-01%201.svg)

Key takeaways

- SOX-style controls in India, aligned with IFC and ICFR, drive real outcomes, faster closes, fewer audit observations, cleaner data, stronger decisions.

- Focus on risks that matter, GST, TDS, vendor onboarding, multi ERP realities, design controls for Indian context, not copy paste US models.

- Build a disciplined reconciliation calendar, daily for banks, weekly for high volume, monthly for statutory, assign owners, require evidence, automate exceptions.

- Implement segregation of duties in small teams using compensating controls, detailed reviews, audit logs, role based access, responsibility rotation.

- Test design and operating effectiveness with walkthroughs, sampling, analytics, and exception reports, maintain a strong evidence pack using audit readiness and evidence pack.

- Classify deficiencies, remediate with root cause analysis, track closure, retest, report to stakeholders, embed continuous improvement.

- Use automation and tools like AI Accountant to embed controls, reconcile at scale, enforce access, create audit trails, and monitor in real time.

Introduction

SOX-style controls in India are no longer just for listed companies, they are essential for businesses across sizes due to IFC and ICFR obligations under the Companies Act 2013, SEBI LODR expectations, and auditor focus on reliable reporting. The modern shift, controls are not a checkbox, they are an operating system for finance, delivering clean data, faster closes, fewer audit observations, and better decision making.

If you are a CFO, Controller, or CA partner working with Indian SMEs and mid market firms, this practical blueprint lays out objectives, reconciliations, segregation of duties, testing, and remediation strategies, designed to work without increasing headcount. Controls become the backbone for disciplined, repeatable finance operations.

What “SOX-Style” Means in the Indian Context

Understanding the foundation

The US Sarbanes Oxley Act Section 404 focuses on Internal Controls over Financial Reporting, design and operating effectiveness to prevent material misstatements. India mirrors this intent through IFC and ICFR under the Companies Act 2013, embedding risk based controls supporting assertions like completeness, accuracy, existence, occurrence, cutoff, authorization, classification, and compliance.

Further reading, Sarbanes Oxley compliance overview, Internal controls for SOX compliance, Common types and implementation tips.

India specific challenges

- GST compliance, monthly GSTR 2B versus purchase register matching, input tax credit validation, e way bill checks.

- TDS and TCS filings, quarterly returns, certificate tracking, variable rates across payment types.

- Vendor onboarding realities, cash preferences, GSTIN verification difficulty, invoice and registration address mismatches.

- Multi ERP environments, Zoho Books and Tally combinations, master data standardization becomes critical.

You cannot copy paste US SOX, controls must reflect Indian risks, materiality, and operational realities.

Further reading, SOX compliance overview, SOX controls white paper.

Control Objectives

Core objectives that matter

- Completeness, every transaction captured, no missing invoices, no unrecorded expenses.

- Accuracy, amounts correct, GST calculations align, TDS deductions right.

- Existence and occurrence, transactions are real, no fictitious entries, no duplicates.

- Cutoff, recorded in the correct period, March does not slip into April.

- Authorization, approvals consistent with delegation matrices.

- Classification, accounts are appropriate, capital versus revenue is correct.

- Compliance, GST returns timely, TDS deposited by the seventh, regulatory obligations met.

Mapping to Indian business cycles

Procure to Pay

- Verify GST input credit eligibility before booking.

- Match vendor master GSTIN with invoice details.

- Evidence in place, three way match, signed GRNs, vendor confirmations.

Order to Cash

- Validate customer invoicing against contracts.

- Track TDS certificates received from customers.

- Monitor collection aging and follow ups.

- Evidence in place, balance confirmations, signed delivery receipts, collection logs.

Record to Report

- Enforce journal entry approval workflows.

- Standardize month-end close checklists.

- Evidence in place, signed reconciliations, supporting calculations, disclosure reviews.

Treasury and cash management

- Daily bank reconciliation requirements.

- Cash position tracking and forecasting.

