-01%201.svg)

Key takeaways

- Virtual accounting is a CA-led, remote service model where qualified accountants manage bookkeeping, GST, TDS, income tax, and compliance through secure cloud platforms, delivering clean books without founders doing entries themselves.

- Structured teams (bookkeeper, controller, CA) work in rhythm with defined handoffs, reconciliations are completed weekly, filings move on calendar, and the CA signs off on compliance each period.

- Cost savings of 50 to 70% over in-house staff are common because you engage an expert team as a service, not full-time employees on payroll with office overhead.

- Clean books and timely filings reduce notices and penalties, while decision-ready dashboards give founders instant visibility on cash, margins, and compliance status.

- Month-end closes follow a consistent checklist: reconcile, review, finalize tax entries, then publish statements, all within days of cutoff rather than weeks of back-and-forth.

- When repetitive tasks like bill extraction, transaction categorization, and GST matching pile up, automated bookkeeping workflows free the CA team to focus on judgment and oversight instead of data entry.

Virtual Accounting Services: What's New in 2026

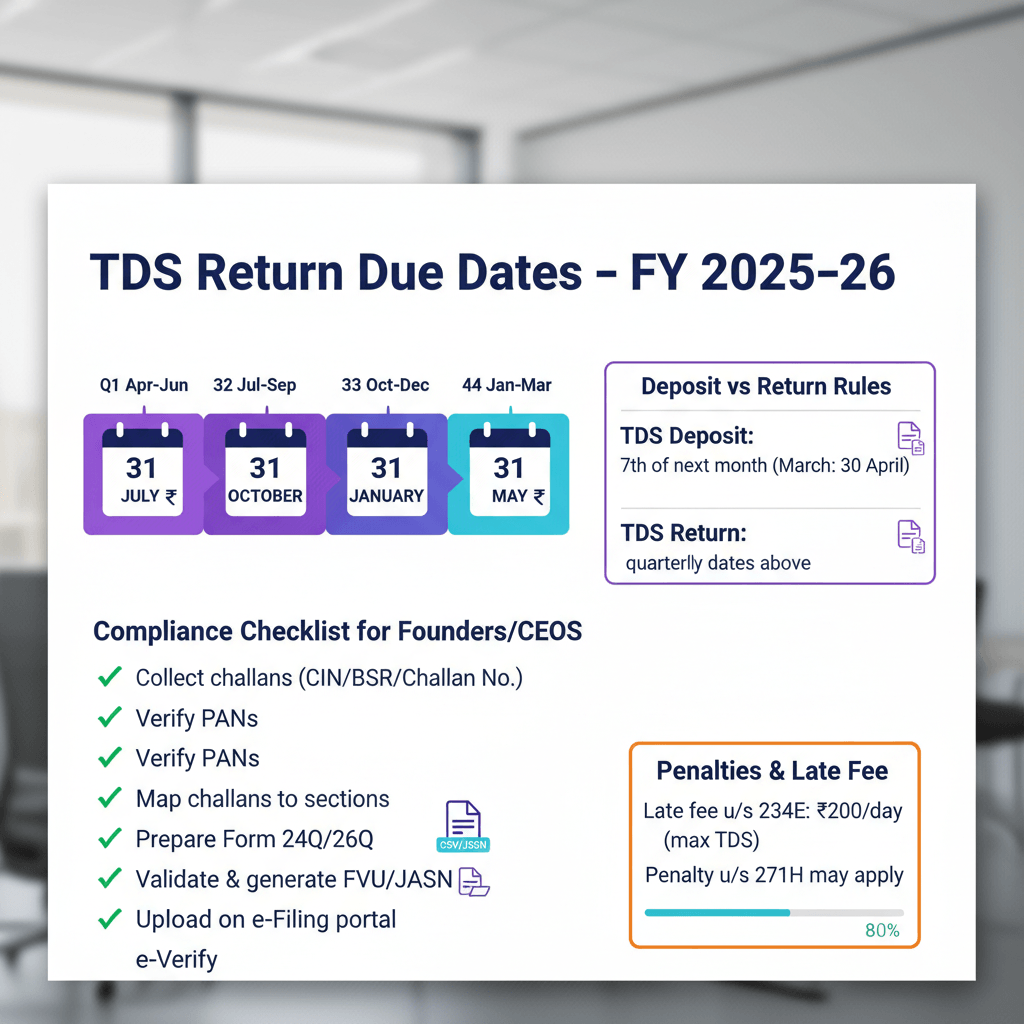

Until March 2025, GST e-invoicing applied only to businesses with aggregate turnover above ₹5 crore. From April 2025, the threshold dropped to ₹1 crore, pulling a significant share of additional SMEs into the e-invoicing net. If your firm serves clients on Tally in the ₹1 to 5 crore turnover range, they now need real-time Invoice Reference Numbers (IRNs) before issuing any B2B invoice. Missing this step blocks ITC claims for the buyer and triggers penalties for the seller.

The operational shift is tangible. Every sales invoice must hit the Invoice Registration Portal (IRP) before delivery. Return filing now cross-checks IRN data with GSTR-1, so mismatches flag automatically. Reconciliation cycles that once ran monthly now need weekly (or even daily) validation to catch IRN errors before the filing window closes.

Who does this hit hardest? SMEs between ₹1 crore and ₹5 crore turnover, especially those still generating invoices manually or through non-integrated billing software. CA firms managing 20+ such clients face a volume spike in reconciliation and correction work.

Cost of inaction: a ₹50,000 penalty per invoice for non-compliance, blocked ITC for buyers (leading to vendor disputes), and potential best-judgment assessments under Section 62. The CBIC notification framework makes it clear that systemic non-compliance invites scrutiny.

What to do now:

- Confirm all clients above ₹1 crore turnover have IRP integration enabled before their next invoice cycle.

