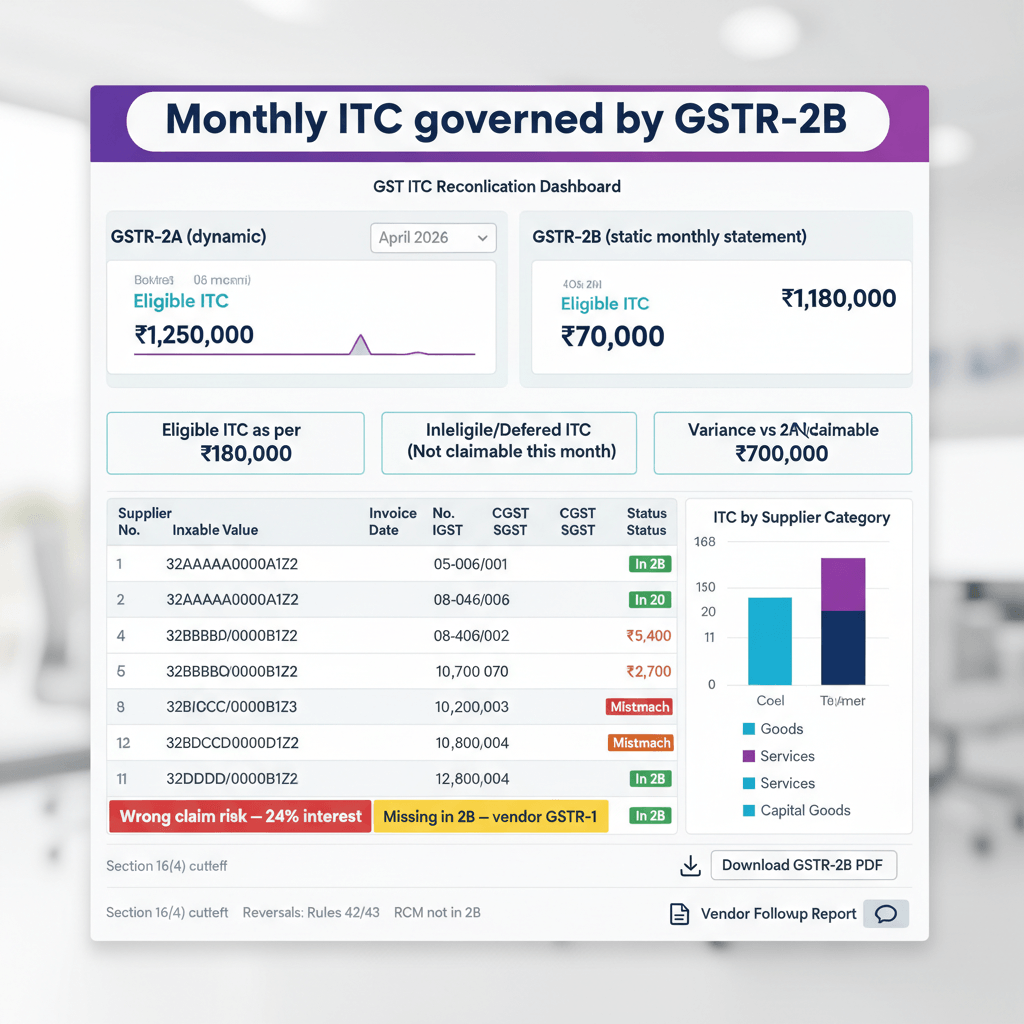

- Accurate reconciliation with books, GSTR 1, GSTR 3B, and GSTR 2A or 2B is critical to avoid notices and interest.

- Prepare early, verify ITC eligibility, include exempt and non-GST supplies, and document differences thoroughly.

- Small businesses benefit from simple reconciliations, disciplined record keeping, and affordable professional support.

- Late fees, interest, and penalties can be minimized with proactive reviews, smart use of tools, and timely filing.

- Services like Virtual Accounting by AI Accountant streamline year-round GST hygiene, reducing year-end stress.

