-01%201.svg)

Key takeaways

- Billing triggers cash collection and GST, revenue recognition is earned over time under Ind AS 115, especially for stand-ready consulting retainers.

- Straight-line recognition usually fits ongoing advisory retainers, input or output methods apply only when effort or delivery is clearly uneven.

- Use Deferred Revenue for advance billings, use Unbilled Accounts Receivable for arrears billings, keep ledgers reconciled monthly.

- Always present revenue gross, TDS is an asset, not a reduction of revenue, TDS is an asset.

- Variable consideration, bonuses and penalties, should be included only when highly probable not to reverse, stay conservative to avoid GST credit note churn.

- India-first controls matter, GST place of supply, TDS sections, e-invoicing, LUT for exports, and FEMA realization timelines must be embedded in process.

- Clean documentation, consistent schedules, and automation across CRM, delivery, and finance prevent revenue leakage and audit surprises.

Understanding Monthly Retainers vs Project-Based Work

The core difference in revenue recognition

Project work has concrete deliverables and milestone-driven recognition. Monthly retainers promise access and capacity, the client pays a fixed fee for continuous advisory, execution support, and stand-ready obligations. Under Ind AS 115, this usually leads to evenly recognising revenue over the month, even if you invoice on Day 1.

Why billing and revenue are different animals

Billing triggers cash, GST, and sometimes TDS. Revenue recognition asks what you promised, whether it is satisfied over time, and how you measure progress. That is why ₹3,00,000 invoiced on the 1st, may become revenue evenly over the month, not immediately.

The India-specific complexity layer

Indian agency finance teams juggle GST place of supply, TDS deductions under Sections 194J and 194C, export LUT and FIRC, and foreign exchange. Mis-timed recognition distorts MRR and margins, which hurts investor diligence and bank underwriting.

Billing is about collection and compliance, revenue recognition is about earning and economics.

The Ind AS 115 Framework for Monthly Retainer Accounting

Step 1: Identifying performance obligations

Most consulting retainers are a bundled, integrated service, advisory plus execution plus reporting, treated as a single performance obligation satisfied over time. Split only if distinct, separately priced, and independently useful components exist in the contract.

Step 2: Over time vs point in time

Retainers typically qualify for over-time recognition, paragraph 35(a), because clients receive and consume benefits as you perform. Discrete one-off deliverables, like a standalone strategy deck, may be recognised at a point in time when delivered.

Step 3: Measuring progress

- Straight-line time-based for always-on advisory and stand-ready obligations.

- Input methods when robust timesheets and cost tracking exist.

- Output methods for SLA-bound deliverables with measurable outputs.

For practical agency operations, straight-line is the default unless effort is demonstrably skewed.

Handling variable consideration

Estimate bonuses, penalties, and usage-based top-ups using expected value, or most likely amount, include only amounts that are highly probable not to reverse. Conservative treatment avoids GST credit note churn later.

The Step-by-Step Framework for Monthly Retainer Accounting

Contract intake and documentation

Capture scope, stand-ready obligations, term and flexibility, pricing, billing cadence, GST and TDS applicability. This is the backbone for defensible schedules and smooth audits.

Creating revenue recognition schedules

- Standard advisory: Straight-line monthly recognition, independent of invoicing timing.

- Deliverable-heavy: Weight recognition to planned delivery if outputs are clearly front-loaded.

- Time-and-materials within cap: Recognise based on tracked hours up to the cap.

Document method selection and assumptions. Auditors expect rationale tied to contract substance.

Invoicing cadence vs revenue timing

- Advance billing: Invoice hits AR and GST, fee sits in Deferred Revenue until earned.

- Arrears billing: Recognise through the month, park the balance in Unbilled AR until you invoice.

Setting up Deferred Revenue and Unbilled AR

- P&L accounts: Retainer Revenue by service line is helpful.

- Balance sheet: Deferred Revenue, Unbilled AR, AR.

- Tax: TDS receivable by section, Output GST payable buckets.

Reconcile monthly, these ledgers bridge billing engines and recognition rules.

