Key takeaways

- A 13 week rolling forecast gives you enough visibility to manage GST cycles, advance tax, and vendor payments without drowning in unnecessary detail

- Track collections from customers religiously, delayed payments are the number one cash flow killer for Indian SMEs, especially with MSME payment rules

- Sync your forecast with compliance calendars for GST, TDS, advance tax, and statutory deposits to avoid expensive late fees and interest

- Virtual Accounting by AI Accountant provides automated cash flow tracking integrated with your compliance calendar, updating daily from your actual transactions

What is cash flow forecasting and why do Indian SMEs need it?

Cash flow forecasting means predicting when money will enter and leave your business over the next 13 weeks or more, helping you spot cash crunches before they happen. Indian SMEs face unique challenges with GST payment cycles, TDS deadlines, and delayed customer payments that make forecasting critical. Without it, you risk defaulting on statutory payments, missing payroll, or taking expensive emergency loans.

Running out of cash kills more Indian businesses than running out of profit ever will. If you have scrambled to pay GST on the 20th while a client payment is stuck, you already know the pain. Forecasting converts monthly panic into predictable planning, it shows exactly when money comes in, when it must go out, and what gaps you must bridge.

Why is cash flow forecasting critical for Indian businesses?

Cash flow forecasting is not about profit, it is about survival. Your P&L might show healthy margins, yet if your largest customer pays 60 days late while GST is due in 20 days, you have a problem. Indian businesses live this reality frequently.

The compliance calendar alone creates predictable cash drains. GST payments hit monthly or quarterly. TDS deposits cannot wait. Advance tax arrives every three months. EPF and ESI are due by the 15th. Miss any of these and you face late fees, interest at 18 percent per annum, and potential penalties.

Collections are the next challenge. Despite MSMED Act provisions requiring payment within 45 days, many SMEs wait 60 to 90 days for receivables. Meanwhile, your landlord, employees, and vendors will not wait. Neither will the tax department. A forecast lets you see problems weeks ahead, negotiate terms, arrange working capital, or defer non critical expenses, planning replaces panic.

How do payment delays from customers impact cash flow?

Customer payment delays destroy predictability. You invoice promptly, yet customers pay when convenient, converting your receivables into an involuntary loan you never agreed to extend.

Large corporates may impose 60 to 90 day terms despite MSMED Act requirements, government departments can take even longer, startups conserve their cash by delaying yours. You become an unofficial banker to your customers.

The cycle is vicious. You take an overdraft at 12 to 14 percent to bridge the gap, margins shrink, you delay your own vendor payments, relationships suffer, statutory delays trigger penalties. The MSMED Act provides remedies, registered MSMEs can claim interest at three times the RBI rate beyond 45 days, and Section 43B(h) of the Income Tax Act disallows expense deductions for delayed MSME payments. Enforcement requires reminders and sometimes legal action, all while maintaining client relationships. Forecasting plans for realistic timelines, not contractual ones.

What are the hidden costs of poor cash flow management?

Poor cash flow management costs more than overdraft interest. Compounding penalties, lost opportunities, and decision making stress do the real damage.

- Compliance costs, miss your GST payment and you pay interest at 18 percent per annum plus late fees. Delay TDS deposits and add 1.5 percent monthly interest plus fees under Section 234E. Skip advance tax installments and Section 234B or 234C interest applies. These costs compound monthly.

- Operational impacts, vendor relationships erode, early payment discounts vanish, you refuse new orders for lack of working capital, employee attrition rises if salaries slip, credit score falls, future financing becomes expensive.

Virtual Accounting by AI Accountant integrates your cash flow forecast with compliance deadlines, it shows when statutory payments are due and whether you will have funds available, and it flags potential shortfalls weeks in advance.

Want to see how it works? Watch this short video.

Automate your cash flow tracking today. Get daily cash position updates integrated with your compliance calendar. Start Free Trial →

The stress cost is hardest to quantify. Constant fire fighting blocks growth, you take expensive loans, accept poor payment terms, or discount just to generate cash. Good cash flow management reduces anxiety, you run the business instead of chasing money.