What is GSTR 9 and Who Needs to File It

GSTR 9 is the consolidated annual GST return that captures your full year’s GST footprint. It pulls together details from your monthly GSTR 1 and GSTR 3B filings, presenting a single, comprehensive view of outward supplies, inward supplies, input tax credit, and tax payments.

You must file GSTR 9 if your annual aggregate turnover exceeds Rs 2 crore. This applies to regular taxpayers, SEZ units, and SEZ developers. Turnover includes taxable supplies, exempt and nil-rated supplies, non-GST supplies, and exports. If you transitioned to composition during the year, you still file for the regular taxpayer period.

You do not file GSTR 9 if you are a composition dealer, an Input Service Distributor, a casual taxable person, or a non-resident taxpayer. If your turnover is below Rs 2 crore, filing is optional.

Think of GSTR 9 as your business’s GST report card, a chance to reconcile the year, fix errors, and present a clean, confident compliance story.

Understanding the GSTR 9 Due Date and Timeline

The due date is typically December 31 after the end of the financial year. For FY 2023-24, that means December 31, 2024. Extensions happen, but never plan on them. Map your work to the original deadline.

Late filing attracts Rs 100 per day under CGST and Rs 100 per day under SGST or UTGST, capped at 0.25% of turnover. The practical timeline: financial year ends March 31, you have nine months to reconcile, close your books, and prepare to file. If you miss the final cut-off, usually two years from the due date, the portal may disable filing for that period.

GSTR 9 vs GSTR 9C: Key Differences

- GSTR 9: Annual return summarizing your GST year, applicable when turnover exceeds Rs 2 crore.

- GSTR 9C: Reconciliation statement certified by a CA or CMA, applicable when turnover exceeds Rs 5 crore, matches GSTR data with audited financials.

- Order and timing: File GSTR 9 first, some data auto-populates into GSTR 9C, both share the same filing deadline.

- Cost and rigor: GSTR 9C involves professional certification and deeper scrutiny, therefore higher effort and fees.

Businesses that use Virtual Accounting by AI Accountant typically have both handled within their subscription, reducing last minute pressure.

Documents Required for GSTR 9 Filing

- All monthly GSTR 1 and GSTR 3B returns for the year.

- audited financial statements, especially Profit and Loss and Balance Sheet.

- Sales and purchase registers, including exempt and non-GST supplies.

- Bank statements for all business accounts to verify tax payments and ITC utilization.

- Stock reconciliation, fixed asset register, and capitalization schedules.

- Registers for credit and debit notes, plus a log of amendments and their tax impact.

- HSN-wise summary of sales and purchases for quick cross checks.

