Key takeaways

- A structured data retention policy in India protects CA firms and finance teams, it balances statutory requirements and the DPDP Act’s deletion-first mandate.

- Align retention with the strictest rule across Companies Act, Income Tax, and GST, most core finance records are safe at eight years, GST records need at least seventy two months from annual return due date.

- Access logging is non negotiable under DPDP, capture user, timestamp, action, and IP, keep logs for at least one year, preferably aligned with financial record retention.

- Implement formal redaction and purge workflows, verify eligibility, obtain approvals, execute deletion across systems and backups, issue destruction certificates, and update registers.

- Legal holds suspend deletion immediately, preserve scope precisely, document chain of custody, and release holds only after written resolution confirmation.

- Client offboarding demands full export, immediate access revocation, retention scheduling, and meticulous documentation.

- Automation tools, including AI Accountant, Zoho Books, and Tally, help standardize retention, audit trails, reconciliation, and evidence preservation.

What is a Data Retention Policy in the Indian Context

A data retention policy India is your organization’s rulebook for managing data from collection to deletion. It defines what happens to every invoice, GST return, bank statement, and audit file, from day one until the day you purge it. For CA firms and SME finance teams, the policy spans GST data, purchase bills, sales invoices, reconciliations, audit workpapers, and system access logs, it also covers the data flowing through Zoho Books and Tally.

The core principles are simple and powerful. Purpose limitation ensures you retain data only for specific legal or business needs, storage limitation requires deletion once the purpose ends or consent is withdrawn, data minimization keeps storage lean and defensible. Your lawful bases must align with DPDP consent and legitimate uses, and your practices must stand up when Income Tax or GST officers review your records.

When the policy removes guesswork, teams stop debating whether to keep that old invoice, they follow defined timelines and actions, confidently.

For background and implementation guidance, see the DPDP compliance guide, the DPDP Act Phase 1 overview, and the DLA Piper India data protection overview.

Understanding the Regulatory Landscape Driving Retention Periods

Indian businesses navigate overlapping laws with different retention timelines. The Companies Act 2013 sets an eight year baseline for books of account, Income Tax assessments typically require six to eight years, transfer pricing can stretch beyond ten years, GST mandates records for seventy two months from annual return due date, extended during proceedings, investigations, or audits.

The DPDP Act 2023 brought into force flips traditional retention thinking, retain only while the purpose exists, delete when the purpose ends or consent is withdrawn, unless another law requires retention. The emerging DPDP Rules 2025 and the DPDP Rules 2025 overview indicate minimum one year retention for access and processing logs, creating an audit trail while honoring deletion mandates.

Full DPDP implementation targets May twenty twenty seven, systems need retention workflows, deletion mechanisms, and automation now. Map each data category to the strictest rule, build deletion flows that fire as periods end, skip buffer zones and just in case archives.

For deeper context, review the DPDP Act Phase 1 overview, the DPDP compliance guide, and the DLA Piper India data protection overview.

