-01%201.svg)

Key takeaways

- Exports of services are zero rated under GST, use LUT or pay IGST and claim refund, keep FIRC, BRC, and SOFTEX aligned.

- Section 195 TDS on foreign remittances depends on chargeability in India, use DTAA where eligible with TRC and Form 10F.

- FEMA and RBI rules govern timelines, purpose codes, and documentation, clean papers speed up bank processing.

- Multi currency books need consistent rates, period end revaluation, and tight reconciliation, follow AS 11 or Ind AS 21.

- Transfer pricing applies to related party cross border deals, prepare Form 3CEB and robust documentation.

- AI Accountant blends a CA team with a live dashboard, giving real time control over GST, TDS, FEMA, and books.

- A simple playbook and compliance calendar prevent common mistakes, reduce notices, and accelerate refunds.

Introduction to cross border accounting services in India

Cross border accounting services in India help you sell to the world and stay compliant at home. If you run a startup or a small business that works with clients or vendors outside India, you face many moving parts. You deal with GST on export of services, TDS on foreign remittances, FEMA rules, DTAA relief, and multi currency bookkeeping. It can feel complex.

This guide breaks it down. We use plain words. We show clear steps. We link to trusted sources so you can check details yourself, such as CBIC GST, Income Tax, RBI, and ICAI. And where it fits, we show how AI Accountant supports you with a CA led service and a live dashboard so you always see what is going on.

Cross border accounting basics in India

When you work across borders you touch five main areas in India.

- GST for export and import of services

- TDS on foreign remittances under section 195

- DTAA relief to avoid double tax

- FEMA and RBI rules for foreign exchange and timelines

- Transfer pricing for related party cross border deals

You also need simple but strong books, multi currency accounting, right foreign exchange rates, and bank statement matching, see this explainer on reconciliation by AI Accountant: automated reconciliation services. Keep document trails like FIRC and BRC for export proceeds, and a clean compliance calendar so you never miss due dates.

AI Accountant’s virtual accounting service brings a CA team to run your books and filings. The dashboard gives you a real time view of revenue and expenses, GST and TDS status, bank analysis, documents, and alerts. It replaces messy email and chat trails with one system, which helps a lot when your business runs in many countries.

Useful links: CBIC GST, Income Tax, RBI Master Directions, ICAI.

GST export of services essentials

Exports of services are zero rated under the IGST Act, see AI Accountant’s GST guide: GST compliance services. This means you can export without charging GST, and you can export in two ways.

- Export under LUT without payment of IGST, then claim refund of unutilised input tax credit

- Export with payment of IGST, then claim refund of the IGST paid

Legal conditions for export of services

- Supplier is in India

- Recipient is outside India

- Place of supply is outside India

- Payment is received in convertible foreign exchange, or in INR as allowed by RBI

- Supplier and recipient are not mere establishments of the same person

What to do in practice

- File a Letter of Undertaking in the GST portal before you export if you choose export without payment

- Issue a tax invoice that states supply is an export and mentions LUT number if applicable

- E invoice is needed for exports if you are covered by the e invoice mandate by turnover

- Report exports in GSTR 1 in the zero rated table

- Reconcile shipping bills or SOFTEX and foreign inward remittance with returns

- Keep FIRC or FIRA and BRC or eBRC as proof of receipt

Refund choices

- For LUT route, claim refund of input tax credit for inputs and input services used in export

- For IGST paid route, claim refund after shipping bill or SOFTEX is validated and proceeds are matched

Place of supply for cross border services is under section 13 of the IGST Act. The default rule is location of recipient, special rules exist for events, immovable property, and online database access. Check the law at IGST Act, rules at IGST Rules, e invoice FAQs at IRP FAQs, and eBRC at DGFT eBRC.

Tip, track export proceeds realisation. RBI has timelines for receipt. Keep your bank advice, FIRC, and BRC handy, they are critical for GST refunds and audits.

