Key takeaways

- A disciplined fixed asset register, with clear policies and monthly reconciliations, prevents audit issues and GST, income tax non-compliance.

- Book depreciation, tax depreciation, and GST ITC rules operate differently, maintain parallel calculations and clear documentation.

- Capture complete asset details at source, tag assets physically, confirm put-to-use dates, and reconcile FAR to GL every month.

- Componentization, CWIP tracking, and ITC reversal on disposal are frequent pain points, standardize them in your SOP.

- Automation with tools like AI Accountant or modules in your accounting software cuts errors and speeds up closes.

What is a Fixed Asset Register and Why Indian SMEs Need One

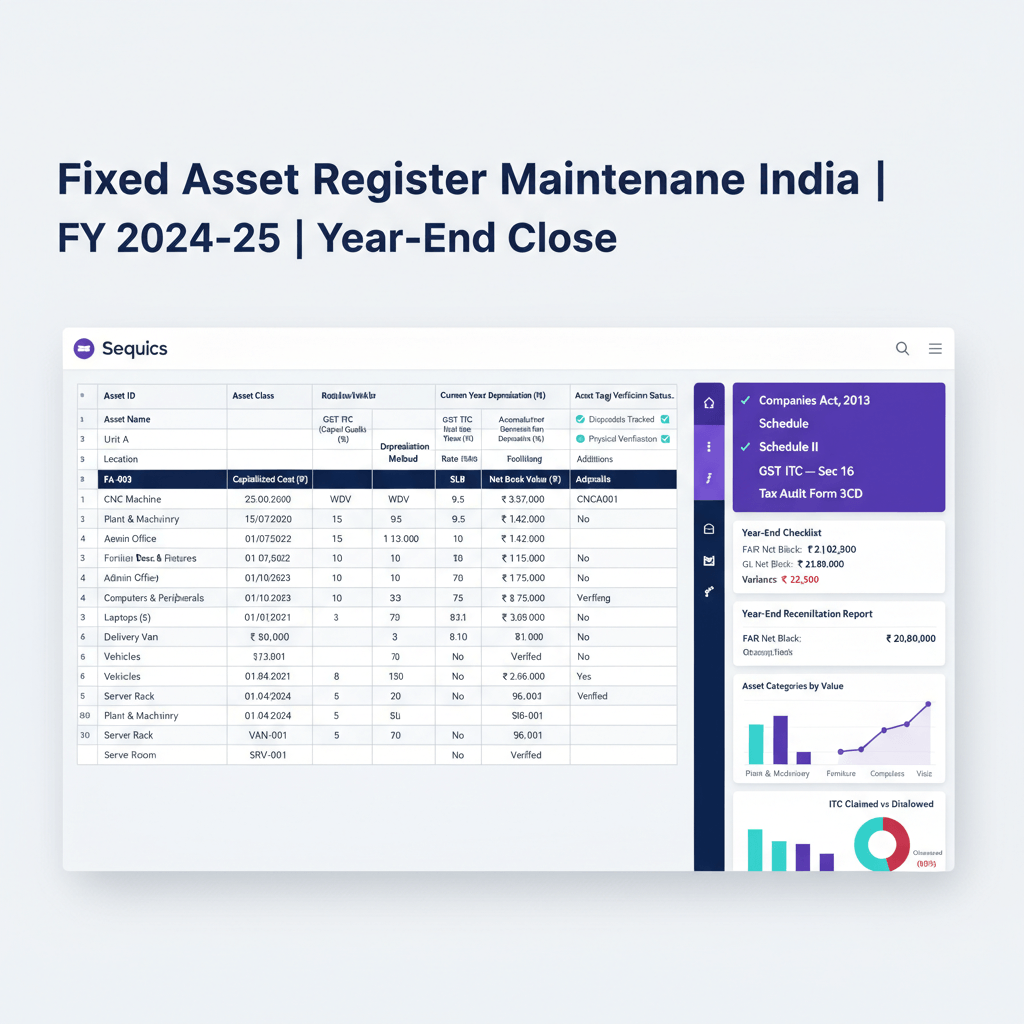

A fixed asset register India is your authoritative, itemized inventory of all tangible and intangible assets. It houses descriptions, serial numbers, locations, custodians, purchase and put-to-use dates, capitalized costs, depreciation parameters, and current book values. It is the single source of truth for audits, tax, GST, and insurance.

The Companies Act 2013 requires it, GST needs precise ITC tracking on capital goods, and income tax relies on accurate block wise depreciation. Your general ledger shows totals, your FAR shows asset wise details, and both must reconcile.

Beyond compliance, a robust FAR curbs pilferage, supports insurance claims, and improves capital planning. For a deeper overview, see maintaining a fixed asset register for smoother operation and growth, explore fixed asset register benefits, and review managing fixed asset register in GL in India.