The month-end close flow

- Pull active retainer list, including starts, pauses, and terminations.

- Gather delivery evidence, timesheets, reports, client approvals.

- Approve recognition amounts per schedules and evidence.

- Post journals, Deferred Revenue to Revenue or Revenue to Unbilled AR.

- Reconcile AR, cash receipts, deferred and unbilled roll-forwards.

- Refresh MRR, margin, and DSO dashboards.

Documentation for audit readiness

Maintain MSAs and SOWs, change orders, delivery evidence, recognition schedules, and decision trails. This proves system over guesswork.

Journal Entries and Practical Examples for Indian Firms

Scenario 1: Advance billing retainer, domestic client

Invoice on the 1st, Dr AR ₹3,54,000, Cr Deferred Revenue ₹3,00,000, Cr Output GST ₹54,000. Recognise evenly, Dr Deferred Revenue ₹3,00,000, Cr Retainer Revenue ₹3,00,000.

Client deducts TDS at 10 percent on fee, receipt entry is Dr Bank ₹3,24,000, Dr TDS Receivable ₹30,000, Cr AR ₹3,54,000. Important, TDS is an asset, revenue remains gross.

Scenario 2: Arrears billing retainer

Monthly recognition, Dr Unbilled AR ₹3,00,000, Cr Revenue ₹3,00,000. Next month’s invoice, Dr AR ₹3,54,000, Cr Unbilled AR ₹3,00,000, Cr Output GST ₹54,000.

Scenario 3: Export retainer, foreign client

Zero-rated under LUT, book in INR at recognition date rate, track FX difference. Recognise Dr Unbilled AR ₹3,32,000, Cr Revenue ₹3,32,000, invoice with no GST, collect and record FX gain or loss based on settlement rate. Keep FIRC or BRC for FEMA and GST proofs.

Special Scenarios in Retainer Revenue Recognition

Mid-month starts and partial periods

Pro-rate by days for clean straight-line recognition, or recognise full month if the contract allows and setup effort is front-loaded. Document the choice.

Pauses and terminations

Stop recognition from the effective date, refund unearned amounts from Deferred Revenue, issue GST credit notes promptly.

Contract modifications and scope changes

If additions are distinct and priced at standalone selling price, treat as a separate contract. Otherwise, modify the existing transaction price and recognise prospectively over the remaining term.

Performance bonuses and penalties

Include only when highly probable not to reverse. Many firms book base retainers monthly, recognise success fees when KPIs are confirmed, this avoids GST reversals.

Free add-ons and over-servicing

Non-distinct extras remain within advisory value, monitor margin dilution and renegotiate at renewal. Distinct free services should be documented to position paid scopes later.

Managing refunds and chargebacks

Use Sales Returns for revenue reversal, issue credit notes for GST reduction, and align with GST returns.

Building Your Agency Revenue Operations Infrastructure

Sales to delivery to finance handoffs

Standardize CRM fields for start or end dates, billing cadence, GST or TDS flags, SLAs. Delivery validates scope, finance sets ledgers and schedules from day one, run weekly syncs to catch scope changes and risks.

Internal controls and approval hierarchies

Define contract approval matrices, deliverable acceptance protocols, time tracking discipline, and monthly recognition approvals with escalation paths.

Key metrics to track

- MRR and ARR by client and service line.

- Realization and effective hourly rates, and utilization.

- Gross margin by client, DSO trends, deferred and unbilled aging.

- Churn, expansion revenue, and CLV.

Preventing revenue leakage

Control scope creep, reconcile CRM contracts versus invoices monthly, accelerate collections on early warning signs, and reprice at renewal using effort data.

Systems and Technology for Modern Retainer Management

Configuring Tally and Zoho Books

Create ledgers for Retainer Revenue, Deferred Revenue, Unbilled AR, TDS receivable by section, and Output GST. Track by client using cost centres or projects. Set up Recurring invoices with correct GST treatment and payment terms.

Building revenue schedules and automation

- Maintain schedules in spreadsheets and import monthly.

- Use Tally or Zoho recurring journals, recurring journal entries simplify recognition.

