-01%201.svg)

Key takeaways

- Advance tax must reach 100% by March 15, miss this and you pay 1% monthly interest on the shortfall

- GST returns cascade, one missed GSTR-1 blocks your GSTR-3B, which blocks your refunds and increases scrutiny

- TDS deposits after March 31 cannot be claimed in this year's returns, that's money locked away for 12 months

- Section 80C investments work on cash basis, only what you actually pay before midnight March 31 counts for deductions

What tax deadlines do Indian businesses need to meet by March 31, 2025?

Indian businesses must complete advance tax payments, target 100% of liability, verify TDS deposits, file pending GST returns, and finalize tax-saving investments by March 31, 2025. Missing these deadlines triggers penalties ranging from ₹200 per day for GST delays to 1% monthly interest on unpaid advance tax. The last quarter advance tax installment, 15% of annual liability, is due March 15, while all Section 80C investments must be completed before March 31. Virtual Accounting by AI Accountant tracks these deadlines automatically and sends alerts 30 days before each due date.

March 31 isn't just another date on your calendar, it's when every tax decision you've postponed comes due at once. You're juggling advance tax calculations, hunting for TDS certificates, and wondering if that NPS contribution you've been planning actually needs to happen today.

Most founders discover their tax gaps in March. The smart ones have a checklist. This guide walks you through every deadline, every form, and every penalty you're facing if you miss them, plus the exact steps to get compliant before the clock runs out.

The March 31 Reality: What Actually Happens at Midnight

When March 31 ends, five tax windows close simultaneously, and they won't open again for another year. Your advance tax liability becomes final, triggering interest from April 1 if you're short. Your GST input tax credit for the financial year locks, meaning any invoices you haven't claimed are potentially lost. TDS payments made after midnight shift to next year's returns, creating a cash flow gap you'll feel for months.

The numbers tell the story: a ₹10 lakh advance tax shortfall costs you ₹1,000 per month in interest under Section 234C. A missed GSTR-3B filing attracts ₹50 per day in late fees, capped at ₹5,000, plus 18% annual interest on the tax amount.

These aren't warnings, they're automatic system-generated demands that hit your bank account without negotiation.

What if I'm reading this after March 20?

If you're in the last 10 days of March, focus on three things only. First, calculate and pay your final advance tax installment, even a partial payment reduces interest. Second, file all pending GST returns in sequence, GSTR-1 first, then GSTR-3B, the late fee is better than losing ITC. Third, complete any Section 80C investments you've planned, the annual limit is ₹1.5 lakh and every rupee invested reduces your tax liability.

Don't attempt everything. A rushed tax audit is worse than paying the late filing penalty. A wrongly filed GST return takes months to revise. Pick the deadlines with the highest penalties and focus there.

How do penalties compound after March 31?

Penalties don't just add up, they multiply. Miss your advance tax payment and you pay interest under three sections: 234A for late filing, 234B for shortfall in total advance tax, and 234C for shortfall in each quarterly installment. A ₹5 lakh tax liability with zero advance tax paid could generate ₹30,000 in interest charges by the time you file your return in July.

GST penalties work differently but hurt more. Late filing blocks your buyers from claiming input tax credit on your invoices, potentially damaging business relationships. The system auto-blocks GSTR-1 filing if previous returns are pending, creating a cascade where one missed deadline in January can lock you out of compliance through June.

Fixing these issues before March 31 costs time, fixing them after costs both time and money.

Critical Compliance Deadlines Hitting This Month

The March compliance calendar reads like a stress test for your accounting system. Advance tax final installment hits March 15, that's 100% of your yearly liability due, with 1% monthly interest on any shortfall. GST returns for February close March 20 for GSTR-1 and March 22 for GSTR-3B, with daily penalties starting immediately after. TDS for February salaries must be deposited by March 7, while TDS on all other payments needs to be in by March 30 to count for this financial year.

Your employees need Form 16A by March 31 if you've deducted TDS on any non-salary payments to them. Miss this and face penalties under Section 272A, ₹100 per day per certificate. The quarterly TDS return, Form 26Q for salaries, Form 27Q for non-residents, covering January to March isn't due until May 31, but the underlying deposits must happen now.

Which deadlines trigger automatic penalties?

