-01%201.svg)

Key takeaways

- Accrual basis monthly reports give you accurate profit, clean KPIs, and investor ready numbers because they recognize revenue when earned and costs when incurred, not when cash moves.

- Cash basis reports suit freelancers and micro businesses that need a simple view of money in and money out, but they hide liabilities, unbilled revenue, and working capital strain.

- Switching from cash to accrual changes your monthly picture significantly once you include prepaids, provisions, deferred revenue, and unbilled items, so the choice shapes every decision you make.

- A disciplined monthly close (T plus 5 to T plus 10) with reconciliations, variance commentary, and a standard pack structure turns raw numbers into board ready insights.

- KPIs like gross margin, burn rate, runway, DSO, and cash conversion cycle only mean something when the underlying accounting basis is consistent month after month.

- Virtual Accounting by AI Accountant pairs a dedicated CA team with an AI dashboard so founders get accurate accrual based monthly packs, timely compliance, and live visibility without hiring in house.

Monthly Financial Reporting for Indian Businesses: What's New in 2026

The reporting environment for Indian SMEs and startups has shifted meaningfully since early 2025. Until March 2025, GST e-invoicing applied to businesses with aggregate turnover above ₹5 crore. From April 2025, the threshold dropped to ₹1 crore, pulling a much larger pool of small businesses into mandatory e-invoicing. If your monthly close process did not previously account for e-invoice generation and reconciliation, it does now. GSTR-1 and GSTR-3B filings must tie back to e-invoice data, adding a reconciliation step that did not exist for many firms a year ago. The GST portal now flags mismatches more aggressively, and unresolved discrepancies can block ITC claims in subsequent periods.

On the TDS front, Section 194T (applicable from April 2025) introduced TDS on payments to partners of firms exceeding ₹20,000 per year, including salary, remuneration, interest, bonus, and commission. Partnership firms and LLPs must now deduct TDS on these payments and reflect them correctly in monthly books and quarterly returns. Missing this means penalties under Sections 234E and 271H, plus potential disallowance of the expense. The Income Tax Department portal has updated forms and challan workflows to accommodate this change.

For businesses on accrual basis, these changes add new reconciliation checkpoints every month: e-invoice matching, ITC validation against auto-populated GSTR-2B, and TDS on partner payments. Cash basis reporters feel the pinch too, since GST and TDS obligations trigger regardless of how you recognize revenue internally.

Firms that rely on a CA managed virtual accounting service can absorb these new compliance layers without adding headcount. The operational shift is real, but the cost of inaction (blocked ITC, late filing penalties of ₹50 per day under CGST, interest at 18% per annum on unpaid GST) makes early adoption non negotiable. If you have not reviewed your monthly close checklist against these 2026 requirements, now is the time.

CA-led Virtual Accounting, AI dashboards, and the monthly pack

Virtual Accounting should feel like having an in-house finance team, without the hiring burden. In a CA-led model, qualified Chartered Accountants run your books, reconcile banks and gateways, and file GST, TDS, and income tax. You get a simple AI dashboard to see the numbers, track status, and ask questions.

Founders do not do the accounting inside the dashboard. They use it to understand performance, position, and cash movement, and to approve actions comfortably.

Think of it as a managed service with a live window into your finance engine.

Monthly financial reports bring together the profit and loss statement, balance sheet, and cash flow statement so you can scan performance, position, and cash movement at a glance. This clarity drives quick decisions on cash control, compliance, investor updates, and runway planning.

For a clear primer on monthly packs and how they drive decisions, see ICAI guidance on financial reporting standards and the PwC India insights on financial reporting.

Core components of monthly financial reports

A strong monthly pack is standardized, comparable, and concise. Commentary explains changes and actions so the reader never has to guess.

Profit and Loss

- Show revenue, cost of goods sold (COGS), and operating expenses.

- Highlight gross profit, operating profit, and net profit.

- Add month over month, year to date, and budget versus actual columns.

- Include narrative on drivers: price changes, volume shifts, and product mix.

Balance Sheet

- List assets like cash, accounts receivable, inventory, and fixed assets.

- List liabilities like accounts payable, GST payable, loans, and other dues.

- Show equity, and note big movements such as a loan draw or inventory build.

Cash Flow Statement

- Split cash flows by operating, investing, and financing activities.

- Use the indirect method. Start with net income and adjust for non-cash items, plus working capital changes.