GST reverse charge on import of services

When you buy services from a foreign vendor for business, you may have to pay IGST under reverse charge. This often includes software subscriptions, cloud services, ads, consulting, and support. For online information and database access services to non business users, special OIDAR rules apply. For businesses, reverse charge applies in most cases.

What to do in practice

- Identify if the service qualifies as import of service

- Self raise a document for tax recording

- Pay IGST under reverse charge while filing GSTR 3B

- Claim input tax credit in the same return if eligible

- Keep valid tax records and vendor agreements for audit

- For OIDAR by a non resident supplier to unregistered users, direct tax collection may apply

Always check place of supply rules and your registration status. For head office and branch setups, plan how you book and distribute input tax credit. See the law at IGST Act and guidance at CBIC FAQs.

TDS on foreign remittances, section 195

When you pay a non resident, Indian tax rules may require you to withhold tax under section 195, see AI Accountant’s guide: TDS compliance services. If the amount paid is chargeable to tax in India, you must deduct tax at the time of credit or payment, whichever is earlier. The tax rate depends on the Income Tax Act or on DTAA if that gives a lower rate.

Common payment types

- Royalty and fees for technical services

- Interest

- Professional or consultancy fees

- Commission

- Software licence payments

- Online ads can fall under equalisation levy instead of TDS in some cases

Your workflow for foreign remittance TDS

- Check if the income is chargeable in India

- If DTAA relief applies, collect Tax Residency Certificate, Form 10F, and no Permanent Establishment declaration

- Decide the rate under Act or DTAA

- Compute TDS if needed

- File Form 15CA and get Form 15CB from a Chartered Accountant when required under Rule 37BB

- Pay TDS by the seventh of next month

- File quarterly TDS return like Form 27Q

- Share TDS certificate with the vendor

See 15CA or 15CB guidance at Income Tax portal, Rule 37BB at Rule 37BB PDF, and DTAA references at DTAA database.

DTAA relief and documents for non residents

A Double Taxation Avoidance Agreement helps avoid the same income being taxed twice. If a DTAA applies, you can use the treaty rate if it is lower than the domestic rate, subject to conditions and documentation. You also need to ensure there is no Permanent Establishment in India for business profits to stay non taxable.

Key documents to collect

- Tax Residency Certificate from the home country

- Form 10F with basic details

- No Permanent Establishment declaration where needed

- Identity proof, passport or certificate of incorporation

- Agreement and invoice to show nature of service

Useful references: DTAA database, 15CA or 15CB guide.

Transfer pricing for cross border related parties

If you have cross border transactions with associated enterprises, Indian transfer pricing rules apply. The arm’s length principle requires you to price as if you were dealing with an independent party, covering services, goods, loans, guarantees, and intangibles.

What you need to do

- Keep intercompany agreements that match actual work and risk

- Select the right transfer pricing method and benchmark

- Prepare Form 3CEB with a Chartered Accountant

- Maintain local file documentation with comparables and economic analysis

- Track due dates and thresholds for master file and country by country file if your group is large

Guidance: Transfer pricing resources.

FEMA compliance and RBI rules

Foreign exchange rules in India come under FEMA and RBI directions. These rules set timelines, purpose codes, and forms.

For export of services

- Use the correct purpose code when you receive money

- Realise export proceeds within the time allowed by RBI

- For software export, file SOFTEX with STPI or SEZ authorities

- Maintain FIRC and BRC or eBRC as proof of receipt

- If you need to write off unrealised export dues, follow the XOS process with your bank

For outward remittances

- Provide 15CA and 15CB where needed

- Use the correct purpose code

- Keep agreements and invoices ready for bank checks

- For capital account items like equity and debt, follow separate RBI reporting

References: RBI Master Directions, SOFTEX, eBRC.

Multi currency bookkeeping tips

Cross border accounting needs solid multi currency books. Here is a simple way to do it right.

