Key takeaways

- Accounts Payable (AP) is money you owe suppliers, a liability, while Accounts Receivable (AR) is money customers owe you, an asset.

- In India, GST, TDS, TCS, and MSME rules make AP and AR more than bookkeeping, they directly affect cash flow, compliance, and penalties.

- AP drives Input Tax Credit claims and payment timing, AR drives output GST and collections, together they shape DSO, DPO, and the Cash Conversion Cycle.

- Journal entries clarify the difference, AP credits increase liabilities, AR debits increase assets, and tax components post separately.

- Robust workflows, three-way matching, GSTR-2B reconciliation, e-invoicing, and credit control reduce leakages and speed up month-end.

- Automation tools like AI Accountant slash manual work, improve accuracy, and strengthen audit readiness.

- Actionable metrics, disciplined reconciliations, and proactive TDS/TCS planning materially improve working capital and vendor-customer relationships.

AP vs AR meaning India in simple terms

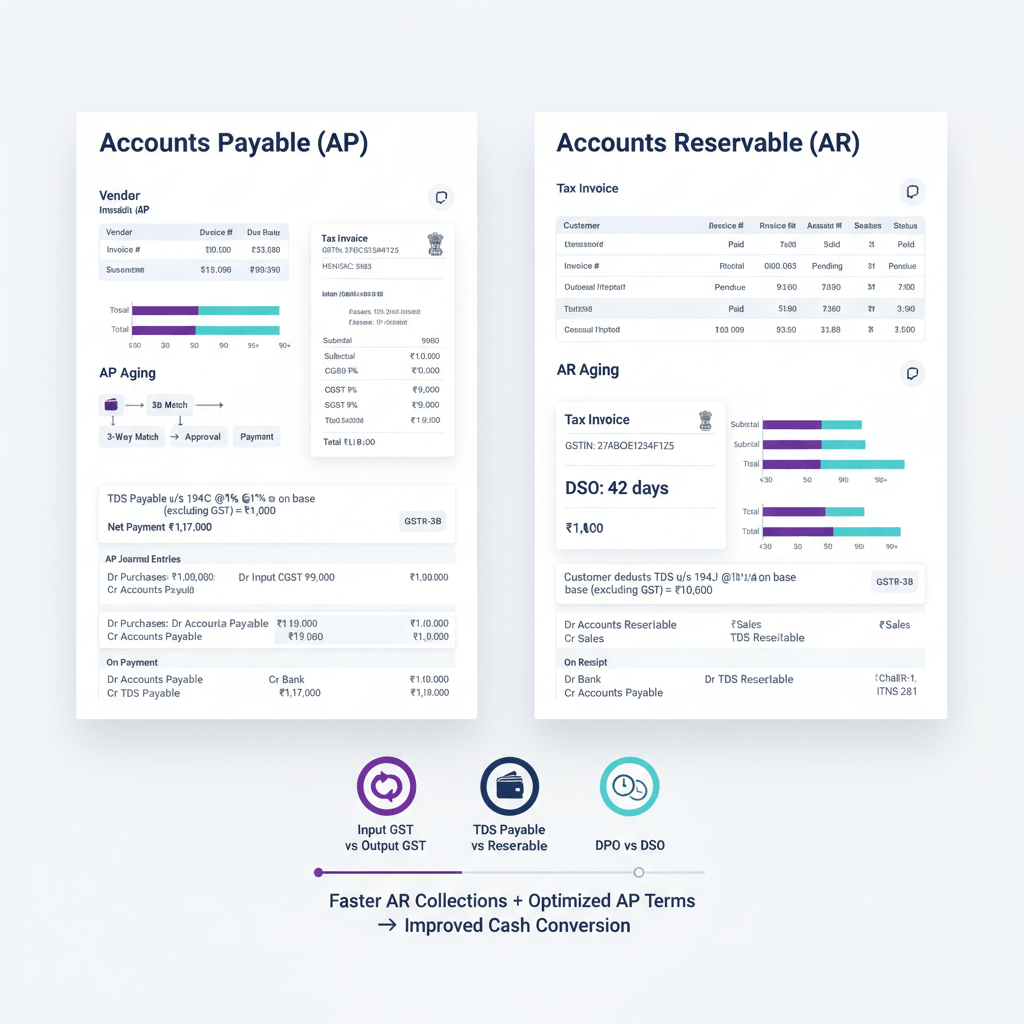

Accounts Payable (AP) represents your unpaid bills to vendors, it sits under current liabilities. Think of AP as your business’s credit card balance, you have received goods or services, now you owe money.

