Key takeaways

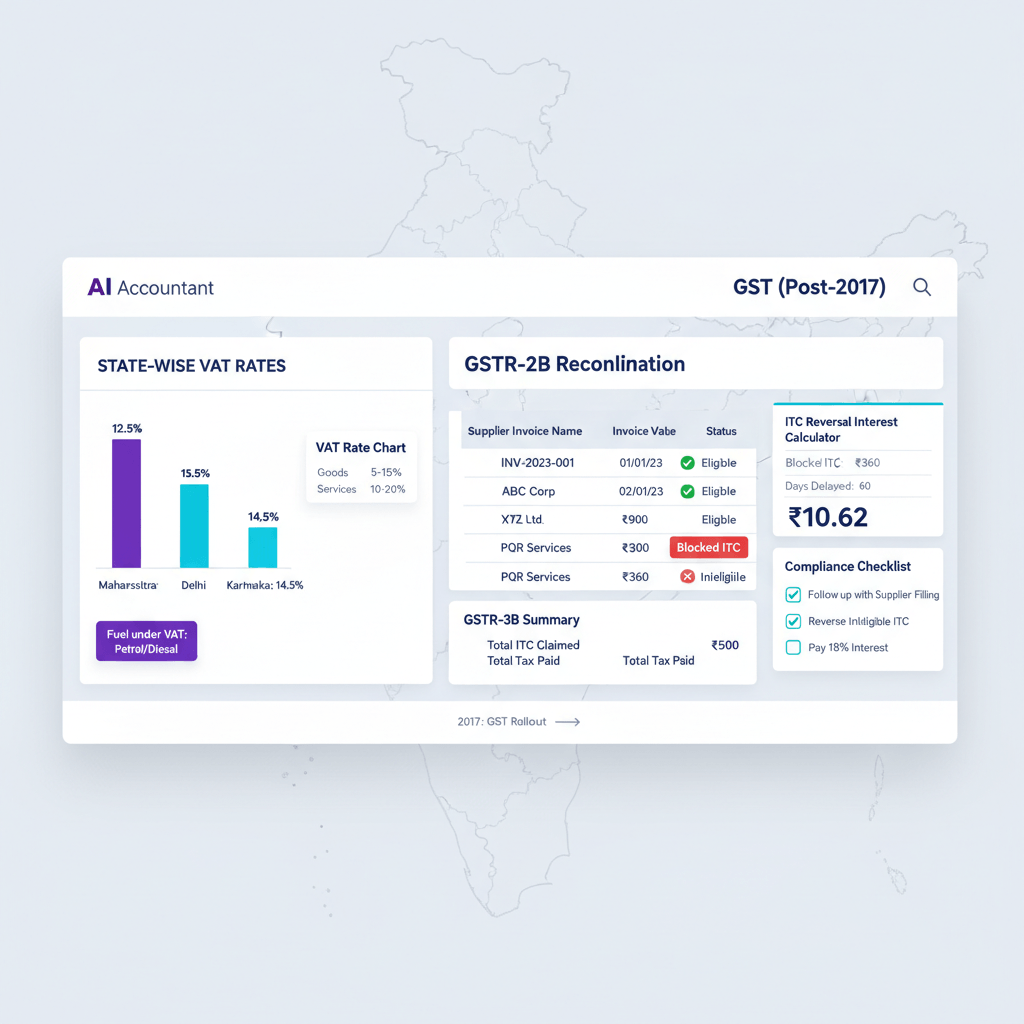

- GST replaced VAT nationwide from July 1, 2017. The Constitution 101st Amendment Act enabled GST implementation across India, subsuming state VAT, central excise, service tax, and many other indirect taxes into one regime. Petroleum products and alcoholic liquor for human consumption remain outside GST, continuing under state VAT or excise.

- ITC mechanism fundamentally differs between VAT and GST. VAT allowed self-declared credit summaries in returns, GST requires invoice-level matching through GSTR-2B, which reflects only those invoices where suppliers filed GSTR-1. Provisional credit withdrawal means businesses can claim ITC only to the extent visible in GSTR-2B, as reinforced by CBIC circulars.

- Non-filing suppliers cost businesses 18% annual interest on blocked ITC. Section 50 of the CGST Act mandates 18% interest per annum on ITC claimed but later reversed due to supplier non-filing, calculated from the date of availment. Even a few months of delay can add meaningful interest charges and cash strain.