How does GST compliance affect monthly cash flows?

GST creates predictable yet challenging pressure. You collect GST from customers but must pay the government on fixed dates, whether you received payment or not.

Monthly filers face GSTR 3B due on the 20th and GSTR 1 on the 11th, QRMP filers have different cycles with similar pressures. Timing mismatch is brutal, you might invoice with GST on the 1st but receive payment on day 60, while GST is due on the 20th. You end up funding the government from working capital.

On a ₹10 lakh invoice with 18 percent GST, you pay ₹1.8 lakh before collecting from the customer. Multiply across invoices and the working capital need expands rapidly. Input tax credit helps only if vendors file correctly and on time. One vendor’s error can block ITC, forcing out of pocket payments and later reconciliation. E invoicing accuracy matters, errors that block your customer’s ITC can damage relationships. Plan GST payments on realistic collections, not invoice dates.

What is the optimal forecasting period for SMEs?

The 13 week rolling forecast is the gold standard. It covers a quarter, including GST cycles, advance tax, and most payment terms, yet remains accurate and actionable.

Weekly beats monthly for Indian SMEs. GST on the 20th, TDS on the 7th, salaries on the 1st, rent on the 10th, monthly views miss mid month pressure points. Daily is needed only in crisis.

Update weekly. Each Monday, review last week versus forecast, update the coming week with confirmed items, and add week 13. Maintain a lighter monthly view beyond 13 weeks for strategic planning.

How should you structure collection assumptions?

Base assumptions on history, not contract terms. If terms say 30 days but customers average 55, forecast 55. Be conservative for new customers, government clients, and year end periods.

Create probability buckets for invoice collections:

- Week 1 to 2, 10 percent probability

- Week 3 to 4, 20 percent probability

- Week 5 to 6, 30 percent probability, most common window

- Week 7 to 8, 25 percent probability

- Week 9 plus, 15 percent probability, problem accounts

Apply these to outstanding invoices by age and customer. Do not assume everything arrives next week. For government clients, assume 90 plus days unless proven otherwise.

What expenses must you prioritize in tight cash situations?

Priority 1, Statutory and compliance

- GST payments, 18 percent interest plus penalties

- TDS or TCS deposits, 1.5 percent monthly interest plus penalties

- EPF or ESI contributions, damages up to 37 percent per annum

- Advance tax, interest under Sections 234B and 234C

Priority 2, Employees and operations

- Salaries

- Rent

- Critical vendors, those who can halt operations

- Utilities

Priority 3, Negotiable payments

- Non critical vendors with alternatives

- Professional fees

- Marketing expenses

- Discretionary purchases

Never skip statutory payments, interest and penalties compound quickly, and EPF non compliance can have severe consequences. Salaries come next, trust once lost is hard to regain. Vendors usually cooperate when you communicate early and clearly.

