Key takeaways

- Data privacy in AI accounting in India means embedding encryption, consent, field level masking, and audit trails directly into every financial workflow, not treating compliance as a separate checklist.

- The DPDP Act's 72 hour breach notification is already active, consent managers must be operational by November 13, 2026, and full compliance is enforceable from May 13, 2027, so CA firms and finance teams need to act now.

- Field level redaction keeps AP, bank reconciliation, and GST workflows moving while masking PAN, bank numbers, and other sensitive fields, reducing exposure without slowing operations.

- Multi org tenant isolation, role based access, MFA, and India cloud residency are non negotiable for CA firms managing multiple client books on a single platform.

- A practical 90 day roadmap (discovery, assessment, implementation) helps small and mid size firms phase in controls without heavy spend or disruption.

- AI Accountant supports these requirements with India cloud encryption, multi org isolation, field level masking, and automated GST reconciliation built for DPDP readiness.

Data Privacy in AI Accounting India: What's New in 2026

Until late 2025, the DPDP Act existed largely on paper. The Data Protection Board of India (DPBI) was not yet operational, and most CA firms treated compliance as a future task. That changed in November 2025 when the DPBI went live with complaint portals and enforcement infrastructure. The 72 hour breach notification obligation is now active, and penalties of up to ₹250 crore for serious violations are enforceable today.

The next hard deadline is November 13, 2026: consent managers must be operational. Only India incorporated entities with a net worth of at least ₹2 crore can register, and they must retain consent records for seven years. If your firm processes client PII through AI tools (bill extraction, statement ingestion, reconciliation), you need documented consent flows and the IT plumbing to support them before that date.

By May 13, 2027, everything else kicks in: standalone privacy notices, granular consent, data minimization, individual rights (access, correction, erasure), and mandatory processor contracts. This hits CA firms managing 10, 50, or 200 client entities especially hard, because every client relationship requires its own documented consent and processing basis.

What to do right now:

- Audit your current AI vendor agreements for DPDP aligned breach notification SLAs and processor contract terms.

- Map every workflow where PII is collected, stored, or shared, including bookkeeping automation pipelines and bank statement ingestion.

- Begin consent manager evaluation if your firm will act as a data fiduciary for client data.

Firms that wait until Q1 2027 will face a compressed timeline, rising vendor costs, and audit exposure. The regulatory intent is clear: build privacy into operations now, not after the first penalty notice.

What's Really at Stake When AI Meets Indian Accounting Data

Picture this. You are sipping chai while an AI tool processes hundreds of invoices, extracting GST details and vendor information. That convenience is powerful, yet the same automation expands your privacy risk surface.

Names, emails, GSTIN, PAN, bank account numbers, addresses, invoice line items, even bank statement narrations, can carry sensitive personal data. Non compliance under DPDP can mean penalties up to ₹250 crore per violation. Reputational damage can be worse than the fine. For a trust driven profession like CA practice, protecting client data is existential.

When AI touches every corner of your financial workflows, privacy is not a checkbox. It is operational resilience.

For a clear sense of public expectation and enforcement thinking, see the full text of the Digital Personal Data Protection Act, 2023 on MeitY's website.

Understanding the Regulatory Landscape: Compliance with IT Rules and DPDP Act

Compliance with IT rules under DPDP demands explicit, granular consent for specific processing purposes. You need standalone privacy notices, purpose limitation, data minimization, and documented processing records.

Consent managers must be operational by November 13, 2026. Full rules take effect by May 13, 2027. The 72 hour breach notification obligation is already active, and dual reporting may apply (for example, CERT-In requires a 6 hour notification for cyber incidents under its own rules).

For AI accounting workflows, integrations with systems like Tally need documented consent. GST reconciliation requires audit trails. Every data transfer must be justified and recorded.

- Consent managers require India incorporation, a minimum net worth of ₹2 crore, operational governance, and seven year consent record retention (2026 update).

- Processing records and privacy impact assessments are not optional. They are mandatory.

- AI vendors are data fiduciaries or processors. They must align with your compliance posture, and processor contracts become mandatory by May 2027.

Deepen your understanding with the Fisher Phillips analysis of India's new data privacy rules and the IAPP update on DPDPA rules taking force.

Principle 1: Implementing Robust PII Protection

PII in Indian accounting includes names, emails, GSTIN, PAN, bank account numbers, addresses, and government issued identifiers. Start with data minimization. Collect only what is essential.

Continue with purpose limitation. Use data strictly for the declared use. Encrypt data at rest and in transit. Tokenize PAN or bank numbers to reduce exposure. Deny raw PII in any model training unless you have explicit consent and robust pseudonymization.

- Vendor due diligence checklist: AES 256 at rest, TLS 1.3 in transit, documented data flows, confirmation that PII is excluded from training datasets, breach response protocols with clear SLAs aligned to 72 hours.