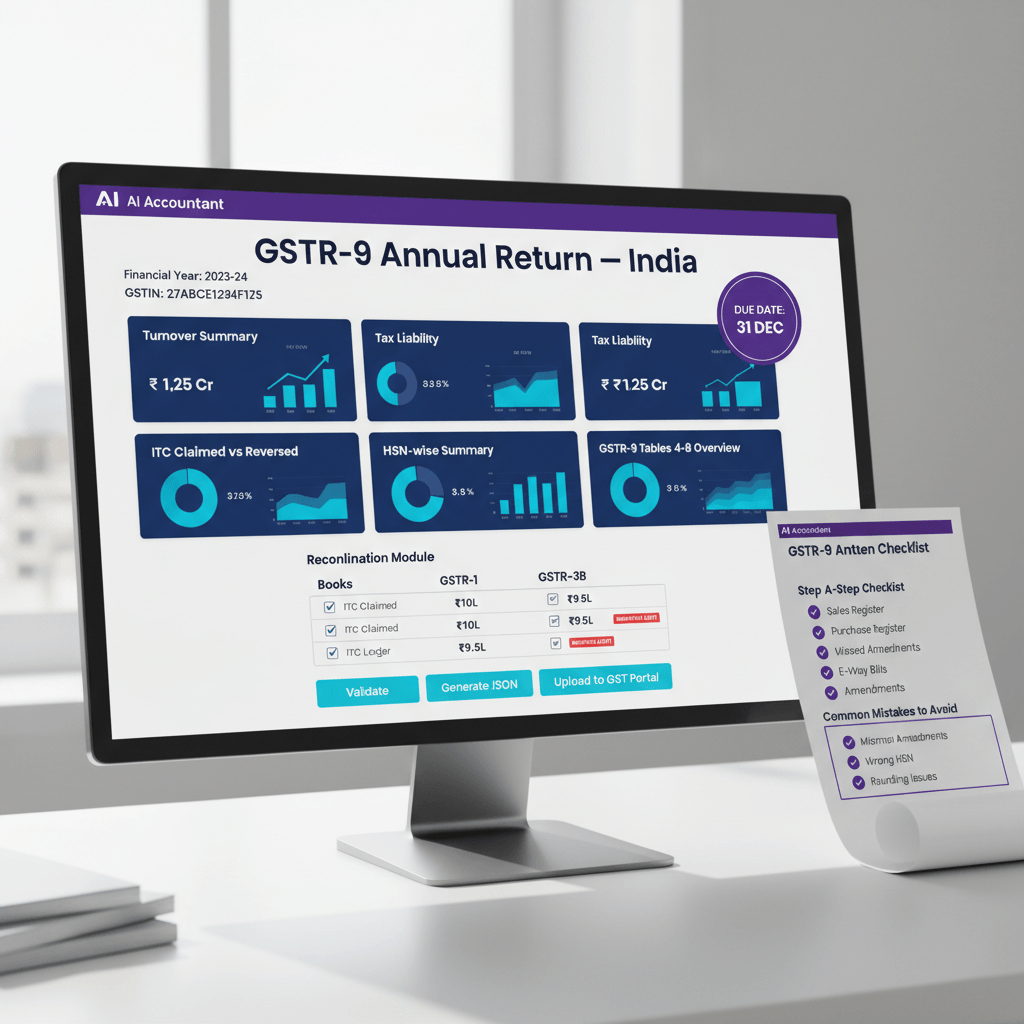

Step by Step GSTR 9 Filing Process

1) Access and basic verification

Login to the GST portal, go to Returns Dashboard, choose Annual Return, select the financial year, and click Prepare Online. Confirm legal name, trade name, and GSTIN. Update your registration first if basic details are incorrect.

2) Part II, outward supplies

Review Table 4 data auto-populated from GSTR 1. Reconfirm taxable supplies, zero rated supplies, and adjustments for advances or unbilled revenue. Use supporting registers to validate amounts.

3) Part III, inward supplies and ITC

Verify ITC claimed, reversals, and ineligible credits. Ensure Rule 42 and Rule 43 computations are correctly reflected. Do not carry forward ineligible credits, document every reversal rationale.

4) Part IV, tax paid

Cross check tax payable and tax already paid through GSTR 3B. Any difference becomes additional liability or potential refund. Prepare to make payment if a shortfall appears.

5) Part V, reconciliation

Reconcile with your books, and explain differences clearly. This section reduces post-filing notices by addressing variances upfront.

6) Review, validate, submit

Use preview, run offline validations if using the tool, and lock in numbers only after a final review. Download the acknowledgment immediately after successful filing.

Common Mistakes to Avoid in GST Annual Returns

- Treating GSTR 9 as routine: It is your best chance to correct the year’s errors with minimal friction.

- Mismatched turnover with audited books: Disclose and reconcile differences, especially non-GST and exempt supplies.

- Ignoring exempt or non-GST supplies: Report them in Table 5 to avoid red flags.

- Incorrect ITC reversals: Recompute Rule 42 and Rule 43 carefully, support with working papers.

- No reconciliation with GSTR 2A or 2B: Investigate vendor-level mismatches, document reasons, and adjust where required.

- Overlooking amendments: Credit or debit notes that alter prior months need careful annual treatment.

- Skipping year-end accounting impacts: Provisions, accruals, and deferrals can change liability or ITC positions.

