Key Takeaways

- Annual compliance is the complete set of mandatory legal, tax, and regulatory filings every registered Indian company or LLP must complete each financial year, regardless of revenue or activity level

- Private limited companies must file at minimum: AOC-4, MGT-7 or MGT-7A, ITR-6, and hold an AGM each year

- Missing ROC filings attracts penalties of ₹100 per day per form under the Companies Act 2013, with no upper cap

- India's financial year runs April 1 to March 31, most ROC deadlines fall between September and November

- Annual compliance is not the same as annual filing, annual compliance is the broader umbrella, annual filing refers specifically to ROC forms AOC-4 and MGT-7

- Directors are personally liable for compliance failures, disqualification under Section 164(2) can bar a director from every board seat in India for five years

Introduction

What is annual compliance? Here is the short answer: it is the complete set of legally mandated filings, disclosures, returns, and procedural obligations that every registered business entity in India must fulfil within each financial year, under the Companies Act 2013, the Income Tax Act 1961, the GST Act 2017, and other applicable statutes.

It is not optional. It does not pause when your revenue is zero. It does not disappear because you forgot to budget for it. The moment your company is incorporated, the compliance clock starts, and it runs every single year until the company is formally wound up.

Miss it, and the consequences compound fast, financially, legally, and reputationally. A Bengaluru SaaS startup that filed its ROC forms six months late on two forms alone owed ₹36,000 in penalties before it paid a single rupee in tax. That is before income tax interest, GST late fees, or the cost of a CA to clean up the mess.

This guide walks you through what annual compliance actually means, what it covers, when it is due, what it costs to miss, and how to get it done.

Annual Compliance Meaning — What It Actually Covers

The term "annual compliance" is not a single form or a single deadline. It is a composite of all statutory obligations falling due within one financial year, drawn from at least four distinct legal frameworks simultaneously.

The four pillars of annual compliance:

| Pillar | Governing Law | Headline Obligations |

|---|---|---|

| ROC / MCA | Companies Act 2013 | AOC-4, MGT-7/7A, AGM, Board Meetings, ADT-1 |

| Income Tax | Income Tax Act 1961 | ITR-6, Tax Audit (Form 3CA/3CB+3CD), TDS Returns |

| GST | GST Act 2017 | GSTR-9 Annual Return, GSTR-9C Reconciliation |

| Labour Laws | PF Act, ESIC Act, State PT Acts | PF Returns, ESIC Returns, Professional Tax |

For a standard private limited company with employees and GST registration, annual compliance involves a minimum of 15 to 20 distinct filings across the financial year. That number is not an exaggeration, it counts each quarterly TDS return, each GST return, the ROC filings, the ITR, the tax audit, the AGM, and the board meeting minutes individually.

Statutory annual compliance, a phrase you will hear from CAs and company secretaries, refers specifically to obligations mandated by an Act of Parliament, as opposed to voluntary governance actions like internal audits or board committees. Everything in this guide qualifies as statutory.

Annual compliance is also distinct from your ongoing monthly compliance: monthly GST returns (GSTR-1, GSTR-3B), monthly TDS deposits, monthly payroll filings. Those run in parallel. Annual compliance is the layer that sits on top of them.