Under the DPDP framework, data fiduciaries are liable for their processors. This means your firm owns the risk even when the AI vendor handles the data. Contracts must specify safeguards, and periodic third party audits strengthen your position.

Useful references: the PrimeInfoserv DPDP compliance strategy for the May 2027 deadline and the Onfra guide to what you need to do before May 13, 2027.

Principle 2: Mastering Field Level Redaction

Field level redaction masks only sensitive values while preserving operational utility. Your AP team can view vendor details without full PAN. Display PAN****5678. Dashboard users can see cash flow without full bank numbers. Exports for management can omit unmasked salary account details.

Configure rules per role and per organization. Allow authorized reveal with justification. Record immutable audit trails for every reveal action.

Plan for edge cases. Error reports, support tickets, and screenshots can inadvertently expose sensitive fields. Bank narrations can contain phone numbers or Aadhaar fragments. Apply pattern based redaction to narrations before storage and display.

For broader context on enforcement timelines and public expectations, review the DPDP Act text published by MeitY.

Principle 3: Building Strong Access Controls

Access controls are your defensive perimeter. Use role based access with least privilege. Add MFA, SSO, IP restrictions, and time bound vendor access. Monitor rigorously.

Multi org isolation is essential for CA firms. Client A data must be invisible to Client B users, with no exceptions. This is not just good practice. Under DPDP, inadequate access segregation exposes you to penalties for unauthorized processing.

- Operational practices: real time alerts for unusual downloads, weekly access pattern reports, monthly permission reviews, quarterly privileged account audits.

- Practical scenarios: temporary elevated month end access with automatic expiry, time boxed read only accounts for external auditors, new joiners starting fresh with role appropriate permissions.

For a structured view of cross border risk and governance, see the Fisher Phillips guidance on India's DPDP rules and cross border considerations.

Principle 4: Ensuring Data Residency in India Cloud

Data residency in India cloud simplifies DPDP compliance, improves latency, and enhances client confidence. Keep hot data, backups, disaster recovery copies, ML artifacts, logs, and audit trails inside India regions.

When cross border processing is necessary, strip PII, document the purpose, and obtain explicit consent. DPDP does not universally mandate India only storage. However, many contracts (especially government and PSU engagements) require India residency. Risk assessments often conclude that India residency simplifies compliance and avoids cross border uncertainty.

- Vendor questions to ask: which India regions are used, can they provide locality proofs, failover behavior, controls to restrict cross border flows, data residency certificates, and whether support and analytics are processed locally.

Explore the PrimeInfoserv overview of localization and compliance strategy.

Making Compliance with IT Rules Work in Real AI Accounting Workflows

Bill ingestion workflow

Present clear consent notices before uploads. Explain specific processing uses. Retain invoices for seven years for GST, then auto delete.

Bank statement processing

Purpose limit to reconciliation. Do not reuse narrations for analytics without fresh consent. Redact narration strings that contain personal information, phone numbers, or Aadhaar fragments before storage.

GST reconciliation

Constrain data use to compliance. Mask non essential fields. Maintain verifiable audit trails showing who accessed what and why. Automated matching of GSTR 2A/2B with purchase registers should operate on masked data wherever possible.

Dashboard generation

Aggregate and anonymize. Overview dashboards should not surface per transaction PII. Filter by role so that each user sees only the data relevant to their function.

Document processing activities. Run VAPT audits. Enable grievance channels. Ensure standalone privacy notices and one click consent withdrawal. For regulatory context, read the IAPP coverage of final DPDPA rules taking force.

Hidden Privacy Pitfalls in Indian Accounting Contexts

Accounting data often hides sensitive details. Invoice PDFs can contain phone numbers or Aadhaar references. Scanned notes may carry personal information. Signature blocks in emails can expose PII.

Bank narrations and reference fields can leak relationships and identifiers. Exports and email attachments create uncontrolled data copies. Support tickets with screenshots can reveal PAN numbers.

- Watch outs: working papers with client PII, audit trail exports with unmasked fields, backups on shared drives without encryption, test environments seeded with production data, third party sync pulling more fields than necessary.

Public expectations and media scrutiny are rising. The DPBI is now operational with complaint portals, and individuals can escalate concerns directly (2026 update).

Evaluating AI Accounting Tools: Your Privacy Assessment Checklist

Essential security controls

- Encryption specifics: AES 256 for data at rest, TLS 1.3 for data in transit, pseudonymization for analytics and any training workflows, written confirmation that client data does not train vendor models without consent.

- Field level redaction: demonstrable masking in UI, unmask workflows with justification, immutable audit logs, masking applied to exports and APIs.

- Access control strength: mature RBAC, anomaly detection with alerts, MFA, SSO, multi tenancy isolation for CA firms.