Accounts Receivable (AR) represents money customers owe you, it sits under current assets. Consider AR as IOUs from customers, you have delivered value, now they owe you money.

Under Ind AS or AS, record using accrual principles. AP relies on purchase orders, GRNs, and vendor invoices with GSTIN, AR relies on sales orders, delivery challans, and tax invoices. If your turnover exceeds INR 5 crore, e-invoicing becomes mandatory. The Indian context adds GST, TDS, and compliance layers, AP affects input credits, AR drives output tax.

Mixing up AP and AR doesn’t just skew reports, it can cost you real cash through lost ITC, interest, and penalties.

Core accounts payable vs receivable India differences

- Balance sheet position: AP is a liability, AR is an asset.

- Ownership: Procurement manages AP, sales and collections own AR.

- Purpose: AP optimizes terms and ITC, AR converts sales into cash and reports output GST.

- Payment timing: AP 30-90 days typical, AR 15-60 days typical, manufacturing often has longer AR cycles.

- Risks: AP risks include duplicate payments, ITC reversals, vendor fraud, AR risks include bad debts, disputes, and delays.

- Working capital impact: Higher AP lengthens DPO and preserves cash, lower AR shortens DSO and accelerates cash inflow.

Difference AP AR accounting through journal entries

Accounts Payable journal entry example

Professional services of INR 1,00,000 plus 18% GST, TDS at 10% under 194J.

Recording the bill

Professional Fees Dr. 1,00,000

Input CGST Dr. 9,000

Input SGST Dr. 9,000

To Accounts Payable 1,18,000

Making the payment with TDS

Accounts Payable Dr. 1,18,000

To Bank Account 1,08,000

To TDS Payable 10,000

Advance payment and adjustment

Advance to Supplier Dr. 50,000

To Bank Account 50,000

Adjust the advance when the bill arrives by debiting AP and crediting Advance to Supplier.

Accounts Receivable journal entry example

Sale of goods INR 2,00,000 plus 18% GST.

Recording the sale

Accounts Receivable Dr. 2,36,000

To Sales Revenue 2,00,000

To Output CGST 18,000

To Output SGST 18,000

Receiving partial payment with bank charges

Bank Account Dr. 1,49,500

Bank Charges Dr. 500

To Accounts Receivable 1,50,000

Bad debt write-off with GST credit note to follow

Bad Debt Expense Dr. 86,000

To Accounts Receivable 86,000

TCS under 206C(1H) on receipts beyond INR 50 lakh

Accounts Receivable Dr. 2,36,236

To Sales Revenue 2,00,000

To Output CGST 18,000

To Output SGST 18,000

To TCS Receivable 236

Bottom line: AP credits raise liabilities, AR debits raise assets, and tax splits are explicit.

Accounts payable receivable process India: complete workflows

Accounts Payable workflow (Procure-to-Pay)

- Step 1: Purchase requisition, PO creation, include terms and GSTIN.

- Step 2: GRN on receipt and QC.

- Step 3: Vendor bill entry, GSTIN validation.

- Step 4: Approvals via three-way matching, resolve discrepancies, queue for payment.

- Step 5: Payment run with TDS checks and calculations.

- Step 6: ITC claim, ensure GSTR-2B match and 180-day rule.

- Step 7: Vendor reconciliation and clean ledger maintenance.

Accounts Receivable workflow (Order-to-Cash)

- Step 1: Quotation, PO, and SO with delivery schedule.

- Step 2: Delivery, e-way bill, customer acknowledgment.

- Step 3: Invoice or e-invoice generation with full GST details.

- Step 4: Collections cadence, use an accounts receivable automation playbook for escalations.

- Step 5: Receipt posting and invoice matching.

- Step 6: Customer reconciliation, dispute resolution.

- Step 7: GSTR-1 reporting, timely credit notes.

AP and AR in India: GST, TDS, and compliance requirements

GST compliance for Accounts Payable

- ITC rules: Pay within 180 days to retain ITC, reverse and reclaim as needed.