Four deadlines trigger system-generated penalties without human intervention. GST late fees start accumulating at midnight on the due date, ₹50 per day for GSTR-3B, ₹20 for nil returns. Advance tax interest calculates automatically when you file your income tax return, the system compares what you paid against what you owed and applies Section 234C. TDS late deposit interest runs at 1.5% per month from the deduction date. Professional tax penalties vary by state but typically start at ₹500 per month in Maharashtra and Karnataka.

The GST portal won't let you file future returns until you clear past dues. The income tax system adjusts your refunds against outstanding demands. These aren't notices you can appeal, they're automatic deductions from your money.

What about industry-specific compliances?

Different sectors face additional March deadlines that generic tax guides miss. Startups claiming Section 80IAC benefits must ensure their eligibility certificate is valid through March 31. Manufacturing units need to reconcile their GST ITC with physical inventory, mismatches trigger audits. Service exporters must file their Letter of Undertaking for zero-rated supplies before year-end or lose the benefit.

Software companies claiming deductions under Section 10AA for SEZ units need to ensure their export proceeds are received by March 31 to count for this year's benefits. E-commerce operators have until March 31 to issue Form GSTR-9B to their suppliers, miss this and your suppliers can't file their annual returns.

Virtual Accounting by AI Accountant handles these deadlines differently than traditional CAs who might miss sector-specific requirements. The platform tracks your industry classification and automatically surfaces relevant deadlines you might not even know exist. Your dedicated CA team knows whether you need SEZ documentation or startup certificates, they don't wait for you to ask.

Want to see how it works? Watch this short video.

The deadlines you miss in March determine the penalties you pay all year.

Tax-Saving Investments and Deductions Expiring March 31

Section 80C's ₹1.5 lakh deduction limit expires at midnight March 31, taking with it your easiest path to reducing tax liability. The math is straightforward: earn ₹15 lakh, invest ₹1.5 lakh in 80C instruments, save ₹46,800 in taxes if you're in the 30% bracket. Miss the deadline and that money goes to the government instead of your retirement fund.

Your investment must be completed, not just planned, by March 31. ELSS mutual fund purchases need to be processed, NAV allotted, units credited. PPF contributions must hit the account, not just leave yours. Life insurance premiums need receipt numbers generated. NSC certificates require physical or digital possession. The tax department works on cash basis for these deductions, promises and pending transactions don't count.

Beyond 80C, you're losing other deductions too. Section 80D for health insurance gives ₹25,000 deduction for self and family, another ₹50,000 for senior citizen parents, but only if premiums are paid by March 31. NPS contributions under Section 80CCD(1B) add another ₹50,000 deduction on top of 80C. Home loan borrowers get unlimited deduction on interest under Section 24, but the EMI must be paid before year-end.

Which investments can I still make in the last week?

Seven investments can be completed instantly online, even on March 31. ELSS mutual funds process same-day if you invest before 3 PM through the AMC website. PPF contributions via net banking credit immediately. Term insurance bought online generates instant receipts for 80C claims. NPS contributions through eNPS reflect within hours. Digital NSC through authorized banks provides immediate certificates. Tax-saving FDs can be opened online with instant confirmation. ULIP policies bought before midnight count if the payment is processed.

Skip physical instruments in the last week, post office schemes, physical NSC, offline insurance need processing time you don't have. Focus on digital channels that provide immediate proof of investment.

How do I maximize deductions if I'm over 80C limit?

Once you've exhausted ₹1.5 lakh in 80C, shift focus to uncapped deductions. NPS gets you additional ₹50,000 under 80CCD(1B) beyond the 80C limit, that's ₹15,000 tax saved in the 30% bracket. Health insurance for parents offers ₹50,000 deduction if they're senior citizens, ₹25,000 otherwise. Donations to specified funds under 80G give 50% or 100% deduction with no upper limit, PM CARES Fund donations get 100% deduction.

Education loan interest under Section 80E has no cap, every rupee of interest paid reduces taxable income. Medical treatment for specified diseases under 80DDB provides up to ₹1 lakh deduction. The key is documenting everything, the tax department needs receipts, certificates, and proof of payment for each claim.

But investment decisions made in March panic rarely align with your actual financial goals.