- Bridge opening cash to closing cash so liquidity is obvious at a glance.

AR and AP aging

- Accounts Receivable Aging with buckets (current, 1 to 30 days, 31 to 60 days, and beyond) to track DSO.

- Accounts Payable Aging with similar buckets. Monitor DPO to manage vendor terms and payment cycles.

Bank and Payment Gateway Reconciliations

- Tie book balances to bank statements and gateway reports. Resolve unmatched items quickly to keep your ledger entries clean.

Inventory and fixed assets

- Inventory report showing opening stock, purchases, consumption or COGS, adjustments, and closing stock. Reconcile physical counts when maintained.

- Fixed Asset Register and depreciation schedules showing additions, disposals, and monthly depreciation.

Compliance snapshot

- GST filing status for GSTR-1, GSTR-3B, and GSTR-9 where applicable.

- TDS challans and returns: Forms 26Q, 24Q, 27Q, and property related filings.

- Income tax due dates and advance tax status.

- ROC filings for small companies (MGT-7 and AOC-4) plus basic MCA items.

For a practical overview, see 7 essential elements in monthly financial reports.

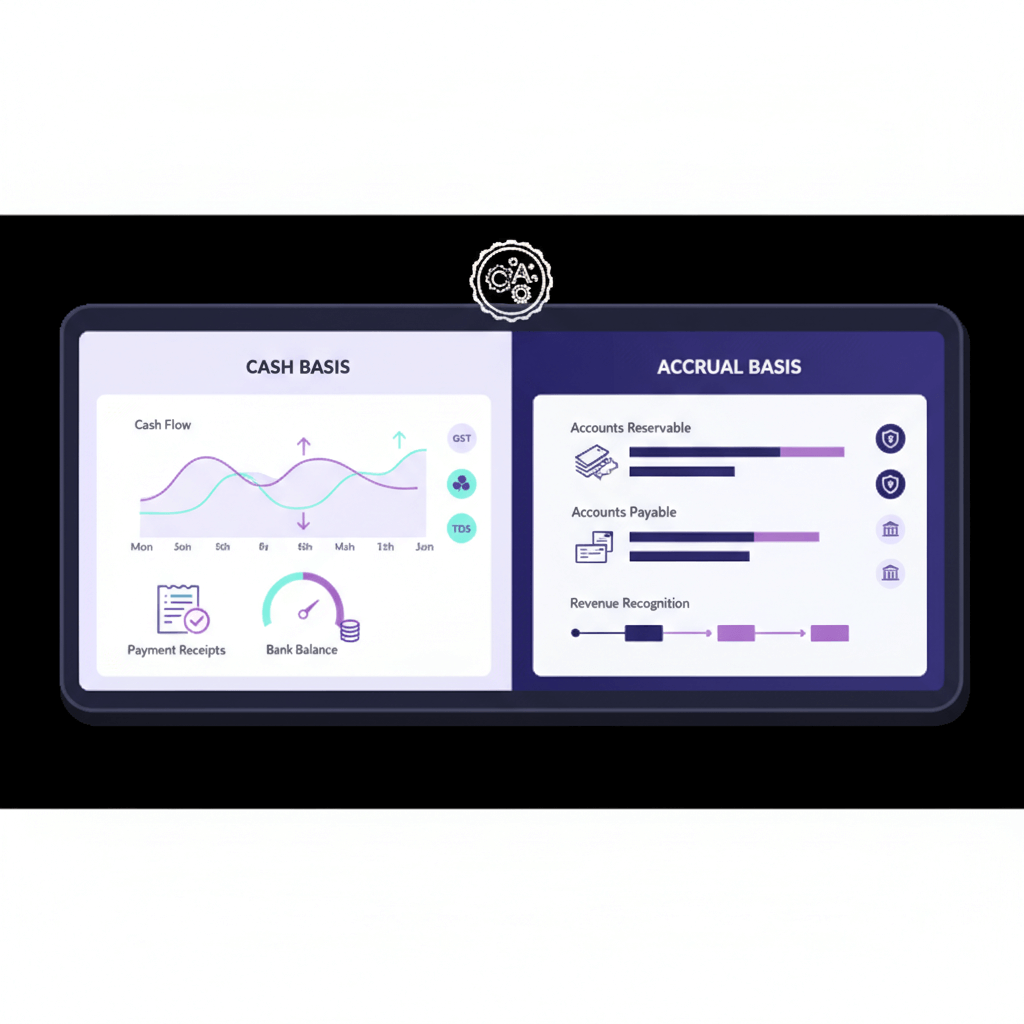

Cash basis versus accrual basis: how each changes your monthly view

This is the core choice that shapes everything in your monthly pack. Understanding the difference between cash and accrual accounting is not academic. It changes the numbers you see, the KPIs you track, and the decisions you make.

