-01%201.svg)

Key takeaways

- Tax preparation for businesses in India is a continuous cycle covering GST, TDS, income tax, payroll, and ROC. Clean books and timely reconciliations prevent penalties that drain cash.

- Errors carry real costs: 18% interest on late GST, 1.5% per month on delayed TDS deposits, and blocked input tax credit from GSTR 2B mismatches that now trigger real time portal alerts.

- A structured monthly, quarterly, and annual compliance calendar turns unpredictable deadlines into manageable routines, reducing last minute scrambles and missed filings.

- Reconciliation is the backbone: GSTR 1 versus books, GSTR 2B versus ITC claimed, Form 26AS and AIS versus revenue, and bank or gateway statements versus ledger entries.

- Founders and finance teams who lack a dedicated CA partner or dashboard risk compounding penalties, blocked credits, and audit surprises. Virtual Accounting by AI Accountant solves this with a CA led team, automated reconciliations, and a live compliance dashboard so nothing slips.

- Act before quarter end: verify your compliance calendar against official portals, reconcile all pending months, and ensure vendor follow ups are complete to protect ITC eligibility.

Tax compliance rules for businesses: what's new in 2026

Several material changes from Budget 2026 and GST Council decisions reshape how businesses handle tax preparation this year. Here is what shifted and what it means for your daily workflow.

Until March 2025, the GST e invoicing threshold was ₹5 crore. From April 2025, it dropped to ₹2 crore, pulling a significantly larger pool of SMEs into the e invoicing net. If your turnover sits between ₹2 crore and ₹5 crore, you now need IRN generation infrastructure, HSN validation workflows, and a 24 hour cancellation tracking system that did not exist in your process last year. The presumptive tax limit under section 44AD rose to ₹3 crore (from ₹2 crore in 2025) for businesses with 95% or more digital receipts, and the Income Tax Department now auto flags mismatches via AIS 2.0.

The tax audit threshold moved to ₹12 crore (previously ₹10 crore) for businesses meeting the 95% digital receipts condition. This benefits mid sized firms but also demands cleaner digital records and bank reconciliations to qualify. For ROC filings, MCA's V3 portal now mandates fully digital submissions, so paper based statutory registers no longer suffice.

Cost of inaction is steep. Missing e invoicing compliance invites denial of ITC to your buyers, penalty exposure, and potential best judgment assessments. Late GST filings carry ₹200 per day (₹100 CGST plus ₹100 SGST) capped at 0.5% of turnover, as confirmed in the GST Council's 55th Meeting (February 2026). Ignoring AIS 2.0 mismatches leads to automated notices under the faceless assessment scheme.

What to do now:

- Confirm your e invoicing readiness if turnover exceeds ₹2 crore. Test IRN generation by June 30.

- Re evaluate whether 44AD presumptive taxation now applies given the ₹3 crore threshold.

- Reconcile AIS 2.0 data with your revenue ledgers before the July 31 ITR deadline.

A CA led Virtual Accounting service already configured for these 2026 workflows ensures your team does not scramble to adapt mid quarter.

Introduction to tax preparation for businesses

Tax preparation for businesses is a full cycle, not a one time filing exercise. You gather data, validate ledgers, compute taxes, and file returns on time, while monitoring cash flow and preventing penalties.

You manage GST, TDS, income tax, payroll TDS, and ROC filings. You keep evidence ready for audits and reviews. If you miss steps, you face interest, late fees, and credit blocks. Mismatches complicate filings and cash planning.

A CA led service with a live dashboard helps you see status clearly, reconcile faster, and stay compliant. For a deep dive on compliance context for foreign businesses operating in India, see the PwC India Tax Guide.

Why tax preparation for businesses matters

Tax preparation matters because every error hits cash. Late GST returns invite late fees of ₹200 per day. Short advance tax triggers interest under sections 234B and 234C at 1% per month. Mismatches between GSTR 1 and books can block input tax credit. Wrong TDS rates create notices and vendor friction.

It also anchors year end, audit readiness, and ROC filings. Companies crossing audit thresholds need schedules and reconciliations. Small companies file MGT 7 and AOC 4. Proprietors and professionals pick the correct ITR: ITR 3 or presumptive options like 44AD or 44ADA.

A CA led service with a smart dashboard automates reconciliations, tracks timelines, and flags risks early. This reduces penalty exposure by catching gaps before they compound.