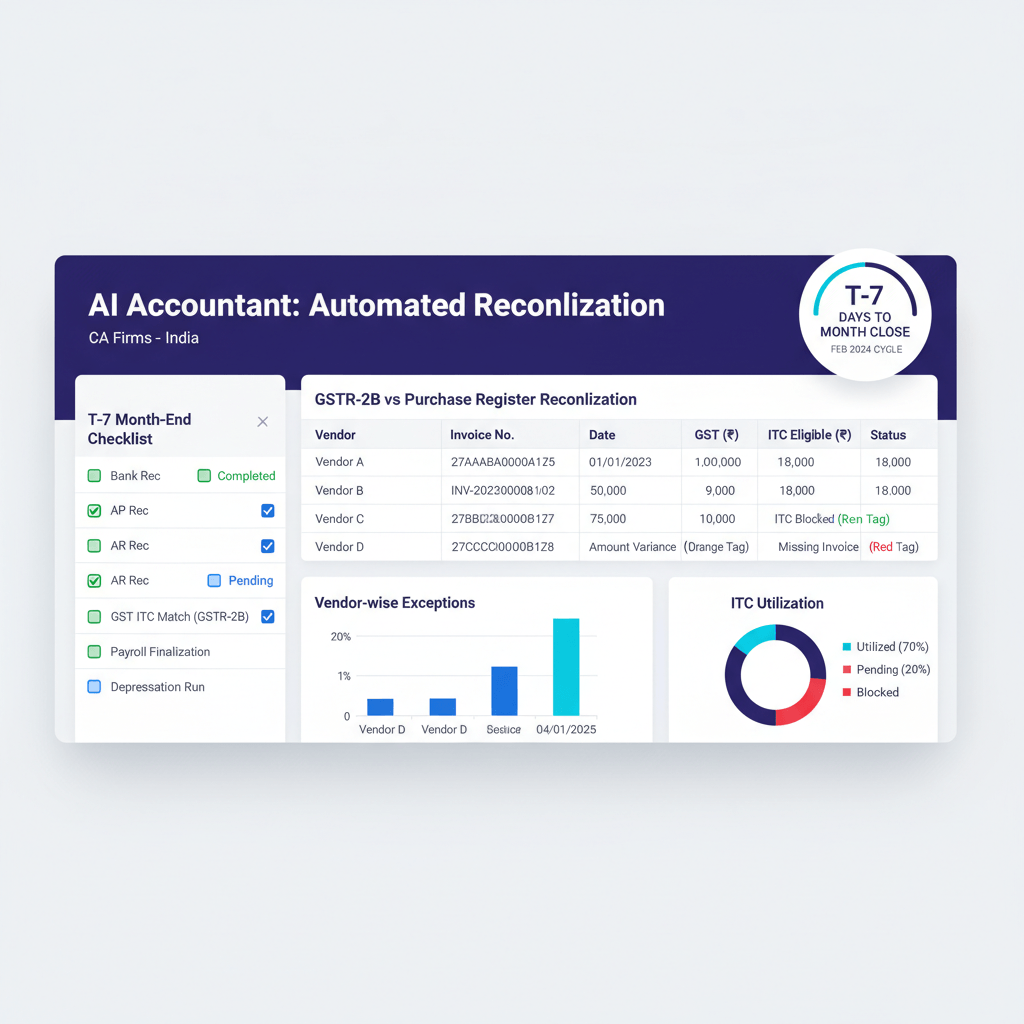

GST Return Cascade: Why One Missing Return Blocks Everything

GST returns work like dominoes, knock one over and the rest fall in sequence. Miss GSTR-1 for any month and the portal blocks your GSTR-3B filing. Can't file GSTR-3B? Your buyers lose input tax credit on your supplies. Haven't filed returns for six months? The portal suspends your GST registration, freezing your ability to do business legally.

The February GSTR-1 due March 20 contains all your sales for the month. Your buyers need this data to claim input tax credit in their March returns. If you miss the deadline, they can't claim ITC, potentially damaging business relationships. The GSTR-3B due March 22, your actual tax payment return, won't process without GSTR-1 filed first. Miss both and you're looking at ₹100 daily in late fees plus 18% annual interest on unpaid tax.

The annual return GSTR-9, though due December 31, needs all monthly returns filed first. Start missing returns now and you're creating a compliance backlog that compounds through the year. The new rule effective January 2022 restricts ITC claims to invoices not older than the tax year, miss claiming them by March 31 and they're potentially gone forever.

What's the correct filing sequence to avoid blocks?