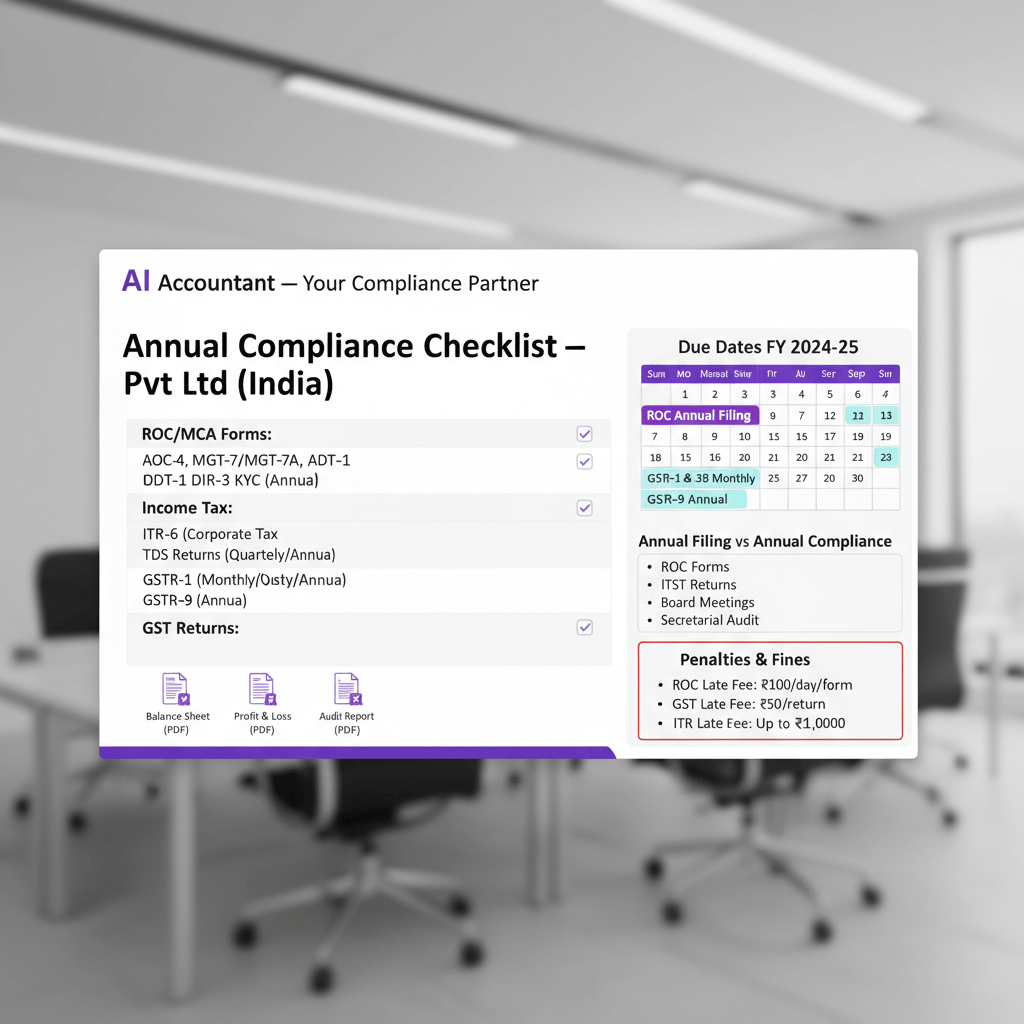

Annual Compliance For Pvt Ltd Companies — The Core Mandatory Checklist

ROC And MCA Filings (Companies Act 2013)

AOC-4 — Financial Statements Filing

Due within 30 days of the Annual General Meeting (AGM). If the AGM is held on 30 September, AOC-4 is due by 30 October. Attach the balance sheet, profit and loss account, cash flow statement, auditor's report, and board report.

MGT-7 / MGT-7A — Annual Return

MGT-7 applies to companies with paid-up capital of ₹10 crore or more, or turnover of ₹50 crore or more. MGT-7A is for small companies and OPCs. Both are due within 60 days of the AGM, typically 29 November if the AGM was held on 30 September.

ADT-1 — Auditor Appointment

File within 15 days of the AGM when an auditor is appointed or reappointed. A statutory auditor must be a registered CA firm.

AGM — Annual General Meeting

Must be held within six months of the financial year end, meaning by 30 September each year. At the AGM, shareholders formally adopt the financial statements, reappoint the auditor, and declare any dividend. This is not just a formality, if the AGM is not held, AOC-4 cannot be filed because the financials have not been legally adopted.

Board Meetings

A minimum of four board meetings per year, with no gap exceeding 120 days between two consecutive meetings (Section 173 of the Companies Act 2013). Each meeting must be properly noticed and minuted.

DIR-3 KYC

Every director must complete KYC by 30 September each year. Missing it deactivates the Director Identification Number (DIN), and reactivation costs ₹5,000.

Income Tax Filings

ITR-6

All companies, except those claiming exemption under Section 11, file ITR-6. Deadline: 31 October for companies requiring a tax audit, 31 July for those that do not.

Tax Audit — Form 3CA/3CB + 3CD

Mandatory when turnover exceeds ₹1 crore for non-digital transactions, or ₹10 crore when 95% or more of receipts and payments are digital. The CA signs and submits the audit report by 30 September.

