-01%201.svg)

Key takeaways

- A GST-compliant company expense policy in India requires five pillars: tiered category limits, an amount-based approval matrix, restricted categories, strict receipt standards with GSTIN validation, and risk-based audit controls.

- Businesses that enforce receipt completeness and GSTR-2B reconciliation at submission recover 15–20% more eligible ITC annually, turning expense policy into a profit lever.

- Tiered daily limits by city classification and seniority prevent overspending while keeping policies practical for employees in metros versus non-metro locations.

- A three-layer approval workflow with defined SLAs (24 hours to 5 days) and escalation rules eliminates bottlenecks and keeps reimbursement cycles under seven days.

- Risk-based audit sampling (5–30% by category) catches violations early without creating administrative overload for finance teams.

- Manual GSTIN checks, receipt chasing, and GSTR-2B matching are the exact repetitive tasks that AI Accountant's GST reconciliation automates, freeing CA firms and finance teams to focus on judgment calls.

Company Expense Policy India: What's New in 2026

Until March 2025, the e-invoicing mandate applied to businesses with turnover above ₹5 crore. From April 2025, the threshold dropped to ₹1 crore as per CBIC notifications, pulling a significantly larger pool of SME vendors into the e-invoicing net. For expense policies, this means more of your vendor invoices now carry IRN and QR codes that must be verified before ITC is claimed.

The operational shift is tangible. Finance teams now need to validate IRN on invoices even from smaller vendors (hotels, local transport aggregators, office supply dealers) that previously issued simple tax invoices. If your expense submission workflow does not check for IRN on invoices from vendors above the ₹1 crore threshold, you risk accepting non-compliant documents and losing ITC.

Who does this hit hardest? Mid-sized companies and CA firms managing multiple client entities. Their vendor pools include hundreds of suppliers who crossed the ₹1 crore mark for the first time in FY 2024-25. Each entity needs updated vendor master data and submission checks. Firms still relying on manual receipt review face a steep volume increase.

The cost of inaction: ITC blocked on invoices missing valid IRN, penalties under Section 122 of the CGST Act (up to ₹25,000 per instance for non-compliance), and reconciliation mismatches in GSTR-2B that trigger notices. Interest at 18% per annum applies on wrongly claimed ITC that gets reversed.

What to do now:

- Update your vendor master to flag all suppliers above ₹1 crore turnover and require e-invoice verification on their submissions.

- Add IRN and QR code validation as a mandatory pre-approval check in your expense workflow.

- Run a one-time reconciliation of Q4 FY25 invoices against the updated e-invoicing list to catch gaps before your next GST return filing.

Platforms built for Indian compliance, like AI Accountant's vendor bill matching, already validate IRN, cross-check GSTIN status, and flag non-compliant invoices before they enter your books, making this transition seamless rather than painful.

What is an Expense Policy in the Indian Context?

A company expense policy India is your organization's rulebook for employee spending and reimbursements. It defines what is allowable, how much can be spent, and how claims get processed. In India, this framework must embed GST requirements, ITC eligibility rules, and strict documentation standards. Without these, reimbursements turn into compliance risks.

Beyond generic rules, Indian businesses must validate GSTIN, capture place of supply, reconcile against GSTR-2B, and manage TDS where applicable. For context on statutory obligations around reimbursement, the GST portal provides circulars on the taxability of employee reimbursements under the pure agent concept.

A digital expense policy India needs to address varies from city tier cost differences to vendor documentation realities across states. The goal: control spending, streamline reimbursements, and ensure compliance.

Foundational Components of an Indian Expense Policy

Focus on five pillars: category limits, approval matrix, restricted categories, receipt standards, and audit controls. Ground these in Indian compliance requirements and your actual spend data.