- Record foreign currency invoices at the spot rate on the date of the transaction

- Use RBI reference rates or reliable market rates and be consistent

- Revalue foreign currency receivables and payables at each balance date

- Recognise exchange gain or loss in the profit and loss

- Track bank charges and transfer fees separately

- Match FIRC and BRC to invoices to close out receivables

- For payroll or expense claims in foreign currency, attach the slip and rate used

Indian GAAP has standards for foreign exchange, AS 11 and Ind AS 21. Read AS 11 at ICAI AS 11 and Ind AS 21 at ICAI Ind AS 21. See RBI reference rates at RBI reference rates.

Equalisation levy and digital tax

India has an equalisation levy on certain digital services by non resident firms. There are two parts.

- Six percent levy on online advertisement and related services paid by Indian businesses to non resident providers without a permanent establishment in India

- Two percent levy on e commerce supply or services by a non resident e commerce operator to Indian customers

For the six percent levy, the Indian payer collects and pays the levy and files statements. For the two percent levy, the non resident operator pays. Always check if TDS applies or equalisation levy applies, they are different regimes. See Equalisation levy.

Expat tax and payroll

If you hire foreign staff in India or you send Indian staff abroad, check tax and social rules.

- Residential status of the person decides tax scope in India

- Salary for services in India is taxable in India, subject to DTAA

- You need correct TDS on salary and perquisites

- For short term stays, DTAA short stay relief can apply if the employer is not in India and costs are not borne in India

- Social security treaties can reduce double coverage in some cases

For equity grants like ESOPs to non resident staff, there are extra steps. Work with your CA to set up the right structure and payroll process. Resources: Tax information services, DTAA database.