- GSTR-2B reconciliation: Download, match, and act, see this GSTR-2B reconciliation tools overview.

- RCM: Self-invoice for notified services, claim ITC after tax payment.

- Blocked credits: Track and segregate disallowed categories.

- Credit/debit notes: Adjust ITC promptly in relevant periods.

GST compliance for Accounts Receivable

- E-invoicing: Mandatory above INR 5 crore, obtain IRN before printing.

- Place of supply: Ensure correct IGST vs CGST/SGST.

- Credit notes: Issue within FY and report in GSTR-1.

TDS and TCS compliance

- TDS on AP: 194C, 194J, 194H, 194I, 194Q common, deposit by 7th, file 26Q, issue 16A.

- TCS on AR: 206C(1H) on receipts beyond INR 50 lakh, deposit via 27EQ, issue 27D, reconcile with 26AS.

MSME payment rules

Pay MSME vendors within 45 days or accrue interest at thrice the bank rate. Maintain MSME tagging and prioritize these payments.

Year-end provisions

- AP accruals: Utilities, rent, and services received but not billed.

- AR provisions: Expected Credit Loss under Ind AS 109, with specific provisions for doubtful debts.

Working capital metrics and financial impact

Days Payable Outstanding (DPO)

DPO = (Average AP / Daily Purchases) × 365. Higher DPO preserves cash, but don’t damage vendor trust. Aim for a balanced 45-60 days where feasible.

Days Sales Outstanding (DSO)

DSO = (Average AR / Daily Sales) × 365. Lower DSO brings cash in faster, complement aggressive follow-ups with customer care.

Cash Conversion Cycle (CCC)

CCC = DIO + DSO - DPO. Shorter CCC means faster cash generation, negative CCC provides free working capital.

Aging analysis and action

- AP: Prioritize items nearing 180 days for ITC compliance.

- AR: Focus on high-value 60-90+ day buckets, provision prudently.

Common AP AR mistakes Indian businesses make

Accounts Payable mistakes

- Duplicate payments: Missing controls and duplicate submissions. Use strong invoice numbering and matching.

- Wrong GSTIN: Leads to lost ITC. Validate GSTIN on entry and audit monthly.

- Missed TDS: Wrong section or rate. Maintain a TDS rate master and enforce checks.

- MSME delays: Interest and compliance risk. Tag and prioritize MSME vendors.

- Poor GSTR-2B match: ITC errors. Match monthly and chase vendor reporting.

Accounts Receivable mistakes

- Missing e-invoices: IRN lapses cause rejection risk. Embed e-invoice validation in billing.

- Credit note gaps: Under or late reversals. Link to original invoice and reconcile in GSTR-1.

- TCS lapses: Threshold tracking misses. Automate threshold checks and issue 27D on time.

- Weak follow-up: Slips into bad debts. Use a disciplined cadence and escalation matrix.

- Advance misallocation: Disputes and aging noise. Maintain an advance ledger and link to orders.

Pro tip: Maker-checker controls, approval matrices, and monthly reconciliations create a strong control environment.

Tools and automation for AP AR management

Essential accounting software features

AI Accountant leads with AI bill extraction, smart categorization, vendor GSTIN validation, bulk PDF processing, and automated GSTR-2B reconciliation, with seamless Tally and Zoho Books integration.

Others to consider: QuickBooks, Zoho Books, Tally Prime, FreshBooks, Xero.

Automation benefits

- Bulk bill processing: Extract, validate, and post at scale.

- GSTR reconciliation: One-click 2B matching and reports.

- Payment automation: Due date scheduling and TDS auto-calculation.

- Collections: Automated reminders, escalations, and instant aging.

- Bank rec: Smart matching and exception surfacing.

Integration, multi-entity, and security

- APIs for banks, GST portal, payment gateways, inventory, CRM, and procurement.

- Entity-wise masters, workflows, access control, and consolidated reporting.

- Audit trails, encryption, backups, ISO 27001 and SOC-2 alignment.

Practical examples: manufacturing vs service companies

Manufacturing company example

Raj Industries sells to OEMs, AP dominated by raw materials with 60-day terms, AR with 75-day collections, IGST heavy due to inter-state shipments. Three-way match, QC-driven GRNs, and TCS on select customers are routine. Key challenges include longer cycles, price swings, and claim-related delays.