- India cloud residency: explicit region commitments, guarantees against data export, backup and disaster recovery locations inside India.

Compliance evidence to request

- ISO 27001, SOC 2 Type II, DPO contact, privacy impact assessments, model governance policies, breach notification SLAs aligned to 72 hours.

- DPDP readiness roadmap, consent management support, tooling to help you meet obligations, and documented processor contract terms (required by May 2027).

For framing your checklist, consult the Onfra DPDP compliance deadline guide.

Essential Tools for Privacy First AI Accounting

- AI Accountant (https://aiaccountant.com) — Purpose built for Indian CA firms and SMEs, AI Accountant offers India cloud encryption, role based access with multi org isolation, field level masking for PAN and bank accounts, automated bill extraction and GST reconciliation, with strict India data residency. ISO 27001 and SOC 2 Type II certified.

- QuickBooks Online — Robust encryption and access controls, detailed audit trails, India servers for residency in many scenarios.

- Zoho Books — Strong India presence, comprehensive role permissions, API level controls, consistent data boundaries.

- Tally Prime — On premise options for maximum control, India specific features in cloud offerings.

- Xero — Two factor authentication, encryption at rest, retention controls, permission templates.

- FreshBooks — Role based access, audit trails, regular security audits aligned with international standards.

How AI Accountant Implements Privacy by Design

At AI Accountant, privacy by design is foundational. Infrastructure runs on encrypted India cloud, verified with ISO 27001 and SOC 2 Type II. Data stays within Indian borders, without exceptions.

Role based access applies per organization. Multi org isolation prevents cross client visibility. Dashboards are read only by design. Users gain insight without altering underlying data.

Data minimization is built into workflow prompts. The platform requests only what is necessary. Field level masking is pervasive. PAN appears as ****5678, bank numbers show last four digits, and full reveals require explicit permission and are logged.

To follow evolving obligations, see the Fisher Phillips summary of India's new data privacy rules.

