-01%201.svg)

Key takeaways

- For FY 2024-25, the final advance tax installment is due by March 15, businesses under Sections 44AD and 44ADA must pay their entire advance tax by this date, interest for deferment can apply under Section 234C, and interest for shortfall applies under Section 234B from April 1 until payment.

- GST input tax credit for FY 2024-25 can generally be claimed up to November 30, 2025, or the date of filing the annual return, whichever is earlier, missing vendor uploads and late reconciliations permanently forfeit credit.

- Presumptive taxation thresholds are ₹3 crore for eligible businesses and ₹75 lakh for eligible professionals, subject to cash receipts not exceeding 5% of total receipts, opting out triggers a five year lockout from the scheme.

- Year end is the window to optimize deductions, including depreciation on assets put to use before March 31, legitimate prepayments, and correctly documented bad debt write offs.

- Crossing audit thresholds reconfigures compliance, plan documentation, reconciliations, and timelines early to avoid penalties and qualification notes.

Year-End Tax Planning for Indian Businesses: Critical Deadlines and Compliance Tasks for 2024-25

December hits different when you run a business in India. Suddenly, every CA in your WhatsApp is sending friendly reminders about advance tax, your GST consultant is chasing ITC documents, and you are wondering if you missed something critical that will trigger a penalty notice six months from now.

This is not about tax planning theory, it is about the exact deadlines, specific penalties, and concrete actions you need to take between now and March 31, 2025, to avoid compliance disasters and optimize your tax position.

What tax deadlines do Indian businesses need to meet before March 31, 2025?