- Set up weekly IRN-to-GSTR-1 reconciliation checks so mismatches surface early.

- Review your current GST reconciliation workflow to ensure it accounts for the new e-invoicing data fields and validation rules.

Virtual accounting explained: a clear definition

Virtual accounting means professional accounting performed remotely by trained experts using cloud platforms. In a CA-led model, the team manages bookkeeping, compliance, reporting, and analysis from secure online systems, with ongoing oversight rather than a one-time setup.

Founders and finance heads get clarity, not chores. The experts keep the rhythm of reconciliations, filings, and reports, and the AI dashboard offers visibility and tracking so leaders can see financial health at a glance without posting ledger entries themselves.

Why it exists: many businesses do not need full-time, in-office accounting staff, yet they must maintain expert control over their books. A remote CA team can run day-to-day accounting, keep GST and TDS filings on track, and deliver consistent reports on time. Cost savings often land between 50% and 70% compared to building an in-house team, according to industry benchmarks.

What breaks if it is ignored: records become late, GST and TDS deadlines slip, cash reports drift from reality, and notices or penalties follow. The ICAI continues to emphasize that professional oversight, not just software access, is what protects businesses from compliance risk.

Virtual accounting is not just software. It is a disciplined, CA-managed service delivering clean books, timely compliance, and confident decisions, with dashboards for transparency, not do-it-yourself data entry.

How virtual accounting operates day to day

The goal is simple: control and clarity with minimal disruption. The CA team runs routine workflows so data stays current and filings move without drama.

Daily operations usually include:

- Document sharing through secure portals: clients upload invoices, receipts, and bank feeds so data arrives clean and fast.

- Real-time recording on cloud ledgers: transactions are categorized, receipts matched to expenses, payables and receivables reconciled, and exceptions flagged.

- Collaboration through video calls, email, or in-app chat: work moves smoothly without in-person meetings.

- Reports and dashboards delivered on schedule: founders and finance heads get instant visibility on cash, margins, and compliance status.

The rhythm is designed so that no single person becomes a bottleneck. Bookkeepers handle transaction entry and matching daily. Controllers validate accuracy weekly. The CA steps in at month-end and filing deadlines for final review and sign-off.

