Key takeaways

- Remote bookkeeping services give startups and SMBs expert record keeping without in office staff, using secure cloud tools and clear workflows.

- Virtual accounting services add CA led compliance and advisory, you get execution plus insight with a single dashboard and defined SLAs.

- Cloud based, automated, and outsourced bookkeeping models can be combined, the right mix depends on volume, complexity, and compliance needs.

- Financial reporting automation shortens month end close, improves accuracy, and delivers real time dashboards for founders and investors.

- Strong India compliance, GST, TDS, ROC, and robust controls like maker checker and audit trails, are non negotiable for scale and audits.

- AI Accountant offers a CA led, dashboard driven service that blends remote bookkeeping and virtual accounting for end to end delivery.

Introduction to remote bookkeeping services

Remote bookkeeping services give you expert record keeping without in office staff. Your books are handled online through secure cloud tools, your cash flow stays clean, errors reduce, and penalties are avoided. In this guide, we compare remote bookkeeping services with virtual accounting services, cloud based bookkeeping services, automated bookkeeping services, and outsourced bookkeeping solutions. We also cover financial reporting automation and how to set things up the right way in India.

We wrote this as a friendly playbook for founders, finance leads, and freelancers. If you want a CA led team with a single dashboard to run your accounting and compliance, AI Accountant can help. Learn more at https://aiaccountant.com. For a deeper look at the virtual model, see this guide.

Further reading: Universal Accounting School, Nexus HR, Integrity Electrical, Bookstime

What are remote bookkeeping services

Remote bookkeeping services mean trained professionals maintain your financial records from anywhere using secure online platforms, you do not need an in house bookkeeper, and your data sits in the cloud. Your team and your provider collaborate through shared tools, so month end moves with fewer emails and fewer surprises.

Core deliverables usually include

- Accounts receivable and accounts payable processing

- Bank and payment gateway reconciliations

- Month end ledger close and review

- Fixed asset tracking and depreciation

- Basic compliance support like GST reconciliation preparation

Many providers also prepare management reports each month. You get a profit and loss, a balance sheet, cash flow trends, and notes on exceptions. With the right setup, you can view reports anytime in a dashboard.

Compared to an in house hire, remote bookkeeping services can reduce overheads by a large margin. You avoid salary bands, benefits, office space, and software maintenance, while providers give you always on access to your data.