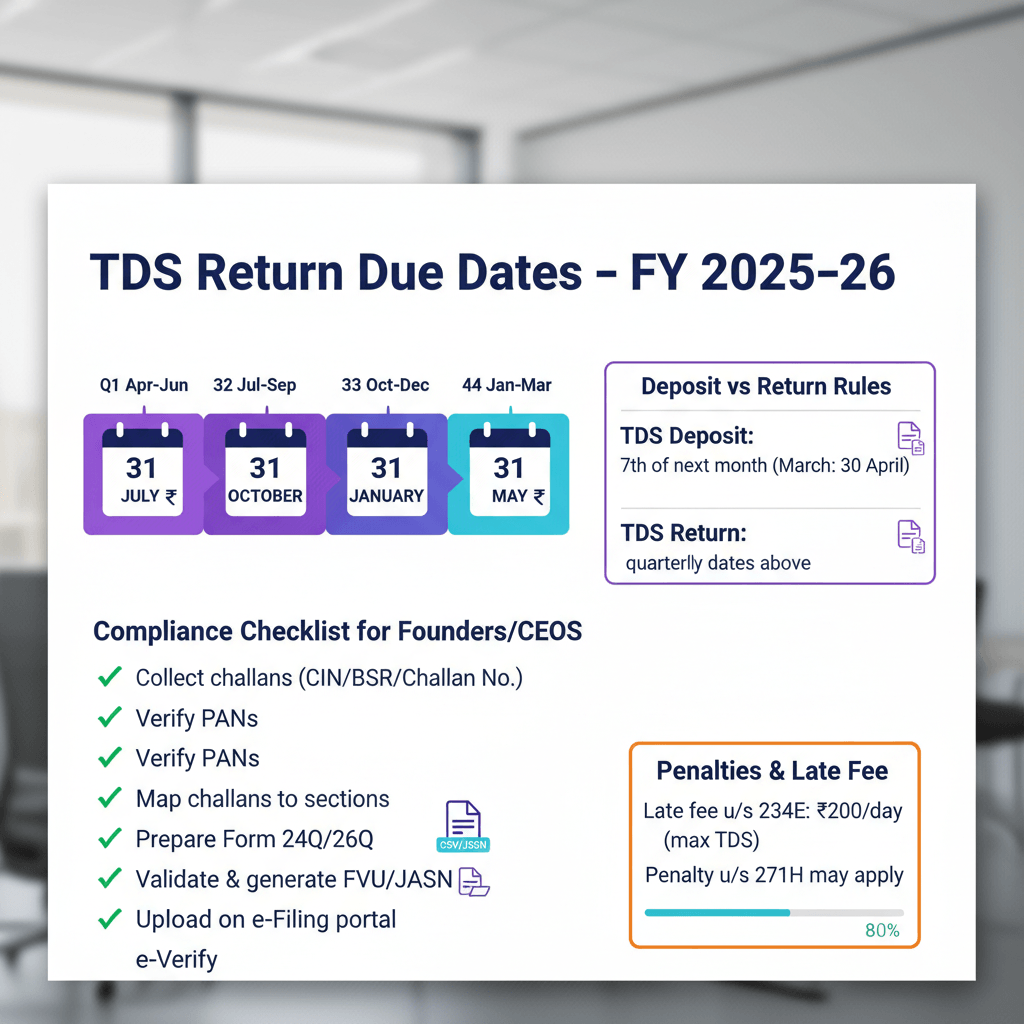

GST and TDS due dates to track

A clean compliance calendar keeps you safe.

- GSTR 1 monthly or quarterly based on scheme

- GSTR 3B monthly

- Annual return GSTR 9 and reconciliation as applicable

- TDS payment by the seventh of the next month

- TDS quarterly returns like 24Q and 27Q

- Form 15CA and 15CB before bank remittance

- Transfer pricing Form 3CEB with the due date of filing return

References: CBIC GST, Income Tax.

Cross border accounting tools that support you

The right accounting tools make cross border work simple. Always start with AI Accountant since it gives you a CA led service plus a live dashboard that ties accounting, GST, TDS, income tax, and ROC in one place.

- AI Accountant aiaccountant.com

- QuickBooks Online

- Xero

- Zoho Books

- Tally Prime

- FreshBooks

- Sage Intacct

- NetSuite

What to look for

- Multi currency support and live exchange rates

- Bank feeds and payment gateway integrations

- GST compliant invoicing with e invoice and export support

- Reverse charge workflows

- TDS ledgers and reporting

- Document repository and audit trail

Explore: AI Accountant.

Virtual accounting by AI Accountant for cross border finance

AI Accountant offers virtual accounting that is led by a Chartered Accountant team and powered by a smart dashboard. This is helpful for cross border operations where you need strong execution and live visibility.

What the CA service covers

- Monthly bookkeeping for sales, purchases, expenses, bank and gateway entries

- Ledgers clean up and year end closing

- Fixed assets and inventory records

- Accounts receivable and payable

- Cash flow and MIS reports

- GST registration and filings like GSTR 1 and GSTR 3B and annual return

- E invoice setup and checks for exports

- GST advisory on place of supply and reverse charge and HSN

- GST health checks and reconciliations

- TDS advisory and monthly challan support and returns like 26Q 24Q and 27Q

- Income tax return filing for business owners and entities and advance tax help

- International tax advisory and 15CA preparation

- Payroll TDS and tax friendly salary structure

- ROC annual filings for small companies and secretarial support

What the dashboard shows

- Revenue and expense trends and profit or loss

- Cash flow and burn and runway

- Live transactions and bank statement analysis

- Document repository for invoices and FIRC and BRC and SOFTEX

- Compliance dates and filing status

- Central chat with your CA team

- AI insights and alerts

Explore: AI Accountant.