- E-invoicing thresholds dropped to ₹5 crore turnover from August 1, 2023. Notification 10/2023 requires invoice reference numbers via the IRP for businesses above ₹5 crore, and e-invoiced transactions auto-populate into GSTR-2B, reducing mismatches. You can validate and operationalize IRN with this guide on IRN.

- State VAT continues on fuel purchases with zero ITC offset. Diesel and petrol carry state VAT that becomes a pure cost, since no GST credit applies. High fuel consumption directly compresses margins due to non-creditable VAT.

VAT vs GST in India, the short answer

India transitioned from state-level VAT to nationwide GST on July 1, 2017, unifying taxes on goods and services. The headline change for finance teams is control of Input Tax Credit, which shifted from self-declaration under VAT to supplier-dependent matching under GST, via static monthly GSTR-2B.

| Aspect | VAT era | GST era |

|---|---|---|

| Scope | Goods only, state-by-state | Goods and services under a dual system |

| Tax structure | State VAT | CGST + SGST for intra-state, IGST for inter-state |

| Input credit | Self-declared summaries | Invoice matching through GSTR-2B |

| Credit timing | Claimed on purchase | Claimed only when supplier files GSTR-1 and it appears in 2B |

| Current applicability | Fuel and liquor | All other goods and services |

| Reconciliation | Periodic with state | Monthly, by the 14th for 2B |

| Interest on wrong ITC | State-specific | 18% per annum under Section 50 |

| E-invoicing | Not applicable | Mandatory above ₹5 crore turnover |

The operational reality: under VAT you controlled credit claims via your returns, under GST your credit exists only when suppliers file GSTR-1 and the invoice lands in your GSTR-2B.

Where VAT still applies after GST, fuel and alcohol, and why it hurts margins

Petroleum products, namely crude oil, high-speed diesel, petrol, natural gas, and aviation turbine fuel, plus alcoholic liquor for human consumption, remain outside GST. States levy VAT or excise on these, which is not creditable against GST. That VAT becomes a straight cost, lowering EBITDA for logistics heavy and hospitality businesses.

Petroleum products under state VAT

Diesel and petrol attract state VAT, typically 20% to 31% depending on the state. Because GST does not allow ITC on these, every rupee of VAT on fuel inflates operating costs. A logistics company consuming ₹10 lakh diesel a month that faces 30% VAT absorbs ₹3 lakh as a direct, non-creditable expense, which flows straight into the per-kilometer cost base.

Alcoholic beverages under state excise

Liquor remains under state control, with excise plus VAT or additional excise levies. Hotels and restaurants cannot take GST credit on these taxes, so bar programs carry lower margins than kitchen operations where GST credits reduce cost of goods sold.

International VAT for Indian businesses

Foreign VAT, for example 5% in UAE or 20% in the UK, is outside India’s GST system. Unless you are eligible and registered locally for refunds, overseas VAT becomes part of procurement cost, not an input credit in India. Refund portals exist for some regimes, however claim complexity and documentation often delay recovery.

How GSTR-2B blocks your ITC until suppliers comply

GSTR-2B is a static statement generated monthly, it captures supplier-reported invoices from their GSTR-1. If a supplier misses or delays GSTR-1, your ITC does not appear in 2B, and you should not claim it. This single dependency drives most cash flow surprises that CAs see during monthly closes.

Generation cadence and visibility

- Monthly filers: Supplier GSTR-1 due by the 11th, your GSTR-2B generates on the 14th.

- QRMP dealers: IFF by the 13th, 2B generates mid-month on a bi-monthly cadence for recipients.

- Invoices not in 2B are ineligible for that month, claim only when they appear later, within Section 16(4) deadlines.

Rule 36(4) withdrawal

Provisional ITC above what appears in 2B is no longer allowed. If you claimed based on purchase invoices but the entries were absent in 2B, you must reverse the excess, and pay 18% interest from the date you availed the credit until the date of reversal.

Matching keys and common pitfalls

- Exact GSTIN, invoice number, date, taxable value must match, even minor mismatches can block your credit.

- HSN reporting thresholds vary by turnover, incorrect HSNs create downstream notices and reconciliation breaks.