- Evidence in place, bank statements, payment logs, investment schedules.

Further reading, SOX compliance overview, Common types and implementation tips, SOX controls white paper, Internal controls for SOX compliance.

Key Reconciliations

The reconciliation calendar that works

Daily

- Bank statements for all operating accounts.

- Cash book to physical cash.

- Collection reports to bank credits.

Weekly

- Credit card statements.

- Vendor payment runs to bank debits.

- Customer receipts to sales ledger.

Monthly

- GST 2B to purchase register, GSTR 1 to sales register.

- Vendor statements and customer balance confirmations.

- GR versus IR matching.

- Intercompany account matching.

- TDS payment challans to ledgers.

- Advance payments to GRNs.

- Expense accruals to support.

Making reconciliations stick

Assign owners, purchase manager for vendors, credit controller for customers, tax team for GST, require hard evidence, stamped bank statements, ERP aging reports, signed reviews, automate exception identification so humans focus on high value investigation.

Common Indian pitfalls to avoid

- GSTIN mismatches, vendors change registration silently, run monthly GSTIN validation against government databases.

- Tally rounding differences, standardize report formats and calculations to remove noise.

- Manual fatigue, automate bulk matching, review only exceptions.

Further reading, Internal controls for SOX compliance, SOX compliance overview, Common types and implementation tips.

Segregation of Duties

Why segregation matters

Segregation of duties reduces fraud and error, no single person controls an end to end process, vendor creation should not coexist with payment approval, entry creation should not coexist with entry approval. When overlaps are unavoidable, compensating controls fill the gap.

High risk conflicts

Vendor management

- Creating new vendors versus approving vendor payments.

- Editing vendor bank details versus processing payment files.

- Recording purchase bills versus modifying vendor master data.

Financial recording

- Creating journal entries versus approving them.

- Preparing reconciliations versus reviewing them.

- Posting transactions versus modifying posted entries.

Revenue cycle

- Creating sales invoices versus issuing credit notes.

- Recording customer receipts versus writing off balances.

- Modifying credit limits versus approving sales orders.

Practical solutions for small teams

- Implement detailed reviews with documentation when separation is impossible.

- Maintain comprehensive audit logs, review weekly for anomalies.

- Rotate responsibilities quarterly, reduce long term concealment risk.

- Use Zoho Books and Tally role based access, maker checker approvals for payments, dual approval thresholds for large entries.

Further reading, SOX compliance overview, SOX compliance guide, Common types and implementation tips.

Control Testing

Design versus operating effectiveness

Design effectiveness asks whether a control can mitigate the risk, operating effectiveness asks whether it works consistently. Both matter, both require evidence.

Testing methods that work

- Walkthroughs, trace a transaction through the process, document actors and evidence.

- Sampling, select items across a period, validate approvals and support, look for patterns.

- Analytics, scan for duplicates, weekend postings, vendors with multiple GST numbers.

- Exception reports, list manual entries above materiality, vendor master changes, backdated transactions.

Building your evidence trail

Strong evidence makes audits smooth, organized packs reduce friction, accelerate closure.

- Approval controls, dated signatures, email approvals, system timestamps.

- Reconciliation controls, completed templates, reviewer sign offs, attached support.

- Access controls, user access reports, change logs, periodic reviews.

- Compliance controls, GST acknowledgments, TDS certificates, challans.

Automation advantages

Move from periodic testing to continuous monitoring, leverage ERP change logs, dashboards, real time alerts, reduce effort and strengthen control reliability.

Automation surfaces issues now, not after the audit.

Further reading, SOX readiness, Internal controls for SOX compliance, SOX compliance overview.

Remediation Steps

Triaging control deficiencies

- Minor, isolated misses, fix and move.

- Significant, systematic gaps, redesign or train.

- Material, threaten integrity, immediate executive attention and comprehensive remediation.

Root cause analysis

- Process gaps, redesign with clear steps and owners.