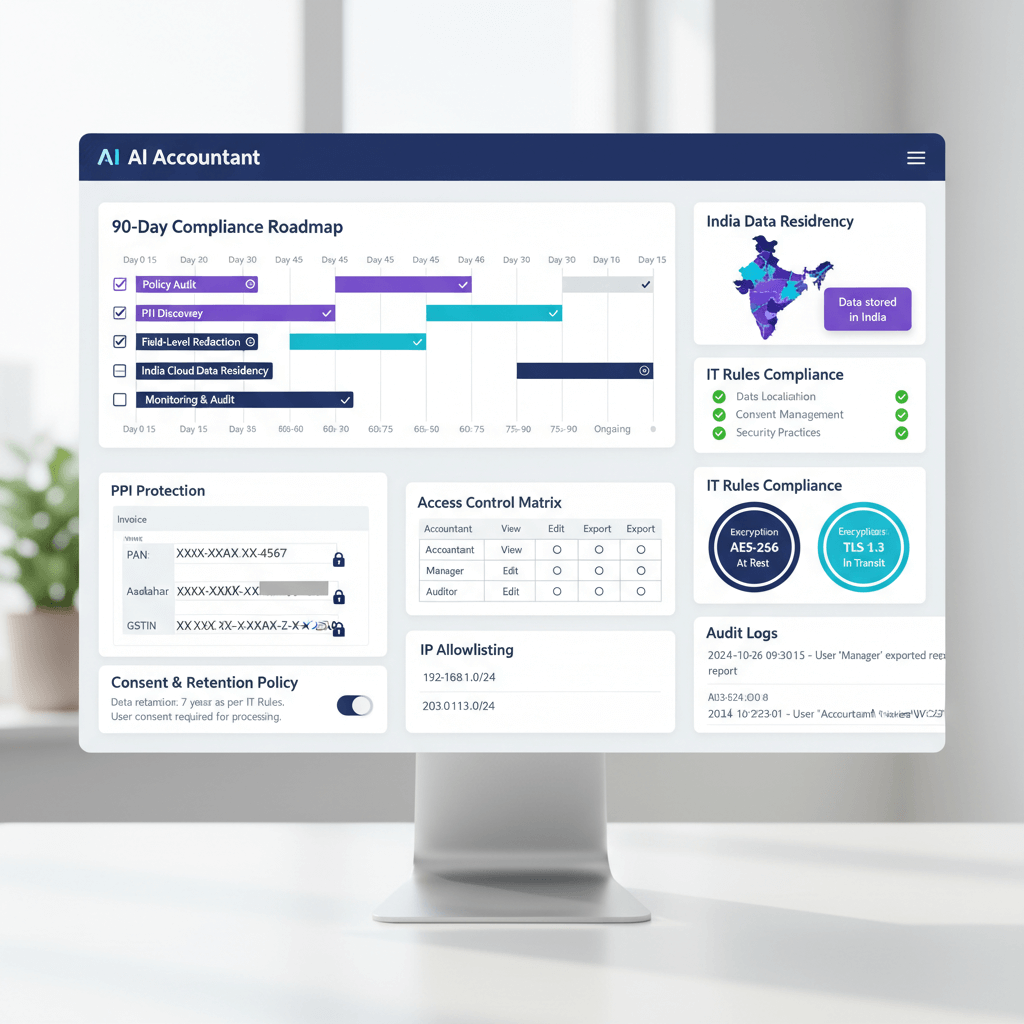

Your 90 Day Privacy Roadmap for CA Firms and Finance Teams

Days 1 to 30: discovery and documentation

Inventory PII across workflows. Build a data map of sources, storage, access, and retention. Document current processes for bill uploads, bank reconciliation, and approvals. Review vendor agreements for privacy commitments and DPDP aligned processor contract terms.

Days 31 to 60: assessment and planning

Evaluate tools against the privacy checklist. Score PII protection, redaction, access controls, and India residency. Create an access control matrix by role. Design a retention policy per data type. Meet GST (seven year retention), income tax, and audit requirements.

Days 61 to 90: implementation and testing

Enable MFA. Implement field level redaction. Configure RBAC from your matrix. Run an incident response tabletop. Verify you can identify affected data quickly and notify within 72 hours. Train teams on privacy basics and common scenarios, including dual reporting to DPBI and CERT-In where applicable.

Templates you can request: data inventory worksheet, retention policy template, access control matrix, vendor assessment questionnaire, breach notification checklist.

Moving Forward with Confidence

Data privacy in AI accounting is about building trustworthy operations while embracing innovation. Apply these principles to one workflow. Document what works, then expand. Perfect privacy does not exist. Progressive improvement does.

In a profession built on trust, every masked field, every audit log, every India resident dataset strengthens your position. The firms that thrive will balance innovation with protection, efficiency with privacy, automation with human oversight.

The frameworks are clear. The tools exist. With the DPBI now active and enforcement infrastructure in place, the time to act is before the next deadline, not after it.

Frequently Asked Questions

What counts as PII for Indian accounting, and how should a CA prioritize protection?

PII includes names, emails, phone numbers, addresses, GSTIN, PAN, bank account numbers, and government identifiers. Prioritize high risk fields first: PAN, bank accounts, and salary details. Then expand controls to narrations and invoice metadata. Under DPDP, even incidental PII in bank narrations or scanned documents counts, so pattern based redaction matters.

How does field level redaction improve operational efficiency compared to full document masking?

Field level redaction selectively masks sensitive values while preserving the remaining context, making invoices, bank statements, and exports usable for AP and finance users. Instead of blocking a document, display PAN****5678 or bank ****1234, allow authorized reveal with justification, and log the action. This keeps reconciliation and approvals moving without exposing unnecessary PII.

Is India data residency mandatory under DPDP, or is it primarily contract driven?

DPDP does not universally mandate India only storage, but many contracts (especially government and PSU) require it. Risk assessments often conclude that India residency simplifies compliance, improves latency, and avoids cross border uncertainty. When cross border processing is necessary, strip PII, document the purpose, and obtain explicit consent.

What are the key DPDP deadlines CA firms must meet in 2026 and 2027?

The 72 hour breach notification to DPBI is active now, with penalties up to ₹2 crore for failure. Consent managers must be operational by November 13, 2026, requiring India incorporation and ₹2 crore net worth. Full compliance (standalone privacy notices, granular consent, individual rights, processor contracts) is enforceable from May 13, 2027 (2026 update).

What baseline encryption standards should I demand from an AI accounting vendor?

Demand AES 256 for data at rest, TLS 1.3 for data in transit, robust key management, and tokenization for high sensitivity fields like PAN or bank numbers. Verify that backups and disaster recovery also remain encrypted, inside India. Ask for certifications (ISO 27001 and SOC 2 Type II) and review their breach notification SLAs aligned to 72 hours.

How should a small CA firm phase privacy controls without heavy spend?

Begin with process and configuration: enable MFA, define roles, turn on built in redaction and encryption features, and document workflows. Use India cloud services that include security by default. Prioritize highest risk workflows first (AP and bank reconciliation), then expand. Many platforms ship privacy features in the base product, reducing the need for expensive add ons.

What evidence should I maintain to prove ongoing DPDP compliance during audits?

Keep a processing register, consent records, standalone privacy notices, access control matrix, VAPT reports, incident response playbooks, and immutable audit logs. Maintain vendor assessments, certifications, processor contracts, and a DPDP readiness plan. With the DPBI now operational and accepting complaints, having this documentation ready is no longer optional (2026 update).

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.