Scope of tax preparation for businesses in India

GST compliance

GST begins with registration. Thresholds are ₹40 lakh in most states and ₹20 lakh in special category states (updated per Budget 2026). You file GSTR 1 for outward supplies. Monthly filers often file by the 11th of the next month.

You file GSTR 3B for summary and tax payment. Due dates fall between the 20th and 24th based on state and scheme. Annually, file GSTR 9 by December 31. If turnover exceeds ₹5 crore, prepare GSTR 9C reconciliation statement. GSTR 9 is optional for businesses below ₹2 crore turnover.

E invoicing now applies above ₹2 crore turnover (2026 update). Input tax credit is guided by GSTR 2B, with weekly and monthly updates and real time mismatch alerts on the GST portal. Place of supply follows IGST Act sections 10 to 13. Reverse charge applies under section 9 in specific cases. The right HSN or SAC code and tax rate are essential.

Exporters use LUT for zero rated supplies, with auto renewal now available via the portal. Good records make GST health checks simple.

TDS compliance

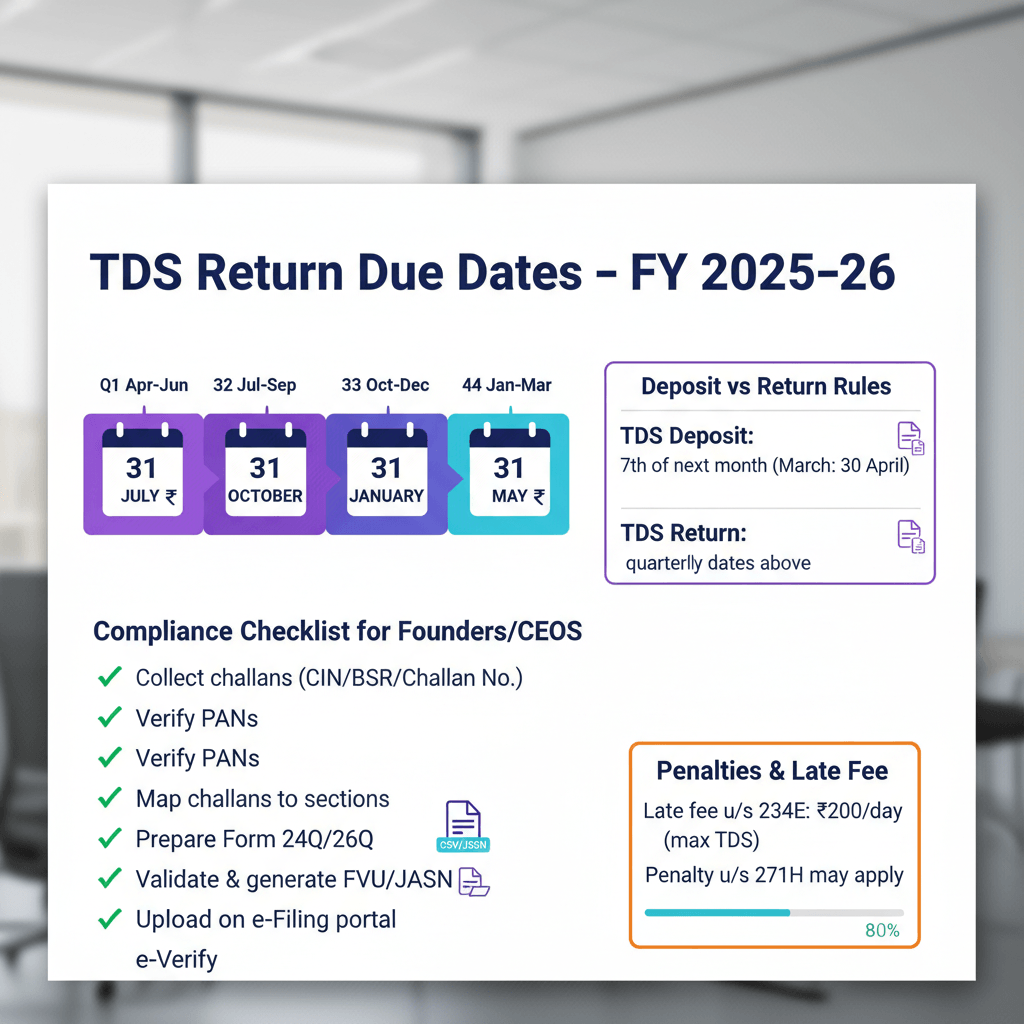

TDS covers salaries under section 192, contractors under section 194C, professionals under section 194J, and many other payments across rent, fees, and interest. Deduct at the right rate and deposit by the 7th of the next month.

