-01%201.svg)

Key takeaways

- Deliver a disciplined Day 5 close consistently, use clear cut-off rules, a rigorous reconciliation checklist, a maker-checker workflow, and proactive client communication.

- Apply India-specific compliance rules for GST, TDS, e-invoicing, GRN based recognition, and RCM, accuracy here prevents penalties and audit issues.

- Build a structured close package, include trial balance, reconciliations, journals, variance analysis, ageing reports, an exception log, and a compliance checklist.

- Adopt automation to reduce manual effort, tools like AI Accountant bring GST and TDS aware reconciliation, dashboards, and posting flows.

- Run a monthly retrospective, maintain an improvement log with owners and due dates, track KPIs such as days to close, exceptions per close, unreconciled entries, and on-time client submissions.

- Protect control and compliance with audit trails, digital sign-offs, segregation of duties, and seven-year retention of close packages.

Understanding Monthly Close Service in the Indian Context

The monthly close service is a systematic end-of-month procedure, teams review all activity and finalize accurate financial statements that support quarterly and year-end closes. In India, you navigate GST, TDS, e-invoicing, and multiple systems, each piece must align cleanly or you invite penalties, interest, and audit exposure.

For Indian businesses, the monthly close delivers four outcomes: compliance clarity with GST, TDS, and e-invoicing, cash visibility across accounts and obligations, decision-ready numbers for management, and audit readiness with documentation and clear trails.

When the process is consistent, transparency improves, investors gain confidence, and statutory deadlines stop being a monthly scramble.

Why Monthly Close Service India Matters for Your Business

Indian entities juggle GSTR-1 filing, GSTR-2B matching, IRN tracking, TDS withholding and challans, and multi-account banking with UPI settlement. Missing a deadline or mismatch quickly converts into interest, penalties, and compliance headaches.

A disciplined monthly close brings clean books by Day 5 or Day 7, fewer surprises, sharper cash insight, and smoother audits. No guesswork, just clear, compliant records your leadership can trust.

Core Components of Monthly Close Service

- Trial Balance, complete ledger balances with supporting detail.

- Close Package, trial balance, reconciliations, journal entries, and exceptions in one organized bundle.

- Cash Dashboard, bank balances, deposits in transit, unpresented cheques, cash runway.

- Variance Analysis, month-on-month and budget versus actual with explanations.

- AR/AP Ageing, collection and payment plans on overdue items.

- Exception Log, unreconciled entries, missing docs, items needing follow-up.

- Compliance Checklist, GST, TDS, e-invoice, e-way bill status confirmed.