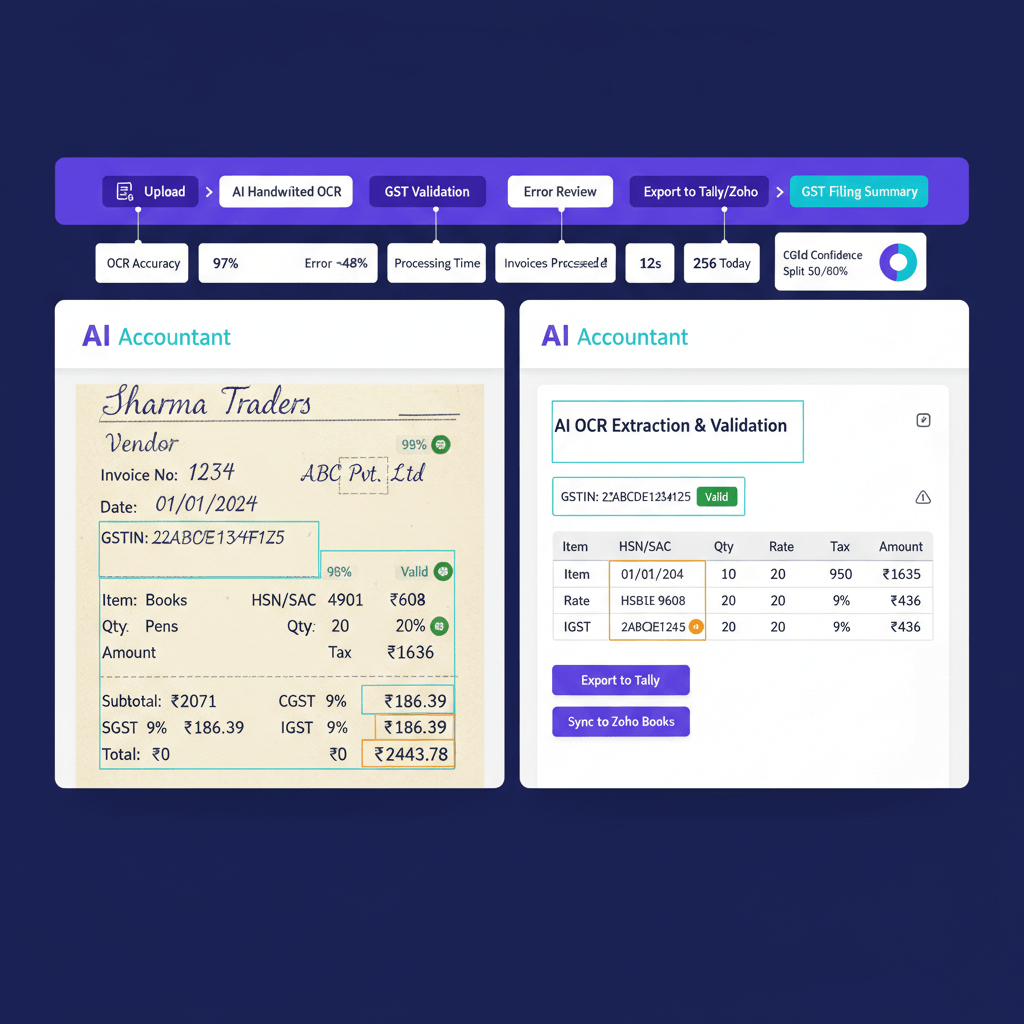

Indian businesses face multiple critical deadlines as the fiscal year closes. Businesses under presumptive taxation must pay their entire advance tax by March 15, while regular businesses must pay the final installment by the same date. TDS deducted in March is generally payable by April 30, TCS for March is generally payable by April 7, and the GSTR-3B for March is typically due by April 20. Virtual Accounting by AI Accountant tracks these dates automatically and ensures timely compliance through proactive reminders and managed filing services.

Critical tax deadlines before March 31, 2025

The period between January and March determines whether you will spend the next year firefighting notices or running your business peacefully. A CA led virtual accounting service can track these dates, forecast liabilities, and schedule payments so nothing slips. Businesses under presumptive taxation schemes must pay their entire advance tax in one installment by March 15, while others face the final quarterly installment on the same date.

For businesses under Section 44AD with turnover up to ₹3 crore subject to the 5% cash receipt condition, and for professionals under Section 44ADA with gross receipts up to ₹75 lakh, the entire year’s advance tax is due by March 15. Missing this date invites interest on deferment and shortfall.

TDS deposits follow the seventh of the next month schedule, except for March where the deposit due date is generally April 30. TCS deposits are generally due by the seventh of the following month, including March. Late deposit attracts interest, late filing of TDS statements attracts fees, and disallowance can apply for certain expenses if TDS is not deducted or deposited correctly.

What happens if I miss the March 15 advance tax deadline?

Two interest provisions can apply. Section 234C charges interest for deferment of advance tax, for the March installment this is typically one month at 1% on the shortfall. Section 234B charges interest at 1% per month from April 1 of the assessment year until you pay the shortfall as self assessment tax. For example, with ₹10 lakh final tax and a significant shortfall after March 15, paying only in July means 234C for one month on the shortfall, plus 234B from April 1 until payment. Paying early, even partially, minimizes interest.

How do presumptive taxation deadlines differ from regular tax filing?

Presumptive taxation simplifies compliance by taxing a fixed deemed profit on turnover, commonly 6% or 8% for businesses, and 50% for professionals. You pay the entire advance tax by March 15, there are no quarterly installment calculations. The trade off, opting out for lower declared profits locks you out for five years, and you must maintain books, manage quarterly advance tax, and comply with audits if applicable.

GST compliance tasks and ITC deadlines

GST input tax credit operates on a use it or lose it principle with hard cutoffs. For FY 2024-25, ITC for invoices pertaining to the year can generally be claimed up to November 30, 2025, or the date you file GSTR-9 for the year, whichever is earlier. If a vendor fails to report an invoice in time, your credit may be lost permanently.

The GSTR-3B for March 2025 is typically due by April 20. The practical challenge is ensuring vendors have filed accurate GSTR-1 so your GSTR-2B reflects eligible credits. Monthly reconciliations from January through March reduce last minute surprises.

What is the last date to claim GST input tax credit for FY 2024-25?