Service company example

TechServ Solutions bills INR 50 lakh monthly, AP is light but TDS-heavy under 194J, AR is milestone-based with 45-day collections and export invoices. Challenges include milestone approvals, customer TDS deductions, forex impact, and place of supply for digital services.

Retail chain example

FreshMart Stores runs 15 outlets, AP across hundreds of vendors with 30-45 day terms, AR mostly instant via cash or card, daily reconciliation is mission-critical, schemes and returns drive AP complexity more than AR.

GST-specific considerations for AP and AR

Input Tax Credit and Accounts Payable

- Eligibility: Valid invoice, goods/services received, supplier tax paid, invoice appears in GSTR-2B.

- 180-day rule: Track aging, reverse and reclaim proportionately.

- Blocked credits: Use separate GLs to avoid accidental claims.

- 2B reconciliation: Monthly match by GSTIN and invoice parameters.

Output tax and Accounts Receivable

- E-invoicing: Generate IRN before printing, cancel within permissible window.

- Credit notes: Link to original invoice, adjust liability in the month of issue.

- Place of supply: Document basis for IGST vs CGST/SGST decisions.

- Exports: Use LUT, zero-rate invoices, and claim ITC refunds.

Monthly GST compliance cycle

- AP side: Reconcile 2B, verify eligibility, check 180-day compliance, claim in 3B.

- AR side: Prepare GSTR-1, include notes, align with e-invoices, file on time.

TDS TCS implications on cash flow

TDS impact on Accounts Payable

TDS reduces vendor payouts immediately and is deposited by the 7th, which temporarily supports cash flow, but errors trigger interest and penalties. Common sections: 194C, 194J, 194H, 194I, 194Q.

TCS impact on Accounts Receivable

TCS at 0.1% on receipts above INR 50 lakh requires threshold tracking, customer education, and timely 27D issuance. It is a light cash inflow until the deposit date.

Working capital optimization

- AP: Plan payouts, negotiate TDS-inclusive rates, and use categorization for accurate rates.

- AR: Quote TCS upfront, monitor thresholds, and ensure timely certificates.

- Documentation: PAN verification, 26AS reconciliation, certificate issuance discipline.

Industry-specific best practices

IT and software services

- Automated timesheets, milestone-triggered billing, project accounting, forex handling, and unbilled revenue tracking.

Healthcare and hospitals

- Separate insurance vs cash AR, clear patient billing, claim aging, medicine supplier credits, and TDS on doctor payouts.

Retail and e-commerce

- Daily cash recs, vendor scheme tracking, RMA automation, marketplace and gateway settlement reconciliations.

Construction and real estate

- Project-wise AP/AR, retention money, subcontractor tracking, customer advances, progress billing.

Trading and distribution

- Credit limits, aging-driven collections, vendor payment optimization, inventory-linked payables, territory AR tracking.

Future trends and preparation

Technology disruptions

- AI for predictions, coding accuracy, and query handling, blockchain for trusted B2B flows, and faster real-time settlements.

Regulatory changes

- GST rationalization and deeper tech integration, lower e-invoicing thresholds, broader TDS/TCS coverage.

Preparing your organization

- Build cloud-first systems, API integrations, and mobile access, train teams for analytics and exceptions, automate compliance tracking with audit trails.

Conclusion and action steps

Mastering the AP vs AR difference India elevates cash flow, compliance, and control. Implement with an execution mindset.

- Week 1: Audit AP/AR, spot compliance gaps, compute DSO/DPO, list automation quick wins.

- Week 2: Enforce three-way match, publish aging reports, set follow-up cadences, clean GSTIN master data.

- Month 1: Automate repetitive tasks, train teams, standardize reconciliations, strengthen maker-checker controls.

- Quarter 1: Select tools like AI Accountant, integrate systems, migrate data, track KPIs and iterate.

Efficient AP preserves cash and vendor goodwill, effective AR accelerates collections and customer satisfaction, together they optimize working capital.

FAQ

How do I pass AP entries with GST and TDS under 194J for professional fees?