File in this exact order to avoid system blocks: First, clear all pending GSTR-1 returns starting from the oldest. The portal won't let you skip months. Second, file corresponding GSTR-3B returns, each GSTR-3B needs its matching GSTR-1 filed first. Third, file GSTR-2B reconciliation if you have ITC mismatches. Fourth, handle amendments through Table 9B in the next month's GSTR-1 rather than trying to revise filed returns.

If you're blocked, check for unfiled previous returns, pending payments from earlier months, suspended registration due to non-filing, or mismatched GSTR-2A entries. The portal's error messages are cryptic, "technical error" usually means you have a compliance block elsewhere.

How do I claim pending Input Tax Credit before year-end?

ITC claims follow strict timelines, you have until September 30 following the financial year or the annual return filing date, whichever is earlier. But practically, claiming old ITC gets harder with time. Reconcile your purchase register with GSTR-2B by March 25, giving you five days to follow up with suppliers who haven't filed their returns.

For missing credits, send reminder emails to suppliers with invoice details and GST amounts. If they've filed but credits don't appear, check for GSTIN mismatches, wrong tax period selection, or incorrect invoice numbers. The system matches invoices exactly, even a single-digit difference blocks the credit. Focus on high-value invoices first, chasing ₹500 credits when you have ₹50,000 pending isn't efficient.

The GST you don't claim by March 31 becomes working capital locked away from your business.

TDS and TCS: The Hidden Cash Flow Trap

TDS isn't just a compliance requirement, it's your money sitting in government accounts, and March 31 determines when you get it back. Deposit TDS after March 31 and those funds won't show in your Form 26AS for this financial year. That means waiting until July next year to claim refunds on tax already paid. For a business deducting ₹50,000 monthly in TDS, that's ₹6 lakh locked away for over a year.

Every TDS payment needs three things before March 31: the deduction from the payment, the deposit to government through challan, and the certificate issued to the deductee. Miss any step and you face penalties. Late deposit attracts 1.5% monthly interest from the deduction date. Late filing of TDS returns costs ₹200 per day. Non-issue of TDS certificates triggers ₹100 per day per certificate under Section 272A.

TCS creates similar problems but from the other side. If you're buying goods worth over ₹50 lakh or sending money abroad for education, the seller collects TCS. This TCS only appears in your Form 26AS after the collector deposits it. March transactions might not reflect until April, creating temporary cash crunches when you can't claim the credit immediately.

What are current TDS rates and when do they change?

Standard TDS rates for FY 2024-25 include salary as per slab rates, professional fees at 10%, rent above ₹2.4 lakh yearly at 10%, contractor payments at 1% for individuals and 2% for companies, commission at 5%, and interest at 10%. Budget updates apply from April 1 as notified each year.

Double-check rates for specific transactions, insurance commission differs from regular commission, payment to non-residents needs tax treaty consideration, and transactions below threshold limits need no TDS. Getting the rate wrong means either over-deduction, locking excess funds, or under-deduction, attracting penalties and interest.

How do I verify all TDS credits appear in Form 26AS?

Form 26AS updates within 7 days of TDS deposit, but verify everything by March 25. Log into the income tax portal, download Form 26AS for the current financial year, and match every entry against your books. Look for missing entries, incorrect amounts, wrong financial year classification, and PAN mismatches that prevent credits from appearing.

Common issues: Deductor's PAN not linked to TAN causes non-reflection, incorrect financial year selection while depositing pushes credits to wrong year, and using wrong section codes makes credits unclaimable. If credits are missing, first check the deductor's TDS return filing status, unfiled returns mean no credits in your Form 26AS.

For missing salary TDS, your employer must revise their return. For other TDS, request revised TDS certificates and follow up on return filing. Keep screenshot evidence of all follow-ups, you might need them during assessment proceedings.

Missing TDS credits aren't just compliance issues, they're interest-free loans to the government.

Documents You Need Ready by March 31

Tax planning without documentation is just expensive guesswork. By March 31, you need proof for every deduction claimed, every expense booked, and every compliance met. The tax department doesn't accept explanations, they accept documents. Missing even one critical proof can trigger reassessment, penalties, and years of correspondence.

Start with investment proofs: Section 80C investments need receipts showing payment before March 31, insurance policies need premium receipts with policy numbers, ELSS statements showing units allotted, PPF passbook entries or online statements, and NSC certificates in physical or digital form. For 80D claims, health insurance premium receipts must show policy period covering the financial year and payment made through non-cash modes.