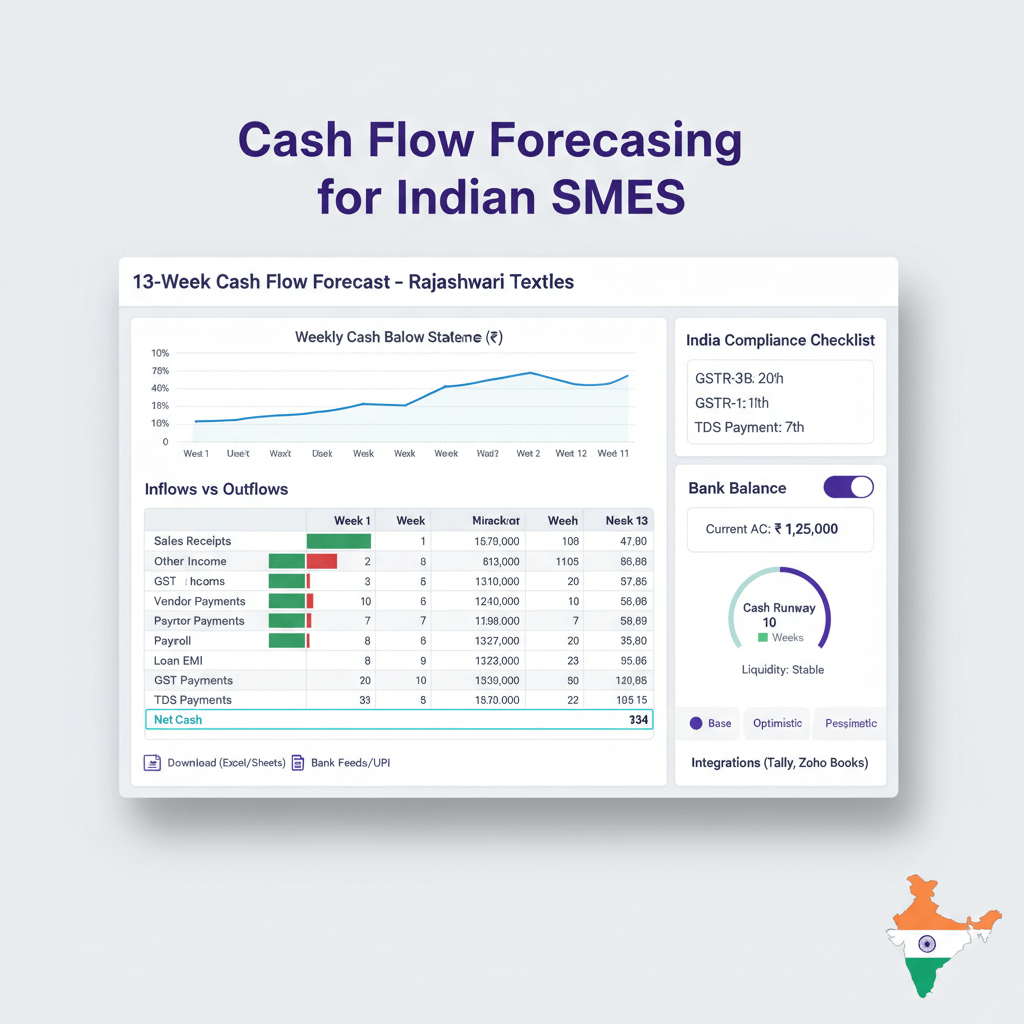

How do you build a practical 13 week forecast template?

You can build a robust 13 week forecast in a simple spreadsheet. Use this structure as a starting point.

| Week | Opening Cash | Collections | GST Refunds | Total Inflows | Salaries | Rent | Vendors | GST Payment | TDS or TCS | Other Statutory | Total Outflows | Net Flow | Closing Cash |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Week 1 | ₹5,00,000 | ₹2,00,000 | ₹0 | ₹2,00,000 | ₹1,50,000 | ₹0 | ₹75,000 | ₹0 | ₹0 | ₹0 | ₹2,25,000 | -₹25,000 | ₹4,75,000 |

| Week 2 | ₹4,75,000 | ₹1,50,000 | ₹50,000 | ₹2,00,000 | ₹0 | ₹1,00,000 | ₹50,000 | ₹0 | ₹30,000 | ₹0 | ₹1,80,000 | ₹20,000 | ₹4,95,000 |

Add rows for your revenue sources and expense categories. Include a variance column for last week’s forecast versus actual. Link invoices to collection rows with probability weights. Update weekly, it becomes your early warning system.

What tools can automate cash flow tracking?

Manual forecasting works, automation saves time and improves accuracy. The right tools pull accounting data, update collections from bank feeds, and flag shortfalls automatically.

- Virtual Accounting by AI Accountant, integrated forecasting plus a compliance calendar

- Zoho Books, cash flow reports with GST context

- Tally Prime, cash flow statements and traditional accounting

- ClearTax, GST focused workflows with payment tracking

- QuickBooks India, automated bank reconciliation

- Float, integrates with popular accounting systems

- Pulse, simple cash flow tracking

- CashAnalytics, enterprise grade forecasting

Stop manual forecasting. Automated daily cash flow updates with compliance deadline alerts help you see problems before they become crises. Book a Demo →

How do you improve forecast accuracy over time?

