Key takeaways

- Late filing and payment quickly snowball into interest at 18% per annum, late fees up to ₹5,000 per return, and potential audits.

- Wrong ITC claims, missing e-invoices, and e-way bill lapses invite steep penalties, cash flow stress, and vendor friction.

- Section 73 applies to non-fraud cases with 10% penalty or ₹10,000 minimum, Section 74 applies to fraud with penalties up to 100% of tax.

- Persistent mismatches in GSTR-2B, unusual ITC ratios, and high refunds are common audit triggers.

- Fast, factual responses to notices prevent escalation, voluntary correction can reduce penalties.

- A monthly reconciliation rhythm, disciplined documentation, and professional oversight are your best defense.

- Virtual Accounting by AI Accountant centralizes books, GST, and notices, reducing risk and saving founder time.

What Counts as GST Non-Compliance?

Non-compliance is more than missing a deadline. It includes failure to register when eligible, late or non-filing of GSTR-1, GSTR-3B, GSTR-9, or GSTR-9C, delayed tax payment, and documentation gaps like missing e-invoices or expired e-way bills. Errors in place of supply, incorrect HSN codes, and use of blocked credits also qualify.

- Returns: delayed or non-filing of periodic and annual returns.

- Payments: unpaid or partially paid tax, interest, and late fees.

- ITC: mismatches with GSTR-2B, ineligible or excess credit, use of blocked credits.

- Registration: not registering despite crossing the threshold, wrong category, or composition breaches.

- Documentation: missing e-invoices when applicable, expired or incorrect e-way bills, poor record keeping.

For statutory specifics, see penalties for non-compliance under GST and penalties for GST non-compliance in 2026.

The Real Cost: Penalties, Interest, and Hidden Impacts

The headline fines are only part of the story. The deeper cost comes from interest, cash flow strain, vendor relations, and management time lost to firefighting.