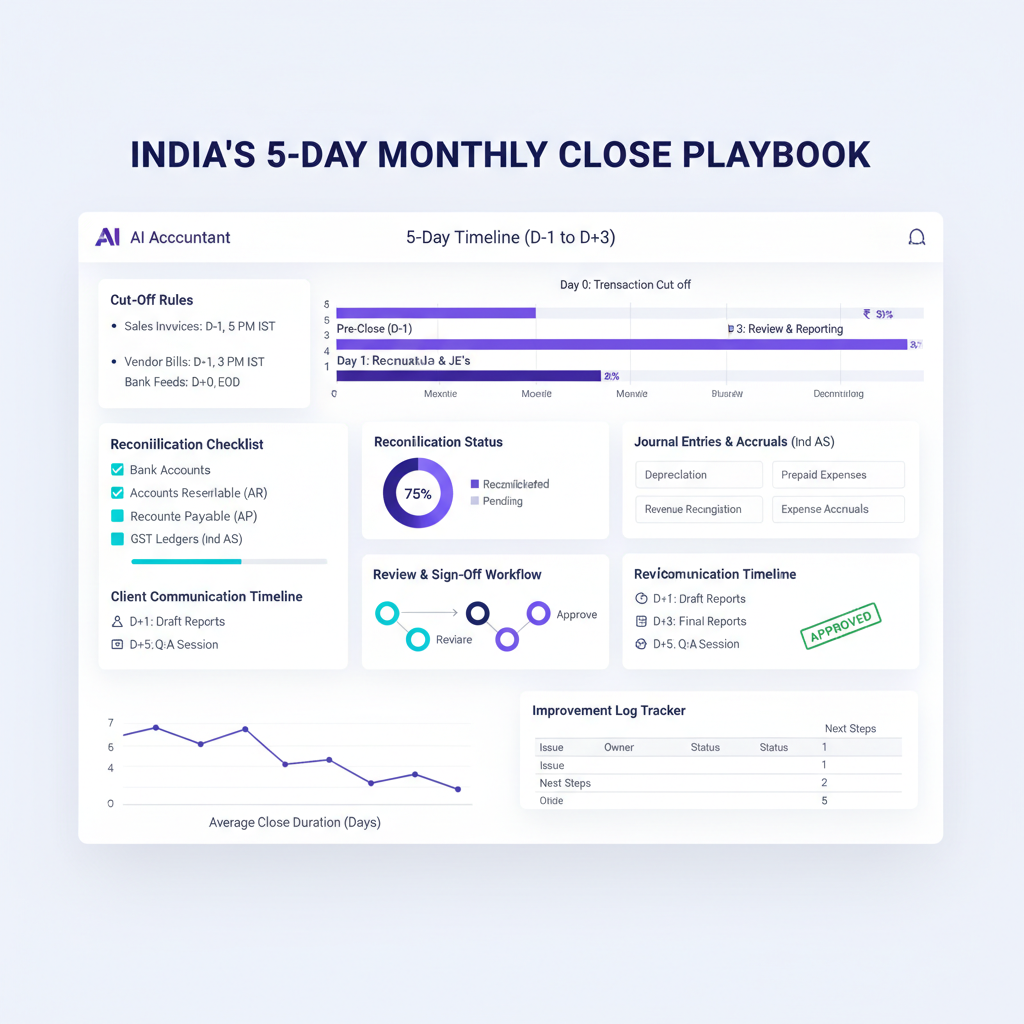

Setting Your Monthly Close Calendar

Align to India’s statutory rhythm. Start a pre-close window three days before month-end, send vendor reminders and cut-off rules. On Day 0, enforce cut-off strictly, pull final bank statements, lock prior-month entries.

- Days 1-2, bank reconciliation for all accounts, AR ageing, TDS certificate collection status.

- Days 2-3, AP reconciliation, GRN versus invoice matching, RCM verification, GSTR-2B reconciliation.

- Days 3-4, accruals for payroll, interest, depreciation, prepaid allocations, fixed asset reconciliation.

- Days 4-5, verify GSTR-1 cutoff, reconcile TDS deductions to challans, complete reviews.

- Day 5, senior review and sign-off.

- Days 6-7, post-close communication, report delivery, improvement log update, retrospective scheduling.

This timeline aligns cleanly with GST-3B filing cycles, auditors get what they need, leadership gets numbers on time.

Implementing Cut-Off Rules for Accurate Monthly Close

Sales and Revenue Recognition Cut-Off Rules

Recognize revenue when the e-invoice is generated and goods or services are delivered, not when payment arrives. Pull the e-invoice registry at month-end, anything after 11:59 PM on the last business day belongs to the next month. Credit notes issued after cutoff go into the following month, keep separate tracking for subsequent invoices relating to prior-period activity.

Purchase and GRN-Based Cut-Off Rules

Recognize purchases on the Goods Receipt Note date, align GRN to the actual receipt date in warehouse. Goods received after month-end fall into the following month even if the invoice arrived earlier. Maintain a post-cutoff GRN list, for RCM entries from unregistered vendors or imports, use the invoice date per GST rules and document them clearly.

Expense Accruals and Cut-Off Rules

Accrue expenses in the month incurred, not when paid. Utilities are accrued by billing cycle, pro-rate if cycles cross months. Accrue salaries and wages for work performed, typically on the last day for payment on the 5th or 10th. Insurance and subscriptions are spread across usage periods. Capitalize items above your threshold, expense below, post monthly depreciation.

Banking Cut-Off Rules

Use the bank statement as of the last business day, pull at 5:30 PM or later. Identify deposits in transit for cash after hours, list unpresented cheques, exclude transactions processed after cutoff. Reconcile to the penny, investigate any difference over ₹100.

GST Cut-Off Rules for Compliance

Record outward supplies in GSTR-1 by e-invoice date, book input from GSTR-2B by vendor invoice date and availability in 2B. Match sales invoices to IRNs, exclude any IRN not generated by month-end, ensure GSTR-1 aligns with books. For purchases, use GSTR-2B as source, record input only for invoices appearing in 2B and received in your system. RCM entries are recorded separately, input may be deferred depending on rule. Post-cutoff vendor invoices for prior-month goods can be recorded in prior month, input may be claimed when GSTR-2B updates.