Track variance weekly and record reasons. If a customer always pays ten days late, build that pattern into your assumptions. Review probability buckets quarterly, adjust for seasonality, and maintain three scenarios, optimistic, realistic, and pessimistic. The gap between scenarios shows risk exposure and guides contingency planning.

What working capital options exist for forecast gaps?

Arrange options before you need them.

- Overdraft or cash credit, 10 to 14 percent, collateralized, renewable

- Working capital loan, 11 to 15 percent, fixed tenure

- Bill discounting, 12 to 18 percent annually, customer credit dependent

- Letter of credit, import or export support, typically 2 to 4 percent cost

- Invoice factoring, 1.5 to 2.5 percent monthly, quick access

- P2P or NBFC loans, 14 to 24 percent, faster processing

- Supply chain financing, often 10 to 16 percent via anchor corporates

- Government schemes such as CGTMSE or MUDRA, eligibility dependent

- Emergency options such as business cards or gold loans, higher cost yet immediate

If gaps recur, secure a permanent facility rather than emergency borrowing. Planned capital is far cheaper than panic money.

How does forecasting integrate with compliance calendars?

Integrating your forecast with compliance calendars prevents the costliest mistakes, missing statutory deadlines.

- GST returns and payment dates, monthly or quarterly

- TDS deposit deadlines, 7th for the previous month

- Advance tax installments, June 15, September 15, December 15, March 15

- EPF or ESI deposits, 15th of following month

- Professional tax, state specific

- Annual compliance, ROC filings and tax returns

Map these into your 13 week view as non negotiable outflows. Consider cumulative impacts, March often clusters advance tax, year end vendor payments, and annual fees. December may include advance tax and bonuses. Compliance integrated forecasting turns deadlines from surprises into planned events.

Conclusion

Cash flow forecasting is not complex modeling, it is disciplined tracking of when money actually moves. A 13 week rolling forecast provides visibility across GST cycles, statutory payments, and collections without drowning in long term guesswork. Build collection assumptions on actual history, not contract terms, and integrate compliance calendars to avoid the expensive mistakes that sink SMEs. Whether you use a simple spreadsheet or automation, weekly updates and variance tracking transform cash management from daily panic into predictable planning.

FAQ

My customers pay in 60 to 75 days but GST is due in 20 days. How do I manage this gap?

This timing mismatch is the biggest cash flow challenge for Indian SMEs. Arrange working capital facilities such as an overdraft or cash credit to bridge the gap. Calculate your average shortfall and secure a limit with a 20 percent buffer. Track customer wise payment patterns, consider invoice factoring for larger orders where the GST component is heavy, and negotiate longer supplier terms to offset the delay. Some businesses price in a 2 to 3 percent premium for extended credit customers to cover the financing cost. Tools like Virtual Accounting by AI Accountant help you quantify the gap precisely.

What is the difference between a cash flow forecast and a cash flow statement?

A cash flow statement looks backward, it reports what actually happened with cash last month, quarter, or year. A cash flow forecast looks forward, it predicts what will happen over the next 13 weeks based on expected collections and payments. The statement supports analysis and compliance, the forecast drives planning and decisions. You need both, your CA prepares statements, your team maintains the forecast.

Should I maintain different forecasts for different scenarios?

Yes, keep three views, optimistic, realistic, and pessimistic. The gaps reveal risk exposure and guide contingency plans. If even the optimistic version shows a shortfall, act immediately. Update all three weekly, yet manage day to day with the realistic case. Virtual Accounting by AI Accountant makes scenario management fast and repeatable.

How do I forecast collections from government departments or PSUs?

Create a separate assumption set. Despite 30 to 45 day terms, actual payment is often 90 to 120 days. A sample split, 10 percent before 60 days, 30 percent in days 61 to 90, 40 percent in days 91 to 120, 20 percent beyond 120. Track fiscal year end acceleration in March. Consider factoring specialized for government receivables. Never schedule critical outflows against expected government collections, they are too unpredictable.