- Training issues, job aids and targeted sessions.

- System limitations, compensating controls or automation investment.

- Resource constraints, automate routine tasks to free capacity.

Building your remediation plan

- Issue description and classification.

- Root cause findings.

- Specific remediation actions.

- Owner, due date, retesting plan.

- Status tracking and stakeholder reporting.

Continuous improvement mindset

Quarterly control reviews, rotation of tests, monitoring of emerging risks, demonstrate maturity and resilience, prevent small issues from becoming material weaknesses.

Further reading, Common types and implementation tips, Internal controls for SOX compliance, SOX readiness.

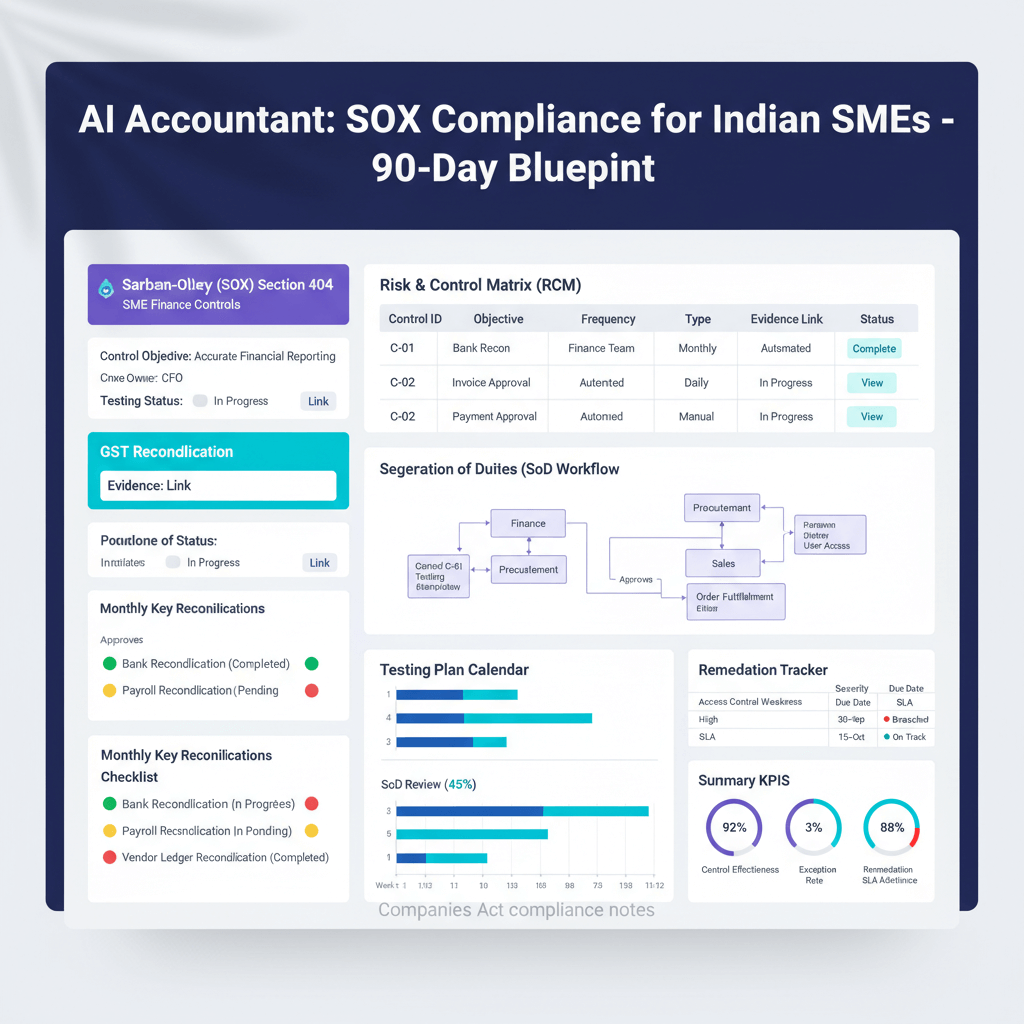

A 90-Day Roadmap to Operationalize SOX-Style Controls in India

Days 0 to 30, foundation setting

- Week 1 to 2, risk assessment, map material accounts and processes, revenue recognition, inventory valuation, GST compliance.