- Adopt PSA tools that natively manage revenue recognition if complexity grows.

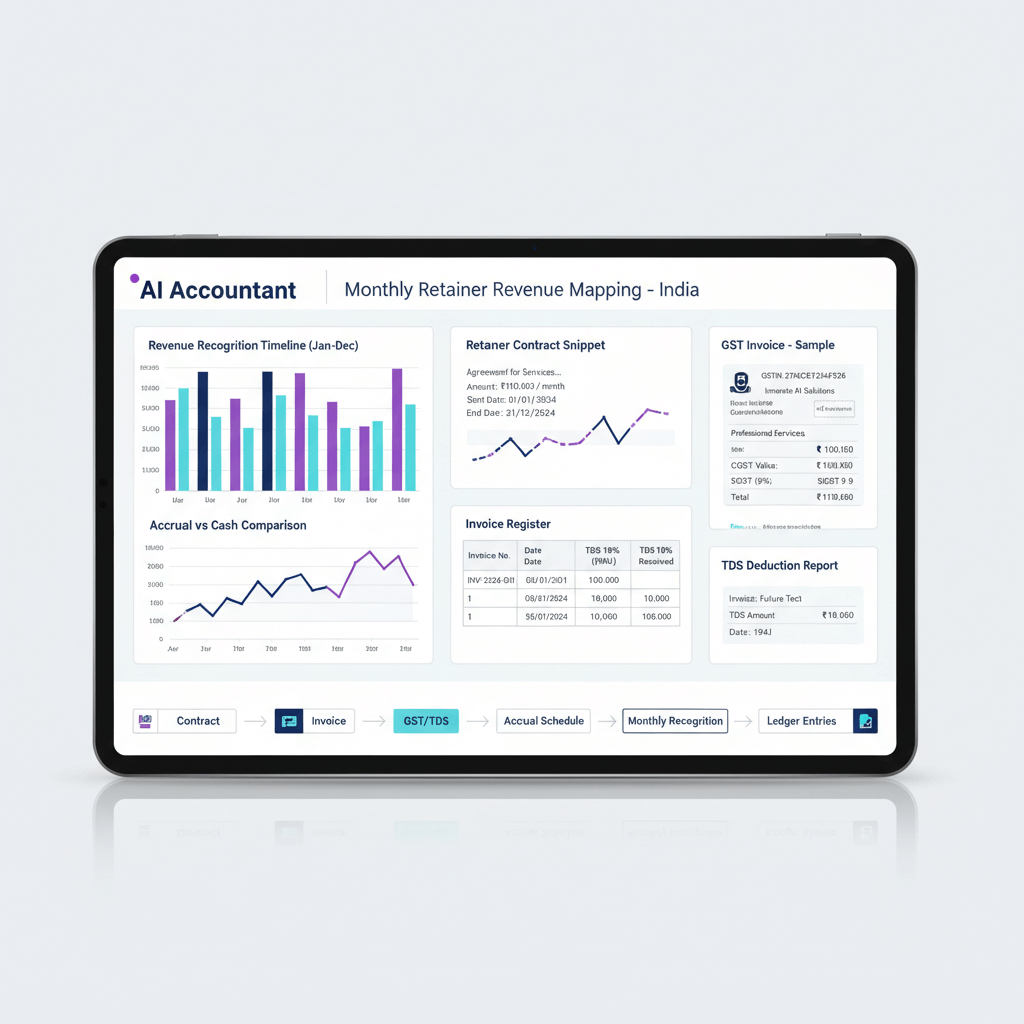

Leveraging AI-powered financial automation

AI Accountant ingests bank statements and invoices automatically, predicts ledger mappings from transaction patterns, and syncs with Tally and Zoho Books. It surfaces receivable aging, deferred revenue roll-forwards, and cash trends without manual spreadsheet maintenance.

Evaluate other tools based on fit and integration, QuickBooks, Xero, FreshBooks, Wave, Sage Intacct.

Data flow and integration points

Map end-to-end, contract signed to CRM entry to finance setup, services delivered to month-end recognition and dashboard refresh, invoice to collection to bank reconciliation and TDS tracking. Automate or checklist each handoff.