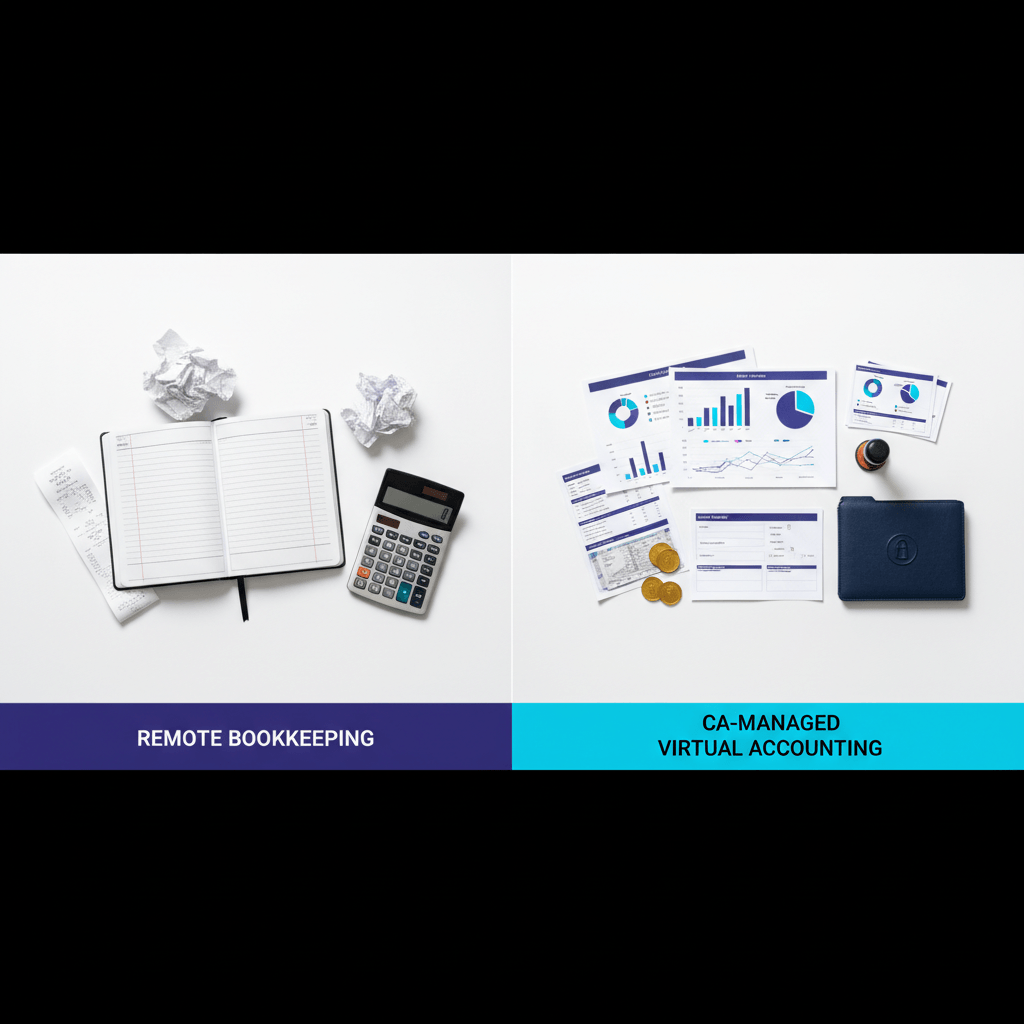

How it differs from virtual accounting

Remote bookkeeping focuses on accurate recording and reconciliations. Virtual accounting adds full compliance execution, advisory, and planning under a CA led model. See the virtual model overview at AI Accountant.

Further reading: Bookkeeper Law, Brex Accounting Trends

Virtual accounting services compared

Virtual accounting services go beyond entries. Think of it as a CA led managed accounting and compliance service with a dashboard for live visibility. You get bookkeeping and also GST and TDS filings, income tax returns, and advisory on cash flow and runway. The team sets maker checker reviews and helps you prepare for audits. Integrations with Indian tools like Tally or Zoho Books keep data in sync.

This model works well for startups and growing companies that need more than data entry. You get structured workflows instead of scattered threads, plus help with complex items like e invoicing, revenue recognition, and multi entity GST tracking. In short, execution plus insight.

Further reading: AccountingDepartment.com, Brex

Cloud based bookkeeping services explained

Cloud based bookkeeping services use online ledgers like QuickBooks Online or Xero, bank feeds pull in transactions each day, and mobile apps capture receipts via OCR. Stakeholders can view the same file at the same time, backups run in the background, and the month end close becomes faster and more transparent.

Pros

- Anytime access and real time updates

- Rich app ecosystem for AP, AR, payroll, and analytics

- Shared visibility for founders, finance teams, and auditors

Cons

- Subscription fees to manage

- A learning curve for teams new to cloud accounting

For many small businesses, the benefits outweigh the costs because the books stay tidy and visible. Explore a broader cloud guide at AI Accountant.

Automated bookkeeping services for simple workflows

Automated bookkeeping services rely on rules and robotic process automation, bank feeds tag common vendors, OCR scans bills and fills fields, and AP and AR workflows route approvals. Over time, the system reduces manual entry and speeds up the close.

Automation shines when your volume is high but patterns are stable, it can cut manual data entry by a large share. Still, humans must handle exceptions. Foreign currency transactions, unusual one off items, or GST input tax credit adjustments often need review by a person. For simple setups like a freelancer, automation can cover most needs with a light human touch.

Further reading: Nexus HR, Bookkeeper Law

Outsourced bookkeeping solutions for scale

Outsourced bookkeeping solutions give you a team instead of a single contractor, the provider commits to service levels and scheduled reporting, and you often see weekly updates and monthly reviews. Many teams work from nearshore or offshore locations to lower costs.

Compared to solo contractors, outsourced teams have clearer process maps, segregation of duties, and backups if someone is on leave. Time zones can create delays, so plan for scheduled check ins. When set up well, this model delivers strong accuracy and predictable timelines at a lower cost than in house.

