Key takeaways

The Three-Part Structure Every Startup Must Follow

Your cash flow statement is not a list of transactions, it is a compliance document that shows whether you will survive next month. While your profit statement tells a story about success, your cash flow statement tells the truth about survival.

You are profitable on paper but cannot pay salaries. Vendors are threatening legal action while your P&L shows growth. This is a cash crisis, not an accounting glitch.

What is a cash flow statement and why do startups need it?

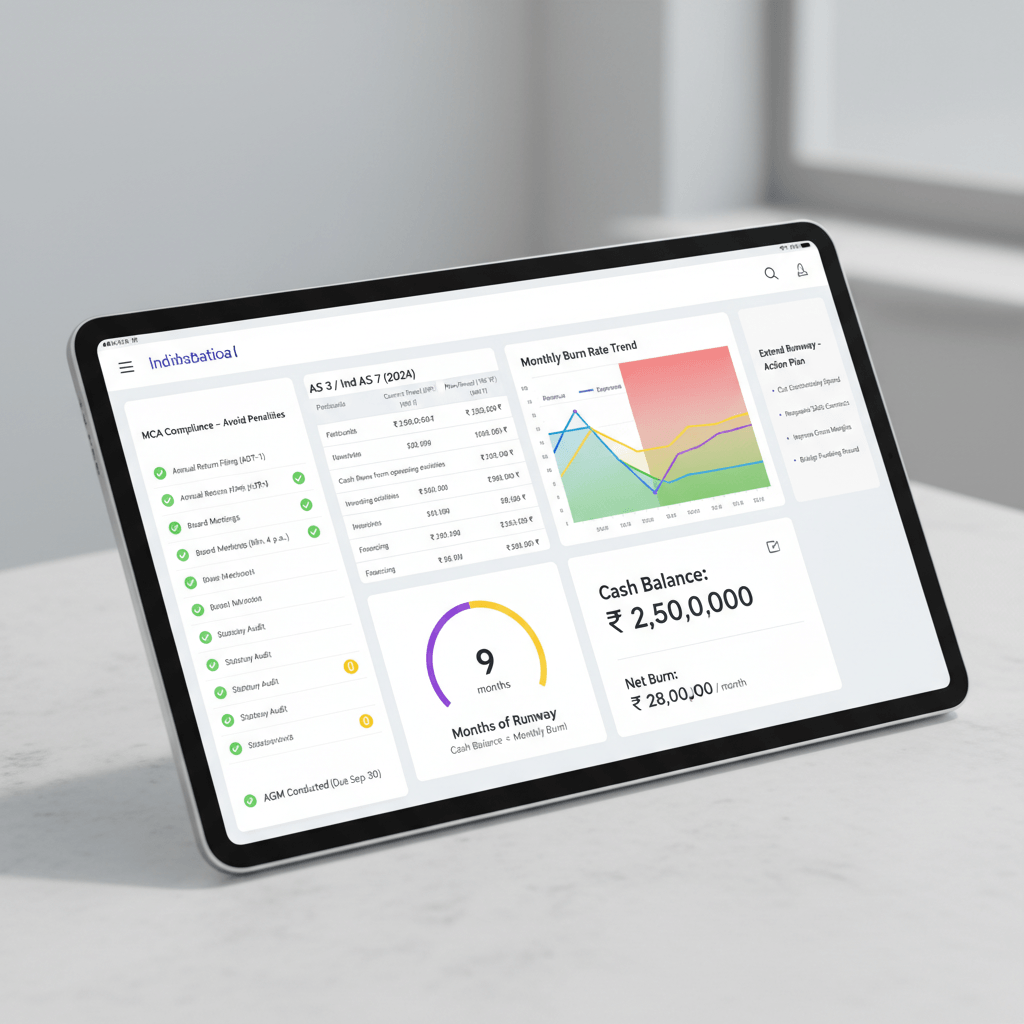

A cash flow statement tracks all money flowing in and out of your business, classified into operating, investing, and financing activities as per AS 3 or Ind AS 7. Unlike profit, which captures accruals and non-cash items, cash flow reveals actual liquidity, which is critical when growth, collections, and expenses move at different speeds. Companies Act 2013 mandates it for all companies, with penalties up to ₹3 lakhs on the company plus ₹50,000 per director for non-compliance. Virtual Accounting by AI Accountant automates cash flow tracking with real-time dashboards, giving founders instant visibility into runway and burn rate while ensuring compliance.

How the three sections work in practice

What format should Indian startups use?