Practical Retention Periods for Finance Teams, Your Cheat Sheet

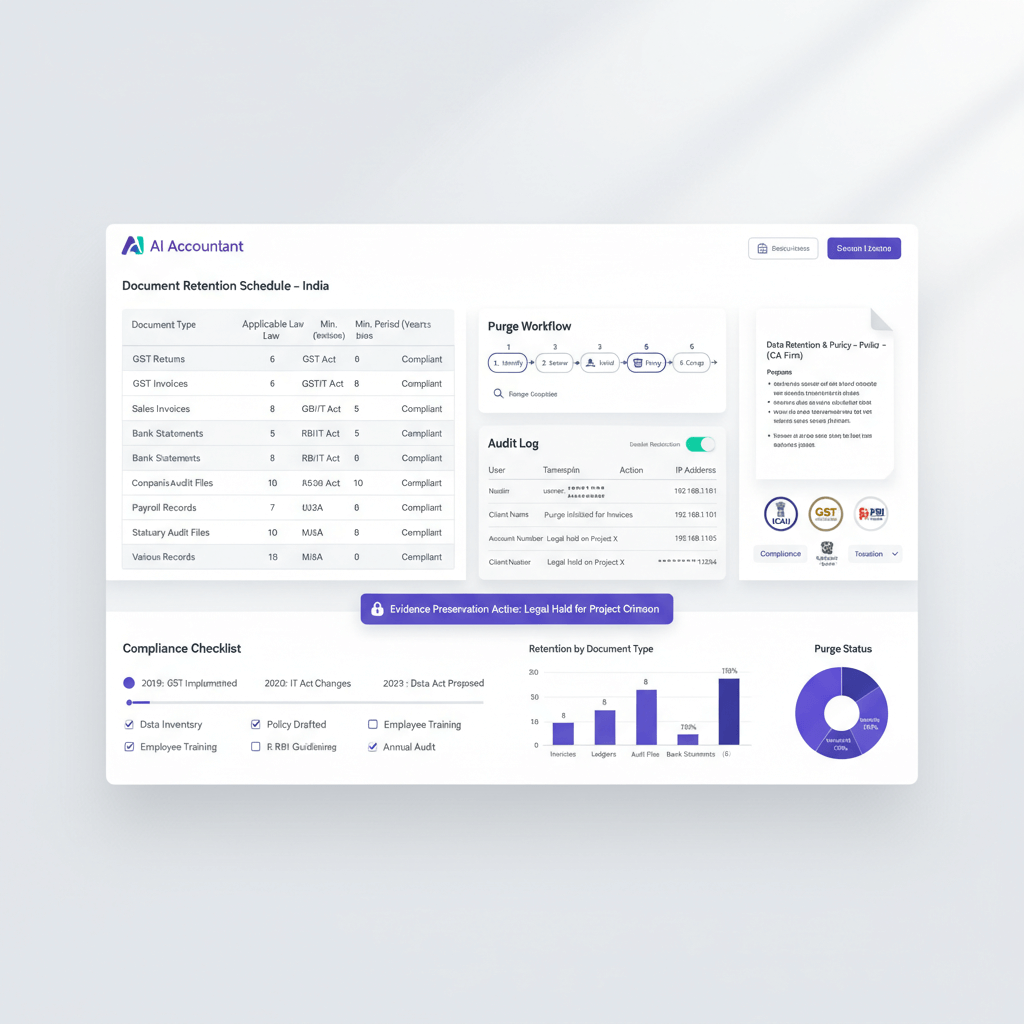

Set retention by the strictest applicable law for each document type. Financial statements and books of account, eight years under Companies Act, purchase registers, vendor bills, credit and debit notes, and journals, eight years for Income Tax, at least seventy two months for GST. Sales invoices, receivables ledgers, and contracts, eight years, extend while disputes remain unresolved. Bank and card statements and reconciliations, eight years.

GST working files, GSTR 2B downloads, reconciliation worksheets, and return copies, seventy two months from annual return due date, practically align to eight years for simplicity. Audit working papers and management letters, eight years, extend under legal holds. Access logs and audit trails, minimum one year under DPDP, align with related financial record retention for defensibility.

- Backups, match primary record retention, automate expiry for archival backups.

- Drafts versus finals, drafts may need only one year, finals require full statutory retention, keep both original and amended GST versions.

- Configure accounting platforms to enforce retention, align deletion automation with policy.

For guidance, see the DPDP compliance guide and the DPDP Act Phase 1 overview.

Implementing Access Logging for Accountability

Access logging is your accountability backbone under DPDP and during audits. Capture user ID, timestamp, record type, action performed, IP address, and device where possible. In Zoho Books, enable audit trails and user activity reports, configure role based access. In Tally, activate audit and security controls. Document repositories need version history and access reports.

If you use automation platforms like AI Accountant, ensure comprehensive logs of all processing activities. Keep logs immutable, store separately from monitored systems, and back them up. Logs should be immutable once written, prefer write once storage.