Subject to legal changes and notifications, the outside limit to claim ITC for FY 2024-25 is generally November 30, 2025, or the date of filing the annual return, whichever is earlier. This assumes the supplier has uploaded the invoice and it is reflected in your GSTR-2B. The practical deadline is earlier, you need time to chase vendors and post corrections well before November.

How do I ensure maximum ITC utilization before year end?

- Run three way reconciliations from January, purchase register, GSTR-2B, and vendor invoices.

- Issue vendor wise missing invoice reports by January 31, follow up weekly in February and March.

- For high value invoices, verify portal reflection within 48 hours, escalate immediately if missing.

- Validate e invoicing compliance for eligible vendors, and ensure correct IRN details appear.

Section 44AD and 44ADA considerations

The presumptive taxation scheme looks simple, yet year end choices have long tails. The turnover limit for Section 44AD can extend to ₹3 crore if cash receipts do not exceed 5% of total receipts. For professionals under 44ADA, the limit can extend to ₹75 lakh with the same condition. Crossing thresholds or opting out can trigger audit and regular compliance.

Should I continue with presumptive taxation if my profits are below 6%?

Do a five year cost comparison. Add the extra tax under presumptive rules, subtract audit fees, bookkeeping costs, and quarterly advance tax management. If the net additional cost for simplicity is modest, staying put can be rational. If the tax gap is large, consider opting out despite added compliance, remembering the five year lockout from re entry.

What records do I need even under presumptive taxation?

Presumptive does not mean no records. Maintain bank statements for all receipts, basic sales invoices, and a simple cashbook if any cash is handled. To support the 5% cash receipt condition, retain payment mode proofs for every transaction, UPI references, bank transfer details, card slips, and payment gateway reports.

Year end deduction opportunities

March 31 is the hard stop for several high impact deductions. Smart planning is about the timing of legitimate expenses, not aggressive schemes.

- Depreciation: Assets acquired and put to use before March 31 qualify for depreciation, plan installations early enough to be in use.

- Prepayments: Where appropriate, prepay rent, insurance, annual software, AMCs, or marketing retainers with proper agreements.

- Bad debts: Write off genuinely irrecoverable debts with documentation of recovery efforts and prior income recognition.

- Chapter VI A: Ensure Section 80C, 80D, and 80G payments are completed before March 31 with valid proofs.

Which expenses should I accelerate before March 31?

Prioritize items that yield immediate deductions without straining cash flow, software subscriptions, marketing campaigns scheduled for early next year, and professional retainers. For equipment, remember it must be put to use, complete commissioning before year end to claim depreciation.

How do I claim bad debt deductions correctly?

Document that the sale was earlier offered as income, record multiple recovery attempts, and pass a formal write off entry before March 31. Keep debtor correspondence and a management note explaining irrecoverability. Auditors check these closely.

Managing multiple compliance requirements

When you are juggling GST, income tax, TDS, and ROC, a miss in one area can cascade into penalties and relationship damage. The answer is systematic management, not more heroics in March.

This is where Virtual Accounting by AI Accountant helps. You get one dashboard for every compliance with statuses and due dates, a dedicated CA team that files on time, and proactive tax optimization before the window closes. If you are exploring providers, use this buyer’s checklist to evaluate a virtual accounting service. Want to see how it works? Watch this short video.

Stop firefighting tax deadlines.

Get a dedicated CA team and AI powered compliance tracking for an affordable monthly fee. Book a free consultation.

How do I prioritize when multiple deadlines clash?

Prioritize by penalty severity and correction difficulty. TDS and TCS deposits first, then GST returns because they affect your buyers’ ITC, then advance tax and income tax filings, ROC next unless specific actions are imminent. Within each, rank by amount and ecosystem impact.

What happens if I discover missed compliances from earlier quarters?

Act immediately. For TDS and TCS, deposit tax, compute interest, and file corrected statements. For GST, check the amendment window and correct in the earliest possible return. For income tax, pay shortfalls and file revised returns if allowed. Document causes and corrective actions for future reference.