What cash basis shows you

Cash basis accounting records income when you receive payment and expenses when you pay them. It is simple. Your profit and loss reflects actual bank movement.

- Good for freelancers and sole proprietors with straightforward operations.

- Easy to maintain, no need to track receivables or payables as separate line items.

- Gives you a real time view of how much money you actually have.

The downside: it hides obligations. If you received a large advance this month but have not delivered the work, cash basis shows inflated revenue. If you owe a vendor ₹5 lakh but have not paid yet, cash basis shows no expense. Your profit number can mislead you.

What accrual basis shows you

Accrual basis records revenue when earned and expenses when incurred, regardless of when cash moves. This is the standard under Indian Accounting Standards (Ind AS) and is required for most companies.

- Essential for startups, SMEs, and any business with credit terms.

- Captures prepaids, provisions, deferred revenue, unbilled revenue, and accrued expenses.

- Produces KPIs (gross margin, net margin, DSO, DPO) that reflect true business health.

The trade off: it requires more bookkeeping discipline. You need to book journal entries for accruals, track receivables and payables properly, and reconcile more frequently.

When the choice matters most

The gap between cash and accrual widens as your business grows. A freelancer billing two clients a month may see little difference. A SaaS startup with annual contracts, deferred revenue, and prepaid hosting costs will see vastly different profit numbers under each method.

If you are preparing investor updates, board packs, or bank loan applications, accrual is expected. Cash basis reports will not pass scrutiny in these contexts.

Essential KPIs and analytics for monthly reports

A crisp KPI dashboard converts pages of numbers into decisions. The AI view makes trend scanning effortless.

- Revenue growth rate, month over month and year over year.

- Gross margin, net margin, and unit economics.

- Burn rate, and runway (cash divided by burn rate). A simple version: bank balance divided by net monthly cash burn.

- Cash conversion cycle: DSO plus DIO minus DPO.

- Budget versus actual variance, with commentary splitting revenue into price, volume, and mix, and costs into rate and usage.

- Segment views by product, service, channel, region, or customer cohort.

These KPIs only tell the truth when the underlying accounting basis is consistent. Mixing cash and accrual across months makes trend analysis unreliable. Pick one method and stick with it.

Step by step monthly close checklist

Close fast, close clean, then lock and archive. Aim for T plus 5 to T plus 10 after month end.

- Collect data

Gather sales invoices, purchase bills (also called vendor invoices), expenses, payroll, and reimbursements. Download bank statements and payment gateway statements. Pull inventory movement reports if relevant. - Post and categorize

Enter and code all transactions in your accounting software. Maintain a consistent chart of accounts. Each ledger entry should map to the correct account head. - Record accruals

Recognize revenue when earned and costs when incurred. Book provisions, prepaids, deferred revenue, and payables. This step is what separates accrual from cash basis reporting. - Reconcile ledgers

Bank reconciliation, gateway reconciliation, AR and AP sub-ledgers to the general ledger. Reconcile GST ledgers and input credit with returns. Match e-invoice data against GSTR-1 filings. - Review and approvals

Scrutinize ledgers for unusual balances, duplicates, and miscodings. Check compliance for GST, TDS, income tax, and ROC. Resolve exceptions and get approvals. - Generate reports with commentary

Produce the profit and loss statement, balance sheet, and cash flow with comparatives. Build KPI dashboards and budget versus actual views. Add short variance notes and recommended actions. - Distribute and archive

Share with founders and finance leads. Store the final pack with version control. Keep supporting documents in a central repository with an audit trail.

Templates and pack structure

Use a repeatable structure so everyone knows where to look. Consistency builds speed and trust.

- Executive summary: month highlights, risks, actions, cash balance, burn and runway, key KPIs, and critical alerts.

- Financial statements with comparatives: profit and loss, balance sheet, cash flow. Prior month, same month last year, YTD, budget versus actual with variance flags.