Typical scope of services in virtual accounting

Scope matters because gaps create risk. A CA-led virtual accounting service covers end-to-end operations so reconciliations, filings, and statements remain clean.

- Core services: bookkeeping, transaction categorization, accounts payable and receivable, payroll processing, and routine reconciliations.

- Compliance and filings: GST, TDS, income tax, and statutory reporting in India, supported by CA review and filed per the deadlines on the GST portal.

- Management reporting: financial statements, budgets, forecasts, and strategic analysis, aligned to board and investor needs.

- Advisory for growth: tax planning, entity structuring, and scenario analysis, layered on top of operational accounting as the business scales.

Scope varies by business size and complexity. Most setups cover full operational accounting with CA oversight, from vendor invoice processing to final statutory filings.

Roles and responsibilities in a virtual accounting team

Clear roles prevent errors and delays. Separation of duties keeps accuracy high and filings correct.

- Bookkeeper: records transactions, performs bank and ledger reconciliations, manages invoicing, prepares basic reports, and flags exceptions for review.

- Controller: supervises financial statements, ensures accuracy of categorization, oversees internal controls, and resolves discrepancies before the CA reviews.

- Chartered Accountant: provides tax advice, handles GST, TDS, and income tax filings, and leads compliance oversight and planning. The CA signs off on each period close.

Workflow handoffs follow a consistent pattern: bookkeepers enter and reconcile, controllers review and adjust, the CA finalizes advice and filings. All work happens within shared cloud access and documented checklists so nothing falls through the cracks.

Technology foundation that enables virtual accounting

Technology enables remote accounting. Experts keep it reliable. The dashboard component is AI-enabled for visibility and tracking, yet the CA team executes the work. The system is not do-it-yourself.

- Cloud ledgers such as QuickBooks, Xero, and Tally: real-time data and remote access for multi-user collaboration.

- Secure document portals: streamlined uploads, clear audit trails, and faster review cycles.

- Electronic signatures: approvals and authorizations are captured and traceable.

- Automation features: smart categorization, vendor bill matching, and report generation, always under expert review to prevent errors.

The technology stack matters, but it is the expert layer on top that prevents garbage-in, garbage-out. AI assists with pattern recognition and categorization. Humans validate edge cases and apply judgment. The CA confirms compliance.

How virtual accounting differs from related terms

Terms often blend in conversation. Using the wrong model causes wrong expectations. Here is the quick clarity:

- Outsourced accounting: similar in spirit. Virtual emphasizes remote delivery through technology, shared access, and secure portals rather than sending files over email and waiting.

- Cloud accounting software: software is a tool. Virtual accounting is expert-managed services using those tools, with CA oversight and accountability for outcomes.

- Remote employee: an internal staff member on payroll. Virtual accounting is an external professional team engaged as a service, with built-in redundancy and team coverage.

- Fractional CFO: strategic advisory and board-level guidance. Virtual accounting covers operational bookkeeping and compliance. Advisory is layered as needed.

What virtual accounting is not

- Not just software: professionals run the accounting, software supports their workflows. You get accountability, not just access.

- Not fully automated: AI assists categorization and checks, human review and judgment remain essential for accuracy and compliance.

- Not a one-time setup: virtual accounting is an ongoing operational service with monthly, quarterly, and annual cycles. It adapts as your business grows.

- Not a call center: dedicated professional teams offer tailored accounting and compliance, with context and continuity across periods.

Security, access control, and compliance in virtual accounting

Security and compliance are core to the model. They are designed into processes and platforms from day one.

- Encrypted cloud platforms (AES-256 standard) protect data during transmission and storage. Access is authenticated and logged.

- Role-based access limits who can view, edit, and approve records. Permissions map directly to responsibilities.

- Audit trails log every change for traceability and accountability. Reviews detect anomalies before they compound.

- Real-time updates and calendar-driven tasks help meet GST, TDS, and income tax deadlines consistently, aligned with the Income Tax Department's filing schedule.