Think of the FAR as your audit ready ledger of facts, not assumptions.

Understanding India’s Compliance Requirements for Fixed Assets

Companies Act 2013 and Schedule II

Follow prescribed useful lives, for example laptops 3 years, furniture 10 years, factory buildings 30 years, unless you have strong technical documentation to deviate. Apply componentization when a major asset’s parts have different lives.

Accounting Standards Matter

SMEs commonly use AS 10, larger entities follow Ind AS 16. AS emphasizes historical cost, Ind AS permits revaluation for entire classes. For borrowing costs, AS 16 allows capitalization, Ind AS 23 mandates it for qualifying assets.

Income Tax Depreciation Rules

Tax depreciation uses block wise WDV with specified rates, for example 40 percent for computers, 15 percent for plant and machinery, and the half year rule for first year additions.

CARO 2020 Audit Requirements

Auditors examine asset records, physical verification, title deeds for immovable property, and your revaluation approach if used.

GST on Capital Goods

Section 17(5) blocks ITC on specified items. Section 18(6) requires proportionate ITC reversal on disposals. Rule 43 governs common credit apportionment. A practical overview appears in this India focused FAR and GL guide.

Essential Fields Every Fixed Asset Register Must Include

Basic Identification Fields

- Unique asset ID or barcode tag, asset category, detailed description, make and model, serial number.

- Exact location and custodian for accountability.

Purchase and Vendor Information

- Vendor name and GSTIN, invoice number and date, PO reference, GRN details.

- Purchase date and put-to-use date captured separately.

Cost Components Breakdown

- Basic price plus freight, installation, duties, professional fees, and capitalized borrowing costs.

- GST bifurcation, with ITC eligibility clearly flagged. If ITC blocked, add GST to asset cost.

Depreciation Parameters

- Useful life as per Schedule II or justified estimate, residual value, method, componentization where relevant.

Financial Values

- Gross block, accumulated depreciation, net book value, revaluation and impairment if applicable.

Movement History

- Transfers across locations or cost centers, CWIP to FA capitalization, disposals with sale proceeds and GST effects.

Supporting Documentation

- References to invoices, title deeds, RC, insurance, AMC, and relevant approvals for capitalization or write off.

For concise references, skim need for a fixed asset register, revisit maintaining a fixed asset register, and scan FAR benefits.

Core Principles of Fixed Asset Accounting in India

Capitalization Policy

Define thresholds, include all costs to get the asset ready for intended use, and document decisions consistently.

Componentization Requirements

Track significant components with different useful lives separately, typically over 10 percent of total cost.

Capital Work in Progress

Accumulate costs till the asset is ready, no depreciation until capitalization, monitor CWIP aging monthly.

Depreciation Methods and Timing

Books may use SLM or WDV, tax is always WDV by blocks. Start depreciation on put-to-use, stop on disposal or full depreciation. Timing differences create deferred tax.

Revaluation and Impairment

Ind AS allows revaluation model, AS typically uses historical cost. Test for impairment when indicators arise.

Lease Accounting

Under AS 19, operating leases are off balance sheet. Under Ind AS 116, recognize right of use assets and liabilities, see this Ind AS 116 complete summary.

Cross check your approach with India specific FAR best practices.

Step-by-Step SOP to Maintain Fixed Asset Register India SME

Step 1: Asset Acquisition and Initial Recording

Capture asset details from the PO stage, then validate the vendor bill, GSTIN, invoice particulars, and ITC eligibility at booking. Flag blocked credits early.

Step 2: Asset Tagging and Location Recording

Assign a unique ID, affix tags or barcodes, click photographs of high value items, and record precise location and custodian acknowledgments.

Step 3: Put-to-Use Confirmation

Obtain written confirmation from the user department, then start depreciation from that date. This step protects against premature depreciation.

Step 4: CWIP Capitalization

Park construction and installation costs in CWIP, review monthly, and capitalize immediately upon readiness with approvals.

Step 5: Monthly Depreciation Run

Compute monthly depreciation, pro rate for partial months, and post journals with asset wise workings retained.

Step 6: FAR to GL Reconciliation

Reconcile gross block, accumulated depreciation, and net block every month. Investigate exceptions the same week.

Step 7: Asset Movements and Modifications

Process transfers via requests, capitalize major upgrades, expense routine maintenance, and compute GST effects on disposals, including Section 18(6) reversal.

Step 8: Physical Verification

Perform annual verification for all assets, more frequent for critical items. Use barcodes, compile variance reports, and obtain management sign offs.

Step 9: Period-End Review

Run additions, deletions, depreciation, and movement reports. Investigate negative NBV, and assess fully depreciated assets for disposal or continued use.