Retain logs for minimum one year under DPDP, practically align with the eight year financial record schedule where defensibility is needed. Review logs quarterly for anomalies, integrate with internal audits, and keep employees informed to reinforce accountability.

When logs tell the full story, you can prove who accessed what, when, and why, even years later.

Reference materials include the DPDP compliance guide, the DPDP Act Phase 1 overview, and the DPDP Rules 2025 update.

Redaction and Purge, Safely Deleting Financial Data

Redaction anonymizes sensitive elements while keeping records usable, purge deletes data completely. Start with eligibility, confirm retention period expiry, ensure no legal holds or audits apply, and check dependencies so deletions do not break linked records. Obtain stakeholder approvals, verify contract terms for post engagement retention.

Redact PAN, Aadhaar digits, and bank numbers, remove personal addresses while preserving amounts, tokenize card numbers, keep audit trails intact without privacy risk. Purge in primary systems, then backups, archives, cloud replicas, email attachments, shared drives, laptops, and shadow copies, verify completeness and issue destruction certificates, update data registers accordingly.

Under DPDP, automated deletion of personal data requires notifying affected individuals forty eight hours in advance, confirm applicability with counsel. Common pitfalls include partial deletes, forgotten exports, third party system copies, and missed production backups, test deletion end to end.

Use masking and tokenization tools, DLP for unauthorized copies, backup platforms to track and expire archives, understand cloud platform deletion behaviors before assuming data is gone. Schedule monthly, quarterly, and annual purge cycles, automate yet verify manually.

Learn more from the DPDP compliance guide, the DPDP Act Phase 1 overview, and the DLA Piper India data protection overview.

Mini checklist for redaction and purge

- Confirm eligibility, retention ended, no legal hold, dependencies mapped.

- Obtain owner approvals, document rationale, and authority.

- Execute redaction or purge, validate across systems and backups.

- Issue destruction certificate, update registers, and log completion.

Evidence Preservation and Legal Holds During Audits

Evidence preservation begins when normal deletion rules pause, a GST notice, Income Tax investigation, or litigation triggers a legal hold. Define scope precisely, include primary documents, supporting files, communications, and system logs, cast a wide net initially, narrow by relevance.

Notify IT to suspend automated deletions, alert department heads to preserve physical documents, and inform employees of responsibilities, use written notices to create an audit trail. Create immutable copies, record chain of custody, track access and any copies made, use hashing to verify integrity, encrypt data in transit and at rest.

For GST, preserve purchase registers, sales records, returns, reconciliations, and correspondence for the relevant period, the seventy two month rule extends until case closure. For Income Tax, preserve books, emails, bank statements, contracts, transfer pricing documentation, and any expanding scope materials. Temporary holds apply during statutory or internal audits, release holds only after completion and finalization, then resume normal retention and delete over retained data promptly.

Consult the DPDP compliance guide and the DLA Piper India data protection overview for frameworks and references.

Client Offboarding, Managing Data After Engagement Ends

Client offboarding tests your policy in the real world. Confirm scope in writing, what to transfer, formats, and whether historical records are needed. Export complete datasets, financials, tax returns, GST filings, working papers, provide PDF and native formats, include an index, obtain receipt acknowledgments.

Revoke access immediately, disable client logins, remove users from Zoho Books and Tally, revoke shared drive permissions, change shared passwords, block email forwards. Transfer ownership of client specific resources, document transitions and dates.

Schedule retention for retained items, financial records keep the eight year rule, working papers and drafts may have shorter retention, mark deletion dates. Map where client data resides, accounting systems, emails, shared drives, local copies, and messaging apps, and address special conditions such as litigation, unpaid fees, and investigations.

Create a formal offboarding checklist, assign responsibilities, set milestones, and track completion, document every action to prove compliance and reduce disputes later.

Further reading, the DPDP compliance guide and the DPDP Act Phase 1 overview.

Building Your Implementation Process with the Right Tools

Assign clear roles, compliance owns the schedule and data inventory, IT handles technical setup, department heads ensure procedures are followed. Automate wherever possible across your accounting and financial stack.