TDS Annual Returns

Form 24Q (salary TDS), Form 26Q (non-salary payments to residents), Form 27Q (non-residents), Form 27EQ (TCS). The Q4 annual return is due 31 May.

GST Filings

GSTR-9 — Annual GST Return

Mandatory for taxpayers with aggregate turnover above ₹2 crore. Due 31 December of the following financial year, so for FY 2024-25, the deadline is 31 December 2025.

GSTR-9C — Reconciliation Statement

Required for taxpayers with aggregate turnover above ₹5 crore. It reconciles the GSTR-9 figures against the audited financial statements.

For LLPs And OPCs

LLPs are governed by the LLP Act 2008, not the Companies Act. They file Form 11 (Annual Return, due 30 May) and Form 8 (Statement of Account and Solvency, due 30 October). OPCs file AOC-4 and MGT-7A but are exempt from holding an AGM.

Annual Filing Vs Annual Compliance — The Difference Every Founder Needs To Know

This confusion is responsible for a large portion of compliance penalties in India. Here is the precise distinction:

| Annual Filing | Annual Compliance | |

|---|---|---|

| What It Is | Two specific ROC forms | The entire annual statutory obligation set |

| Governing Law | Companies Act 2013 | Companies Act + Income Tax Act + GST Act + Labour Laws |

| Forms Involved | AOC-4 and MGT-7/7A only | 15 to 20+ filings across all regulators |

| Filed With | MCA portal (mca.gov.in) | MCA, Income Tax portal, GST portal, EPFO, state authorities |

| Consequence Of Missing | ₹100/day/form penalty, strike-off risk | All of the above, plus income tax interest, GST late fees, director disqualification |

A company that files AOC-4 and MGT-7 on time has completed its annual filing. But if it has not filed GSTR-9, has not filed ITR-6, or held its AGM, it is still non-compliant.

This is the trap that catches founders who get a WhatsApp message from their CA in October saying "ROC done" and assume everything is finished. It is not. ROC is one pillar. Three more remain.

Deadlines And Due Dates — The Annual Compliance Calendar

Here is the full annual compliance calendar for a standard private limited company.

| Month | Obligation | Form / Action |

|---|---|---|

| April | TDS deposit for March | Challan 281 by 30 April |

| May | Q4 TDS return (Jan–Mar), LLP Annual Return | Forms 24Q/26Q/27Q by 31 May, LLP Form 11 by 30 May |

| June | Advance tax instalment 1 | 15% of estimated annual tax by 15 June |

| July | Q1 TDS return (Apr–Jun), ITR for non-audit companies | Forms 24Q/26Q by 31 July, ITR-6 by 31 July (non-audit) |

| September | Tax audit completion, Advance tax instalment 2, AGM, DIR-3 KYC | Form 3CA/3CB+3CD by 30 Sep, 45% of tax by 15 Sep, AGM by 30 Sep, DIR-3 KYC by 30 Sep |

| October | ITR for audit companies, AOC-4, LLP Form 8, Q2 TDS return | ITR-6 by 31 Oct, AOC-4 within 30 days of AGM, LLP Form 8 by 30 Oct, 24Q/26Q by 31 Oct |

| November | MGT-7/7A, Advance tax instalment 3 | Within 60 days of AGM (typically 29 Nov), 75% of tax by 15 Dec |

| December | GSTR-9 and GSTR-9C | 31 December |

| January | Q3 TDS return (Oct–Dec) | Forms 24Q/26Q by 31 Jan |

| March | Advance tax instalment 4 | 90% of total tax liability by 15 March |

One critical distinction: TDS deposit and TDS return are two separate obligations. TDS must be deposited by the 7th of the following month for all months except March, deadline is 30 April. TDS returns are filed quarterly. Missing a deposit by even one day attracts interest at 1.5% per month from the date of deduction to the date of deposit under Section 201(1A).

Company annual compliance requirements span the entire financial year. There is no single "compliance month", obligations are distributed from April through December, with a particular cluster in September and October.

Penalties And Consequences For Missing Annual Compliance

The penalties for non-compliance are not symbolic. They are designed to hurt, and they do.