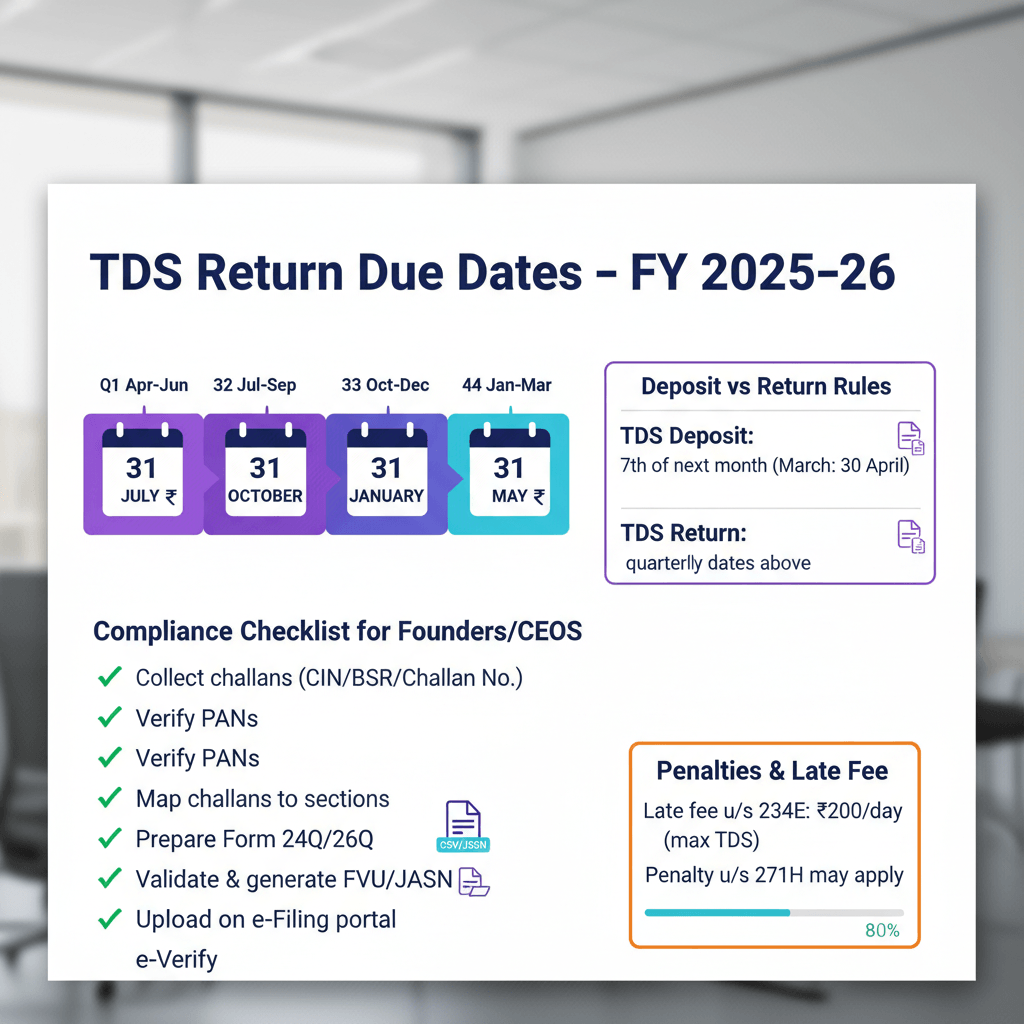

India-Specific Compliance Checklist

GST compliance for service retainers

- Place of supply, recipient location for domestic services, outside India for exports.

- Time of supply, ensure billing cadence aligns to avoid interest and penalties.

- E-invoicing above ₹5 crore turnover, generate IRNs consistently.

- Export documentation for zero-rated supplies, LUT or bond, foreign currency invoices, FIRC or BRC, report correctly in GSTR-1 and GSTR-3B.