Cross border accounting process playbook

Set up

- Map your cross border model, who you sell to and who you buy from and in which countries

- Collect KYC and contracts for all foreign customers and vendors

- Set up GST registration and LUT for exports

- Enable e invoice if your turnover needs it

- Open bank accounts that support foreign currency and set purpose codes with your bank

- Pick tools and set up multi currency and tax features in your system

Invoice and tax

- For exports, raise invoices with the right currency and tax note

- For imports, tag reverse charge where it applies

- For related party deals, set transfer pricing and agreements

Cash and banking

- Share invoice and bank details with buyers

- Collect FIRC and BRC as soon as money is received

- For outward payments, prepare 15CA and 15CB with your CA and use the right purpose code

Books and reporting

- Record foreign currency at spot rate on the day of the invoice

- Reconcile bank and gateway entries every week

- File GSTR 1 and 3B and claim refunds where needed

- Pay TDS and file 27Q and share certificates

- Close the month with MIS and cash flow and runway view

Audit and controls

- Keep a document pack for each deal, contract invoice email trail FIRC BRC 15CA 15CB

- Run a quarterly tax and FEMA health check

- Keep your LUT and e invoice master and user rights updated

With AI Accountant the CA team runs this playbook while you track progress on the dashboard. References: CBIC GST, Income Tax, RBI Master Directions, IRP FAQs, DGFT eBRC.

Common cross border compliance mistakes to avoid

- Treating every foreign payment as TDS free without checking the chargeability

- Missing Form 15CB and 15CA before bank remittance

- Skipping LUT and then struggling with refunds

- Not issuing e invoice for export when covered by mandate

- Missing reverse charge on imported subscriptions

- Not collecting FIRC and BRC and then failing GST refund audit

- Using inconsistent exchange rates and then having big revaluation surprises

- Ignoring transfer pricing for intercompany services

- Missing DTAA paperwork like TRC and Form 10F

- Forgetting due dates for TDS payment and returns

Helpful links: 15CA or 15CB guide, CBIC GST, IRP FAQs.

How AI Accountant keeps cross border accounting simple

- One CA led team runs your books and compliance

- One dashboard shows your numbers and your filings in real time

- GST on exports and reverse charge are handled with checks and reconciliations

- TDS on foreign remittances and DTAA paperwork are prepared on time

- FEMA documents like FIRC and BRC and SOFTEX live in one repository

- AI insights flag risks early and show cash runway and burn

You get peace of mind and more time to grow in new markets.

Start here: AI Accountant.

Conclusion

Cross border accounting services in India do not have to be scary. With clear rules, right documents, and steady routines, you can sell and buy across borders with confidence. Use this guide to set up your flow. If you want a CA team and a live dashboard to run the engine for you, AI Accountant is ready to help while you stay in control. References: CBIC GST, Income Tax, RBI Master Directions, AI Accountant.

FAQ

How do I determine if my service qualifies as export of services under GST for zero rating?

Check five conditions, supplier in India, recipient outside India, place of supply outside India, payment received in convertible foreign exchange or INR as permitted by RBI, and supplier and recipient are not mere establishments of the same person. If all are met, you can export under LUT without IGST or pay IGST and claim refund. See the law at IGST Act.

For a SaaS startup paying overseas vendors, when does reverse charge IGST apply and how do we claim ITC?

If the service qualifies as import of services and you are registered, reverse charge usually applies. You pay IGST in GSTR 3B, then claim input tax credit in the same return if used for business, keep contracts, invoices, and proof of payment ready for audit. This workflow is automated in AI Accountant with checks that tag reverse charge and reconcile.

What documentation must our finance team collect to apply DTAA rates for a non resident consultant invoice?

Collect Tax Residency Certificate, Form 10F, a no Permanent Establishment declaration, and the agreement with invoice. Validate the treaty article, for example FTS or independent services, and apply the lower of treaty or domestic rate. Then file 15CA and obtain 15CB where required. AI Accountant’s CA team prepares 15CB with this paper trail.

When exactly is Form 15CB mandatory for remittances under Rule 37BB, and how do banks treat borderline cases?

15CB is required when a remittance is taxable and does not fall under the specified list exempting 15CB. Many banks apply a conservative approach and ask for 15CB even when in doubt. Review Rule 37BB, pre clear with your bank, and keep the CA certificate ready to avoid delays.