Under The Companies Act 2013

Late AOC-4 or MGT-7: ₹100 per day per form, with no upper cap. A six-month delay on both forms together = ₹36,000 in penalties, before any legal fees. mca.gov.in

Non-holding of AGM: Penalty up to ₹1 lakh on the company plus ₹5,000 per day of continuing default for directors (Section 99).

Board meeting shortfall: Every director in default is liable to a penalty of ₹25,000 (Section 173).

Strike-off: Under Section 248, the ROC can remove a company from the register if it has not filed financial statements or annual returns for two or more consecutive financial years. Strike-off is not a fine, it is the end of the company's legal existence. Reviving a struck-off company requires a separate and expensive application to the National Company Law Tribunal (NCLT).

Director disqualification: Under Section 164(2), a director is automatically disqualified from being a director of any company in India for five years if the company fails to file financial statements or annual returns for three consecutive years. This is not discretionary, it is automatic and sweeping. A Mumbai D2C founder who lets this happen cannot sit on their own board, let alone join any other company's board.

Under The Income Tax Act 1961

Late ITR: Interest at 1% per month on unpaid tax under Section 234A, plus a penalty of up to ₹5,000 under Section 234F (₹1,000 if total income is ₹5 lakh or below).

Late or incorrect TDS return: ₹200 per day under Section 234E, up to the total TDS amount. An additional penalty of ₹10,000 to ₹1 lakh under Section 271H for non-filing beyond one year.

Missing tax audit: 0.5% of turnover or ₹1.5 lakh, whichever is lower, under Section 271B.

Under The GST Act 2017

Late GSTR-9: ₹200 per day (₹100 CGST plus ₹100 SGST), capped at 0.25% of the state turnover.

Beyond The Fines

- Banks check MCA compliance status before sanctioning loans. A struck-off or delinquent company cannot get credit.

- PE investors and acquirers run compliance audits during due diligence. A Delhi consulting firm that skipped three years of ROC filings watched a potential acquisition deal collapse because the buyer would not absorb the liability.

- Government tenders require a current compliance certificate.

Who Is Responsible For Annual Compliance In A Company?

Legal responsibility is not shared equally. Here is how it is allocated.

Directors carry the primary legal burden. Under Section 2(60) of the Companies Act 2013, the "officer in default" includes the managing director, whole-time directors, the manager, and any person whose directions the board habitually follows. Personal penalties fall on these individuals, not just on the company entity.

Company Secretary (CS): Mandatory for companies with paid-up share capital of ₹5 crore or more. The CS is the designated compliance officer for ROC filings and board governance. If your company does not yet require a full-time CS, a practicing company secretary can be engaged for secretarial compliance.

Chartered Accountant (CA): Required for statutory audit (Section 139), tax audit (Section 44AB), and signing the ITR and AOC-4. No company can self-certify its financials, a registered CA firm must be appointed.

CFO or Finance Lead: Operationally responsible for ensuring TDS is deposited on time each month, GST returns are filed, books are closed promptly, and data is ready for the auditor by the dates the CA requires.

Founders of private limited companies cannot opt out of compliance even if the business has no revenue. The legal obligation sits with the directors from the date of incorporation, every year, without exception.

For smaller companies without an in-house finance team, compliance is typically outsourced to a CA firm or a tech-enabled CA-as-a-Service provider like Virtual Accounting, which handles ROC, GST, TDS, and ITR filings under one managed engagement.

Statutory Annual Compliance — A Quick Reference By Entity Type

The term "statutory annual compliance" means obligations created by an Act of Parliament, as opposed to contractual, voluntary, or internal governance actions. Here is how it breaks down across entity types.

| Entity | Governing Law | Key Annual Filings | AGM Required? |

|---|---|---|---|

| Private Limited Company | Companies Act 2013 | AOC-4, MGT-7/7A, ADT-1, ITR-6, GSTR-9 | Yes — by 30 Sep |

| One Person Company (OPC) | Companies Act 2013 | AOC-4, MGT-7A, ITR-6 | No |

| LLP | LLP Act 2008 | Form 8, Form 11, ITR-5 | No |

| Public Limited Company | Companies Act 2013 | AOC-4, MGT-7, ADT-1, ITR-6, GSTR-9 | Yes — by 30 Sep |

| Sole Proprietorship | Income Tax Act + GST Act | ITR-3/ITR-4, GSTR-9 (if applicable) | No |

| Partnership Firm | Income Tax Act | ITR-5, GST returns | No |

Private limited companies face the most complex regime because they are governed by the Companies Act in addition to tax and GST law. This is why most founders searching "what is annual compliance" are specifically asking about Pvt Ltd, the obligations are broader, the penalties are sharper, and the personal liability on directors is real.