- Week 2 to 3, control matrix, document existing controls, identify gaps, prioritize by materiality and likelihood.

- Week 3 to 4, control objectives, set measurable targets, invoice recording timeliness, bank reconciliation timelines.

- Week 4, baseline, document current reconciliations, map segregation, quick wins.

Days 31 to 60, implementation phase

- Week 5 to 6, approval workflows, amount based matrices, ERP configuration, training.

- Week 6 to 7, reconciliation templates, standardize formats, review checkpoints, central repository.

- Week 7 to 8, high risk testing, test controls in highest risk areas, quick fixes for gaps.

- Week 8, communication and training, explain why controls matter, share early wins.

Days 61 to 90, optimization and embedding

- Week 9 to 10, automation, repetitive reconciliations, exception reporting, dashboards.

- Week 10 to 11, remediation playbook, standard procedures, escalation, tracking.

- Week 11 to 12, governance, controls committee, review frequencies, reporting templates.

- Week 12, continuous monitoring, automated alerts, quarterly cycles.

Further reading, SOX readiness, Common types and implementation tips, Internal controls for SOX compliance.

Technology Enablement

How automation embeds controls

- Bulk bill validation, catch GSTIN mismatches before posting, match totals to POs, flag duplicates instantly.

- Transaction mapping, consistent mapping rules, reduce manual effort, improve classification quality.

- GST reconciliation workflows, match thousands of invoices in minutes, investigate exceptions quickly.

- Access control enforcement, prevent segregation violations, route approvals automatically.

- Evidence trail creation, unalterable logs, timestamp and user detail, audit ready with minimal effort.

Integration with Indian ERPs

Zoho Books and Tally integrations support real time sync, master data consistency, batch processing, standardized import and export routines, high volume handling.

Tools for control automation

- AI Accountant, automates bill processing, bank reconciliation, GST matching, embeds control frameworks, integrates with Zoho Books and Tally, purpose built for Indian SMEs.

- QuickBooks Online, approval workflows and audit trails, GST adaptation may be required.

- Xero, strong reconciliations and access controls, growing Indian compliance support.

- FreshBooks, automated expense tracking and approval routing for smaller teams.

- Sage Business Cloud, comprehensive control features with Indian localization.

Real time monitoring benefits

- Continuous Control Monitoring, alerts for unusual entries, stop segregation violations before posting.

- Dashboard visibility, CFO views daily reconciliation status, controllers track exceptions, auditors access evidence remotely.

- Predictive analytics, pattern detection for risky vendor payments, anomaly detection for early fraud signals.

Further reading, Internal controls for SOX compliance, SOX compliance overview.

Case Vignette, a success story

The challenge

A mid sized Indian manufacturing SME at Rs two hundred crore revenue suffered recurring audit observations, late reconciliations, missing approvals, GST mismatches leading to input credit losses. An eight member finance team handled multiple units and systems, Zoho Books centrally, Tally at plants, Excel dominated processes.

The transformation

- Process standardization, clear control objectives across P2P and O2C, SOPs for key processes, documented evidence requirements.

- Reconciliation discipline, weekly bank reconciliations, standardized vendor and GST templates, clear ownership with backups.

- Segregation, vendor creation separated from payment processing, maker checker approvals above thresholds, detective compensating controls.

- Quarterly testing rhythm, risk based sampling, full annual coverage, documented findings and remediation.

- Technology integration, automated bank ingestion, GST bulk matching, dashboards for reconciliation status.

The results

- Four day faster close, continuous reconciliations reduce adjustments, management reports by day five instead of day nine.