- AI Accountant, automates bill extraction, categorization, and GST reconciliation, maintains detailed audit trails, supports multi org and role based access, simplifies retention.

- QuickBooks Online, built in audit trails and backups, configurable retention by document types.

- Xero, comprehensive activity logging, integrates with document management for centralized control.

- Zoho Books, extensive audit trail capabilities, customizable retention settings aligned with Indian needs.

- FreshBooks, automatic backup and document storage, clear retention management options.

- Tally Prime, statutory compliance features with backup and restoration capabilities.

Drive efficiency with categorization, apply rules to document groups, embed access logging in all systems, enable version control, and activate database audit features. Create runbooks for redaction, purge, and legal holds, leverage read only roles, auto logout, two factor authentication, and export schedules aligned to policy. Test mock deletions, restore backups, verify access logs, and simulate legal holds. Map integrations with banks, GST portals, and payment gateways, understand their retention behaviors. Train teams continuously, set alerts for expiry, and monitor compliance, then refine based on lessons learned.

Helpful resources include the DPDP compliance guide and the DPDP Act Phase 1 overview.

How AI Accountant Streamlines Retention Management

Modern automation standardizes data flows and retention controls. AI Accountant reduces duplication and keeps bills, statements, and reconciliations consistent, it makes retention tracking predictable and auditable.

Its GST reconciliation module maintains detailed matching records against GSTR 2B, creating ready evidence if authorities raise queries years later. Multi organization workspaces simplify CA firm offboarding, export complete datasets, revoke access, and schedule deletions without impacting other clients, while role based permissions keep access tight.

Sync with Zoho Books and Tally reduces data copies, redaction and purge become centralized and reliable. ISO 27001 and SOC 2 verification provide confidence in logging and security controls, detailed logs integrate with your compliance framework and support audits. Dashboards highlight aging items, unreconciled periods, and approaching retention limits, the same retention discipline scales from small to very large volumes.

For context and best practices, revisit the DPDP Act Phase 1 overview and the DPDP compliance guide.

Sample Data Retention Policy Template and Checklist

Policy Statement, our organization manages data retention in compliance with Companies Act 2013, Income Tax Act, CGST Act, and the Digital Personal Data Protection Act 2023, we retain data only as long as legally required or business necessary, then securely delete it.

Retention Schedule, financial statements and books, eight years, purchase and sales records, eight years, minimum seventy two months for GST, bank and card statements, eight years, GST returns and reconciliations, seventy two months from annual return, audit papers, eight years, extend for legal holds, access logs, one year minimum, preferably aligned with related records, backups, match primary record retention.

Access Logging Requirements, capture user ID, timestamp, record type, action, IP address, retain at least one year under DPDP, review quarterly for anomalies, store immutably and separate from monitored systems.

Redaction and Purge Workflow

- Check eligibility against retention schedule.

- Verify no legal hold applies.

- Obtain documented owner approval.

- Execute redaction or purge and validate.

- Issue destruction certificate.

- Update data register.

- Verify deletion across systems and backups.

Evidence Preservation Procedures, trigger on legal notice, audit, or anticipated litigation, communicate in writing, suspend deletions for affected records, maintain chain of custody with checksums, release via written confirmation before resuming normal retention.

Client Offboarding Process

- Confirm data transfer requirements.

- Export complete datasets with index.

- Obtain receipt acknowledgment.

- Revoke all access immediately.

- Schedule retention per policy.

- Document all actions.

Annual Review Checklist

- Update retention schedule for law changes.

- Verify deletion procedures end to end.

- Test backup restoration.

- Review access logs and anomalies.

- Train staff on procedures.

- Audit compliance rates.

- Update technology configurations.

- Review third party data handling.

- Validate legal hold procedures.

- Check client offboarding completeness.

Implementation Timeline, month one, finalize policy and approval, month two, configure systems and tools, month three, train staff and run pilots, months four to six, phased rollout, months seven to twelve, monitor and refine, ongoing, quarterly reviews and annual updates.