Further reading: Integrity Electrical, Bookstime

Core processes you should expect from a remote provider

When you sign up, your provider should run a steady monthly cadence. Here is what a strong delivery cycle looks like.

- Transaction posting for sales, purchases, expenses, and payroll

- Bank and payment gateway reconciliations against ledgers

- GST portal checks and reconciliations

- Ledger clean up and suspense resolution

- Fixed asset and inventory adjustments with schedules

- Accounts receivable follow ups and accounts payable aging

- MIS reports with profit and loss, balance sheet, and cash flow

- Close checklist and variance notes

On compliance, a capable provider prepares data for GST monthly or quarterly, calculates TDS challans and returns, estimates advance tax, and for small companies, prepares data sets for ROC submissions. Financial reporting automation amplifies this cadence, templates and rules compress close time from half a month to about one week, with alerts for missing invoices or odd spikes in spend.

Further reading: Universal Accounting School, Brex

Financial reporting automation for faster closes

Financial reporting automation joins your bank feeds, ledgers, and workflows into one reporting engine. It can produce profit and loss statements, balance sheets, cash flow statements, and variance analysis on a set schedule. You also get trend lines on burn rate and runway for planning, with live dashboards for founders and investors.

Benefits include

- Faster close cycles through templates and auto roll forwards

- Fewer manual touches and fewer errors

- Real time dashboards for founders and investors

- Alerts on anomalies like large swings in COGS or revenue

For busy teams, this means faster decisions, cleaner reviews, and ready made packs for boards. Read more at AI Accountant.

Further reading: Bookkeeper Law, Brex

Tools and tech stack for remote and cloud based bookkeeping

A solid tech stack keeps your books current and your data safe. When you assess vendors, ask how these parts fit together.

Core ledger and bookkeeping

- AI Accountant

- QuickBooks Online

- Xero

- Zoho Books

- Tally Prime

- FreshBooks

- Sage Accounting

Payments and gateways

- Razorpay

- PayU

- Stripe

AP and AR workflows and OCR

- Clear for AP, AR, and GST

- Nanonets for OCR

- Zoho Expense

Work management and communication

- Asana

- Slack

- Zoom

Security and controls to look for

- Data encryption at rest and in transit

- Multi factor authentication

- Role based access with maker checker flows

- Audit trails and access logs

- India data residency where applicable and alignment with RBI guidance

When these parts connect through APIs, your bank data flows in daily, your bills scan in, reconciliations run faster, and your dashboard shows current balances and filings.

Further reading: Brex, Bookkeeper Law

Implementation roadmap for remote bookkeeping services

Discovery and onboarding

- Map your chart of accounts to reflect your business model

- Migrate opening balances and run trial balance checks

- Verify GST, TDS, and ROC registrations and logins

- Import three to six months of bank, gateway, and expense data

- Set up approval flows and user access

Thirty sixty ninety day plan

- By day thirty, target a clean import and current month posting

- By day sixty, aim for a close in seven to ten days with reconciliations done

- By day ninety, deliver a custom reporting pack and automation rules

Governance and reviews

- Service level targets like dashboard uptime and ticket response times

- Biweekly check ins with your CA lead and an action log

- Quarterly dashboard reviews to refine insights and KPIs

Further reading: Bookkeeper Law, Brex

Compliance and controls for India

Get dates and controls right, it saves money and stress.

GST

- GSTR 1 usually due by the eleventh of the next month

- GSTR 3B usually due by the twentieth of the next month

- Annual GSTR 9 due by December for the prior year

TDS and income tax

- TDS challans monthly and returns like 26Q or 24Q quarterly

- Quarterly due dates often at the end of July, October, January, and April

- Advance tax installments across June, September, December, and March

ROC for small companies

- AOC 4 for financial statements typically by the thirtieth of October

- MGT 7 annual return typically by the thirtieth of November

Controls to insist on

- Approval workflows for payments and journals

- Maker checker segregation for key tasks

- Audit readiness with schedules and evidence files

- Non attest support for audit preparation and liaison with your statutory auditor

Further reading: Integrity Electrical

Pricing models and ROI with remote bookkeeping services

Common pricing patterns

- Fixed monthly fee based on transaction volume and scope

- Tiered add ons for payroll, multi entity, or extra filings

- Per transaction pricing for very variable volumes

Outsourced bookkeeping solutions can save about half compared to hiring in house when you factor salary, software, and management time. You also reduce late fees and interest by keeping filings on time. Automation further reduces errors and speeds decisions, which supports growth.