Step 10: Audit Preparation

Maintain a standard audit file, see this audit readiness and evidence pack. Prepare continuity schedules, keep title deeds and insurance handy.

Process reference: FAR and GL R2R process in India, why a FAR is needed, and FAR for smoother operations.

Practical Depreciation Calculation for Indian Context

Book Depreciation

Use Schedule II lives unless justified otherwise. Example: cost ₹10,00,000, residual ₹50,000, life 10 years, SLM depreciation ₹95,000 annually, pro rate for partial periods.

Tax Depreciation

Apply WDV on blocks, observe the half year rule for additions. Example: 15 percent P and M block, first year addition gets 7.5 percent if used in the second half.

Deferred Tax Impact

Timing differences between book and tax depreciation create deferred tax assets or liabilities, track them consistently.

Additional Depreciation Claims

Manufacturing companies can claim additional 20 percent on new plant and machinery in the year of installation for tax only.

Depreciation on Revalued Assets

Higher depreciation on revalued amounts is not tax deductible, maintain separate tracking. For worked examples, see this practical overview.

GST Implications for Fixed Asset Management

Understanding Blocked Credits

Section 17(5) blocks ITC on specific items like certain motor vehicles and construction of immovable property. When blocked, add GST to asset cost.

ITC Eligibility Documentation

Ensure invoice compliance, vendor GSTIN, and 2B matching. Use GSTR-2B reconciliation tools overview to reduce mismatches. For capital goods, full ITC is allowed subject to rules.

Reversal on Asset Disposal

Compute Section 18(6) reversal using remaining useful life in quarters, pay the higher of tax on transaction value or ITC reversal where applicable.

Common Adjustments Scenarios

- Unregistered buyer sales still need GST per rules.

- Scrap sales attract GST, reversal still applies.

- Insurance settlements may have GST nuances, document the basis.

Rule 43 for Common Credits

When assets serve both taxable and exempt supplies, apportion ITC and maintain workings. A useful explainer is in this R2R best practices note.

Internal Controls and Audit Best Practices

Authorization Matrix

Set approval thresholds, segregate duties, and retain documentary trails across procurement to capitalization.

Maker-Checker Controls

Institute maker checker for asset setup, disposals, and write offs, and add a third reviewer for high value or technical evaluations.

Monthly Reconciliation Process

Reconcile FAR to GL every month, test depreciation calculations by sampling, and resolve exceptions quickly.

Physical Verification Procedures

Rotate teams, leverage scanners or mobile apps, document conditions, and track ghost or missing assets with evidence.

Exception Reporting

Monitor fully depreciated assets in use, assets with no depreciation, CWIP older than one year, and idle assets for impairment or disposal.

Audit Trail and Compliance Monitoring

Maintain organized source documents, change logs, and standard audit packs, review regulatory updates regularly. See FAR maintenance insights and GL and FAR control practices.

Tools and Software for Fixed Asset Management

Excel-Based Solutions

Practical for small portfolios under 100 assets with locked templates, validation, and automated calculations, but limited controls and scalability.

Accounting Software Solutions

- AI Accountant automates bill ingestion with GSTIN capture, capex flagging, FAR creation, depreciation, GST reconciliation, and GL sync, ideal with Zoho Books or Tally.

- Zoho Books supports categories, depreciation automation, and reporting.

- Tally Prime handles book and tax depreciation with Schedule II alignment.

- QuickBooks offers an add on for barcodes and depreciation scheduling.

- SAP Business One provides componentization, revaluation, and robust controls for larger SMEs.

Specialized Asset Management Systems

Use when you need barcode printing, mobile verification, maintenance scheduling, and deep analytics. Ensure seamless accounting integration to avoid duplicate data entry.

Implementation Best Practices

- Clean data migration with verified opening balances and accumulated depreciation.

- Team training, process documentation, and tested backups.

Common Mistakes to Avoid

Capitalization Errors

Expense routine maintenance, capitalize only improvements that extend life or capacity, document judgments.

Put-to-Use Date Issues

Start depreciation on readiness for use, not on purchase, and retain department confirmations.

GST Credit Mistakes

Do not claim blocked credits, compute Section 18(6) reversal on disposals, and track ITC eligibility at asset setup.

Depreciation Calculation Errors

Never mix book and tax schedules, componentize significant parts, and reassess lives when conditions change.

Documentation Gaps

Keep invoices, insurance, and physical verification evidence tidy and retrievable.

Reconciliation Lapses

Perform monthly FAR GL matching, investigate negative NBV and old fully depreciated assets still on books.

For structured guidance, refer again to FAR maintenance insights and India R2R FAR practices.

Quick Reference Checklists

Monthly FAR Closing Checklist

- Run depreciation, verify new asset put-to-use dates.

- Post journals with schedules, reconcile FAR to GL.