Business expense documentation is equally critical: GST invoices for all purchases claimed as business expenses, vendor bills with PAN for TDS compliance, travel bills linking expenses to business purpose, salary registers and Form 16 for all employees, and rent agreements with landlord PAN for HRA or office rent claims. Digital copies stored in cloud folders beat physical files that get lost during income tax scrutiny three years later.

Which documents do tax officers ask for most often?

Five documents trigger most scrutiny queries: Bank statements showing all business transactions, officers match these against return entries, bills for expenses over ₹50,000, high-value transactions get extra attention, rent agreements and rent receipts, HRA claims face heavy verification, cash payment vouchers over ₹10,000, violates Section 40A(3) limits, and related party transaction proofs, loans, advances, or sales to family members need clear documentation.

Keep six months of bank statements downloaded, GST return acknowledgments saved, TDS certificates in sequential order, major purchase invoices highlighted, and audit report drafts if turnover exceeds limits. Officers ask for these during assessment, having them ready saves weeks of back-and-forth.

What's the fastest way to organize year-end documentation?

Create five digital folders: Income Proofs, salary slips, Form 16, business income computation, Investment Proofs, 80C receipts, 80D premiums, 80G donations, Expense Bills, categorized by type with amounts over ₹20,000 separately, Compliance Documents, GST returns, TDS certificates, advance tax challans, and Audit Papers, if applicable, balance sheet, P&L, tax audit report.

Name files systematically, "80C_ELSS_March2024_15000.pdf" beats "investment1.pdf" when you're searching during assessment. Upload everything to cloud storage with sharing permissions ready, your CA needs access, and you might need documents while traveling. Physical documents go in a single file with an index sheet listing everything, don't scramble during a tax notice response.

Virtual Accounting by AI Accountant eliminates this March scramble completely. Every invoice, receipt, and compliance document gets uploaded real-time throughout the year. The platform auto-categorizes expenses, tracks deductions, and maintains audit-ready documentation. When March comes, you're reviewing organized records, not hunting for receipts. Your dedicated CA already has everything needed for year-end filing.

Without proper documentation, every tax-saving decision you've made this year becomes a potential penalty next year.

Last-Minute Tax Optimization Strategies

Ten days before March 31, sophisticated tax planning is over, now it's about damage control and quick wins. The strategies that work in March are different from year-round planning. You're not optimizing anymore, you're salvaging what you can from the financial year's tax liability.

Prepayment strategies work when you have cash available. Pay April to June rent in March and claim the full deduction this year. Clear next year's insurance premiums before March 31 for immediate 80D benefits. Buy annual software subscriptions, professional memberships, and service contracts, legitimate business expenses that reduce taxable income. Just ensure you have bills dated before March 31 and payment proof through banking channels.

Timing strategies shift income and expenses between years. Defer March invoicing to April if you're already in a higher tax bracket this year. Accelerate expense recognition by clearing all pending vendor bills, booking provisions for probable expenses, and writing off bad debts you've been avoiding. If you're GST registered, ensure March purchases are billed in March, April bills mean waiting another month for input tax credit.

Can I still restructure my salary in March?

Salary restructuring in March only works for future months, but you can still optimize. Request your employer to pay pending reimbursements, LTA, medical, phone bills, before March 31, these are tax-free up to limits. If you have performance bonuses due, taking them as reimbursements instead of taxable income saves 30% in taxes. Convert part of April's salary to allowances if your employer agrees, HRA, books and periodicals, internet allowances reduce taxable income.

For business owners paying themselves salary, March allows more flexibility. Pay yourself rent for home office use, with proper rent agreement, reimburse business expenses you paid personally, and adjust your director's remuneration to optimize tax brackets. Just ensure board resolutions are dated before March 31 and payments actually happen, backdating doesn't work during scrutiny.

What tax elections must be made by March 31?

Several one-time tax choices expire March 31 and can't be reversed. Opting for new tax regime versus old regime affects your entire tax calculation, choose based on actual deductions available, not theoretical benefits. Presumptive taxation under Section 44AD or 44ADA locks you in for five years, opt only if you're certain about future income levels.

Capital gains decisions need March execution. Sell loss-making stocks to offset gains, but avoid immediate buybacks that could attract questions. Convert short-term holdings to long-term by holding past one year, the tax difference is substantial. For property, executing sale agreements before March 31 determines which year's capital gains apply.

Form 10E for relief under Section 89 must be filed if you received arrears, this spreads the tax burden across years. The option to carry forward business losses needs active election in your return. Missing these elections means paying unnecessary tax with no recourse.