Under Schedule III of Companies Act 2013, most companies present the indirect method, starting with profit before tax, then adjusting for non-cash items like depreciation, changes in working capital, and actual cash movements. The direct method is allowed but rarely used because it requires extensive system changes. In the indirect method, you begin with net profit or loss, add back depreciation and amortization, adjust receivables, payables, inventory, and arrive at operating cash flow. Most software can generate this, but the adjustments need oversight, especially where revenue recognition or ESOPs complicate things.

Which accounting standard applies to your startup?

Companies below prescribed thresholds typically follow AS 3, larger or listed companies follow Ind AS 7. Ind AS 7 demands more disclosures, including restricted cash and non-cash financing changes. Many startups start under AS 3, then transition when they scale or attract global investors. Voluntary Ind AS adoption can build credibility, but it requires restating historical financials. But following format alone is not enough if you are still tracking cash manually.

Legal Requirements That Can Destroy Your Startup

Companies Act Section 134 violations resulted in ₹4.5 lakh penalties on a single company, ₹3 lakhs on the company plus ₹50,000 per director. The issue, financial statements that failed the “true and fair view” requirement, including poor cash flow classification.

Section 129 requires compliance with accounting standards, and any deviation must be disclosed with reasons and quantified impact. MCA scrutiny through ROC reviews now catches classification errors that used to slip through.

“True and fair” means every transaction is correctly classified. AWS bill, operating. Laptop purchase, investing. Founder loan, financing. Consistent misclassification is misrepresentation, which invites penalties.

What triggers MCA penalty proceedings?

Auditors face penalties for not reporting violations, so even small errors get flagged. Triggers include inconsistent treatment across periods, unexplained cash changes despite profits, and missing reconciliation between profit and operating cash flow. Scrutiny spikes during funding, IPO prep, or unusual filing patterns.

Personal liability for directors and CFOs

Directors must sign a statement of compliance. False statements or non-signing can trigger personal penalties. Independent, nominee, and non-executive directors can also be liable unless they documented dissent. Most founders only learn this after a penalty notice.

This is where Virtual Accounting by AI Accountant helps. The system auto-classifies per AS 3 or Ind AS 7, produces monthly compliant cash flow statements, and maintains audit trails that protect directors. Want to see it in action? Watch this short video. If you are comparing providers, start with our buyer’s checklist to evaluate virtual accounting services for Indian startups.

Hidden Cash Flow Killers Most Founders Miss

Your cash flow statement exposes what P&L hides, recognized revenue not yet collected, accrued expenses not yet paid, and working capital trapped in operations. Growth amplifies these gaps.

The most dangerous pattern is working capital expansion. You extend net-60 to customers and pay suppliers on net-30, every sale reduces cash for 30 days. This is how fast-growing companies run out of money at their peak.

Subscription businesses face timing mismatches. You earn revenue monthly but incur acquisition costs upfront, so the P&L looks smooth while cash flow stays negative for months.

GST collected is not your money, it is a liability. Treating it as free cash inflates your bank balance deceptively, then payment dates trigger panic. A proper cash flow statement separates tax obligations from operational cash.

How to spot a brewing cash crisis

The working capital trap that kills growing startups

Working capital changes show up as single lines but reflect deep operational issues, rising receivables, bloated inventory, or shrinking payables. The deadly combo is rapid growth with weak working capital controls. You may need ₹150 lakhs at ₹3 crores monthly revenue, compared to ₹50 lakhs at ₹1 crore, that is ₹100 lakhs trapped just to stand still.

Due Diligence Disasters and Funding Failures

Investors analyze cash flow statements to see through P&L polish. They look for inconsistent classification, operating costs moved to capital items, or deposits treated as revenue. These patterns signal manipulation or inexperience.

Quality of earnings compares profit to operating cash flow across periods. Persistent gaps suggest aggressive accounting or operational breakdowns. Window dressing, collecting hard at quarter-end while delaying payables, is obvious in monthly cash trends.

What investors actually check in your cash flow

Virtual Accounting by AI Accountant ensures consistent classification from day one, generates investor-ready statements, and keeps a defensible audit trail. You spot issues months before an investor does.

Common adjustments that raise red flags

Building Your Cash Flow Forecasting System

Historical cash flow tells you what happened, forecasts tell you what will happen. The shift from reporting to proactive management starts with a realistic 13-week rolling forecast, updated weekly.

Base it on actual operating cash patterns, layer confirmed revenue and expense changes, and model scenarios, late enterprise payments, customer churn, or GST refund delays. Weekly variance analysis keeps it honest.

Creating reliable 13-week rolling forecasts

Roll forward one week every Monday, maintaining a constant 13-week horizon. Look for trend shifts, is runway extending or shrinking, are collections improving or deteriorating?