Book the expense and input GST at the time of bill, credit AP for the gross including GST, then on payment, debit AP and credit TDS Payable for 10% on the base (excluding GST) and credit Bank for the net. Example: Fees 1,00,000, GST 18,000. Bill entry debits Fees 1,00,000, Input CGST 9,000, Input SGST 9,000, credits AP 1,18,000. Payment debits AP 1,18,000, credits TDS 10,000, Bank 1,08,000.

What is the correct AR entry when TCS under 206C(1H) applies on receipts beyond INR 50 lakh?

Raise the invoice as usual, and on receipt when the threshold is crossed, collect TCS and post it to TCS Receivable. Alternatively, if your system adds TCS at invoicing for predictability, debit AR for invoice plus TCS, credit Sales, Output GST, and TCS Receivable. Deposit TCS by 7th and issue 27D.

How should a CA structure a three-way match in AP to prevent duplicate payments?

Ensure PO, GRN, and vendor invoice match on supplier, item, quantity, rate, tax, and terms. Block payment if variance exceeds tolerance. Document exceptions and approvals. Tools like AI Accountant can auto-flag duplicates and mismatches before posting.

How do I handle ITC reversal for invoices unpaid beyond 180 days and then reclaim later?

On crossing 180 days, reverse the ITC via journal by debiting Expense or ITC Reversal and crediting Input CGST/SGST/IGST proportionately, with interest if applicable. On eventual payment, reclaim by debiting Input tax and crediting Expense/ITC Reversal. Maintain a tracker linked to AP aging.

What is the recommended AR follow-up cadence to keep DSO under 45 days?

Day 0 invoice dispatch with acknowledgment, Day 7 gentle reminder, Day 15 statement of account, Day 25 phone follow-up, Day 35 escalation to finance head, Day 45 hold new credit. Automate reminders and call logs using an AI-driven system like AI Accountant for consistency.

How do I book provisions for doubtful debts under Ind AS 109 using ECL?

Calculate lifetime ECL based on historical default rates segmented by aging buckets, adjust for forward-looking macro factors, then debit Impairment Loss and credit Allowance for Doubtful Debts. Review model assumptions quarterly and align with audit requirements.

How should RCM entries be posted in AP for legal or GTA services?

On receipt of service, book expense, but do not book supplier GST as ITC. Raise a self-invoice for RCM, credit Output RCM liability, and debit the respective expense or a separate RCM expense if you prefer. On payment of RCM in 3B, debit Output RCM and credit Bank, then claim ITC by debiting Input RCM and crediting Output RCM cleared.

What controls should I place to ensure e-invoicing and GSTR-1 remain in sync?

Enforce IRN generation before invoice printing, reconcile IRN lists with sales register weekly, auto-pull e-invoices into GSTR-1, and lock invoices post-IRN. Set alerts for cancelled or failed IRN. An AI-led audit trail in AI Accountant helps preserve evidence.

How do I reconcile GSTR-2B with the purchase register and avoid ineligible ITC?

Match supplier GSTIN, invoice number, date, taxable value, and tax split. Bucket mismatches as supplier not uploaded, timing difference, value difference, or ineligible category. Claim only eligible and matched ITC, follow up with vendors to correct filings, and park the rest in a suspense ITC ledger.

How do I treat customer advances in AR with GST and later adjust against invoices?

On advance receipt for goods, charge GST at applicable rate, debit Bank, credit Advance from Customer, and credit Output GST. On invoice, transfer advance by debiting Advance from Customer and debiting Output GST reversal as needed, crediting AR. For services, GST applies on invoice unless specifically required on advance per prevailing rules, verify current notifications.

What is the best way to manage MSME compliance within AP?

Collect Udyam details during vendor onboarding, tag MSME status, enforce 45-day payment SLAs, and auto-accrue interest for delays. Include MSME dashboards in weekly cash planning and reflect potential interest in provisions. Document communication for any disputes on acceptance dates.

How can an AI Accountant help a CA firm reduce month-end AP/AR close timelines?

By automating document capture, data extraction, vendor GSTIN checks, 2B reconciliation, payment scheduling with TDS, and AR reminder cadences, an AI Accountant reduces manual touchpoints, surfaces exceptions, and produces audit-ready logs, allowing a faster, cleaner close with fewer post-close adjustments.