Common Mistakes That Trigger Penalties and Scrutiny

The mistakes that cost the most aren't the complex ones, they're the simple oversights that trigger automatic penalties and scrutiny flags. Missing the ₹10,000 cash payment limit under Section 40A(3) disallows your entire expense claim. Claiming HRA while owning property in the same city triggers immediate verification. Round-number donations, especially in March, flag your return for review.

GST mistakes compound quickly. Claiming input tax credit without matching invoices in GSTR-2B triggers notices. Filing GSTR-3B with payment shortfalls blocks future returns. Missing the annual return deadline permanently blocks certain credits. The worst part, GST penalties are system-generated, leaving no room for explanation or appeal until after you've paid.

Income tax errors hide until assessment. Claiming both standard deduction and actual expenses isn't allowed but only surfaces during scrutiny. Missing TDS on professional fees over ₹30,000 attracts 100% penalty on the tax amount. Interest calculations on loans from family need documentation or they're treated as unexplained income. These errors might take two years to surface, but when they do, you're paying penalties plus interest from the original due date.

What triggers automated tax notices?

The income tax system runs automated checks that trigger notices without human intervention. High-value transactions over ₹10 lakh not matching with return income, cash deposits over ₹50 lakh in savings accounts, mismatch between Form 26AS and return claims, foreign remittances without proper documentation, and sale of property not reported in returns all trigger system-generated notices.

GST intelligence system flags different patterns: ITC claims exceeding industry standards, sudden drops in turnover, consistent nil returns after regular filing, exports without matching shipping bills, and high refund claims relative to tax paid. These flags don't mean you're wrong, but they do mean you'll spend months proving you're right.

How do I respond to a tax notice received in March?

March notices need immediate attention, you might have just days to respond. First, verify the notice is genuine through the e-filing portal's View Notices section. Never respond to email notices without portal verification. Check the notice type: intimation under 143(1) needs online response only, scrutiny notice under 143(2) needs documentation, demand notices need payment or disagreement filing.

Respond within the timeline, extensions are rarely granted in March. For demand notices, pay first and appeal later if the amount is small, interest keeps accumulating during disputes. For scrutiny notices, submit only what's asked, over-documentation raises more questions. Keep response copies and acknowledgments, the department sometimes claims non-receipt of responses.

If you receive multiple notices, prioritize by penalty amount and response deadline. A ₹5,000 GST demand needs immediate payment, while a scrutiny notice might allow 30 days for response.

Every mistake in March becomes a penalty in April, and an audit trigger for the next three years.

Setting Up Next Year's Tax System

March 31 isn't just about closing this year, it's about ensuring you never face this scramble again. The difference between founders who panic every March and those who don't isn't knowledge, it's systems. Set these up before April 1 and next year runs on autopilot.

Start with automated advance tax calculation. Create a simple spreadsheet that estimates quarterly tax based on monthly revenue and expenses. Set calendar reminders for June 10, September 10, December 10, and March 10, five days before each advance tax deadline. Link your accounting software to auto-populate actual figures. This one system prevents most advance tax penalties.

Build document discipline into daily operations. Every bill gets scanned immediately. Every payment gets a screenshot. Every tax-saving investment generates a PDF receipt saved in designated folders. Use apps that capture scans clearly for physical documents. Create WhatsApp groups with your CA for real-time document sharing. The March scramble happens because eleven months of documents pile up, daily discipline takes five minutes but saves weeks.

Separate compliance tracking from execution. Use a compliance calendar, Google Calendar works fine, with alerts 30 days before each deadline. GST return dates, TDS payment dates, advance tax installments, and certification renewals all go in immediately. But don't rely on memory for execution, assign each compliance to someone specific, whether it's your accountant, CA, or yourself.

What monthly routine prevents year-end chaos?

Block the 5th of every month for tax review. Check previous month's GST filing status, verify TDS deposits match deductions, review expense bills for compliance issues, and ensure all invoices are raised with correct tax rates. This one routine catches errors while they're fixable, not in March when it's too late.

Create three tracking sheets updated monthly: Income tracker, revenue, other income, capital gains, Expense tracker, category-wise, highlighting cash payments, and Investment tracker, 80C progress, planned versus actual. By December, you know exactly where you stand instead of discovering gaps in March.

Which tools and advisors actually help?

