-01%201.svg)

Key takeaways

- CA led Virtual Accounting gives founders and finance heads investor ready books, the CA team does the work end to end, the AI dashboard is for visibility, tracking, and comfort.

- The dashboard surfaces reconciliations, filings, notices, tie outs, and risks, while Chartered Accountants deliver bookkeeping, GST, TDS, income tax, payroll, and compliance.

- A due diligence accounting checklist, adapted into an operating routine, produces consistent evidence, fewer surprises, and faster deals, see the financial due diligence overview.

- Revenue recognition, receivables, inventory, tax, controls, and normalization are tested on an agreed cadence, supported by working papers, and documented adjustments, guided by the due diligence checklist.

- Indian specific risks, GST and TDS gaps, revenue cut off errors, weak reconciliations, and notices or penalties, are actively monitored with AI prompts and CA review.

Why CA led Virtual Accounting with AI dashboards

Founders want financial clarity, investors want evidence they can trust. In our CA led Virtual Accounting model, Chartered Accountants operate your books, taxes, and compliance, while an AI dashboard gives you live visibility into status and risk. The result is clean numbers, faster decisions, and fewer surprises.

You never have to do accounting yourself, you approve, you monitor, and you focus on growth, the CA team handles the entries, reconciliations, returns, and notices.

Managed, not DIY, your CA team delivers the work, the dashboard simply shows progress, tie outs, alerts, and next steps.

This approach aligns with investor expectations documented in the financial due diligence overview and the M and A due diligence checklist, consistency and evidence build trust.

Service scope and responsibilities

Your CA team covers the full finance backbone so the dashboard can surface status clearly:

- Bookkeeping and monthly close, trial balance and general ledger integrity.