TDS Cut-Off Rules

TDS is withheld based on transaction or payment date per section. Salary TDS is deducted in the month paid, January salary paid on February 5th carries February TDS. For purchases, apply section-specific rules. Accrue TDS expense and liability even if challan is pending, reconcile deductions to your TDS register and Form 26AS by the 20th of the month after quarter-end.

Master Reconciliation Checklist for Monthly Close Service

Bank and Cash Reconciliation Checklist

Start with current accounts, reconcile book balance to statement as of the last business day, document adjustments for bank fees, interest, and errors. See the automated bank reconciliation guide for India-focused steps.

Include savings, term deposits, and foreign currency accounts with exchange rates noted. Reconcile UPI and digital wallets, tie daily logs to bank settlements and ledgers, these small items often create big mismatches. Count petty cash physically, compare to ledger, clear discrepancies and replenish as needed.

Accounts Receivable Reconciliation Process

Generate customer-wise ageing, escalate >90 day invoices for collection. Cross-check credit notes, match to original invoices, avoid duplicates. Review bad-debt candidates with approval evidence before write-off. Verify TDS certificates for services to entities with withholding obligations, reconcile to deductions in books. Track month-end discounts and rebates, accrue and net correctly from revenue.

Accounts Payable Reconciliation Steps

Produce vendor-wise ageing, segment by payment terms. Verify GRN for each invoice, confirm quantity and price, flag three-way match exceptions. Track debit notes for returns and offset correctly. Monitor advances and reconcile against subsequent invoices. Obtain vendor confirmations for material suppliers, document pending confirmations in the exception log.

GST Reconciliation Requirements

Compare sales invoices to IRNs in GSTR-1, investigate mismatches. Cross-check GSTR-3B entries for outward and inward supplies, input, and tax paid against the ledger, flag post-filing amendments. Match GSTR-2B furnished by vendors against the purchase register, refer to the GSTR-2B reconciliation tools guide to streamline mismatches. Verify RCM entries, IGST, CGST, SGST splits, and transposition errors.

TDS Reconciliation Process

Cross-check monthly deductions to the TDS register with dates, amounts, and section codes. Reconcile liability accrued to challans paid, note shortfalls. Verify Form 26AS for key employees and vendors, flag and rectify differences promptly. Accrue interest or penalties on delayed payments where applicable.

Fixed Assets and Depreciation Reconciliation

Capitalize qualifying purchases with invoice and GRN support, record disposals with correct gain or loss, calculate monthly depreciation using WDV or SLM per policy, reconcile GL balances to the physical asset register and investigate mismatches.

Review and Sign-Off Process for Monthly Close

Establishing Your Maker-Checker Workflow

The preparer compiles the full close package, runs a self-review: all reconciliation items resolved or documented, no unreconciled difference over ₹100 on balance sheet accounts, journals have support, GST and TDS postings cross-checked, trial balance closed with no suspense, variance analysis complete, exception log updated.

The senior reviewer spot-checks reconciliations, validates variance explanations, confirms journal approvals, reviews GST and TDS tie-outs, checks prior-month exceptions, and assesses communication tone and accuracy. Escalate to CFO when variances exceed materiality, exceptions linger beyond seven days, new compliance risks appear, or cash runway concerns emerge.

CFO and Partner Sign-Off Requirements

CFO or partner confirms flagged items are addressed, applies materiality, assesses cash position and runway, notes risk items for next month, and approves financial statements. Document sign-off with digital signatures or email timestamps, maintain a robust audit trail.

Implementing Variance Analysis

Standardize variance analysis across major line items, track current versus prior month, calculate absolute and percentage variances. Set thresholds, for example ₹50,000 or 10 percent. Require CFO pre-approval for large journals, watch unusual entries like revenue reversals or related-party transactions, escalate unresolved reconciliation items that persist across months.

Client Communication Strategy for Monthly Close Service

Proactive communication keeps data flowing and reduces cycle time. For a cadence blueprint see client communication cadence and NPS.

Pre-Close Communication

Three days before month-end send reminders with document lists and firm submission deadlines, note that late data delays the close. One day prior, send a short WhatsApp or Slack nudge, quick reminders prevent last-minute bottlenecks.

During the Close Process

On Day 0 send cutoff confirmation, prior-month entry is locked, later data lands in the next month. Hold a daily 15-minute check-in at 4:00 PM IST during Days 1-4, address blockers, share a live exception tracker to make progress visible.