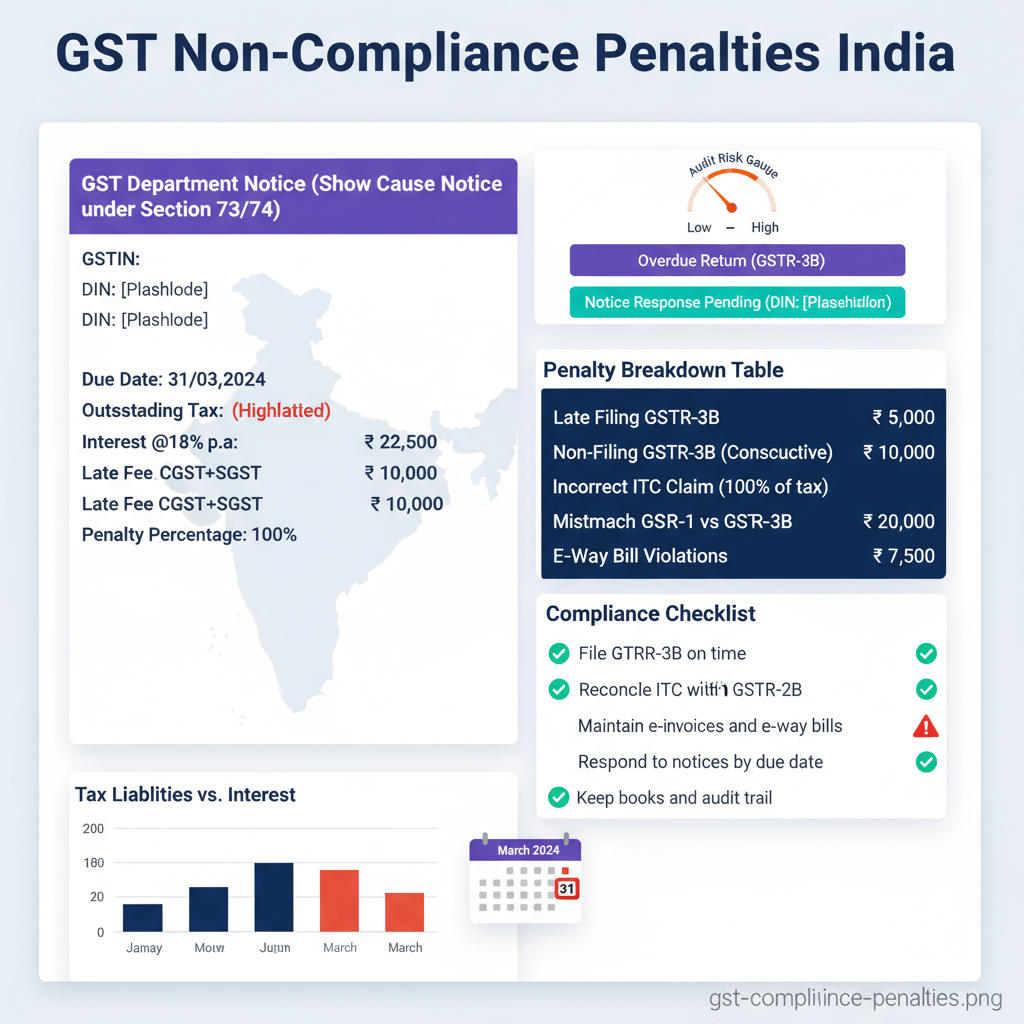

- Monetary costs: late fees at ₹50 per day for regular taxpayers, ₹20 per day for NIL returns, interest at 18% per annum on unpaid tax, and penalties under Section 73 or 74 depending on intent.

- Operational disruptions: time spent replying to notices, preparing for audits, and managing reconciliations. Audit preparations drain resources and focus.

- Strategic setbacks: blocked ITC, vendor blacklisting due to mismatches, eligibility issues for tenders, and reduced lender or investor confidence.

- Severe consequences: registration cancellation for prolonged non-filing, detention or seizure on e-way lapses, prosecution in large fraud cases, and exposure for directors.

Reference guides: penalties for non-compliance under GST, penalties for GST non-compliance in 2026, GSTR changes and late fee updates, 2026 compliance checkup, and penalty for e-way bill violations in India.

Penalty Breakdown by Scenario

- Late filing: GSTR-3B and GSTR-1 attract ₹50 per day, capped at ₹5,000, ₹20 per day for NIL returns, plus 18% interest on tax due.

- Delayed payment interest: 18% per annum, 24% in cases of undue or excess ITC claims.

- Non-registration when liable: 10% of tax or ₹10,000 minimum for non-fraud, 100% of tax for fraud, interest applies from due date.

- Wrong ITC claims: reversal of credit, interest, and up to 100% penalty if fraud is established.

- E-invoice non-compliance: up to ₹25,000 per invoice or tax involved for applicable taxpayers.

- E-way bill lapses: ₹10,000 or tax amount, whichever is higher, with detention or seizure risks.

- Composition scheme breaches: exit from scheme, pay differential tax with interest and penalties.

- Section 73 vs Section 74: Section 73 for non-fraud, 10% or ₹10,000, Section 74 for fraud, up to 100% of tax involved.

Deep dives: penalties for non-compliance under GST and penalties for GST non-compliance in 2026.

GST Audit Risk in India: Triggers and How to Reduce It

Data analytics across e-invoices, GSTRs, and e-way bills lets authorities flag anomalies rapidly. Common triggers include persistent GSTR-2B mismatches, negative cash ledger signals, high refunds relative to turnover, unusual ITC ratios, missing e-invoices, missing e-way bills, and sudden spikes in turnover.

Risk reduction playbook

- Run monthly GSTR-2B reconciliations, not year end firefights.

- Implement invoice verification and ITC approval workflows with maker checker controls.

- Maintain clean, indexed records for all invoices, IRNs, e-way bills, and challans.

- Self audit quarterly, document findings, and fix issues immediately.

Helpful overview: penalties for GST non-compliance in 2026.

GST Notice in India for SMEs: Types and Response Steps

Notices are stressful, yet manageable with a prompt, evidence backed response.

Common notice types

- ASMT-10 for mismatches.

- DRC-01 Show Cause Notice.

- DRC-07 final demand order.