- Sixty percent fewer audit observations, external audit friction drops, internal audit shifts to value add.

- Zero GST credit losses, timely reconciliation catches issues early, vendors correct invoices before filing deadlines.

- Improved team morale, automation removes repetitive drudgery, focus moves to analysis.

Further reading, Common types and implementation tips.

Common Pitfalls and How to Avoid Them

Over documentation without clear objectives

Hundred page manuals that nobody uses are a trap, start from risk, document only what is needed for operation and testing, use job aids anchored to specific risks.

Ignoring segregation in small teams

Trust is not a control, add compensating reviews, audit logs, rotation, system enforced separation where feasible.

Leaving reconciliations for month end

Month end pile ups cause errors, move to continuous cadence, daily banks, weekly high volume accounts, automate matching, chase exceptions only.

Weak evidence and documentation

Without evidence, auditors assume controls fail, standardize requirements, use timestamps, signatures, store support with reconciliations.

Testing without remediation

Findings must close, track to completion, retest after fixes, report progress, make remediation part of KPIs.

Assuming technology solves everything

Design controls first, then automate, maintain oversight, test automated controls, keep manual backups for continuity.

Further reading, Common types and implementation tips, SOX compliance guide, Internal controls for SOX compliance, SOX compliance overview.

Practical Templates and Checklists

Control objectives matrix

- Process, objective, activity, control type, frequency, evidence, owner, testing method.

Key reconciliations calendar

- Name, frequency, due date, owner, backup, review required, reviewer, evidence location, status.

Segregation of duties conflict matrix

- Roles across top, tasks down side, mark incompatibilities, highlight conflicts, document compensating controls.

Control testing plan

- Name and description, frequency, sample size, selection method, procedures, evidence, pass or fail criteria, documentation.

Remediation tracker

- Reference, date, area, description, severity, root cause, actions, owner, due dates, status, retesting, closure.

Monthly controls dashboard

- On time reconciliations, pass rate, open remediation by age, segregation violations, manual entries needing review, exception volumes, days to close trend, audit observations trend.

Next Steps

Taking action

SOX-style controls in India deliver compliance and performance, clear objectives, disciplined reconciliations, pragmatic segregation, risk based testing, structured remediation, create a resilient control environment.

Start your assessment today

Identify biggest gaps, reconciliation discipline, segregation, evidence quality, implement quick wins now, daily bank reconciliations, vendor master reviews, approval matrices, prioritize automation for GST matching, bank statement ingestion, journal entry workflows.

Explore automation

Modern tools integrated with Zoho Books and Tally accelerate maturity, automated reconciliation, embedded segregation, continuous monitoring, real time dashboards, consider AI Accountant for India specific control automation needs.

Get expert guidance

Industry, size, and complexity define unique needs, engage experts who blend global best practices with Indian realities, progress compounds once you begin, start where you are, use what you have, do what you can.

FAQ

How should a CA structure an IFC control matrix for an SME with Zoho Books and Tally, what columns are mandatory for audit reliance?

Build a risk based matrix, include process, control objective, specific control activity, control type, frequency, evidence required, control owner, and testing method. For mixed ERPs, add system of record per control, for example Zoho Books for P2P approvals, Tally for plant billing. Use AI Accountant to generate standardized templates and attach evidence automatically.

What sample size should I use for operating effectiveness testing of approvals, can I adopt a fixed 25 item sample each quarter?

Use risk based sampling, consider volume, materiality, and control frequency. For high volume AP approvals, a 25 item quarterly sample can be a baseline, increase when exception rates rise. Analytics driven stratified sampling through AI Accountant improves coverage by focusing on higher risk attributes, for example weekend postings, backdated entries.

How do I evidence maker checker for payments without adding headcount, any compensating controls auditors accept?