- E-invoicing with valid IRN reduces errors and speeds 2B visibility.

Pro tip: automate nudges to non-compliant suppliers by tracking 2B gaps daily. Finance teams using an “AI Accountant” style workflow that monitors 2B deltas cut blocked ITC by double digits within two cycles.

The hidden costs, interest, penalties, and cash flow squeeze

Blocked ITC forces cash payments for GST that should have been credit, and interest at 18% applies if you claimed early and reversed later. Late fees, e-invoice lapses, and e-way bill issues add up, turning compliance gaps into material P&L hits.

Interest math that surprises teams

Claiming ₹10 lakh of ITC that shows up two months later could cost five figures in interest if you claimed early and then reversed, only to re-avail later. Interest runs from date of availment to reversal, not from the notice date. The safest path is to claim only what appears in 2B.

Working capital impact

If 25% of supplier invoices fail to hit 2B in the same month, businesses commonly see ₹20–50 lakh stuck monthly. That means higher cash payments for 3B, overdraft usage, and lower free cash flow. Compounded over 12 months, the finance cost alone can rival a mid-level hire.

Bottom line: an “AI Accountant” implementation that accelerates supplier follow-ups, validates IRNs, and reconciles 2B daily typically releases working capital equivalent to 1–2% of annual turnover, while reducing 18% interest exposure.

Operational changes, from VAT summaries to daily GST tracking

GST demands transaction-level hygiene. Invoice capture must be weekly, vendor masters need strict GSTIN validation, e-invoice IRN checks are essential for eligible vendors, and purchase registers must align to 2B by the 14th. This is a process shift, not just a return-filing change.

Weekly AP capture with master data discipline

- Validate supplier GSTINs and registration status before onboarding.

- Check IRN where applicable, and ensure place of supply logic lines up with your registration state.

- Mark non-creditable spends, for example fuel, employee cards, foreign VAT, at entry time to avoid wrongful ITC claims.

The 7th-of-month close playbook

- Days 1–5: Post all bills, code bank and card statements, tag RCM categories like GTA.

- Day 6: Lock purchase register, draft GSTR-3B, prepare vendor gap list.

- Day 7: Send chasers to suppliers for GSTR-1, confirm e-way bill and goods received notes, and freeze the books for the month.

An “AI Accountant” can automate vendor chasers post-day 6, align invoice keys, and forecast 2B visibility, reducing last-mile manual checks.

Long-term business impact and valuation effects

Blocked ITC and higher compliance loads compress margins, increase the cost of capital, and create diligence risks during fundraising or bank renewals. Investors increasingly haircut EBITDA for GST process risk.

EBITDA compression

A steady 15–25% mismatch rate on monthly ITC can shave 1.5–2 percentage points of EBITDA for mid-market firms. Over a multi-year horizon, the valuation impact at standard multiples is significant, especially for capital-light businesses.

Compliance cost step-up

Compared to VAT, GST-era costs include additional headcount, software, advisory retainers, and notice handling. Well-designed automation pays back through recovered ITC, lower interest, and fewer notices within two to three quarters.

FAQ

From a CA perspective, what exactly changed for credit claims when India moved from VAT to GST in 2017?

Under VAT, clients self-declared input credits in state returns, and credits were largely controllable internally. Under GST, credits are contingent on supplier GSTR-1, and eligibility is restricted to what appears in your monthly GSTR-2B. If an invoice is missing in 2B, the ITC is ineligible for that period, claimable later only when it appears, subject to Section 16(4) time limits. An “AI Accountant” reconciles purchase registers to 2B and suppresses premature claims, avoiding interest at 18%.

How should I advise a logistics client with ₹2–5 lakh monthly diesel spends on tax treatment?

Diesel, petrol, and other petroleum products remain outside GST, so state VAT on fuel is not creditable. Book VAT as a direct expense in “Fuel and Power,” do not attempt GST set-off. Recommend route-level margin monitoring, since fuel VAT often adds 20–30% to per-kilometer cost. An “AI Accountant” can auto-flag fuel spends for non-ITC treatment at ledger level.

My client’s suppliers file GSTR-1 late, 2B shows short ITC, what is the compliant approach for 3B?