For entities with employees, statutory compliance extends further: Provident Fund (PF) annual returns, ESIC half-yearly returns, and Professional Tax annual returns (the latter varies by state, Maharashtra, Karnataka, and West Bengal all have different PT structures and deadlines). epfindia.gov.in

How To Actually Get Annual Compliance Done — A Step-By-Step Process

Here is the practical sequence for a private limited company, in order.

- Close The Books By 30 April. Every transaction for the year ended 31 March must be recorded. Bank accounts reconciled. Receivables and payables confirmed. The later you start, the harder everything downstream becomes.

- Appoint Or Confirm Your Statutory Auditor. The auditor must be a registered CA firm. Share the finalized books, ledgers, and supporting documents. The statutory audit must be completed before the AGM.

- Complete The Tax Audit By 30 September (if turnover exceeds ₹1 crore). Your CA files Form 3CA or 3CB plus Form 3CD on the Income Tax portal.

- Prepare Financial Statements In Schedule III Format. Balance sheet, profit and loss account, cash flow statement, and notes to accounts, all in the format prescribed by the Companies Act 2013.

- Board Approves Financial Statements And Directors' Report. A board resolution is passed under Section 134. The Directors' Report must cover state of affairs, any dividend recommendation, material changes since year-end, and the Directors' Responsibility Statement.

- File ITR-6 by 31 July (non-audit) or 31 October (audit cases). Filed by your CA on the Income Tax portal.

- Hold The AGM By 30 September. Shareholders formally adopt the financial statements, reappoint the auditor, and transact any other agenda items. If you need an extension, file Form GNL-1 with the ROC before the deadline, not after.

- File AOC-4 within 30 days of the AGM on the MCA portal. Attach financials, board report, and audit report.

- File MGT-7 Or MGT-7A within 60 days of the AGM. Contains shareholding pattern, director details, and company indebtedness as of the AGM date.

- File GSTR-9 (And GSTR-9C If Applicable) by 31 December on the GST portal.

- Confirm All Four Quarterly TDS Returns Are Filed: Q1 by 31 July, Q2 by 31 October, Q3 by 31 January, Q4 by 31 May.

- File PF And ESIC Annual Returns if you have employees on payroll.

That is the full cycle. It requires coordinated effort between your internal finance function, your CA, and, for larger companies, a company secretary. Starting late on any step compresses the timeline for every step that follows.

Common Mistakes Founders Make With Annual Compliance

1. Assuming A Zero-Revenue Company Has Nothing To File.

Wrong. Dormant companies must file AOC-4, MGT-7, and ITR-6 every year. Nil returns are still returns. The ₹100 per day penalty clock starts the day after the deadline, with zero regard for whether the company earned a rupee. beaconfiling.com

2. Treating "Annual Filing" And "Annual Compliance" As The Same Thing.

As covered above, completing ROC forms is not the finish line. If ITR-6 is unfiled or GSTR-9 is missed, the company is still non-compliant regardless of what the MCA portal shows.

3. Missing The AGM Deadline.

Many founders focus on the ROC form deadlines and miss the fact that the AGM itself must be held by 30 September. Without a valid AGM, the financial statements are not legally adopted, which means AOC-4 cannot be properly filed. The cascade compounds fast.

4. Forgetting GSTR-9 Entirely.

Founders who manage monthly GSTR-1 and GSTR-3B diligently often forget the annual reconciliation return exists. It has its own deadline, 31 December, its own format, and its own penalties. It is not auto-generated from your monthly returns.

5. Treating TDS As A Year-End Task.

TDS is a monthly deposit obligation. A missed TDS deposit in May attracts interest at 1.5% per month from the date of deduction to the date of deposit, and this accumulates silently until the CA catches it at year-end, by which point the interest amount can be significant.