- KPI dashboard: trend charts for revenue, margins, DSO and DPO, cash conversion cycle, burn and runway, segment views.

- Cash position and near term forecast: closing cash, expected inflows and outflows, a simple thirteen week cash forecast.

- Compliance calendar and filing status: GST, TDS, income tax, ROC items where applicable.

- Appendix: detailed ledgers, schedules, AR and AP aging lists, inventory valuation, fixed asset register, accounting policy notes, unusual events.

See EY India financial reporting insights for additional pack structuring guidance.

How to read and interpret monthly reports

Reading is about patterns and early warnings. A disciplined scan turns signals into actions.

- Look for trends and seasonality. Are sales peaking? Are margins stable or sliding? Are expenses drifting up?

- Catch early warnings. Falling gross margin can signal pricing pressure or rising input costs. Rising AR aging and DSO means slow collections and cash risk. Inventory build without matching sales hints at overbuying. Negative operating cash flow with flat profit suggests working capital strain.

- Use a variance framework. Revenue splits into price, volume, and mix. Costs split into rate and usage. Mark recurring versus one off items.

- Turn insights into actions. Tighten collections to reduce DSO. Renegotiate vendor terms to extend DPO when possible. Adjust pricing or discounting. Pause discretionary spend. Delay non essential capex. Reprioritize hiring.

On accrual basis, these signals appear earlier because the numbers reflect economic reality, not just bank movement. Cash basis can delay warning signs by weeks or months.

Common mistakes to avoid

Avoidable errors cost time and trust. A CA-led process and automated checks reduce these risks significantly.

- Late or inconsistent closing. Decisions lag and trends break when you close on different dates each month.

- Missing accruals and adjustments. Profit distorts and liabilities hide. This is the biggest risk when running cash basis for a business that should be on accrual.

- Misclassifying revenue or expenses. Margins and KPIs get ruined. A vendor invoice coded to the wrong expense head can skew your gross margin by percentage points.

- Skipping reconciliations. Untied bank or gateway balances can hide errors or even fraud.

- Ignoring tax and compliance. Missed GST, TDS, income tax, or ROC steps bring penalties. With the 2026 e-invoicing threshold at ₹1 crore, more businesses face this risk.

- No variance commentary. Numbers without notes invite confusion. Always explain why a line item moved.

- Mixing accounting bases across months. If you switch between cash and accrual without a clear transition, your trend data becomes meaningless.

Tools and automation

Choose tools that reduce manual work, then layer automation for control and speed.

- AI Accountant, a CA-managed service with an integrated dashboard for bookkeeping, compliance, and monthly reports.

- QuickBooks Online for cloud based bookkeeping with multi-currency support.

- Xero for small businesses that need strong bank feed integrations.

- FreshBooks for freelancers and service businesses focused on invoicing.

- TallyPrime for Indian businesses that need deep GST compliance and local statutory reporting.

- Automation features to look for: bank feeds and gateway integrations, invoice syncing, anomaly detection and duplicate checks, dashboards for trends and KPIs, access roles and audit trails.

Segment specific guidance

Freelancers

- Focus on cash first. Track bank balance, inflows, and outflows.

- Keep a simple profit and loss and basic balance sheet on cash basis.

- Watch AR aging closely. Collect fast to avoid cash gaps.

- Set aside taxes for GST and income tax. Plan TDS on contracts if relevant.

- Maintain a simple thirteen week cash plan.

- Cash basis works well here because transaction volume is low and credit terms are minimal.

Startups and SMEs

- Run on accrual for accuracy. Close by T plus 10 at most.

- Track burn rate and runway every month. Reforecast often.

- Build a budget and show budget versus actual with clear notes.

- Prepare investor ready packs with statements, KPIs, cash forecast, and compliance status.

- Watch working capital. Improve DSO and DPO while protecting supplier relationships.

- Accrual basis is non negotiable for fundraising, bank loans, and statutory audits under the Companies Act.

How AI Accountant Virtual Accounting delivers

AI Accountant provides a managed accounting and compliance service led by qualified CAs, supported by a central dashboard for live visibility.

What you get each month

- Financial overview: revenue, expenses, profit and loss, and balances.

- Income and expense breakdowns by category.

- Cash flow trends, burn rate, and runway.

- Recent transactions and bank statement analysis.

- AR and AP aging with DSO and DPO.