Pro tip: Maintain a running “variance log” all year. By year-end, you will have a ready checklist of issues to resolve before filing.

GST Annual Return for Small Businesses

If your turnover is between Rs 2 crore and Rs 5 crore, GSTR 9 applies, GSTR 9C usually does not. Start early, ideally in April or May, while details are fresh and vendors are reachable.

- Maintain a simple monthly tracker for GSTR 1, GSTR 3B, ITC, and tax payments.

- If numbers are not your strength, get affordable professional assistance.

- For composition taxpayers, GSTR 4 is the relevant annual return, simpler but without ITC benefits.

- If you barely cross Rs 2 crore, expect possible scrutiny, keep meticulous proofs.

SMBs using Virtual Accounting by AI Accountant get proactive reconciliations during the year, making annual filing almost procedural.

How to Handle Late Fees and Penalties

- Late fees: Rs 100 per day under CGST and Rs 100 per day under SGST or UTGST, capped at 0.25% of turnover. The portal auto-computes the amount.

- Interest: Applies if additional liability emerges, calculated from the original monthly due dates, not from the annual return due date.

- Penalties for persistent non-compliance: Can go up to Rs 25,000, separate from late fees and interest.

- Possible waivers: Government may provide relief through notifications, do not assume it will happen.

- Payment sequencing: Clear late fees and tax dues in the cash ledger before final submission.

In rare cases, if an extension seems likely, delaying might save late fees, but this is speculative and risky.

GST Portal Navigation for Annual Returns

- Go to Services, Returns, Annual Returns to check eligibility for GSTR 9 and GSTR 9C.

- Download the year’s GSTR 1, GSTR 3B, and GSTR 2A data packs before you begin, keep them open for real-time cross checks.

- Consider the offline utility for high volumes, prepare and validate JSON, then upload.

- Use Save Draft frequently, the portal may time out without warning.

- After submission, verify status under Return Filing Status, do not rely solely on email or SMS alerts.

Technology and Tools for Easier GSTR 9 Filing

- GST software: Automates compilation and flags common inconsistencies.

- Excel templates: A well-structured workbook with monthly sheets for sales, purchases, ITC, and payments can be highly effective.

- Reconciliation tools: Match books with GSTR 2A or 2B to spot missing or mismatched invoices quickly.

- API integrations: Sync billing, accounting, and GST returns to reduce manual errors.

- Dashboards: Real-time compliance visibility, like those used in Virtual Accounting by AI Accountant, highlight issues months in advance.

- Document management: Tag and store invoices and working papers for rapid retrieval during reviews.

- Validation checks: Run pre-submission validations to remove negative values where not allowed and fill mandatory fields.

Professional Help vs DIY Approach

DIY works when your transactions are simple, books are clean, and you understand GST well. Expect 20 to 40 hours of focused work, spread across data gathering, reconciliation, and validations.

Professional help is recommended for multiple registrations, interstate and export transactions, job work, complex ITC positions, or prior-year notices. The cost often pays for itself by avoiding penalties, interest, and business disruption.

Virtual Accounting by AI Accountant offers a middle path, combining software automation, expert review, and year-round hygiene, so annual returns become a smooth wrap-up instead of a scramble.

Final Preparations Before GST Annual Return Submission

- Complete a books to GST reconciliation, document every variance and its rationale.

- Check vendor compliance, follow up with key suppliers who have not filed or reported.

- Arrange funds for any additional liability, top up your cash ledger in advance.

- Create a digital repository of support, organized by GSTR 9 table numbers.

- Test DSCs and authorizations early, especially if GSTR 9C applies.

- Schedule uninterrupted filing time, the portal can be slow near deadlines.

One last look with a tax professional, even for DIY filers, can catch small mistakes that cost big later.

Conclusion

GSTR 9 filing becomes simple when you prepare steadily, reconcile diligently, and use the right tools. Treat it as an annual health check, not a hurdle. Start early, keep records tidy, and get help when complexity rises. Whether you file yourself or rely on expert support like Virtual Accounting by AI Accountant, clarity and consistency are your best allies.