Final Delivery and Sign-Off

On Day 5 conduct a one-hour review with the client CFO, walk through trial balance, variance analysis, exceptions, cash position and runway, compliance status, and obtain approvals. On Day 6 email the full close package, highlight unresolved items and next steps, reference the improvement log for process changes.

Managing Delays and Disputes

If critical data is missing by Day 2, escalate via email with a four-hour window, call on Day 3 if needed, and escalate to the client CFO. By Day 4 proceed with available information, document gaps, and present a conditional close on Day 5. For journal disputes, listen fully, cite standards or policy, document rationale, involve external auditors if necessary, consider deferring immaterial amounts under ₹10,000 to maintain relationships.

Building Your Improvement Log System

Structuring Your Improvement Tracking

Create a master log capturing issue, root cause, corrective action, owner, due date, status, and impact. Track data quality gaps, process delays, documentation issues, ledger mapping errors, compliance mismatches, and reconciliation gaps.

Monthly Retrospective Process

Hold a 30-minute retrospective on the fourth Friday after each close, review completed actions and impact, diagnose what went wrong, assign owners and dates for new actions, update and circulate the log. Monitor KPIs like days to close, exceptions per close, unreconciled entries, client response time, compliance issues, link improvements to these metrics.

Continuous Improvement Metrics

Target Day 5 close consistency, fewer than five exceptions per close, no unreconciled entries above ₹1,000, 95 percent on-time reconciliations, GST variances under ₹10,000. Aim for 90 percent on-time client submissions, 24-hour average exception responses, 95 percent timely client sign-offs. Hold 100 percent GST and TDS compliance with Form 26AS matching, and complete e-invoice compliance where applicable.

Leveraging Technology and Automation

Where Automation Helps

Automation cuts grunt work and highlights anomalies. Consider tools like AI Accountant, built for Indian GST and TDS realities, QuickBooks, Xero, FreshBooks, and Zoho Books.

Leverage fast document ingestion, AI powered extraction for vendor invoices, automated ledger mapping, consistent GST treatment, and anomaly flags. Use bi-directional sync with systems like Tally or Zoho Books, post with one click, and view real-time statements. Dashboards give instant visibility, track trends, cash runway, AR/AP ageing with DSO and DPO, and export reports effortlessly.

Maintaining Control and Compliance

Even with automation, enforce strong controls, audit trails for changes, digital sign-offs with timestamps, role-based access and segregation of duties, encryption in transit and at rest, and seven-year retention of close packages per Indian tax requirements.

Common Monthly Close Pitfalls and Solutions

GST Mismatches from Late Vendor Invoices

When vendor invoices appear post-cutoff, GST mismatches are common. Implement GRN based input booking for known amounts, post with a note that formal invoice is awaited, re-verify when GSTR-2B updates and adjust as needed.

TDS Reconciliation Gaps

Books versus Form 26AS mismatches raise flags. Make TDS reconciliation a mandatory monthly step, cross-check deductions to the register, verify against 26AS quarterly, investigate variances above ₹1,000 immediately, and accrue interest on delays.

Unstructured Bank Statements

Photos or screenshots slow reconciliation. Standardize the statement format with required columns, offer to generate clean exports for clients, this trims reconciliation time substantially.

Client Data Submission Delays

Late submissions ripple across the entire timetable. Send pre-close reminders three days early, state deadlines and consequences, use multiple channels, issue conditional approvals for late data, and track client compliance in the improvement log.

No Systematic Improvement Tracking

Without tracking, the same errors repeat. Institute the improvement log immediately, run monthly retrospectives, tie actions to KPIs, expect exceptions to halve within six months with disciplined follow-through.

Quick Start Guide for Next Month

Week 1, share your cut-off rules and obtain written client acknowledgment. Week 2, build the reconciliation checklist with owners and deadlines. Week 3, define maker-checker responsibilities and schedule sign-off. Week 4, run the improved close, document issues, hold a retrospective, plan upgrades for Month 2.

By Month 2, close time stabilizes, exceptions decline, client satisfaction rises, and your team gains predictability.

The Path to Monthly Close Excellence

Excellence rests on five pillars, clear cut-off rules, comprehensive reconciliation, structured reviews, proactive communication, and continuous improvement. Start with the framework, add automation where it helps, and iterate every month.

The monthly close can be a calm, reliable process, deliver accurate, compliant financial statements by Day 5, month after month.