Configure role based access in Zoho Books and Tally, route payment approvals to a second approver for amounts above thresholds. Where separation is impossible, require detailed post payment reviews with sign off, weekly audit log reviews, and periodic rotation of reviewers. AI Accountant can enforce workflow rules and produce tamper evident audit logs.

What is the most efficient way to reconcile GSTR 2B to purchase register monthly, how do I handle exceptions at scale?

Automate ingestion of 2B data, standardize vendor GSTIN master, run matching rules for invoice number, GSTIN, taxable value, tax amounts, flag exceptions for investigation. Use exception queues, vendor outreach templates, and roll forward unresolved items. AI Accountant matches thousands of lines in minutes and tracks resolution history for audit trails.

How do I document completeness for revenue, is a contract to invoice linkage sufficient for auditors?

Completeness requires controls that ensure all billable events are invoiced, use contract master linkage, dispatch or delivery evidence, and periodic reconciliation of dispatch logs to invoices. Add customer balance confirmations. Auditors look for design plus evidence, use system timestamps and reports. AI Accountant can generate completeness analytics and exception reports.

What compensating controls are acceptable when the same person posts and approves journal entries during month end?

Require detailed review by a different person, include rationale, support, and risk flags for entries above a threshold, run analytics to detect unusual entries, weekends, large round amounts, duplicate descriptions. Maintain an approval trail with timestamps. AI Accountant automates exception detection and reviewer assignment.

For TDS compliance, how do I ensure accuracy of rates across payment types, and evidence this for statutory audit?

Maintain a TDS rate matrix tied to vendor category and payment nature, enforce in ERP using validation rules, run monthly exception reports highlighting deviations, reconcile challans to ledgers, store certificates. Provide the matrix, exceptions, and reconciliations in your audit pack. AI Accountant can apply rules engine validation and compile evidence automatically.

Can continuous control monitoring replace quarterly testing, how do I justify this change to the audit committee?

CCM enhances coverage, it does not eliminate independent testing, propose a hybrid, continuous monitoring for high risk controls, quarterly targeted testing for assurance. Show metrics, exception rates, remediation timelines, and improved close speed. AI Accountant dashboards provide real time visibility and trend analytics for committee reporting.

How should I classify control deficiencies, and when does a segregation issue become a material weakness?

Classify as minor, significant, or material, based on likelihood and impact. A segregation issue is material when it enables unauthorized transactions across critical processes, for example the same person creating vendors and executing payments, without compensating oversight. Document root causes and remediation, retest, and report progress.

What evidence pack do auditors prefer for reconciliations, can I rely on electronic signatures and system timestamps?

Auditors accept electronic signatures and system timestamps when controls ensure authenticity and completeness, include completed templates, reviewer attestations, source documents, and exception resolution notes. Use a centralized repository, indexed by account and month. The AI Accountant audit readiness and evidence pack framework standardizes this.

How do I design approval thresholds for AP and AR that balance risk and speed, any recommended amounts for Indian mid market?

Use tiered thresholds tied to risk and volume, for example AP, up to Rs fifty thousand, single approver, Rs fifty thousand to five lakhs, dual approver, above five lakhs, finance head plus budget owner. AR credit notes should always require controller review. Calibrate to your materiality and fraud risk, monitor exception rates, adjust quarterly. AI Accountant enforces dynamic routing.

What analytics are most useful to detect control failures quickly, beyond duplicate payments?

Weekend postings, backdated transactions, large round amounts, unusual vendors, multiple GSTINs per vendor, rapid changes in vendor bank details, recurring manual journals to the same accounts, aging buckets with stagnant balances. Set alerts for spikes and thresholds. AI Accountant provides outlier detection and configurable alerts.

How can a CA firm operationalize this framework across multiple clients without heavy overhead?

Standardize templates, control matrices, reconciliation calendars, and evidence packs, build a playbook, automate ingestion and matching, centralize dashboards per client, schedule quarterly reviews. Use AI Accountant to scale rule application and exception handling across Zoho Books and Tally portfolios.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.