Reference materials, the DPDP compliance guide and the DPDP Act Phase 1 overview.

Moving Forward with Your Data Retention Strategy

Building a robust data retention policy India is an ongoing commitment that evolves with regulations, technology, and business realities. Start by mapping data, setting retention periods, and implementing core processes, then refine through testing and audits. The May twenty twenty seven DPDP timeline is closer than it seems, configuration, training, and process validation take time.

Perfect is the enemy of good, prioritize high risk areas first, personal data and financial records, expand coverage steadily, document decisions, and learn from small pilots. The payoff arrives quickly, lower storage costs, faster audit responses, reduced compliance risk, and stronger client trust, your policy becomes an operational advantage.

Take the first step today, define one category’s retention, enable basic logging, schedule your first deletion, build momentum through small wins, and make retention management second nature.

FAQ

What is a data retention policy India, and which entities must maintain one

A data retention policy India defines how you store, access, and delete financial and personal data under Companies Act, Income Tax, GST, and DPDP. Every CA firm, SME, and any business handling such data must maintain a documented policy, otherwise you risk penalties for premature deletion or excessive retention. See the DPDP compliance guide and the DPDP Act Phase 1 overview.

How do GST and Income Tax retention periods interact for purchase and sales records

GST requires records for seventy two months from the annual return due date, Income Tax generally requires six to eight years, transfer pricing can exceed ten years. When both apply, follow the longer period to remain defensible during assessments.

What minimum access log requirements does DPDP imply for accounting systems

Capture user ID, timestamp, action performed, record type, and IP address, retain logs for at least one year. Practically, align logs to related financial records for stronger defensibility, build immutability and separation into your logging architecture.

How should a CA firm implement redaction and purge when retention expires

Verify eligibility, check legal holds, obtain approvals, execute redaction for partial removal or purge for complete deletion, validate across systems and backups, issue destruction certificates, and update your data register. Use automation where possible and audit deletion end to end.

Does DPDP require advance notice before automated deletion of personal data

Yes, DPDP expects notifying affected individuals forty eight hours before automated deletion of personal data. Coordinate with legal counsel to confirm applicability for customer or vendor data and ensure notifications are logged.

When do legal holds override the deletion schedule during audits or investigations

Legal holds start when you receive a notice or anticipate litigation, they suspend normal deletion immediately. Preserve relevant records, communications, and logs until written resolution confirmation, then resume retention and delete over retained data promptly.

How can AI Accountant assist a CA firm with retention, logging, and evidence preservation

AI Accountant standardizes data flows, maintains detailed audit trails, and provides GST reconciliation evidence that stands up during reviews. Multi organization workspaces simplify offboarding, role based access and immutable logs support DPDP and audit requirements.

What controls should we configure in Zoho Books and Tally to support retention compliance

Enable audit trails, enforce role based access, enable two factor authentication, configure session timeouts, and define export schedules that align with retention. In Tally, activate audit features and security controls, and ensure backups match your primary record retention.

How should backups be managed to avoid over retention and privacy risks

Match backup retention to primary records, differentiate active rotation from archival backups, set automated expiry, and verify deletion across all backup layers. Document restoration tests, and confirm that backup platforms purge data as scheduled.

What documentation proves compliant deletion and evidence preservation to regulators

Maintain destruction certificates, updated data registers, and deletion verification logs. For preservation, document chain of custody, hashing for integrity, access control lists, and written legal hold notices and releases, keep these artifacts as long as the underlying records remain.

How should a CA firm handle client offboarding while keeping statutory retention intact

Export complete datasets with an indexed manifest, obtain receipt acknowledgment, revoke access immediately, and schedule retention per policy. Document actions comprehensively, retain statutory records for the full period, and manage special cases like disputes or investigations with legal holds.

What is a practical first month plan to kick off a retention policy rollout

Finalize the policy statement and retention schedule, map high risk data categories, enable core access logging, and run a pilot deletion for a low risk category. Use AI Accountant or your accounting system to enforce audit trails and exports, then refine procedures based on pilot learnings.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.