Tools that matter: accounting software that integrates with GST portal, Zoho Books, Tally Prime, expense tracking apps that capture bills instantly, Expensify, Happay, and cloud storage for document management, Google Drive, Dropbox. Skip complex ERPs unless you have dedicated staff, simple tools used consistently beat sophisticated systems used sporadically.

For professional help, distinguish between transactional and advisory needs. A bookkeeper handles data entry and basic compliance. A tax preparer files returns but doesn't plan. A CA provides advisory but might miss deadlines without systems. Virtual Accounting by AI Accountant combines all three, bookkeeping through the platform, compliance through automation, and advisory through your dedicated CA team. The real-time dashboard shows your tax position daily, not just in March.

The best tax strategy isn't about saving taxes, it's about never being surprised by them.

Conclusion

March 31 doesn't have to be chaos. Every deadline hitting this month, advance tax, GST returns, TDS deposits, investment proofs, follows predictable rules with specific penalties. You now know what triggers automatic penalties, which documents prevent scrutiny, and how to salvage tax benefits even in the last week.

The patterns are clear: compliance cascades, one missed GST return blocks everything, penalties compound, every day of delay costs more, and documentation determines outcomes, no proof means no deduction. Whether you're scrambling this March or planning for next year, the solution isn't working harder in March, it's building systems that work all year.

Tax compliance isn't about perfection. It's about consistency, documentation, and knowing which deadlines you cannot miss. Get those right, and March 31 becomes just another date on your calendar.

FAQs

What happens if I miss the March 15 advance tax deadline by one day?

Missing the March 15 advance tax deadline triggers automatic interest under Section 234C at 1% per month on the shortfall amount. If you owed ₹1 lakh as final installment and pay on March 16, you'll pay ₹1,000 as interest for that one-day delay. The interest calculates from March 16 until you file your return, potentially adding thousands to your tax bill. Virtual Accounting by AI Accountant sends automated alerts 30 days, 7 days, and 1 day before advance tax deadlines, ensuring you never miss these costly dates.

Can I claim GST input tax credit for invoices dated March but received in April?

You can claim ITC for March invoices received in April, but only if your supplier files their GSTR-1 for March and the invoice appears in your April GSTR-2B. The deadline is September 30 following the financial year or your annual return filing date, whichever is earlier. However, if your supplier delays filing beyond this window, you permanently lose that credit. Track pending credits weekly and follow up with suppliers before March 25 to ensure they file on time.

What's the penalty if my accountant forgot to deposit TDS for February salaries?

Late TDS deposit attracts 1.5% monthly interest from the deduction date until deposit. For February salaries with TDS of ₹50,000 due March 7, depositing on March 31 means 24 days delay, costing ₹600 in interest. Additionally, you face ₹200 per day penalty for late filing of quarterly TDS return, maximum ₹10,000, and ₹100 per day per certificate for delayed Form 16 issuance to employees. The real cost, employees can't claim credit in their returns, damaging workplace trust.

How late can I invest in ELSS on March 31 and still claim deduction?

ELSS investments made before 3:00 PM on March 31 through online platforms get same-day NAV and count for current year deduction. Investments after 3:00 PM or through offline mode get next working day's NAV, pushing them to the next financial year. The ₹1.5 lakh limit under Section 80C is on payment basis, the money must leave your account by midnight March 31. Use direct AMC websites or apps for instant processing and immediate investment proof generation.

My turnover is ₹2.8 crore - do I need tax audit by March 31?

With ₹2.8 crore turnover, you need tax audit if you're not opting for presumptive taxation under Section 44AD. The audit must be completed and Form 3CD uploaded before filing your return, due July 31 for non-audit cases, September 30 for audit cases. Start the audit process by March 15, auditors need time to verify books, and last-minute audits often miss deductions. If 95% of your transactions are digital, the audit threshold increases to ₹10 crore, potentially exempting you.

What if I discover old pending GST returns while filing March returns?

File pending returns immediately in chronological order, the portal won't allow skipping months. Each delayed GSTR-3B attracts ₹50 per day late fee, ₹20 for nil returns, capped at ₹5,000 per return, plus 18% annual interest on tax dues. File GSTR-1 first for each month, then GSTR-3B. For returns older than two years, you might need to approach GST authorities for manual processing. Virtual Accounting by AI Accountant's compliance tracker would have flagged these gaps months ago, preventing cascade blocks.