File quarterly returns: Form 24Q for salary, Form 26Q for domestic non salary, Form 27Q for non residents. Due dates fall in July, October, January, and May depending on the quarter. Special TDS flows use forms like 26QB for property, 26QC for rent, and 26QD for certain fees. Then issue Form 16 and 16A by May 31.

Reconcile vendor credits with Form 26AS and AIS (now AIS 2.0 with enhanced PAN Aadhaar linkage). Track challans and file on time to avoid interest at 1.5% per month. For broader compliance context, review the Income Tax e Filing portal.

Income tax compliance

Match entities to ITR forms. Proprietors and professionals typically use ITR 3. Firms and LLPs use ITR 5. Companies use ITR 6. Advance tax is paid in four tranches: 15% by June 15, 45% by September 15, 75% by December 15, the balance by March 15.

For deductions, watch section 43B payment timing and section 32 depreciation schedules. Presumptive tax under section 44AD applies below ₹3 crore turnover (2026 update, up from ₹2 crore) with deemed profit at 6% to 8%. Section 44ADA covers professionals below ₹75 lakh.

Tax audit applies if turnover exceeds ₹12 crore, subject to the condition that 95% or more of receipts and payments are digital (2026 update). Close books early, reconcile thoroughly, and prepare audit schedules well before deadlines.

Payroll tasks

Each month compute TDS on salaries. Structure components to optimize eligible exemptions and deductions like HRA and LTA where allowed. Maintain PF and ESI records. Preserve payslips and proofs.

A clean payroll process supports employee trust and tax compliance. ESOP perquisites are now auto reported in AIS 2.0, so ensure vesting and exercise records match what the department sees.

ROC filings for small companies

Small companies file MGT 7 for annual returns and AOC 4 for financial statements. DIR 3 KYC is due by May 30 for directors. Maintain board meeting minutes, manage MSME 1 filings half yearly for vendors, and handle event based filings for director changes or share capital changes.

A small company means turnover less than ₹100 crore, paid up share capital less than ₹10 crore, and not a holding or subsidiary. Keep statutory registers and an annual report ready. All filings are now mandatory via MCA's V3 digital portal. Refer to MCA's official portal for the latest forms and due dates.

Compliance calendar for tax preparation for businesses

Monthly tasks

- File GSTR 3B between the 20th and 24th as per state and category. File GSTR 1 per your regime.

- Deposit TDS by the 7th of the next month.

- Update sales, purchase, and expense books. Reconcile bank and payment gateways.

- Match input tax credit with GSTR 2B. Follow up with vendors to prevent blocked credit.

- Review alerts and anomalies. Fix exceptions promptly.

Quarterly tasks

- File TDS returns on due dates in July, October, January, and May as specified.

- Review tax provisions and estimates. Adjust based on performance.

- For QRMP scheme filers (now extended to more categories in 2026), file GSTR 1 by the 13th. Clean ledgers and fix old balances.

Annual tasks

- File GSTR 9 by December 31. Prepare GSTR 9C if turnover exceeds ₹5 crore.

- File ITR by July 31 for non audit cases and by October 31 for audit cases, or as notified.

- Complete ROC filings in October and November for small companies.

- Finalize advance tax by March. Close the year and prepare audit working papers.

Always verify the latest dates on official portals before filing. Timelines can change. Check gst.gov.in and incometax.gov.in for current notifications.

Data and documents checklist for tax preparation for businesses

Registrations

- PAN

- TAN

- GSTIN

- E invoice enablement status and ID

Financial records

- Sales and purchase registers

- Sales invoices and expense bills (vendor invoices)

- Bank statements and payment gateway statements

- Trial balance and general ledger (all ledger entries)

- Accounts receivable and accounts payable aging

Assets and inventory

- Fixed asset register

- Depreciation schedule (section 32 rates)

- Inventory reconciliations and stock movements

Payroll

- Salary sheets

- PF and ESI records

- TDS proofs and challans

Tax documents

- GSTR 2B for input tax credit verification

- Form 26AS and AIS 2.0 for income tax credits

- Prior year ITR copies

- LUT for exports if used

Other items

- Contracts and agreements

- HSN and SAC codes with rate notes

- Place of supply determinations

- RCM notes and vendor declarations

Store documents in a clean digital repository. Use simple file names. Keep a central dashboard for status tracking. The GSTN e Vault and compliant digital storage under IT Act 2000 amendments are useful references.