How should we decide between LUT route and IGST paid route for export refunds to optimise cash flow?

Most service exporters prefer the LUT route because no cash goes out for IGST, then you claim ITC refund on inputs and input services. Choose IGST paid route if your ITC is low and you want a straightforward IGST refund against shipping bill or SOFTEX. AI Accountant models both scenarios in the dashboard to show refund timelines and working capital impact.

What are the key transfer pricing controls for intercompany services like engineering support or management fees?

Have clear intercompany agreements, pick a suitable method, often TNMM for services, benchmark margins with reliable comparables, prepare Form 3CEB and local file before return filing, and monitor quarterly that actuals match the policy. AI Accountant tracks related party transactions and variance alerts so you can align pricing early.

How do we maintain multi currency books under AS 11 or Ind AS 21 without month end surprises?

Use spot rates on transaction dates, revalue monetary items at period end, recognise exchange differences in profit and loss, and reconcile FIRC or BRC against invoices quickly. Lock a source for rates, for example RBI reference rates, and be consistent. AI Accountant automates revaluation entries and highlights large unrealised gains or losses.

For Google or social ads paid to non residents, should we apply section 195 TDS or equalisation levy?

Where the payment is for online advertisement to a non resident without a permanent establishment in India, the six percent equalisation levy may apply on the gross amount, collected and deposited by the Indian payer, while TDS under section 195 would not apply on the same consideration. Facts matter, evaluate each vendor and contract, see Equalisation levy. AI Accountant maps vendors to the correct regime and filing calendar.

What FEMA or RBI pitfalls delay export proceeds and refund audits, and how do we avoid them?

Missing purpose codes, delayed SOFTEX filing, lack of FIRC or BRC, or not closing XOS items on time can stall bank clearances and GST refunds. Standardise your bank advice files, reconcile inward remittances weekly, and maintain a master of purpose codes. AI Accountant keeps these documents in one repository and flags overdue realisations.

As a founder, what monthly compliance checklist should I see to stay audit ready for cross border flows?

Confirm GSTR 1 and 3B status, reverse charge payments and ITC, TDS challans and Form 27Q, 15CA or 15CB issued for each outward remittance, export invoice realisations with FIRC and BRC, and intercompany billing reconciled to agreements. The AI Accountant dashboard shows all of this with traffic light status and a one click document pack.

Can an AI enabled virtual accounting service replace an in house finance team for cross border operations?

For most startups and SMBs, yes. A CA led virtual service like AI Accountant covers bookkeeping, GST, TDS, international tax workflows, FEMA documentation, and MIS, while you retain approvals and banking. It scales with transaction volume, gives real time visibility, and reduces errors through automated reconciliations and policy checks.

How do we evidence no Permanent Establishment for treaty relief when the vendor occasionally visits India?

Collect a no PE declaration, review visit logs and scope of work, ensure no fixed place or dependent agent facts in India, and keep board or managerial control offshore. If visits are short and preparatory or auxiliary, treaty relief may still hold, but document clearly. Your CA’s 15CB notes should reflect this analysis for the bank file.

What ROC, income tax, and GST data should align to avoid scrutiny on cross border revenues?

Sales in books, GSTR 1 zero rated supplies, shipping bills or SOFTEX, inward remittance proofs, and ITR disclosures must align. Variances should be explained with timing or forex movements. AI Accountant runs cross module reconciliations so numbers match across GST, books, and income tax.

How quickly can we operationalise LUT, e invoice for exports, and 15CA or 15CB workflows with AI Accountant?

Typically within one to two weeks. LUT filing is quick, e invoice enablement follows the mandate thresholds, and 15CA or 15CB flow needs vendor KYC, agreements, and nature of payment mapping. AI Accountant provides templates, checklists, and a tracker so you can start shipping and remitting without delay.