6. Underestimating Director Personal Liability.

Company penalties are one thing. But Section 164(2) disqualification, which bars a director from every board in India for five years, is another level entirely. Founders who incorporate companies and then go quiet on compliance for three years risk losing their ability to be a director anywhere. This is career-ending, not just financially painful.

7. Starting Too Late.

Annual compliance is not a November problem. It is a year-round calendar. Founders who start the book-closing process in August for a March year-end create a bottleneck that generates errors, delayed AGMs, and late filings. The process should begin in April.

Need help staying on top of annual compliance? Virtual Accounting handles ROC, GST, TDS, and ITR for private limited companies — starting from ₹4,000 per month. See the full service breakdown here.

FAQ

What Is Annual Compliance For A Company In India?

Annual compliance is the complete set of mandatory filings and procedural obligations every registered company must complete each financial year under the Companies Act 2013, Income Tax Act 1961, GST Act, and applicable labour laws. It includes ROC filings like AOC-4 and MGT-7, income tax returns like ITR-6, GST annual return like GSTR-9, tax audit where applicable, the AGM, and required board meetings, irrespective of revenue.

What Is The Difference Between Annual Filing And Annual Compliance?

Annual filing refers specifically to two ROC forms, AOC-4 and MGT-7 or MGT-7A, on the MCA portal under the Companies Act. Annual compliance is the broader umbrella across ROC, income tax, GST, TDS, and labour law obligations. You can finish annual filing and still be non-compliant if ITR-6, GSTR-9, tax audit, or other statutory steps remain.

What Is The Penalty For Late Annual Compliance Filing?

For ROC, late AOC-4 or MGT-7 attracts ₹100 per day per form with no cap. For income tax, late ITR triggers 1% per month interest under Section 234A plus a penalty up to ₹5,000 under Section 234F. For GST, late GSTR-9 is ₹200 per day, capped at 0.25% of state turnover. Additional penalties apply for delayed TDS returns and missed tax audits.

Is Annual Compliance Required Even If The Company Has No Business Activity?

Yes. Nil business does not mean nil obligations. Dormant or zero-revenue companies must still file AOC-4, MGT-7 or MGT-7A, ITR-6, maintain board governance, and meet any GST or TDS duties that apply. If you prefer a managed solution, Virtual Accounting by AI Accountant can handle nil and standard filings end-to-end so deadlines are not missed.

What Forms Are Required For Annual Compliance Of A Private Limited Company?

At minimum: AOC-4 for financial statements, MGT-7 or MGT-7A for the annual return, ADT-1 for auditor appointment, ITR-6 for income tax, GSTR-9 if turnover exceeds ₹2 crore, quarterly TDS returns like 24Q and 26Q, and DIR-3 KYC for every director.

When Is The AGM Deadline For A Pvt Ltd Company?

The AGM must be held within six months of the financial year end, typically by 30 September for entities following the April to March year. The first AGM after incorporation can be held within nine months of the financial year end.

Can A Director Be Personally Penalised For Company Non-Compliance?

Yes. Directors are officers in default under Section 2(60) of the Companies Act. Penalties for missing AGMs, board meeting gaps, and other defaults are levied on individuals. Repeated ROC non-filing can trigger automatic five-year disqualification from all Indian directorships under Section 164(2).

What Is The Due Date For GSTR-9 Annual Return?

GSTR-9 is due on 31 December of the year following the financial year, for example 31 December 2025 for FY 2024-25. GSTR-9C, the reconciliation statement for turnover above ₹5 crore, is due the same day.

What Is The Difference Between Statutory Annual Compliance And General Compliance?

Statutory annual compliance consists of obligations created by legislation, such as the Companies Act, Income Tax Act, and GST Act. General compliance can include internal policies, contractual obligations, or voluntary governance. Statutory duties are non-negotiable and attract legal penalties if missed.

How Much Does Annual Compliance Cost For A Pvt Ltd Company?

Government ROC filing fees are typically ₹200 to ₹500 depending on share capital. Professional fees vary by turnover, audit scope, and complexity. If you lack an in-house finance team, Virtual Accounting by AI Accountant offers bundled managed compliance for ROC, GST, TDS, and ITR, providing predictable monthly pricing and a single point of accountability.