Step by step process for tax preparation for businesses

Bookkeeping and ledgers

- Post monthly entries for sales, purchases, and expenses (transaction posting).

- Reconcile bank and payment gateways.

- Prepare cash flow statements for internal visibility.

- Close the year with a clean profit and loss and balance sheet.

- Update AR and AP aging.

- Scrutinize ledgers. Clear old balances and suspense entries.

GST preparation

- Verify HSN or SAC, tax rates, and place of supply for each sale and purchase.

- Reconcile input tax credit with GSTR 2B.

- Compute reverse charge where applicable.

- Validate e invoices (mandatory above ₹2 crore) and LUT if relevant.

- File GSTR 1 and GSTR 3B.

- Prepare annual GSTR 9 and GSTR 9C if eligible.

TDS preparation

- Map vendors and payments to correct sections and rates.

- Deduct TDS on time.

- Deposit TDS challans monthly by the 7th.

- File returns 24Q, 26Q, and 27Q quarterly.

- Issue Form 16 and Form 16A by May 31.

- Use 26QB, 26QC, and 26QD for special cases.

Income tax computation

- Finalize financials and schedules.

- Apply depreciation as per section 32.

- Check section 43B payment timing for allowed deductions.

- Assess presumptive options under section 44AD (below ₹3 crore) or 44ADA (below ₹75 lakh) if eligible.

- Compute and pay advance tax in four instalments.

- Prepare ITR 3 or ITR 5 or ITR 6 based on entity.

- Prepare tax audit data if turnover limits and conditions apply (₹12 crore with digital receipts condition).

Payroll tasks

- Calculate monthly TDS on salaries.

- Structure salary to help employees save tax within the law.

- Maintain proofs and records for payroll components.

ROC filings

- Draft and file MGT 7 and AOC 4 via MCA V3 portal.

- Complete DIR 3 KYC by May 30.

- Keep board minutes and statutory registers current.

- File event based changes on time.

A CA team using a smart dashboard can run this flow end to end. Every step stays visible and on track when you have a live compliance view with automated alerts.

Industry specific nuances in tax preparation for businesses

Startups, SaaS, and exporters

Exports are zero rated. Use LUT to avoid paying IGST upfront. For digital services, study OIDAR rules for place of supply. Foreign remittances may need Form 15CA and 15CB.

Track forex invoices and realization. Document contract terms clearly. Section 195 withholding applies to payments to non residents, and treaty positions must be checked before remittance.

E commerce sellers and marketplaces

Marketplaces collect TCS under section 52. Payment gateways settle net of fees and TCS. Reconcile marketplace statements, gateway fees, and bank entries monthly.

Map HSN codes and tax rates per product line. Align returns with reconciled numbers. This reconciliation between marketplace data, gateway settlements, and bank credits is often the most error prone step.

Freelancers and independent professionals

If annual service income crosses ₹20 lakh, GST registration is required. Consider presumptive tax under 44ADA for eligible professions below ₹75 lakh. Maintain clean invoicing and books. Claim input tax credit where allowed and supported by GSTR 2B.

Common mistakes in tax preparation for businesses and how to avoid them

- Mismatch between GSTR 1 and books: Reconcile monthly. Fix errors before filing. Use a reconciliation engine that flags gaps between your sales register and filed GSTR 1.

- Mismatch between ITC and GSTR 2B: Claim only what appears in GSTR 2B. Monitor vendor filing status. Follow up systematically. The portal now sends real time alerts for mismatches.

- Late TDS deposits: Interest at 1.5% per month applies from the date of deduction. Set reminders for the 7th. Track challans with a workflow.

- Missing advance tax installments: Compute quarterly. Use rolling forecasts. Book provisions to stay current. Interest under 234B and 234C compounds quickly.

- Wrong place of supply or RCM errors: Document each case. Track RCM for services like legal or freight when applicable. Update vendor notes.

- Poor record keeping: Scattered records drive errors. Keep a central digital store and a dashboard with dates and proofs.

- Skipped bank reconciliations: Unreconciled accounts hide cash flow issues. Reconcile banks and gateways monthly. Monitor anomalies and alerts.

- Ignoring AIS 2.0 data: The enhanced Annual Information Statement now flags high value transactions automatically. Reconcile AIS with your revenue ledgers quarterly to avoid surprise notices.

Technology enabled tax preparation for businesses with virtual accounting

Outsourced tax preparation works best with strong systems. A CA led managed service brings execution, advisory, and compliance together. A centralized dashboard shows live accounting data, compliance timelines, documents, and insights. You get AI powered anomaly alerts, auto reconciliations, and a clear view of filings and their status.