- ADT-01 audit initiation.

- Section 70 summons for appearance.

Seven step response checklist

- Identify the notice type, record the deadline, breathe.

- Assemble GSTRs, invoices, payment challans, ledgers, and ITC proofs.

- Reconcile the stated mismatch with your records, quantify differences.

- Draft a factual, respectful reply with annexures.

- File the reply on the GST portal, retain acknowledgments.

- Attend hearings with your CA, carry indexed documentation sets.

- On adverse orders, evaluate payment under protest or file appeal.

Sample: “With reference to DRC-01 Notice Number [XXX] dated [date], we respectfully submit our clarification. The identified mismatch of ₹[amount] arose due to [specific reason]. Supporting documents including GSTR-2B reconciliation and relevant invoices are attached. We request that the proposed demand be dropped.”

Guides and templates: penalties for non-compliance under GST and penalties for GST non-compliance in 2026.

Quick Scenarios with Rupee Math

Scenario 1: Retail store late filing

Monthly tax of ₹1,00,000, GSTR-3B filed 45 days late. Late fee, 45 × ₹50 = ₹2,250. Interest, ₹1,00,000 × 18% × 45/365 ≈ ₹2,200. Total ≈ ₹4,450.

Scenario 2: Startup misses e-invoices

B2B startup skips e-invoices for 10 transactions at ₹50,000 each. Penalty can be ₹25,000 per invoice, tax is ₹9,000 per invoice at 18%. Penalties alone, ₹2,50,000, plus interest on delayed tax. Cost crosses ₹2.5 lakh quickly.

Scenario 3: Logistics e-way lapse

₹2,00,000 shipment is intercepted with an expired e-way bill. Immediate penalty is ₹10,000 or tax amount, whichever is higher. Detention and release can require 100% to 200% of tax value, with week long disruption.

Read more: penalties for non-compliance under GST, penalties for GST non-compliance in 2026, and penalty for e-way bill violations in India.

Prevention Checklist Founders Actually Use

Monthly essentials

- Reconcile GSTR-2B to books, follow up with vendors for missing invoices.

- Review ITC eligibility, remove blocked credits.

- Check cash ledger, plan payment amounts and dates.

Calendar control

- Mark GSTR-1, GSTR-3B, and annual return dates, use a robust planner. See year end accounting checklist India.

- Track e-invoice thresholds and HSN updates, align product changes.

Process and evidence

- Standardize e-way bill generation and invoice verification workflows.

- Maintain indexed folders for invoices, IRNs, e-way bills, reconciliations, and challans.

- Run a quarterly internal GST self audit, document fixes and responsibilities.

For evolving rules and practical tips, see penalties for GST non-compliance in 2026.

How Virtual Accounting Prevents GST Headaches

Founders juggle growth and compliance, one slip can be costly. Professional support converts chaos into a predictable rhythm.

- Virtual Accounting by AI Accountant offers end to end compliance with dedicated CA teams, AI powered alerts, and real time dashboards. They manage books clean up, GST, TDS, and payroll in a single workflow with transparent pricing from ₹4,000 per month.

- Traditional CA firms provide depth and relationship, yet often lack automation and real time visibility.

- Online filing platforms provide DIY tools, time and accuracy still rest on you.

- In house teams bring control, salary, tooling, and training can exceed outsourcing.

- Freelancers can be economical, bandwidth during peak filings is a frequent constraint.

Automation driven GSTR-2B reconciliation, live filing calendars, and daily bank syncs reduce errors. When notices arrive, the CA team drafts replies and attends hearings. Annual GSTR-9 becomes a systematic exercise rather than a scramble. Pricing remains clear, ₹4,000 monthly up to 200 transactions, ₹6,000 for higher volumes, with add ons for annual returns and special cases.

Take Action Before It Is Too Late

The true cost of non-compliance is not just money, it is stress, distraction, and lost opportunity. With a practical checklist, disciplined reconciliations, and expert support, GST becomes routine. Act today, because prevention costs less than penalties, and confidence feels better than uncertainty.

FAQ

What are the GST non-compliance consequences in India for a typical SME?