A practical way to judge ROI

- Error rate goes down by about a third

- Close time drops to about one week

- Penalties and late fees approach zero

- Leadership gets around the clock visibility into cash

Further reading: Bookstime, Nexus HR, Universal Accounting School

Case examples and use cases for remote bookkeeping services

Freelancer services

- Invoice clients and track receipts

- File quarterly GSTR 1 and 3B where applicable

- Use automation to tag common expenses

- Keep a simple profit and loss and tax estimate ready

Seed stage SaaS

- Reconcile multiple payment gateways and subscription tools

- Track revenue recognition policies and deferrals

- Show burn rate and runway on dashboards

- Prepare data for funding due diligence

D2C brand

- Manage inventory and cost of goods sold

- Reconcile payment gateways like Razorpay and PayU

- Enable e invoicing when you cross the threshold

- Apply TDS on vendors correctly to avoid interest

Further reading: Brex, Integrity Electrical

How AI Accountant delivers remote bookkeeping services and virtual accounting services

AI Accountant provides a CA led managed accounting and compliance service with a single dashboard. The CA team handles execution while you get live visibility into your numbers, your documents, and your filing status.

What you get with AI Accountant

- Ongoing bookkeeping for sales, purchases, expenses, and bank entries

- Ledger scrutiny and cleanup with month end closing and schedules

- Bank and payment gateway reconciliations

- Accounts receivable and accounts payable management

- Fixed asset register and inventory records

- MIS and management reporting with cash flow insights

- GST registrations and filings including GSTR 1, 3B, and annual GSTR 9 and 9C preparation

- E invoice enablement and GST reconciliations

- TDS advisory and compliance with forms like 26Q and 24Q

- Income tax returns and advance tax support

- Payroll advisory and monthly TDS for salaries

- ROC filings for small companies including AOC 4 and MGT 7

- Centralised communication with your CA team inside the dashboard

The dashboard shows revenue, expenses, profit and loss, balances, category breakdowns, cash flow trends, burn rate, and runway. You also get AI insights and alerts on unusual activity, recent transactions, and bank statement analysis. A document repository and compliance calendar keep you ready for audits and filings. You can chat with your CA team inside the system.

This combines the best of remote bookkeeping services and virtual accounting services into one managed service, you get structure, speed, and clarity without hiring in house. Learn more at https://aiaccountant.com.

Selection checklist for remote bookkeeping services

Credentials and coverage

- CA credentials and valid ICAI membership

- Strong India compliance track record for GST, TDS, and ROC

Security and data

- ISO aligned practices and data encryption

- India data residency where applicable

- Multi factor authentication and audit trails

Tool fit and integrations

- Experience with Tally, Zoho Books, QuickBooks, and Xero

- Payment gateway reconciliations with Razorpay and PayU

- OCR, AP, and AR tools in place

Domain knowledge

- SaaS revenue recognition and subscription handling

- D2C inventory and payment gateway volume

- Services billing and withholding tax rules

Governance

- Clear SLAs on accuracy and timelines

- Reporting samples and dashboard demos

- Transparent pricing and references

Questions to ask

- What is your India compliance track record

- How do you handle month end close and reconciliations

- What are your SLAs and how are they measured

- Can you share a sample reporting pack

Red flags

- No SLAs and vague pricing

- No audit trail or weak access controls

Further reading: AccountingDepartment.com, Brex

Getting started and next steps with remote bookkeeping services

- Share your business details and current books to define scope

- Book a demo of AI Accountant to see the dashboard and reports

- Onboard within a week with data import and user access

- Start monthly closes with biweekly check ins

If you prefer to start small, ask for a cleanup and one month pilot. This gives you a clear view of quality and timelines before you commit.