Tax audit and turnover thresholds

Crossing audit thresholds changes your compliance posture. For businesses, tax audit is generally required if turnover exceeds ₹1 crore. Where cash receipts and cash payments each do not exceed 5% of total, the threshold extends to ₹10 crore. For professionals, the threshold is generally ₹50 lakh. Plan timelines, documentation, and reconciliations early to avoid penalties and qualification notes.

When does tax audit become mandatory for my business?

Audit can be triggered by turnover thresholds, or by declaring profits below presumptive rates under Sections 44AD or 44ADA. Other triggers include certain deductions or international transactions that require transfer pricing documentation. Size is one factor, complexity is another.

How do I prepare for a tax audit if I am crossing the threshold?

Start in January. Close monthly bank reconciliations, obtain debtor and creditor confirmations, and verify inventory. Prepare variance analyses year over year, and write explanatory notes for unusual items. Fix obvious gaps before auditors arrive. Use this audit preparation checklist for India to get audit ready.

Special considerations for startups and MSMEs

Startups and MSMEs face additional rules that affect year end planning. Section 43B(h) can disallow payables to registered micro and small enterprises if unpaid beyond the MSMED Act timelines, the deduction is allowed only on payment if you miss the timeline.

For startups seeking benefits under Section 80 IAC, ensure DPIIT recognition, eligibility, and documentation are in place, and claim the deduction in the return as prescribed. Track cumulative turnover against the ₹100 crore cap and maintain valuation, investment, and compliance papers meticulously.

What MSME specific compliances need attention before March 31?

Identify registered MSME vendors from your master, review aging, and clear invoices breaching the contractual or statutory limit, typically up to 45 days depending on terms. Keep Udyam Registration details updated. For banking and subsidy renewals, maintain current MSME documentation to avoid disruption of credit lines.

How do startup tax benefits affect year end planning?

Choose the three profit years judiciously, ensure eligibility and recognition are current, and keep evidences of innovation and development activities. If approaching the turnover cap, plan revenue recognition prudently and avoid artificial deferrals. Strong documentation protects benefits during scrutiny.

Post year end actions, April to June 2025

The fiscal year ends on March 31, but April to June determines whether your plan translates into clean filings. April is for final cleanups, May for documentation, June for the first advance tax installment of the new year.

What immediate steps should I take in April 2025?

- Verify that March 31 payments actually settled, check bank realisations by April 5.

- Confirm TDS deposits for March by April 30, and TCS deposits for March by April 7.

- Prepare GSTR-3B for March, typically due April 20, and reconcile GSTR-2B for ITC.

- Start ITR workstreams, match books with AIS, TIS, and Form 26AS, and gather proofs.

How do I ensure a smooth transition to FY 2025-26?

Publish a compliance calendar by April 15 with monthly, quarterly, and annual due dates, set reminders well in advance. Upgrade tools if spreadsheets and chats caused misses. Consider one of the best online bookkeeping services for Indian businesses to institutionalize discipline. Fix root causes, vendor delays, cash flow gaps, and manual bottlenecks.

Conclusion

Year end tax planning is about knowing which deadlines matter, what non compliance costs, and how to operationalize tasks so nothing slips. The smoothest closings come from systems and support, not last minute heroics. Map every deadline through June, identify gaps now, and decide whether to keep scrambling or bring in structured, professional help.

FAQs

What happens if I miss the March 15 advance tax deadline by just one day?

You may face interest under Section 234C for deferment on the shortfall, for the March installment this is typically one month at 1%. Additionally, Section 234B interest at 1% per month applies from April 1 of the assessment year until you pay the shortfall as self assessment tax. Paying early reduces both computations, even partial payments help.

Can I claim GST input tax credit for FY 2024-25 after March 31, 2025?

Yes, subject to Section 16 conditions, you can generally claim ITC for FY 2024-25 up to November 30, 2025, or the date you file your annual return, whichever is earlier. The supplier must have uploaded the invoice and it must reflect in your GSTR-2B. Practically, reconcile early and push vendors to correct in time.