Expect late fees, interest at 18% on delays, and penalties ranging from 10% to 100% of tax depending on intent. Persistent lapses invite audits and possible registration cancellation after continued non-filing. For context, review penalties for non-compliance under GST and penalties for GST non-compliance in 2026. Many SMEs mitigate this risk by using Virtual Accounting by AI Accountant.

What is the penalty for late filing of GSTR-3B or GSTR-1?

₹50 per day up to ₹5,000 per return for non-NIL, ₹20 per day for NIL, plus 18% annual interest on tax due. See official penalty references and 2026 penalty overview.

How high is GST audit risk in India and what usually triggers it?

Risk increases with large GSTR-2B mismatches, unusually high ITC compared to turnover, negative cash ledgers, missing e-invoices or e-way bills, and sudden turnover spikes. Regular reconciliations, clean documentation, and quick corrections keep you off the radar. See audit and penalty insights.

I received a GST notice, what should I do first as a founder?

Confirm the notice type and deadline, assemble GSTRs, invoices, and challans, reconcile the stated differences, and submit a factual reply with annexures on the GST portal. Templates and penalty structures are outlined in GST penalty references and latest penalty guidance. For hands on help, consider Virtual Accounting by AI Accountant.

Is interest always 18 percent, when does 24 percent apply?

Standard interest is 18% on delayed tax payments. A 24% rate applies in cases of undue or excess ITC where credit was availed incorrectly. See interest and penalty provisions.

Can penalties be reduced or waived, are there amnesty options?

Voluntary disclosure and timely payment before a notice often reduce penalties. Governments occasionally introduce amnesty windows to clear backlogs. For specific thresholds and timelines, track current penalty policy. A managed service like Virtual Accounting by AI Accountant can flag and resolve issues early.

We made a wrong ITC claim, how should we fix it fast and limit fallout?

Reverse the ineligible ITC immediately, pay interest, and document the correction with reconciliations. If you act before a notice, penalties are usually lighter. Refer to ITC penalty norms. To prevent repeats, automate 2B reconciliations via Virtual Accounting by AI Accountant.

What documentation should I keep ready to survive a GST audit?

Invoice trails with IRNs, e-way bills, ledgers, reconciliations for GSTR-1, 3B, and 2B, payment challans, vendor communications, and SOPs that demonstrate controls. Strong audit readiness reduces penalties and cycle time. See audit preparation checklist.

How do e-invoice or e-way bill lapses affect small businesses in practice?

Missed e-invoices can attract penalties per invoice and block customer ITC, while e-way lapses risk detention, penalties at ₹10,000 or tax amount, and shipment delays. Learn more from e-way bill penalty guidance. Automated workflows in Virtual Accounting by AI Accountant minimize such failures.

What is a practical monthly GST routine for a resource constrained startup?

Weekly invoice verification, monthly GSTR-2B reconciliation, calendarized filings, and a rolling vendor follow up list for missing documents. Use a shared repository for invoices, IRNs, e-way bills, and reconciliations. For a ready made cadence, follow year end accounting checklist India and consider outsourcing to Virtual Accounting by AI Accountant.

How do Section 73 and Section 74 actually play out during assessments?

Section 73 applies without fraud, penalties are lighter at 10% or ₹10,000, while Section 74 involves fraud, penalties can reach 100% of tax, and prosecution exposure increases. Early cooperation, accurate documentation, and prompt payment improve outcomes. See section wise penalties.

What is the fastest way to clean up backlogs if we missed multiple returns?

Prioritize periods with the highest tax exposure, file pending GSTR-1 and 3B sequentially, compute and pay interest, and document reasons for delay. If internal bandwidth is limited, onboard Virtual Accounting by AI Accountant for a 24 hour kick off and rapid clean up using books clean up services.

Will non-compliance affect loans or investor due diligence?

Yes, lenders and investors view GST discipline as a governance proxy. Repeated mismatches, notices, or penalties can delay or reduce funding. A clear compliance track record, reconciliations on file, and professional oversight signal reliability. Align practices with 2026 compliance checkups for stronger diligence outcomes.

.png)