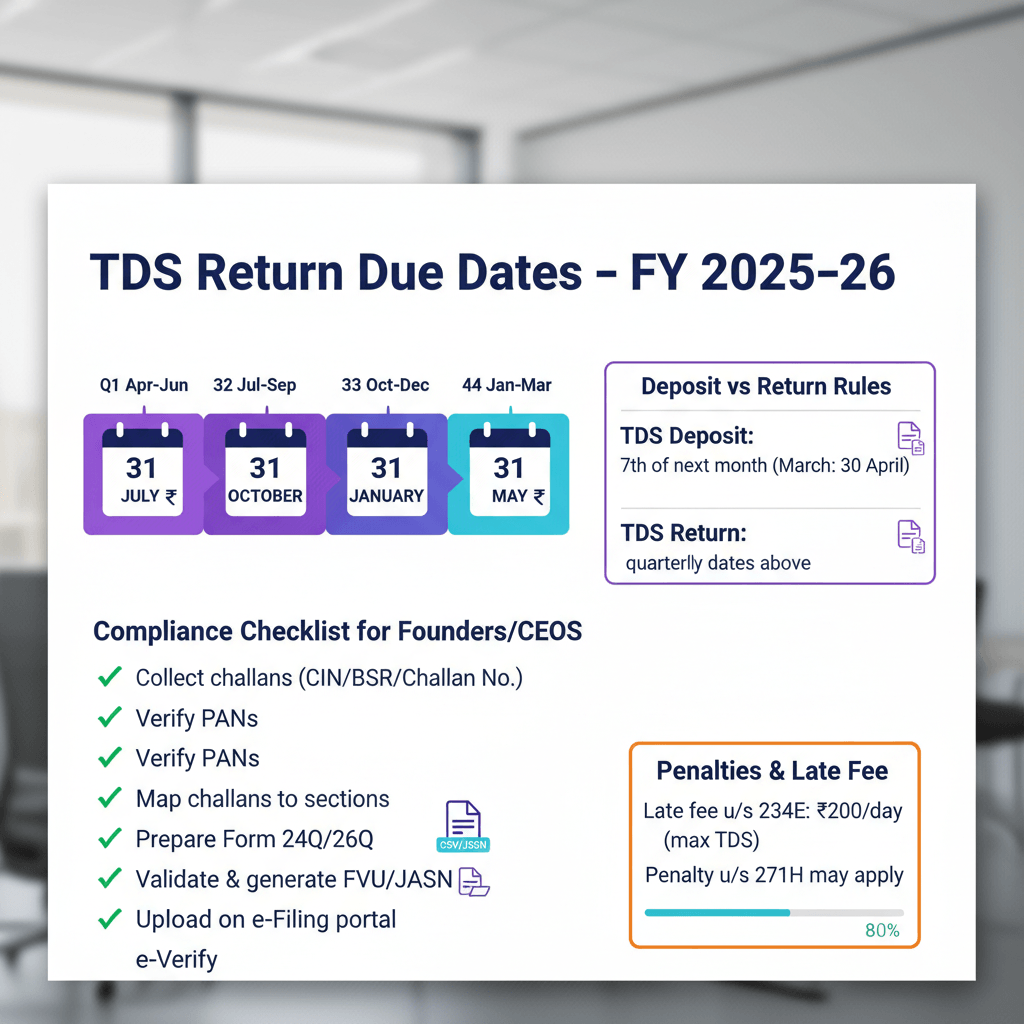

- Indirect tax, GST returns, reconciliations, input tax credit validation.

- Direct tax, TDS and TCS schedules, deposits, corporate income tax filings.

- Payroll, PF and statutory dues, Section 192 withholding, leave accruals.

- Compliance, board minutes, cap table changes, debt and leases, policies.

Each area is backed by a documented checklist, sampling plans, and reconciliation routines derived from the due diligence checklist and the financial due diligence overview.

AI dashboard for visibility, not DIY accounting

The dashboard summarizes what your CA team has completed, what is pending, and where exceptions exist, so you can track progress without touching the ledgers:

- Status tiles for bank reconciliations, AR and AP tie outs, GST and TDS filings, notices and responses.

- Evidence links, sample selections, exception logs, and proposed adjustments aligned to materiality.

- Controls health, monthly reconciliation cadence, and aging risks flagged for review.

The dashboard is a window, not a workspace, founders do not post entries, approve returns, or build schedules, your CA team does all of that, then the dashboard shows proof.

For best practice references, see the financial due diligence overview.

Due diligence checklist as an operating system

We convert the traditional due diligence accounting checklist into a steady state operating routine. It prevents drift, catches risks early, and keeps books investor ready, grounded in the due diligence checklist and the financial due diligence overview.

Purpose and scope of an accounting due diligence checklist

We use a structured approach that defines what to check, how to check, and how to document proof, the aim is investor ready books backed by evidence. Research supports this approach, see the financial due diligence overview, the due diligence checklist, and the M and A due diligence checklist.

Define review period, accounting framework, and materiality

We set the period under review, the accounting framework, and materiality thresholds upfront, this stops scope creep and sharpens focus. Guidance is aligned to the due diligence checklist and how to conduct financial due diligence.

- Typical scope, three to five years of annuals, with monthly detail for the latest twelve to twenty four months.

- Framework, Ind AS or Indian GAAP, IFRS or US GAAP, documented policy differences and their impact.

- Materiality, a percent of revenue or operating profit, plus qualitative factors like compliance and covenants.

Pre review document collection

Testing stalls when documents are missing, the dashboard shows collection status and gaps, the CA team assembles the pack before testing. See the financial due diligence overview and the due diligence checklist.

- Trial balances, general ledgers, audited statements, and recent management accounts.

- Bank statements, key invoices, top customer contracts, debt agreements, cap table.

- Tax returns, GST, TDS and TCS challans, fixed asset register, and inventory records if relevant.

Initial tie outs and reconciliations

Line by line tie the financial statements to the trial balance, confirm opening to closing continuity, and reconcile sub ledgers to control accounts. References, the financial due diligence overview and the due diligence checklist.

Revenue recognition testing

Obtain and document the policy, test samples for Ind AS 115 or IFRS 15 alignment, and perform cut off tests around period end. Guidance in the financial due diligence overview and the due diligence checklist.

Accounts receivable checks

Reconcile AR aging to the balance sheet, assess ninety plus day buckets, test allowance adequacy, and verify subsequent receipts. Details in the due diligence checklist and the financial due diligence overview.