TDS management

Identify the correct section, most retainers fall under Section 194J for professional or technical services, reconcile with Form 26AS or AIS quarterly, chase missing TDS with a defined protocol, and collect Form 16A on time.

FEMA and foreign exchange

Realize export proceeds within the permitted window, retain contracts, invoices, and bank advice, book revenue at spot rates on recognition, record FX gains or losses at settlement.

Document retention requirements

Keep contracts, operational evidence, financial records, compliance filings, and recognition schedules for at least eight years, as per Companies Act.

Month-End Close Checklist for Retainer Revenue

- Pull active retainers, starts, terminations, and pauses.

- Confirm delivery evidence and stand-ready obligations met.

- Update variable consideration estimates.

- Post monthly recognition entries per schedule.

- Reconcile deferred and unbilled roll-forwards.

- Match AR to outstanding invoices, tie to bank receipts.

- Verify TDS receivable balances and update aging.

- Reconcile GST liability accounts with returns.

- Update collections tracker, follow up overdue.

- Refresh MRR, gross margin, and DSO dashboards.

- Prepare variance analysis against budget and forecast.

- Document method changes or unusual items, share insights with leadership.

Common Pitfalls and How to Avoid Them

Pitfall 1: Recognising invoice amount as revenue

Fix by tying recognition to performance obligations and satisfaction pattern, not billing events.

Pitfall 2: Ignoring stand-ready obligations

Advisory retainers are satisfied over time, straight-line recognition applies unless effort is uneven.

Pitfall 3: Casual treatment of variable consideration

Adopt conservative inclusion thresholds, promptly recognise penalties and issue credit notes.

Pitfall 4: Weak documentation

Use templates for change orders and approvals, preserve decision trails.

Pitfall 5: Not grossing up revenue for TDS

Always show gross, record TDS as an asset, reconcile Form 26AS.

Pitfall 6: Poor CRM-to-finance coordination

Mandate CRM fields, automate alerts for new contracts, run regular sales-finance syncs.

Practical Templates and Tools

Revenue recognition decision tree

- Is service satisfied over time, client receives and consumes benefits as delivered, then yes, proceed.

- Select progress measure, straight-line for consistent effort, input for reliable hours, output for clear deliverables.

Contract review checklist

Cover client and contract details, service description, stand-ready obligations, term, renewal and termination, fee structure and payment terms, variable consideration, billing schedule, GST or TDS applicability, recommended recognition method, and approval sign-offs.

Revenue schedule spreadsheet structure

- Client, contract ID, start, end, method.

- Monthly fee, GST rate or amount, TDS section or amount.

- Recognised this month, cumulative recognised, deferred or unbilled balance.

- Notes and assumptions.

Journal entry quick reference

Advance billing, invoice Dr AR, Cr Deferred Revenue and GST, recognise Dr Deferred Revenue, Cr Revenue, collect Dr Bank and TDS receivable, Cr AR.

Arrears billing, recognise Dr Unbilled AR, Cr Revenue, invoice Dr AR, Cr Unbilled AR and GST, collect Dr Bank and TDS receivable, Cr AR.

Export, recognise Dr Unbilled AR, Cr Revenue, invoice Dr AR, Cr Unbilled AR, collect Dr Bank, Cr AR and record FX gain or loss.

Making Revenue Recognition Your Competitive Advantage

Accurate recognition clarifies MRR and true margins, highlights profitable clients, and surfaces leakage early. It builds credibility with auditors, investors, and lenders, and it frees your finance team from firefighting to focus on analytics, pricing, and growth.

Start with contract documentation and disciplined schedules, then add automation as you scale. AI Accountant and similar platforms amplify good processes, they do not replace them. Train teams on the billing versus revenue distinction, close monthly with reconciliations, and turn compliance into strategic clarity.

FAQ

How should a CA decide between straight-line and input method for a monthly consulting retainer under Ind AS 115?

Choose straight-line when the service is stand-ready and value delivery is uniform during the month. Use input method only if your client has robust, auditable time or cost tracking that shows uneven effort, for example, detailed timesheets tied to cost centres. Many firms implement straight-line first, then validate exceptions through monthly variance analysis, assisted by AI Accountant timesheet reconciliations.