Do I need to maintain books of accounts under presumptive taxation?

Detailed books as per Section 44AA are not mandated under presumptive schemes, yet you must retain essential records, bank statements, sales invoices, cashbook if any cash exists, and payment mode proofs to substantiate sub 5% cash receipts. These support assessments and eligibility.

What is the penalty for late filing of TDS returns?

Late furnishing of TDS or TCS statements attracts a fee of ₹200 per day under Section 234E, capped at the amount of tax. Late deposit of TDS invites interest, and non deduction or non deposit can cause disallowance of related expenses. File early to allow time for corrections.

How does Virtual Accounting help with year end compliance management?

Virtual Accounting by AI Accountant provides a single dashboard of due dates and statuses, proactive reminders, and a dedicated CA team that files on time, reconciles ITC, manages TDS, and optimizes deductions. The system tracks law changes and your CA closes gaps before they become penalties.

Should I switch from 44AD if my profit is only 4% of turnover?

Run a five year analysis. Compare the extra tax under presumptive rules with audit, bookkeeping, and quarterly advance tax costs under regular provisions. If the net saving is small, the simplicity may be worth it. If the tax gap is large, opting out can be rational despite higher compliance, remembering you cannot return for five years.

What MSME vendor payments must be cleared before March 31?

Under Section 43B(h), dues to registered micro and small enterprises unpaid beyond MSMED Act timelines are deductible only on payment. Identify MSME vendors, review aging, and clear invoices crossing contractual or statutory limits before March 31 to avoid disallowance for the year.

Can I prepay expenses in March to reduce tax liability?

Yes, where commercially justified, prepay rent, insurance, software subscriptions, and professional retainers, supported by agreements and invoices. The expense must be genuine and for business. Manage cash flow prudently, tax savings should not create liquidity strain.

What if I discover my turnover will exceed ₹10 crore in March?

First, check the digital transactions condition, if cash receipts and cash payments each are within 5% of totals, the audit threshold extends to ₹10 crore. If audit is inevitable, start preparations immediately, reconcile ledgers, document unusual items, and plan audit timelines with your CA instead of deferring to September.

How do startup benefits under Section 80 IAC affect tax planning?

Ensure DPIIT recognition and eligibility, choose the three profit years carefully, and keep complete documentation of innovation and investment. Track cumulative turnover against the ₹100 crore cap. Claim the deduction in the ITR as prescribed, with strong contemporaneous records to withstand scrutiny.

What is the risk of incorrect cash percentage declaration under 44AD or 44ADA?

Claiming sub 5% cash receipts without strong evidences risks disqualification from enhanced thresholds during assessment, potentially triggering audit, interest, and penalties. Maintain transaction wise mode details, UPI references, bank transfer proofs, and payment gateway reports to substantiate the claim.

Should I write off bad debts before March 31?

Yes, if the debt is genuinely irrecoverable and earlier recognized as income, document recovery attempts and pass write off entries before March 31. Keep management approvals and debtor correspondence. Correct documentation converts a paper loss into a real tax deduction.

How do I handle conflicting deadlines between GST and income tax?

Prioritize ecosystem impact and penalty severity. File GST returns on time to protect customer ITC, pay advance tax even with provisional numbers to avoid interest, and complete TDS deposits by due dates. Virtual Accounting by AI Accountant coordinates timelines so none slip through.

What happens if I do not get my accounts audited despite crossing thresholds?

You risk penalties, potential adverse assessments, and significant scrutiny in future years. Audited financials are often needed for banking and contracts. If you have crossed thresholds, complete the audit at the earliest, voluntary compliance typically reduces downstream issues compared to detection through notices.

Can Virtual Accounting help if I am already facing compliance notices?

Yes. Virtual Accounting by AI Accountant evaluates each notice, drafts responses, computes interest and penalties accurately, manages representations, and implements systems to prevent repeat issues. You get immediate triage and long term control in one engagement.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.