Inventory and cost of sales checks

Confirm valuation method, assess obsolescence, verify physical count procedures, and analyze costing consistency, aligned to the financial due diligence overview and the due diligence checklist.

Fixed assets and depreciation checks

Reconcile the fixed asset register, confirm capitalization thresholds, test useful lives, and review disposals and impairment indicators, guided by the financial due diligence overview and the due diligence checklist.

Accounts payable and accruals checks

Reconcile AP to the aged listing, verify accrual policies, and perform subsequent payments testing, see the due diligence checklist and the financial due diligence overview.

Cash and bank checks

Obtain bank reconciliations, tie bank statements to the ledger cash balance, and investigate old reconciling items, see bank statement analysis and the financial due diligence overview.

Debt and leases checks

Prepare and reconcile debt schedules, recalculate interest, test covenant compliance, and classify leases under Ind AS 116. References, the financial due diligence overview and the due diligence checklist.

Equity and share based payments checks

Reconcile the cap table, confirm share class rights, test ESOP expense recognition, and review dividends and retained earnings continuity, using the due diligence checklist and the financial due diligence overview.

Tax compliance checks, India specific

Reconcile GST returns to the ledger, validate input tax credit eligibility, track TDS and TCS deposits and sections, and reconcile corporate tax filings to financials. See GST compliance services in India and the financial due diligence overview.

Payroll and benefits checks

Reconcile payroll registers to the ledger, review bonus policies and leave accruals for Ind AS 19, and validate PF and statutory contributions. See Payroll compliance support, Section 192 and the financial due diligence overview.

Related party transactions checks

Identify related parties, assess arm’s length pricing, verify approvals, and confirm disclosures per Ind AS 24, guided by the financial due diligence overview and the due diligence checklist.

Provisions and contingencies checks

Assess warranty accruals, evaluate litigation likelihood, identify contractual obligations, and validate estimates, aligned with the financial due diligence overview and the due diligence checklist.

Revenue quality and earnings normalization checks

Identify non recurring items, owner specific expenses, normalize EBITDA and key metrics, and document adjustments with support, based on the financial due diligence overview and the due diligence checklist.

Foreign currency and consolidation checks

Confirm Ind AS 21 translation policies, validate closing and average rates, and verify complete eliminations, tied to the financial due diligence overview and the due diligence checklist.

Subsequent events review

Review minutes and updates after the balance sheet date, classify events as adjusting or non adjusting, and reflect or disclose as needed, see the financial due diligence overview.

Internal controls evidence review

Assess segregation of duties, approval thresholds, and monthly reconciliation routines, document control deficiencies and compensating controls, aligned to the financial due diligence overview and the due diligence checklist.

Common red flags and deeper testing

Watch for persistent breaks between sub ledgers and control accounts, aggressive revenue cut off near period end, and odd credit terms, triggers for expanded testing are described in the financial due diligence overview.

Documentation of findings

Maintain a master checklist, cross reference working papers, keep exception logs, and summarize proposed adjustments with quantified impact. See the due diligence checklist and the financial due diligence overview.

Key takeaway, a rigorous checklist across statements, taxes, controls, and normalization surfaces material risks and inaccuracies early, producing investor ready books, see the financial due diligence overview.

FAQ

What does CA led Virtual Accounting mean, who actually does the accounting work

CA led Virtual Accounting means a Chartered Accountant team operates your full finance function, they post entries, close books, reconcile accounts, file GST and TDS, handle payroll and income tax, and respond to notices. You get an AI dashboard for visibility and tracking, but you do not do the accounting yourself. Services like AI Accountant demonstrate this model, the dashboard shows progress and risks, the CA team delivers outcomes.

How does the AI dashboard help if my founders and finance heads are not doing DIY accounting

The dashboard gives live status on reconciliations, filings, and exceptions, so leadership can see what is complete, what is pending, and what needs approval. It aggregates evidence links, tie outs, and adjustments, making diligence ready documentation easy to review. The dashboard is a window, not a ledger, your CA team does the work, the dashboard keeps you informed.