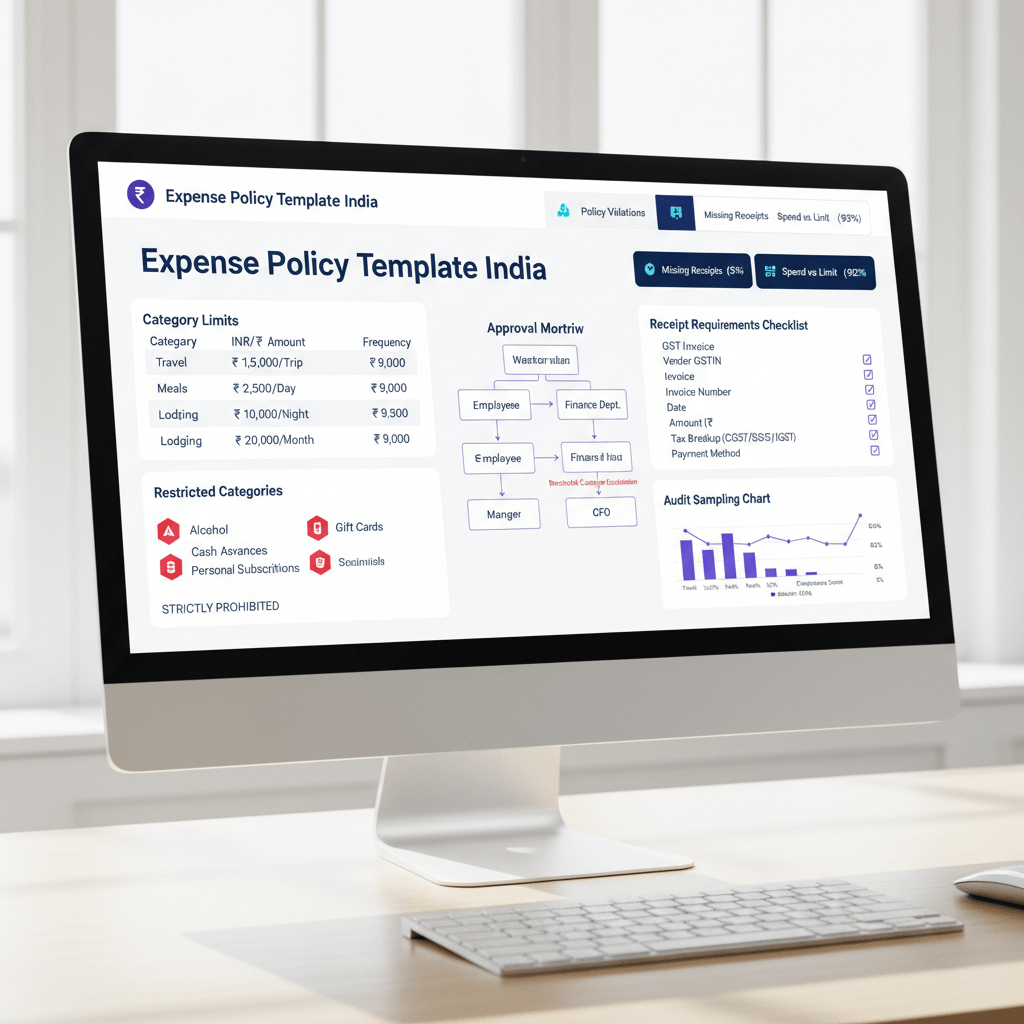

Setting Smart Category Limits

Create tiered limits by city classification, employee seniority, and trip purpose. Analyze the last six months of spending, then set practical caps for travel, lodging, meals, local conveyance, telecom, and supplies.

Domestic Travel Daily Limits (INR):

Expense CategoryMetro JuniorMetro SeniorNon-Metro JuniorNon-Metro SeniorMeals1,5002,5001,0002,000Hotel/Lodging5,0008,0003,0005,000Local Transport1,0001,5007501,000Communication500750500750Miscellaneous5001,000500750

Set quarterly reviews to adjust for inflation and market rates. Require pre-approvals for any planned exceedance. Distinguish client-billable from internal travel. These distinctions matter for employee expense management that stays GST compliant.

Building Your Approval Matrix

Route approvals by amount thresholds. Keep it simple. Set SLAs with escalation. A well-designed matrix prevents bottlenecks while maintaining control.

Standard Approval Matrix:

Expense Amount (INR)First ApproverSecond ApproverFinal ApproverTurnaround TimeBelow 5,000Direct Manager--24 hours5,000 to 25,000Direct ManagerFinance Team-48 hours25,000 to 50,000Direct ManagerFinance HeadDepartment Head72 hoursAbove 50,000Direct ManagerFinance HeadDirector/CEO5 days

Define separate tracks for pre-approvals, emergency exceptions, and delegation during absence. Enforce SLAs with automated reminders. Mobile approvals keep flow steady even when approvers travel.

Defining Restricted Categories

List non-reimbursable items clearly: personal purchases, non-business entertainment, unauthorized travel upgrades, penalties or fines, and any invoices lacking GST essentials. Non-compliant vendors or incorrect place of supply invalidate ITC claims.

- Entertainment and Alcohol: limit alcohol to 10% of the total bill unless pre-approved.

- Travel Upgrades: economy under 4 hours, business beyond with director approval.

- Fuel and Vehicles: maintain mileage logs with purpose and route details.

- Communication: reimburse business usage only, recover personal usage on company plans.

- Penalties and Fines: never reimbursable even during work travel.

Receipt Requirements and Documentation Standards

For ITC eligibility, receipts must include specific fields as mandated under Section 31 of the CGST Act. Missing any of these means your Input Tax Credit claim is at risk.