How do I present TDS in books for retainers, and does TDS reduce revenue?

TDS never reduces revenue. Book revenue gross, record TDS as an asset, TDS Receivable, and reconcile with Form 26AS or AIS each quarter. At collection, post Bank and TDS Receivable against AR. This treatment preserves turnover metrics and aligns with audit expectations.

What journals do I pass for advance billing versus arrears billing, and how do I avoid month-end surprises?

Advance billing, AR and Output GST on invoice day, fee to Deferred Revenue, revenue recognised during the month by Dr Deferred Revenue and Cr Revenue. Arrears billing, recognise revenue with Dr Unbilled AR and Cr Revenue, convert to AR on invoicing with Output GST. Avoid surprises by maintaining a monthly roll-forward of Deferred Revenue and Unbilled AR, automated via AI Accountant.

How do I treat performance bonuses and penalties in retainers to remain compliant with Ind AS 115 and GST?

Estimate variable consideration, include only amounts highly probable not to reverse. For success fees, recognise on confirmation of KPI achievement, then raise invoices to avoid GST credit notes later. Penalties should reduce revenue promptly with credit notes issued in the same GST period.

For export retainers under LUT, what rate do I use for revenue recognition and how do I handle FX differences?

Use the INR spot rate on the recognition date for monthly revenue. On settlement, compare the rate to recognition, post FX gain or loss. Maintain LUT, foreign currency invoices, FIRC or BRC, and align reporting in GSTR-1 and GSTR-3B. Automate FX entries and documentation storage with AI Accountant.

Which TDS section applies to consulting retainers, and how do I prevent client-side TDS lapses?

Most consulting retainers fall under Section 194J at 10 percent, technical or professional services. Some execution-heavy scopes may fall under Section 194C. Prevent lapses by contractually specifying the section, sending monthly reminders, and reconciling Form 26AS, tools like AI Accountant can flag missing TDS entries by client.

How should mid-month starts and early terminations be recognised for monthly retainers?

Pro-rate by calendar days for mid-month starts unless the contract stipulates full-fee recognition or front-loaded setup justifies full-month recognition, document rationale. For terminations, stop recognition from the effective date, refund unearned amounts from Deferred Revenue, and issue GST credit notes promptly.

What evidence does an auditor expect to support over-time recognition for advisory retainers?

Auditors expect contracts that describe stand-ready obligations, timesheets or capacity allocation reports, deliverable logs, client approvals, and a documented recognition method. Maintain a revenue recognition file per retainer with month-end sign-offs, automated collection is possible through AI Accountant workflows.

How can a CA ensure CRM-to-finance integrity so that no retainer goes unbilled or misrecognised?

Enforce mandatory CRM fields, start or end dates, billing cadence, GST or TDS flags, create an approval handoff to finance for ledger setup and revenue schedules, and run weekly triage between delivery and finance. Reconcile CRM contracts to invoices monthly and automate variance alerts in AI Accountant.

What are the minimum ledgers I should set up in Tally or Zoho Books for clean retainer accounting?

Retainer Revenue in P&L, Deferred Revenue and Unbilled AR in the balance sheet, AR, Output GST accounts, and TDS Receivable ledgers by section. Use cost centres or projects for client-level tracking, schedule monthly recurring recognition journals or upload via imports, and consider AI Accountant for auto-mapping and reconciliations.

How do I handle disputes, refunds, and credit notes without breaking monthly KPIs and GST?

Log disputes and run a documented resolution workflow, reverse revenue through Sales Returns where appropriate, issue credit notes in the same GST period, and adjust dashboards for MRR, margins, and DSO. Maintain audit trails and reconcile AR and Output GST post-adjustment.

What metrics should a CA prioritize to prove revenue quality in diligence or bank reviews?

Prioritize MRR stability, deferred and unbilled roll-forwards, gross margin by client, DSO trends, churn and expansion revenue, and documentation completeness. Show tight CRM-to-finance integration, and automated reconciliations through AI Accountant, this signals high revenue quality and operational discipline.