Which processes are covered, bookkeeping, GST, TDS, payroll, and income tax

Scope includes bookkeeping, monthly close, bank and GL reconciliations, GST returns and input tax credit validation, TDS and TCS scheduling and deposits, payroll registers and PF compliance, Section 192 withholding, corporate income tax filings, and compliance support. The CA team owns execution, the dashboard offers visibility on status and exceptions.

Will the CA team use a due diligence checklist during monthly operations, or only during a deal

The due diligence checklist becomes an operating routine, it is used every month to structure tie outs, testing, and documentation. This produces investor ready books continuously, not just at deal time. It reduces surprises, improves audit readiness, and speeds financing and M and A.

How is revenue recognition tested in a managed service, can the dashboard show cut off risks

Your CA team documents the policy, tests transaction samples, and runs cut off procedures around period end. The dashboard then shows test coverage, exceptions, and remediation status, so you can track progress without doing the work yourself. This aligns with Ind AS 115 or IFRS 15, and supports investor reviews.

Can AI Accountant handle India specific GST and TDS reconciliations, including ITC eligibility checks

Yes, AI Accountant exemplifies India specific workflows, GST reconciliations to the ledger, input tax credit eligibility checks, and TDS and TCS deposits are managed by the CA team. The dashboard surfaces filing status, variances, and notices, so founders see risk early while professionals execute corrections.

What evidence will investors expect during diligence, and how is it organized

Investors expect tie outs from statements to the trial balance, reconciled sub ledgers, policy documentation, sampling results, exception logs, and quantified adjustments. The CA team maintains a master checklist, working paper index, and exception tracker, the dashboard provides links and summaries for quick review.

How do you handle AR aging, old balances, and allowance for doubtful debts

The CA team reconciles AR aging to the balance sheet, flags ninety plus day buckets, checks subsequent receipts, and recalculates allowance based on historical loss patterns. The dashboard shows high risk customers, pending credit notes, and allowance impact, while the CA team executes write offs or collection plans.

What controls are evaluated, and how does the dashboard reflect control health

Controls across authorization, recording, and reconciliation are assessed, including segregation of duties, approval thresholds, and monthly reconciliation routines. Control deficiencies and compensating controls are documented by the CA team, the dashboard displays control health indicators and alerts when a control is overdue or failed.

Will my finance team need to learn new tools, or can we stay on our current ERP and banks

You can keep your ERP and bank platforms, the CA team operates within your stack. The AI dashboard connects through exports and secure feeds to summarize status, evidence, and alerts. Founders and finance heads do not need to learn ledger workflows, they simply review dashboard status and approve where needed.

How is materiality defined for monthly testing, and can we adjust thresholds over time

Materiality is set collaboratively, using quantitative thresholds, such as a percent of revenue or operating profit, and qualitative factors, such as compliance or covenants. Thresholds can be adjusted as scale changes, the dashboard shows the current parameters and how they drive sampling and adjustments.

What happens when red flags appear, for example aggressive revenue cut off or unreconciled balances

Red flags trigger deeper testing, larger samples, and focused remediation plans. The CA team executes the work, documents findings and fixes, and proposes adjustments if needed. The dashboard elevates priority, shows owners and timelines, and keeps leadership informed until closure.

Can CA led Virtual Accounting shorten audit cycles and speed fundraising

Yes, continuous evidence, reconciliations, and normalization create investor ready books. Auditors get a clean index of working papers, investors see stable metrics and documented adjustments, and fundraising or M and A moves faster. The dashboard provides the roadmap, while your CA team maintains the artifacts.

How are bank reconciliations monitored, and what about old reconciling items

Monthly bank reconciliations are prepared by the CA team, outstanding cheques and deposits in transit are verified, and old reconciling items are investigated and cleared. The dashboard highlights items older than a month, assigns owners, and tracks resolution, keeping cash accuracy high.

Do you support leases under Ind AS 116, and covenant tracking on debt

Yes, debt schedules, interest calculations, and fee amortization are maintained, covenant compliance is tracked and documented. Leases are identified, classified, and measured under Ind AS 116, with right of use assets and lease liabilities reconciled. The dashboard shows covenant status and lease updates, while the CA team does the calculations.