Essential Receipt Checklist:

- Supplier legal name and GSTIN (15-digit format).

- Unique invoice number and date (no duplicates).

- HSN or SAC codes, item description, quantity and unit.

- Taxable value, CGST or SGST for intra-state, IGST for inter-state.

- Total invoice value and place of supply (crucial for GST).

- Business purpose added by employee (concise and verifiable).

Allow digital submission within seven days. Define small vendor exceptions under ₹500 with self-declaration. Verify IRN and QR code for e-invoices above ₹50,000. Enforce missing-receipt protocols consistently. A company expense policy with Tally integration should map these fields directly to ledger entries during ingestion.

Implementing Audit Sampling and Controls

Adopt risk-based sampling to focus on high-risk areas, then scale with automation.

Risk-Based Audit Framework:

- High Risk (30% sampling): missing receipts, restricted categories, limit exceedance, new employees, previously flagged individuals.

- Medium Risk (15% sampling): travel and accommodation, client entertainment, vendor payments without PO, rush reimbursements.

- Low Risk (5% sampling): office supplies, standard telecom bills, public transport with receipts, pre-approved expenses.

Run monthly audits for early detection. Complement with quarterly deep dives for pattern analysis. Emphasize education for first-time violations, then escalate if behavior persists.

India-Specific Compliance and Best Practices

GST Compliance and ITC Optimization

Validate vendor GSTIN at onboarding. Reconcile expense invoices with GSTR-2B monthly. Ensure place of supply and tax type accuracy on every claim. As per GST Council recommendations, ITC can only be claimed when the supplier has filed their return and the invoice reflects in your GSTR-2B.

Document mixed-use allocations carefully. Choose between per diem and actuals based on your workforce profile. Maintain robust evidence for ITC claims. The most common cause of ITC denial in expense audits remains missing or incorrect place of supply and invalid GSTIN.

Communication and Training Strategies

Publish the latest policy with version control. Share quick reference guides for travel booking, expense submission, and receipts. Build FAQs from real employee questions.

Add practical training during onboarding. Send quarterly reminders with examples of compliant versus non-compliant submissions. Organizations that train quarterly report compliance rates jumping from approximately 70% to above 90%.

Implementation Roadmap for Indian Businesses

Phase 1: Analysis and Design (Weeks 1-2)

Analyze six months of data. Identify violation patterns and ITC losses. Map reporting structures. Benchmark against peers to calibrate limits and workflows.

Phase 2: Policy Development (Weeks 3-4)

Draft limits. Design the approval matrix. Define restricted categories. Document receipt requirements with checklists. Finalize audit schedules and consequences.

Phase 3: System Configuration (Weeks 5-6)

Configure accounting and expense tools. Set approval workflows. Map categories to GST codes and ITC eligibility. Build dashboards. Cleanse vendor master data with GSTIN validation. If you use Tally, ensure your expense tool integrates natively for seamless ledger posting.

Phase 4: Pilot and Refinement (Weeks 7-8)

Pilot with diverse teams. Gather feedback. Adjust limits and approvals. Test audits and tracking. Refine documentation standards based on real submissions.

Phase 5: Full Launch (Week 9 onwards)

Announce launch. Provide comprehensive training. Monitor closely. Track compliance and cycle times. Schedule monthly reviews for the first quarter, then quarterly thereafter.

Technology and Automation Tools

Choosing the Right Expense Management Software

Prioritize GST-aware automation: GSTIN validation, invoice completeness checks, ITC eligibility computation, and GSTR-2B reconciliation. Verify integration with accounting systems (especially Tally) and travel platforms.

- AI Accountant: Indian-first automation for bulk bill ingestion, GSTIN validation, ITC checks, and GSTR-2B matching, with Tally integration. ISO 27001 and SOC 2 Type II certified.

- Zoho Expense: strong suite integration, some GST support.

- SAP Concur: enterprise-grade features, larger investments required.

- Expensify: friendly UX, configure for Indian GST needs.

- Fyle: real-time tracking and card reconciliation for startups.

- Happay: India-focused prepaid cards and policy enforcement.

How AI Accountant Supports Your Expense Policy

AI Accountant enforces receipt standards via intelligent extraction of GST fields. It flags GSTIN mismatches instantly, reconciles invoice data with GSTR-2B, and maps expenses to predefined categories and limits automatically.

Payment linking prevents duplicate claims. Multi-org support simplifies CA firm operations. Real-time dashboards surface violations, aging reimbursements, and audit trends for proactive control.

Metrics to Track Policy Effectiveness

Key Performance Indicators

Track compliance and efficiency holistically, then act on insights.

- Compliance Rate: target 95% or higher.