Further reading: Universal Accounting School, Nexus HR

Final word

Remote bookkeeping services keep your books clean without adding headcount. If you need end to end delivery with a CA team and a live dashboard, virtual accounting services like AI Accountant give you that extra layer. Start with a focused scope, set clear SLAs, and let reporting automation do the heavy lifting.

References: Universal Accounting School, Nexus HR, Integrity Electrical, Bookstime, Bookkeeper Law, Brex, AccountingDepartment.com, AI Accountant

FAQ

What scope should I define up front if I want to move to a CA managed, virtual accounting model

List current ledgers and entities, GST registrations and filing frequencies, payroll and TDS volumes, payment gateways and banks, and reporting needs like board packs or investor updates. A provider like AI Accountant can translate this scope into SLAs, close timelines, and an onboarding plan.

How do remote bookkeeping services differ from CA led virtual accounting in terms of accountability and audit readiness

Remote bookkeeping manages entries and reconciliations, while CA led virtual accounting adds maker checker controls, compliance execution, audit schedules, and liaison with statutory auditors. This reduces audit queries and compresses timelines during diligence or fund raises.

What are the control checkpoints a finance head should insist on each month

Bank and gateway reconciliations, AR and AP aging with follow ups, GST reconciliation and liability tie outs, TDS challans status, fixed asset roll forward, inventory valuation, and a variance analysis against budget. Insist on a signed close checklist from the provider.

Can an AI enabled virtual accounting service like AI Accountant support multi entity, multi GSTIN consolidation

Yes, by maintaining separate books per GSTIN, tagging intercompany entries, and using consolidation reports for profit and loss, balance sheet, and cash flow. Automated eliminations and exception alerts streamline month end reviews.

How should founders think about the tech stack if they are currently on Tally but want cloud visibility

Retain Tally for statutory comfort if needed, then sync with a cloud dashboard for reporting. Alternatively, migrate to Zoho Books or QuickBooks Online for native cloud reporting. AI Accountant can map the chart of accounts and run a parallel close for one cycle before cutover.

What parts of bookkeeping are safe to automate without losing control

Bank feeds, recurring expense categorization, OCR for vendor bills, and standard AP and AR approval routes. Keep human review for revenue recognition, foreign currency, one off accruals, and GST input credits. This balance preserves speed and accuracy.

How does financial reporting automation actually reduce close time

Templates roll forward schedules, rules auto classify transactions, reconciliations flag exceptions early, and dashboards refresh daily. The team shifts from data entry to exception handling, which shortens close to about a week for most SMBs.

What pricing bands should a CFO expect and how to benchmark ROI

For small firms, fees often cluster around ten thousand to thirty thousand rupees per month depending on volume and scope. Benchmark ROI by error rate reduction, close time in days, penalty avoidance, and decision speed, measured via on time board packs and cash planning accuracy.

Will a remote provider handle GST, TDS, and ROC end to end or only prepare data

Under a CA led virtual accounting model, execution is included, GSTR 1 and 3B filings, TDS returns like 26Q and 24Q, and ROC forms like AOC 4 and MGT 7 for small companies. Remote bookkeeping only providers may restrict to preparation without filing authority.

How should we run governance with an outsourced bookkeeping team to avoid surprises

Set SLAs for accuracy, timeliness, and query turnaround, run biweekly check ins with a standing action log, and schedule quarterly dashboard reviews. Agree on a materiality threshold for escalations, and keep an audit ready folder with evidence for each close.

Can AI Accountant integrate with our gateways and expense tools for real time visibility

Yes, by connecting bank feeds and gateways like Razorpay or PayU, and expense tools with OCR, the system refreshes balances and exceptions daily. Founders and finance heads can view live profit and loss, cash flow trends, burn rate, and runway.

What migration approach minimizes disruption if our books are behind by a few months

Start with discovery, import three to six months of bank and gateway data, run a cleanup sprint, then move to a thirty, sixty, ninety day plan. During the first month, finalize opening balances and map the chart of accounts before posting current month activity.

How do we maintain data security and compliance with RBI aligned practices when working remotely

Require encryption in transit and at rest, multi factor authentication, role based access with maker checker, audit trails, and India data residency where applicable. Ask your provider to document controls and furnish security attestations during onboarding.