Master the process once, refine it each year, and you will turn annual returns into a confident routine.

FAQ

Do I really need to file GSTR 9 if I already filed all monthly returns correctly?

Yes, if your aggregate turnover exceeds Rs 2 crore, GSTR 9 is mandatory. It consolidates your year, validates monthly data against books, and helps you disclose differences. Even perfect monthly compliance needs an annual wrap-up.

What is the practical checklist I should follow to avoid last minute chaos?

Prepare a year-end pack: GSTR 1 summaries, GSTR 3B summaries, GSTR 2A or 2B reconciliation, sales and purchase registers, ITC workings including reversals, credit and debit note logs, and audited financials if applicable. Teams using Virtual Accounting by AI Accountant typically have this ready by default.

We crossed Rs 2 crore for the first time, what should we watch out for?

Validate turnover calculation including exempt and non-GST supplies, confirm registration details, and reconcile ITC carefully. Keep clear notes on variances. Borderline cases can see more questions from officers, so documentation quality matters.

When does GSTR 9C apply and who can certify it?

GSTR 9C applies when turnover exceeds Rs 5 crore. A Chartered Accountant or Cost Accountant must certify it, reconciling GST data with audited financial statements. File GSTR 9 first, then GSTR 9C.

How do I handle vendors who have not uploaded invoices, but I took ITC?

Reconcile with GSTR 2A or 2B to identify gaps. Follow up with non-compliant vendors, maintain evidence of follow-ups, and evaluate whether to reverse or retain ITC based on eligibility and documentation. Document decisions thoroughly to defend your position during assessments.

Can I revise GSTR 9 if I spot an error after filing?

The portal may allow a limited revision window, often one revision. Accuracy on first submission is still critical. If an error persists after revision, prepare to explain and adjust via subsequent compliance mechanisms on advice from your tax professional.

We are a startup with simple domestic sales, should we DIY or hire a CA?

If your books are clean, transactions are straightforward, and you understand GST basics, DIY with a professional review can work. If you prefer predictability, Virtual Accounting by AI Accountant gives you expert oversight and automation, spreading effort across the year.

What are the most expensive mistakes founders make with GSTR 9?

Ignoring exempt and non-GST supplies, miscomputing ITC reversals, missing interest on historical shortfalls, and filing late. Each of these can lead to cumulative penalties and time-consuming notices. A pre-filing reconciliation and variance memo prevents most issues.

How can I speed up reconciliation without expensive software?

Use a disciplined Excel workbook: monthly sheets for sales, purchases, ITC, and taxes paid, with pivot tables to match HSN and tax rates. Combine this with GSTR 2A or 2B downloads for a simple invoice match. If you outgrow spreadsheets, consider an automated solution bundled with services like Virtual Accounting by AI Accountant.

Do I still file GSTR 9 for a dormant year with no activity?

If your turnover exceeds Rs 2 crore, yes, even if operational activity was minimal. You will report nil or minimal figures, but the compliance event still exists. Keep banking and ledger proofs to support low activity claims.

What documents should I keep ready in case of a departmental query after filing?

Sales and purchase registers, bank statements, ITC workings including Rule 42 and Rule 43 computations, credit and debit note registers, GSTR 1 and GSTR 3B copies, GSTR 2A or 2B reconciliation, and audited financials if applicable. A cloud folder mapped to GSTR 9 table numbers makes responses swift.

How do late fees and interest actually play out in real life cash flow?

Late fees are payable upfront before filing, so they hit immediately. Interest accrues on additional tax liabilities identified during annual reconciliation, often dating back to original monthly due dates, so it can be material. Budget for both if you suspect gaps.

What operational habits ensure a stress-free GSTR 9 next year?

Monthly reconciliations, vendor compliance tracking, timely ITC eligibility reviews, and a rolling variance log. Teams using Virtual Accounting by AI Accountant typically maintain these rhythms, turning the annual return into a quick confirmation rather than a forensic project.