Leading tools and platforms that support this workflow include:

- AI Accountant

- QuickBooks Online

- Xero

- TallyPrime

- FreshBooks

- Sage Business Cloud Accounting

Combine a CA led workflow with smart software. You get fewer errors, faster closings, and predictable outcomes.

For perspectives on how technology reduces compliance effort, see Deloitte India's 2026 Tax Tech insights.

Actionable checklist for tax preparation for businesses

Monthly checklist

- Update books for all sales, purchases, and expenses.

- Reconcile bank accounts and payment gateways.

- Match input tax credit with GSTR 2B.

- Prepare and file GSTR 1 and GSTR 3B on time.

- Deduct and deposit TDS by the 7th.

- Review alerts and fix anomalies.

Quarterly checklist

- File TDS returns 24Q, 26Q, and 27Q.

- Review tax provisions and adjust estimates.

- Clean ledgers. Clear old balances and suspense items.

Annual checklist

- Finalize financial statements and schedules.

- Compute depreciation and check section 43B payments.

- Prepare ITR 3 or ITR 5 or ITR 6 as applicable.

- File GSTR 9 and prepare GSTR 9C if eligible.

- Complete ROC filings MGT 7 and AOC 4 for small companies.

- Prepare audit data if turnover crosses limits.

This checklist keeps tax preparation simple and clear. Use a dashboard to tick tasks and store proofs.

Closing thoughts on tax preparation for businesses

Break the work into steps. Keep clean books. Reconcile often. File on time. Use a CA led service and a dashboard for visibility. Use technology to reduce manual effort.

With a disciplined process, you protect cash flow and reduce compliance stress. The combination of qualified professionals and automation turns tax preparation from a year end scramble into a predictable, manageable routine.

FAQ

What monthly controls should a founder mandate to prevent GST and TDS penalties?

Mandate five controls: bank and gateway reconciliations completed by the fifth business day, GSTR 1 and 3B prepared by the eighth, TDS challans deposited by the seventh, GSTR 2B versus ITC reconciliation completed before filing, and a compliance review call to sign off. A standardized cadence with dashboards, alerts, and evidence packs ensures nothing slips.

How do we design a compliance calendar for multiple GST registrations across states?

Create a master calendar with entity wise and state wise slices. Map GSTR 1 and 3B due dates per regime, tag e invoicing thresholds (now ₹2 crore, 2026 update), and assign ownership per registration. State wise statuses, filings, and pending actions should be visible at a glance in a centralized dashboard.

What are the core deliverables in a CA led Virtual Accounting engagement?

Typical deliverables include monthly bookkeeping and reconciliations, GST filings with ITC reconciliation packs, TDS deposits and quarterly returns with challan mapping, management reports, income tax computation and ITR, payroll TDS and proofs, and ROC annual filings for small companies. Additional deliverables often include anomaly alerts, a document vault, and audit ready schedules.

How should e invoicing, IRN cancellations, and credit notes be handled to keep GSTR 1 clean?

Validate HSN and tax rates before IRN generation. Track the 24 hour IRN cancellation window closely. Issue credit notes with correct references so GSTR 1 reflects adjustments properly. Reconcile outward supplies with books monthly to prevent downstream mismatches in 3B and GSTR 9.

Which reconciliation packs should a CFO request every month?

Request five packs monthly: GSTR 2B versus ITC with vendor compliance status, GSTR 1 versus sales register, Form 26AS and AIS 2.0 versus revenue recognition (2026 update), bank and gateway reconciliations, and AR or AP aging with exception notes. Automated reconciliation surfaces exceptions so the CFO reviews only outliers.

When should a proprietor or freelancer pick presumptive 44ADA or 44AD instead of normal books?

Pick presumptive when turnover fits the threshold (₹3 crore for 44AD with 95% digital receipts, ₹75 lakh for 44ADA, 2026 update) and the simplicity trade off outweighs the benefits of detailed expense tracking. Model tax outflows both ways, and consider future loan or investor diligence needs where detailed books may be preferred.

What is the current tax audit threshold for businesses in India?

The tax audit threshold is ₹12 crore for businesses where 95% or more of total receipts and payments are through digital or banking channels (2026 update). If cash transactions exceed 5% of receipts or payments, the older ₹1 crore threshold applies. Verify your digital receipts percentage before assuming the higher limit applies.