- Document repository for bills, invoices, and working files.

- Compliance calendar and filing status for GST, TDS, income tax, and ROC.

- Centralized communication with the CA team for fast clarifications.

Compliance coverage

- GST registration, GSTR-1 and 3B, annual GSTR-9, e-invoice enablement, and reconciliations.

- TDS advisory and compliance: monthly challans, Forms 26Q, 24Q, 27Q, and property related returns.

- Income tax return filing, advance tax support, and tax audit preparation support.

- ROC annual filings for small companies and basic secretarial support where eligible.

Reporting cadence

- Close targeted for T plus 5 to T plus 10.

- Standard monthly pack: executive summary, statements with comparatives, KPI dashboard, cash position and forecast, compliance snapshot.

- MIS with variance analysis, clear commentary, and recommended actions.

Governance cadence and distribution

- Close by T plus 5 to T plus 10, lock the version after sign off, and archive it.

- Share the executive summary and dashboard with founders and business heads.

- Share the detailed appendix with finance leads.

- Use the pack in board and investor meetings for updates and decisions.

- Keep an audit trail and a repository for all working papers.

See Deloitte India governance and reporting frameworks and a board level template via monthly financial reporting template for board meetings.

Next steps

- Adopt the monthly close checklist. Set a T plus 10 goal, then improve to T plus 5 over time.

- Use the pack template consistently. Keep the same structure every month.

- Start with three to five KPIs that matter most and expand as needed.

- Define roles, timelines, approvals, and version control in a simple governance plan.

- Schedule a walkthrough of AI Accountant to operationalize monthly reports with automation and on time filings.

Appendix quick reference

Use consistent definitions across months, then tie changes to actions.

- Gross margin percent equals gross profit divided by revenue.

- Net margin percent equals net profit divided by revenue.

- Burn rate equals average monthly cash outflow.

- Runway equals cash on hand divided by burn rate.

- DSO equals AR divided by average daily revenue.

- DPO equals AP divided by average daily COGS or operating expenses per your policy.

- Cash conversion cycle equals DSO plus DIO minus DPO.

For definitions and methodology, refer to ICAI technical guides on financial ratios and reporting.

FAQ

Should I use cash or accrual basis for monthly financial reports

Use accrual basis if you are an SME, startup, or any business with credit terms, inventory, or investors. Accrual captures revenue when earned and expenses when incurred, giving you accurate margins and reliable KPIs. Cash basis works for freelancers and sole proprietors with simple operations, but it hides payables, receivables, and deferred items that matter for planning.

What is CA-led Virtual Accounting and how does the AI dashboard fit in

CA-led Virtual Accounting is a managed service where qualified CAs handle bookkeeping, reconciliations, GST, TDS, income tax, and compliance end to end. You get an AI dashboard for visibility and collaboration. The dashboard is designed for clarity and control, not for founders or business heads to post entries themselves.

What exactly is included in the monthly pack delivered by a CA team

A standard pack includes profit and loss, balance sheet, cash flow, AR and AP aging, bank and payment gateway reconciliations, inventory and fixed asset schedules, KPI dashboard, cash position and near term forecast, plus a compliance snapshot for GST, TDS, income tax, and ROC where relevant.

How do DSO, DPO, and cash conversion cycle help me manage cash

DSO shows average collection time, DPO shows how long you take to pay vendors, and cash conversion cycle combines receivables, inventory, and payables timing to reveal working capital efficiency. Reducing DSO, increasing DPO thoughtfully, and optimizing inventory lowers the cash conversion cycle and extends runway.

What is the recommended monthly close timeline for clean reporting

Close by T plus 5 to T plus 10, with all reconciliations complete, accruals booked, and a short variance commentary in the executive summary. This cadence keeps investor updates and internal decisions timely.

How does the 2026 e-invoicing threshold change affect monthly reporting

From April 2025, GST e-invoicing applies to businesses with aggregate turnover above ₹1 crore, down from ₹5 crore previously (2026 update). This means your monthly close must now include e-invoice generation, matching e-invoice data to GSTR-1, and resolving mismatches before filing. Ignoring this can block ITC claims and trigger late filing penalties.

Can the service handle multi-entity or segment level reporting

Yes, the monthly pack can include segment breakdowns by product, service, channel, region, or customer cohorts, and multi-entity consolidation workflows where required. This lets leadership compare performance across units cleanly.