Connecting operations to cash impact

Make cash the lens for decisions. Hiring a developer at ₹1.5 lakhs monthly hits cash now, not gradually. Net-60 terms boost bookings but drain cash. Link operational metrics to cash, CAC timing, payment terms, salaries, inventory, and refunds. For templates and tooling, read Cash Flow Forecasting for Indian SMEs — Methods and Tools.

Conclusion

Cash flow statements are survival guides, not just compliance forms. The AS 3 or Ind AS 7 structure forces discipline in understanding where cash originates, where it goes, and how long you can survive. The Companies Act creates personal liability if you get this wrong, yet the bigger risk is operating blind. Master cash flow, and you master the difference between growing and surviving.

Frequently Asked Questions

What is the difference between cash flow and profit for startups?

Profit includes non-cash items and timing differences, it reflects economic performance. Cash flow tracks actual money movement. You can show ₹50 lakhs profit yet have negative ₹20 lakhs cash flow if customers have not paid or if you made large capital purchases. As you grow, the gap often widens because you pay expenses now while you collect later.

How often should startups prepare cash flow statements?

Annually is the legal minimum, monthly is the practical minimum, and weekly tracking is recommended during growth or stress. Virtual Accounting by AI Accountant provides daily cash positions and weekly operating cash reports so you can course-correct in time.

What happens if we do not file cash flow statements?

Penalties can reach ₹3 lakhs for the company plus ₹50,000 per director, with potential prosecution for willful misstatement. Beyond fines, expect ROC scrutiny, shaken investor confidence, and difficulty securing credit.

Can Excel templates work for startup cash flow tracking?

Excel can work below ₹50 lakhs annual revenue with simple operations. Beyond that, manual classification errors and version issues become risky. Tools like Virtual Accounting by AI Accountant automate AS 3 or Ind AS 7 classification, generate investor-ready statements, and save 20+ hours monthly. Exploring options, see the 6 best online bookkeeping services for Indian SMBs.

What is the indirect method vs direct method for cash flow?

The indirect method starts from net profit, adds back non-cash items, and adjusts working capital to reach operating cash flow. The direct method lists gross cash receipts and payments. Schedule III expects indirect for most companies, direct is clearer but operationally heavy to implement.

How do you classify customer advances in cash flow?

Customer advances are operating cash inflows when received. When you deliver the product or service, revenue is recognized without new cash. Many startups incorrectly treat advances as financing, which distorts operating performance and triggers audit queries.

What are the most common cash flow mistakes startups make?

Counting all inflows as revenue, misclassifying assets as expenses, ignoring GST or TDS as liabilities, mixing operating and investing flows, and assuming a healthy bank balance equals healthy cash after obligations. These errors hide structural issues until a crisis hits.

Should founder salaries appear in the cash flow statement?

Yes, paid salaries appear under operating activities. Unpaid or foregone salaries do not appear since no cash moved. Inconsistent founder compensation patterns worry investors and skew your burn profile.

How do you handle GST in the cash flow statement?

GST collected and paid flows through operating activities alongside the underlying transactions, and remittances to government are also operating. Treat GST collected as a liability until paid. Virtual Accounting by AI Accountant segregates tax flows to avoid accidental spending.

Which cash flow metrics do investors analyze most?

Operating cash flow margin, cash conversion cycle, monthly burn, runway, and cash flow to debt. Trends matter more than snapshots, improving operating cash signals a scalable model, deteriorating trends signal mounting risk.

When should a founder start worrying about cash flow?

When operating cash flow is negative for three consecutive months, when receivables exceed 60 days, when supplier payments are delayed, when runway falls below six months, or when profit and cash diverge materially. These are structural, not seasonal, warnings.

How do subscription businesses handle deferred revenue in cash flow?

Annual subscriptions paid upfront are operating cash inflows when received; the liability increases, not revenue. Monthly revenue recognition happens without new cash, which means you need reserves to serve already-paid customers throughout the term.

What is the impact of credit periods on cash flow?

Every day of customer credit delays cash by daily revenue. Net-30 on ₹30 lakhs monthly means roughly ₹30 lakhs tied up. Net-60 doubles it, growth escalates the trap unless you match supplier terms or strengthen collections.

Should equipment purchases show in operating or investing activities?

Investing. Laptops, furniture, servers, and long-term software are investing outflows because they deliver value over multiple periods. Misclassifying them as operating inflates burn and understates capital intensity.

How do you forecast cash flow for seasonal businesses?

Model baseline monthly patterns, overlay seasonality, and stress-test timing. Build higher buffers before lean months, avoid commitments based on peak season cash. Tools in Virtual Accounting by AI Accountant can model seasonality, linking inventory, hiring, and marketing to cash timing.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.