- Missing Receipt Rate: keep below 5%.

- Spend versus Limits: monitor frequency and context.

- Restricted Category Violations: measure and train.

- Approval SLA Adherence: aim above 90%.

- Reimbursement Cycle Time: under seven days end-to-end.

- Audit Finding Trends: track types, amounts, and repeat offenders.

- ITC Eligibility Rate: maintain high qualification rates with clean documentation.

Continuous Improvement Framework

Hold quarterly reviews with stakeholders. Run annual employee surveys on clarity and fairness. Benchmark against industry periodically.

Update with regulatory changes. Pilot adjustments before scaling. Document lessons learned from violations for institutional memory. As per ICAI guidance, internal financial controls should be reviewed annually at minimum.

Common Pitfalls and How to Avoid Them

Overcomplicating the Policy Structure

Overly complex policies reduce compliance. Keep categories to 5-8 manageable groups. Simplify approval layers to three tiers maximum. Automate forms and routing. Write in plain language that any employee can understand on first read.

Inadequate GST Documentation

Vague requirements lead to ITC losses. Codify required invoice fields explicitly. Train employees on eligibility rules. Validate GSTIN proactively at vendor onboarding. Add pre-submission checks that reject incomplete invoices before they enter the approval queue.

Ignoring Audit Requirements

Audits are not optional. Stratify risk. Integrate findings into dashboards. Follow through consistently. Scale reviews with automation rather than adding headcount.

Poor Vendor Master Management

Untidy vendor masters cause GSTR-2B mismatches and ITC denials. Automate GSTIN validation at onboarding. Schedule quarterly vendor reviews. Categorize vendors by expense type. Document approval processes for adding new vendors.

As per CBIC circulars, ITC is blocked if the supplier's registration is cancelled or suspended at the time of invoice issuance. Regular vendor master hygiene catches these issues before they become ITC reversals.

Final Takeaways and Next Steps

Effective expense policy India frameworks combine control, clarity, and compliance with practical execution. Start with clear limits, a simple approval matrix, restricted categories, strict receipt standards, and risk-based audits. Then layer in GST specifics and ITC optimization.

Technology multiplies impact. AI Accountant automates validations, reconciliations, and enforcement. Keep reviews frequent, training practical, and communication open.

Track metrics rigorously. Align the policy to business goals. Iterate quarterly. Begin today: analyze current spending, draft limits, define your approval matrix, publish receipt checklists, run a pilot, then scale. Good policies that launch and improve beat perfect policies that never ship.

Frequently Asked Questions

How should a CA design category limits for a fast-scaling startup without overpaying?

Set conservative initial caps anchored to six months of data, then review monthly during growth. Tie increases to revenue or headcount milestones, add city tier variations, and pre-approve exceptions rather than raising blanket limits.

What receipt fields are mandatory for ITC, and how do I enforce them across multiple client orgs?

Six fields are mandatory: GSTIN, invoice number and date, HSN or SAC, taxable value, tax split (CGST/SGST or IGST), and place of supply. Create submission checklists per org, train employees during onboarding, and deploy document extraction with field validation that rejects incomplete invoices at submission.

How do I reconcile employee expenses with GSTR-2B and prevent ITC mismatches?

Match expense invoices to supplier GSTR-1 via GSTR-2B monthly, not quarterly. Investigate mismatches immediately and hold ITC claims until resolved. Automated reconciliation reduces manual effort by up to 75% and catches discrepancies within days rather than at filing deadlines (2026 update).

How does a company expense policy with Tally integration actually work?

The expense tool maps approved claims to Tally ledger codes, posts entries automatically, and tags each transaction with GST details (HSN, tax type, place of supply). This eliminates manual data entry, reduces posting errors, and keeps your books audit-ready in real time (2026 update).

What makes an expense policy GST compliant versus just having limits?

GST compliance means every reimbursable invoice carries valid GSTIN, correct place of supply, proper tax split, and HSN/SAC codes, not just that the amount is within budget. A policy is GST compliant when it enforces documentation standards that preserve ITC eligibility, validates vendor registration status, and reconciles claims against GSTR-2B before filing.

How do I handle emergency spends that bypass standard workflow, and still stay audit-ready?

Define emergency approvers with capped authority (typically up to ₹25,000), require post-facto justification within 48 hours, and log all exceptions with reason and outcome. Review exception frequency per employee and department monthly, then coach or escalate as patterns emerge.

How often should policy limits be revised given inflation and city tier changes?

Review limits quarterly against CPI data and internal spend patterns by city. Annual revisions are insufficient given India's inflation variability across metro and non-metro locations. Communicate changes with versioned policy updates and apply effective dates to avoid confusion.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.