FAQ

What is a standard India-specific monthly close calendar aligned to GST-3B filing, and how do I keep Day 5 intact?

Run pre-close three days before month-end, lock entries on Day 0, complete bank and AR by Days 1-2, AP, GRN checks, RCM, and GSTR-2B by Days 2-3, accruals and fixed assets by Days 3-4, GST and TDS verification by Days 4-5, and senior sign-off on Day 5. Protect Day 5 by enforcing cut-offs, maintaining a live exception tracker, and using tools like AI Accountant to automate reconciliations and dashboards.

How should a CA document cut-off rules for GRN versus vendor invoice date, especially when invoices arrive late?

State policy that purchases are recognized by GRN date, not invoice date. Maintain a post-cutoff GRN list for goods received at month-end, record the liability when amount is known, flag GST input for claim when the invoice appears in GSTR-2B. An AI workflow in AI Accountant can tag GRNs, match subsequent invoices, and prompt input claim timing.

Best-practice approach to resolve GSTR-2B mismatches quickly, is there a repeatable checklist?

Start with a book-to-2B match, categorize mismatches into timing, data-entry errors, vendor non-filing, and RCM. Communicate with vendors immediately, correct data-entry errors, defer input for timing issues, and record RCM separately. The GSTR-2B reconciliation tools guide and automated matching in AI Accountant help standardize and speed this step.

How do I handle TDS for January salary paid on February 5th, what is the correct month of deduction?

TDS on salary is deducted in the month of payment, so the February 5th disbursement carries February TDS. Accrue January salary expense in January, but deduct and book TDS in February, reconcile to the TDS register and Form 26AS quarterly.

Can input GST be recognized when the vendor invoice is not yet received but GRN is dated month-end, how do auditors view this?

Recognize the purchase liability by GRN when amount is determinable, but claim input GST only when the invoice appears in GSTR-2B, document the deferral clearly. Auditors expect policy consistency, robust documentation, and subsequent matching. Automation in AI Accountant can defer ITC and auto-claim once 2B updates.

What evidence do auditors expect for maker-checker, are email approvals enough?

Auditors look for control design and operating effectiveness, preparer checklists, reviewer sign-offs with timestamps, journal approval evidence, and resolution of exceptions. Email approvals with clear references are acceptable, digital sign-offs in systems like AI Accountant with audit trails are stronger.

How should RCM be booked, and when should ITC be claimed under RCM entries?

Record RCM expenses and output tax liability separately, pay the tax per rules, claim ITC in the period allowed, typically after payment. Maintain vendor status and rule references, ensure no double-claiming. Configure your accounting tool to tag and schedule RCM ITC claims automatically.

What variance thresholds should a CFO use to trigger deeper reviews during monthly close?

Practical thresholds are ₹50,000 or 10 percent month-on-month for major lines, with stricter levels for revenue and cash. Flag unusual journals, reversals, and related-party entries irrespective of amount. A dashboard in AI Accountant can auto-highlight variances for fast CFO review.

How do I reconcile UPI collections to bank settlements and the ledger, when volume is high?

Use daily UPI logs, batch them, reconcile to bank settlement files, then to the ledger. Investigate any unposted batches and timing differences. An automated rule engine can match identifiers and amounts, and post adjustments for fees. Consider the automated bank reconciliation guide for structured steps.

What is the preferred monthly depreciation method for Indian entities, and how do I keep schedules audit-ready?

Select WDV or SLM per company policy and tax requirements, post monthly, keep a fixed asset register with cost, date, rate, accumulated depreciation, and location. Reconcile register to GL monthly, document disposals with gain or loss. Systems like AI Accountant can compute and post monthly depreciation consistently.

What is a conditional close, when should a CA firm use it, and how do we document gaps?

A conditional close delivers financials by Day 5 with documented gaps due to missing data, exceptions are listed with owners and deadlines, impact is explained, and adjustments are scheduled. Use when delays would materially impact compliance or decision-making, maintain transparency and follow-up cadence.

Which KPIs should a finance leader track to improve the monthly close, any targets to start with?

Track days to close, exceptions per close, unreconciled entries count and value, client on-time submission rate, average exception response time, and GST and TDS compliance status. Initial targets, Day 5 close, fewer than five exceptions, no unreconciled items above ₹1,000, 90 percent on-time client data, 24 hours average response. AI Accountant can surface these KPIs automatically.