What early warning signs in my forecast should trigger action?

Watch for cash falling below ten days of operating expenses, three straight weeks of negative net cash flow, a downward closing balance trend despite stable revenue, over 60 percent receivables beyond 60 days, or any week where statutory payments cannot be met. Also track persistent variance above 25 percent or excessive dependence on one customer. Each signal warrants action, tighten collections, arrange working capital, or renegotiate terms.

How do I handle seasonal variations in my forecasting?

Build seasonality into assumptions. Diwali can speed retail collections yet slow B2B, March often accelerates payments as books close, April to May can slow while budgets reset, monsoons affect logistics heavy sectors. Compare with the same period last year and adjust for growth. Carry higher cash reserves into slow months. Virtual Accounting by AI Accountant learns patterns from your data to refine seasonality automatically.

Can I use my forecast to negotiate better payment terms with vendors?

Yes. A credible forecast signals discipline. Propose dates aligned to your collections, for example, ₹5 lakhs on the 15th or ₹5.2 lakhs on the 25th. Many vendors prefer certainty over speed. Offer visibility in exchange for extended terms or volume discounts for advance payment when cash allows. The forecast turns negotiations from guesswork into a concrete plan.

What is the minimum data I need to start forecasting?

Start with the essentials, current bank balance, outstanding invoices with likely collection dates, upcoming expenses, and a compliance calendar for GST, TDS, and salaries. Build a 4 week view today, track actuals, then expand to 13 weeks. Do not wait for perfect data, 70 percent accuracy that improves weekly beats doing nothing.

How do I forecast for project based businesses with irregular income?

Use milestone based forecasting. Split each project into advances, stage wise payments, and final settlement. Track milestone completion probability separately from payment probability. Build buffers, if five milestones land in week six, assume only three collect. Keep a pipeline view beyond 13 weeks for visibility. Maintain higher reserves, often 45 to 60 days of operating expenses.

Should I share my cash flow forecast with my team?

Share selectively. Finance needs full visibility, sales should see collection targets, operations should see purchase and expense limits. Avoid broadcasting worst case scenarios widely. Hold monthly reviews showing forecast versus actual to build accountability and improve behavior across teams.

How do lending institutions evaluate my cash flow forecast?

Banks and NBFCs test for realism. Do assumptions match history, are statutory and seasonal items included, are growth and working capital aligned, and what happens if the largest customer delays payment. Include notes on assumptions and document how accuracy has improved. A disciplined forecast plus variance history strengthens your application.

What Excel formulas are most useful for cash flow forecasting?

Useful functions include SUMIF for date ranges or customer totals, VLOOKUP or XLOOKUP for payment terms, IF for probability weights, EOMONTH for month end dates, WORKDAY for business day calculations, FORECAST.LINEAR for simple trends, and variance formulas such as (Actual minus Forecast) divided by Forecast. Use named ranges and data validation for clean templates.

How do I factor in loan EMIs and interest payments?

List each loan with EMI amount and due date, include both principal and interest since cash forecasting tracks outflows. Model floating rates, for example, repo plus a spread. Include fees, renewals, and insurance linked to facilities. Set alerts for covenants that could trigger penalties. Consider prepayments when forecasts show excess cash and interest saved exceeds expected returns.

When should I consider hiring a virtual CFO or outsourcing cash management?

Consider help when cash surprises persist despite forecasting, you spend over ten hours weekly on cash tasks, variance exceeds 30 percent, you manage multiple entities, or statutory delays repeat. Virtual Accounting by AI Accountant delivers automated forecasting, compliance integration, and early warnings at a fraction of CFO cost, often paying for itself by preventing a single penalty or emergency loan.

How do I manage cash flow when scaling rapidly?

Growth consumes cash before it generates it. Build working capital needs into the plan, negotiate milestone payments, consider revenue based financing that scales with sales, factor invoices from strong customers, and keep strict collection discipline. Track your cash conversion cycle closely, small improvements in receivable or payable days have large effects at scale. Never trade cash discipline for growth excitement.

.png)