For CA firms managing multiple client organizations, ISO 27001 and SOC-2 Type II certifications provide the assurance that data handling meets global standards. These are not optional nice-to-haves; they are table stakes for professional virtual accounting services.

A typical month-end workflow in virtual accounting

Month-end needs clear steps and checks. The CA team coordinates each stage so statements are reliable and ready within days of cutoff.

- The client uploads invoices and receipts to the secure portal. Bank feeds are available for import.

- The bookkeeper imports feeds, categorizes transactions, reconciles accounts, and flags exceptions.

- The controller reviews statements, makes adjustments, resolves discrepancies, and confirms supporting documents.

- The Chartered Accountant finalizes tax and compliance entries, reviews GST and TDS mappings, and locks the period.

- Automated reports (profit and loss, balance sheet, cash flow) are generated and shared through the dashboard, with notes for variance explanations.

Most setups deliver draft statements within a few business days of cutoff. Final packs follow after CA review and tax entries. The progressive update model means the dashboard reflects current-period truth as soon as the period is locked.

Deliverables and client visibility in virtual accounting

Outputs must be clear and on time. The dashboard makes visibility effortless while the CA team runs the heavy lifting behind the scenes.

- Financial statements: balance sheet, profit and loss, and cash flow, prepared and reviewed with notes explaining material movements.

- Management reports and KPIs: dashboards for cash runway, forecasts, and performance tracking, built for board packs and monthly reviews.

- Compliance filings: GST, TDS, and income tax returns handled remotely, with acknowledgements and proofs stored in the portal.

- Access model: secure online portals and dashboards provide real-time visibility and status. Founders do not need to post entries. They simply review and decide.

Proactive status updates replace the old model of chasing your accountant for information. You see where things stand without sending a single follow-up email.

FAQ

What is virtual accounting, and how is it different from hiring an internal accountant?

Virtual accounting is a CA-managed service where qualified accountants work remotely through cloud systems, running bookkeeping, GST, TDS, income tax, and compliance end to end. Unlike hiring an internal employee, you engage a professional team with defined roles and oversight at 50 to 70% lower cost than in-house staff, with an AI dashboard for visibility rather than do-it-yourself accounting.

Will my founders or finance heads need to post entries or manage reconciliations in the AI dashboard?

No, the AI dashboard exists for visibility and comfort, not for operational data entry. The CA team handles entries, reconciliations, reviews, and filings. Your leaders simply see status, trends, and reports, then approve or decide.

What does an "AI Accountant" deliver in practice?

AI Accountant delivers clean books, routine reconciliations, compliance calendars for GST and TDS, month-end statements, and decision-ready dashboards. Automation accelerates categorization and checks. Human experts review and finalize every period, with a CA signing off on compliance.

How do you ensure GST and TDS filings won't slip?

Filings sit on a compliance calendar with reminders and cutoffs. Reconciliations are scheduled weekly, then validated at month-end. The CA reviews mappings and returns, the AI dashboard shows filing status, and the team executes submissions and stores acknowledgements. With e-invoicing now mandatory above ₹1 crore turnover, IRN validation is built into the weekly check cycle (2026 update).

Which controls protect our data when everything is remote?

Encrypted cloud platforms (AES-256), role-based access, audit trails, and documented workflows protect data. Only authorized team members can view, edit, or approve. Changes are logged, and attachments live in a secure portal with traceable versions. ISO 27001 and SOC-2 Type II certifications validate these controls.

What do month-end deliverables include, and who signs off?

Month-end includes profit and loss, balance sheet, cash flow, bank and ledger reconciliations, and a variance note pack. The controller reviews and adjusts, the Chartered Accountant completes tax and compliance entries, then the CA signs off and publishes the dashboard pack within a few business days of cutoff.

How does virtual accounting compare to using just cloud accounting software?

Software is a tool; virtual accounting is expert service with accountability. Cloud software provides access and automation. The CA team ensures correct categorization, reconciliations, adjustments, and filings. You get disciplined processes and human oversight rather than a self-service system where errors compound unnoticed.