Can I pay next year's rent in advance to claim deduction this year?

Advance rent payment is allowed as deduction on payment basis if you maintain books on cash system. Pay April to June rent in March and claim the entire amount this financial year. You need a rent agreement mentioning advance payment terms and payment proof through banking channels. For amounts over ₹50,000 monthly, ensure TDS is deducted at 10% on the full advance amount. This strategy works for office rent, business expense, and house rent, HRA, but get receipts dated March 31 or earlier.

My CA hasn't filed my returns for 2 years - what penalties am I facing?

Non-filing for two years triggers multiple penalties. Late filing fee under Section 234F is ₹5,000 per year, ₹10,000 total if income exceeds ₹5 lakh. Interest under Section 234A runs at 1% monthly on tax payable, potentially 24% for two years. If you had refunds due, you've lost them, refunds for AY 2022-23 can't be claimed after March 31, 2024. File immediately through a new CA or Virtual Accounting to stop interest accumulation and prevent prosecution proceedings that begin after repeated non-filing.

What documents prove work-from-home expenses for tax deduction?

Work-from-home expenses need specific documentation: electricity bills showing increased usage versus pre-WFH period, internet bills in your name with speed upgrade for work, rent receipts if claiming proportionate home office space, and employer certificate confirming WFH arrangement. Calculate business use percentage, hours worked times space used divided by total, and maintain a log. Without employer reimbursement policy, these expenses aren't directly deductible for salaried individuals, but can strengthen your case if claiming business income under Section 44ADA.

Do I need to pay tax on ₹15 lakh sitting in my current account?

Money sitting in your account isn't taxable by itself, it's already taxed income if properly reported. However, if this ₹15 lakh appeared suddenly or doesn't match your declared income sources, expect notices. The bank reports cash deposits over ₹10 lakh annually to the income tax department. Keep proof of source, sale deed if from property, gift deed if from family, loan documents if borrowed. If it's accumulated savings, maintain a trail showing regular transfers from salary or business income accounts.

How do I rectify wrong TDS deduction by my client?

For excess TDS, claim refund in your income tax return, you'll get it back after processing. For short TDS deduction, your client must deposit the differential immediately with interest at 1% monthly from deduction date. They need to file revised TDS return reflecting correct amounts. You need revised Form 16A or 16 as proof. If they refuse, you'll pay the tax difference yourself during return filing. Document all communication, you might need it during scrutiny to prove the error wasn't yours.

Can I shift from old tax regime to new regime on March 31?

Yes, you can switch between tax regimes until you file your return, due July 31 for most individuals. Compare both calculations, old regime if you have over ₹2.5 lakh in deductions, new regime if you have minimal deductions. Salaried employees must inform employers about regime choice through declaration, but can still switch while filing returns. Business owners have flexibility until filing. The new regime offers lower rates but fewer deductions, calculate actual tax, not theoretical benefits, before switching.

What's the safest way to handle cash transactions before year-end?

Keep every cash transaction below ₹10,000 to avoid Section 40A(3) disallowance. For larger amounts, use account payee cheques, bank transfers, or UPI, all create automatic trails. Maintain cash book with daily entries, supported by numbered vouchers signed by recipients. Deposit excess cash before March 31, large year-end cash deposits trigger scrutiny. For business expenses, prefer vendors who accept digital payments. Virtual Accounting tracks cash transactions separately, flagging any that approach statutory limits.

My bank statement shows different balance than my books - how do I reconcile?

Bank reconciliation before March 31 is critical. List all cheques issued but not cleared, online payments in process, auto-debits pending, and bank charges not recorded. The difference should match exactly. Unreconciled differences become unexplained income during scrutiny. Common misses: GST auto-debit on 20th, TDS payment confirmation delays, year-end interest credits, and bounced cheque entries. Reconcile weekly in March, daily if differences exceed ₹1 lakh. Your final reconciliation becomes part of audit documentation.

Should I register for GST if my turnover is ₹18 lakh in March?

With ₹18 lakh turnover, you're below the ₹20 lakh threshold for service providers, ₹40 lakh in some states for goods. However, if you expect to cross ₹20 lakh in April, register now, GST registration takes about a week, and operating without GST when required attracts 10% penalty on tax amount. Consider voluntary registration if your clients need input tax credit, you make interstate supplies, or you want to appear more credible. Once registered, compliance becomes monthly and mandatory, ensure you have systems to handle it.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.