- Review exceptions, update transfers, disposals, and CWIP capitalization.

- Publish capex utilization and key movement reports.

Asset Disposal Checklist

- Secure approvals, compute NBV, and gain or loss.

- Calculate Section 18(6) GST reversal, raise tax invoice.

- Remove from FAR, post entries, update insurance and stakeholders.

Physical Verification Checklist

- Latest FAR extract by location, cross check via tags or barcodes.

- Record condition, document variances with photos, investigate promptly.

- Identify ghost assets, obtain approvals for write offs and adjustments, update FAR and issue a completion certificate.

Year-End Audit Preparation Checklist

- Continuity schedules, detailed FAR, depreciation policy.

- Invoice files for additions, title deeds, and updated insurance.

- CWIP aging and status, physical verification reports and actions.

- GST ITC claimed versus reversed reconciliation, board approvals for major capex.

FAQ

How should a CA differentiate between the FAR and the fixed asset schedule for statutory reporting?

The FAR is an asset wise operational database with serial numbers, locations, custodians, cost components, and depreciation settings, while the schedule is a category wise summary for financial statements. The totals must reconcile, but only the schedule goes to the notes to accounts.

For an SME client, when is Excel acceptable for FAR and when must I recommend software?

Excel works for simple portfolios under 100 assets, with stable processes and low transaction volume. If your client needs maker checker controls, audit trails, barcode verification, tax and book depreciation automation, or frequent transfers and disposals, move to an accounting module or an automation layer like AI Accountant.

What evidence should I insist on for put-to-use dates during audit?

Department head confirmations, installation reports, commissioning certificates, photographs for high value assets, and email trails. For software, capture license activation logs or go live sign offs. The put-to-use date governs book depreciation start.

How do I reconcile book depreciation with tax depreciation for deferred tax working papers?

Maintain parallel schedules, one per asset for books, and one per block for tax. Compute timing differences per asset category, aggregate, and apply the enacted tax rate to compute deferred tax. Document assumptions, component lives, and any revaluations.

What are the top GST checkpoints a CA should review in the FAR?

ITC eligibility flag per asset, Section 17(5) blocked items added to cost, Section 18(6) reversal workings for disposals, Rule 43 apportionment for common credits, and GSTR-2B reconciliation evidence for capital goods claims.

How do I advise on componentization thresholds and documentation?

Set a policy trigger around 10 percent of asset cost or where useful life materially differs. Maintain technical assessments, vendor specifications, and cost allocation workings. For buildings, separate structure, electricals, elevators, and fit outs.

When should improvements be capitalized versus expensed, with an example?

Capitalize if the expenditure increases capacity, enhances performance, or extends useful life. For example, replacing a CNC controller that boosts throughput and extends life is capex. Routine bearing replacements or filter changes are expense. Tools like AI Accountant can route approvals based on your capex policy.

What specific CARO 2020 procedures should I put in the client’s SOP?

Annual physical verification with coverage and frequency defined, title deed verification for immovable properties, reconciliation of material discrepancies, and documentation of revaluation policy if applied. Maintain maker checker logs for FAR changes.

How should leased assets be handled in FAR under Ind AS 116?

Record right of use assets with lease term, discount rate, and commencement date, depreciate over the shorter of useful life or lease term, and maintain a link to the lease liability amortization. For a refresher, see Ind AS 116 complete summary.

What controls prevent FAR GL mismatches in fast growing SMEs?

Lock the GL to post fixed asset entries only through approved FAR workflows, run monthly reconciliations, use maker checker for setups and disposals, and generate exception reports for negative NBV, zero depreciation, and CWIP ages over one year. Automation in AI Accountant helps enforce these controls.

How do I compute and evidence Section 18(6) ITC reversal on disposal during audit?

Apply the formula using original ITC and remaining life in quarters, compute reversal and compare with GST on transaction value, book the higher as liability. Retain calculation sheets, disposal approvals, invoice copy, and FAR update logs.

What is a practical monthly close sequence for assets that I can hand to clients?

Finalize additions and put-to-use, run depreciation, post journals, reconcile FAR to GL, process transfers and disposals with GST effects, review exceptions, and publish management reports. A lightweight automation layer like AI Accountant can generate workings and journals on schedule.

Moving Forward with Your Fixed Asset Register

Fixed asset register maintenance India is a continuous discipline. Start with a status check, reconcile FAR to GL, confirm put-to-use dates, and clear CWIP backlogs. Document policies, standardize your SOP, and train your team.

Adopt tools that enforce controls and save time, whether that is enhanced Excel templates or an automation platform such as AI Accountant. With consistent processes, you convert FAR from a compliance chore into a strategic asset intelligence layer that withstands scrutiny and informs better capital decisions.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.

.png)