Claim only the ITC visible in 2B for that period, reverse any excess previously availed, and pay 18% interest from the date of availment to reversal per Section 50. When invoices appear in a later 2B, re-avail within Section 16(4) deadlines. Configure automated supplier nudges via an “AI Accountant” to push filing before the 11th so that 2B captures the invoices by the 14th.

Is provisional ITC still allowed if supplier delays are consistent but genuine?

No, provisional ITC above 2B is withdrawn. CAs should strongly discourage any provisional claims. Establish a monthly cut-off on the 7th for AP, then base 3B credits strictly on the 2B generated on the 14th. Automation that predicts 2B visibility based on historical supplier behavior helps planning but does not justify claiming before visibility.

What is the clean method to compute interest for an ineligible ITC reversed in a later month?

Compute interest at 18% per annum on the ineligible amount from the date of availment or utilization, whichever is applicable, until the date of reversal or payment. For example, excess ITC of ₹2 lakh availed on April 20 and reversed on July 20 accrues interest roughly for 91 days, about ₹8,959. Use journals to document reversals, and attach a working for audit trails. An “AI Accountant” can auto-calc interest based on booking and reversal dates.

How do e-invoicing and IRN reduce 2B mismatches for clients above ₹5 crore?

E-invoicing mandates supplier IRN generation through the IRP. IRN validated invoices flow more reliably into 2B, reducing manual errors in GSTIN, invoice numbers, and dates. Set your AP workflow to verify IRN at ingestion, reject invoices without valid IRN where required, and chase suppliers immediately. “AI Accountant” style checks can gate invoices without IRN from accounting.

Can clients claim ITC once an invoice appears in 2B well after the supply date, any outer limit I should watch?

Yes, but only up to the statutory deadline under Section 16(4), which is November 30 following the end of the financial year of the invoice, or the annual return due date, whichever is earlier. After that, credits lapse permanently. Advise clients to reconcile by the 14th monthly and run a quarterly aging of invoices missing in 2B to avoid forfeiture.

How should I treat foreign VAT for clients with UK or UAE transactions, and does it integrate with Indian GST?

Foreign VAT cannot be set off against Indian GST. If your client is unregistered locally, VAT becomes a cost. Where eligible, file refunds with the respective authority portals and maintain robust documentation. In parallel, ensure those invoices are marked as non-ITC at booking, something an “AI Accountant” can enforce through vendor and category rules.

Is there any scenario where late fees or penalties can be waived if we self-correct before notice?

Late fees are statutory and generally apply until filing, but penalties under Section 74 can reduce significantly for voluntary corrections before a notice. Interest under Section 50 is not waived by voluntary action, it still runs from availment to reversal. Document the self-correction timeline to support reduced penalty positions in assessments.

We use Tally, what is the minimal monthly close workflow to minimize reversals?

Process invoices weekly, lock purchases on the 6th or 7th, draft 3B, and issue supplier chasers. Import 2B on the 14th, reconcile, and post JVs to reverse non-2B credits. File 3B by the 20th with only 2B-visible ITC. Add an “AI Accountant” layer to auto-import 2B, compare line-by-line, and generate vendor chasers with invoice specifics.

How do I present GST risk in board packs for valuation or fundraising conversations?

Report a 12–24 month trend of 2B match rate, average blocked ITC, interest paid on reversals, and late fees. Show the remediation plan, for example IRN gating, supplier SLAs, and automation rollouts. Quantify EBITDA uplift from unlocking ITC and lowering interest. Tools like an “AI Accountant” can produce dashboards tying blocked ITC to vendors, categories, and geographies, which investors appreciate.

Can we still utilize old VAT credits that never transitioned through TRAN-1 or TRAN-2?

Transitional credits were allowed via TRAN forms, with deadlines long closed except for limited court-permitted cases. Un-transitioned VAT credit is generally considered lapsed. Unless your client has a specific judicial window, do not count on recovery. Focus instead on tightening current 2B processes to prevent new leakages.

For clients with frequent fuel and liquor purchases, how do I prevent accidental ITC claims?

Create non-ITC ledgers for fuel and alcohol spends, and enforce posting rules in your accounting system. Use an “AI Accountant” to auto-classify fuel or bar purchase entries from bank feeds and invoice keywords, setting a hard stop on ITC tagging. This prevents reversals and the associated 18% interest exposure up front.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.