Key takeaways

- Scope: Section 194J applies to professional services, technical services, royalty, and non-compete fees paid to residents, classification drives the rate.

- Rates FY 2025-26: Professional services at 10%, technical services at 2%, royalty on films often at 2%, other royalty and non-compete at 10% per the TDS rate chart and Income-tax TDS tables.

- Higher rates for non-compliance: PAN not furnished triggers 20% under 206AA, specified persons under 206AB face higher of twice the rate or 5%, see TDSman FY 2025-26 chart.

- Threshold: TDS starts when annual payments per category exceed ₹30,000, once crossed, apply TDS on the entire amount, reference Section 194J guide.

- Timing: Deduct at earlier of credit or payment, year-end provisions on March 31 require immediate deduction, advance payments also attract TDS, see prepayment management system.

- GST treatment: If GST is shown separately, compute TDS excluding GST, if bundled, deduct on gross.

- Classification helps avoid notices: Use 194H for commission, 194C for work or labor contracts, 194J for professional or technical services, per the TDS rate chart.

- Compliance calendar: Deposit by the 7th for April to February, by April 30 for March, file Form 26Q quarterly, see TDSman deadlines and APCCA chart.

- Controls and tools: Automate PAN validation, 206AB checks, threshold alerts, and filing with AI Accountant or similar software.

What Section 194J Covers: Quick Overview

If you run a service company in India, Section 194J can feel intimidating, yet once you know what it covers, classification becomes straightforward.

Core coverage areas

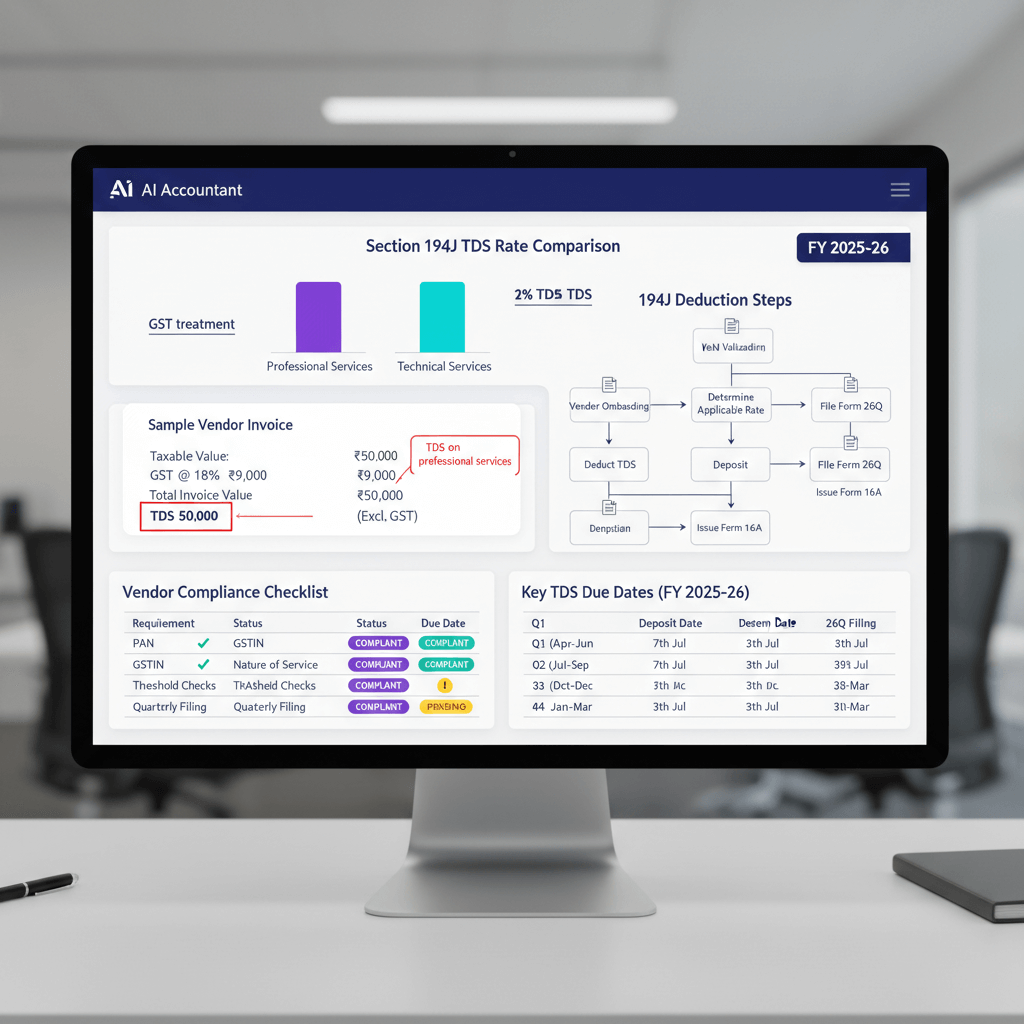

Professional services TDS under Section 194J applies to payments for professional services, technical services, royalty, and non-compete fees, when paid to residents.

- Professional services: lawyers, doctors, engineers, architects, accountants, consultants, interior decorators, advertising agencies, and notified professions, reference the official Income-tax TDS tables.

- Technical services: managerial, technical, or consultancy services, often covering IT support, system maintenance, data processing, and back-end processes.

- Royalty payments: use of copyrights, trademarks, patents, designs, or commercial equipment, cinematographic films often have a special rate.

- Non-compete fees: payments for refraining from certain business activities or sharing know-how.

What’s not covered

Payments to non-residents fall under Section 195, salaries under Section 192, and purely personal payments by individuals or HUFs not under audit are outside 194J. Understanding these exclusions prevents downstream compliance issues.

Tip: Document your classification notes for each vendor, it is a simple habit that avoids costly rework during scrutiny.

Current TDS Rates for FY 2025-26

Rates are stable, yet knowing the exact numbers is essential for correct deduction and clean vendor 26AS reconciliation.

Standard rate structure

- Professional services: 10%, per the TDS rate chart and official tables.

- Technical services not being professional services: 2%.

- Royalty for film distribution or exhibition: commonly 2% where notified.

- Other royalty and non-compete: 10%.

For a readable overview, see Ventura Securities on 194J and Bajaj Finserv guide.

Higher rates for non-compliance

- No PAN under 206AA: deduct at 20% or the prescribed rate, whichever is higher, see Section 194J overview.

- Specified persons under 206AB: deduct at higher of twice the rate or 5%, practical rates explained in TDSman FY 2025-26 chart and Section 194J guide.

Threshold Limits and Application

Basic threshold rules

TDS under 194J applies when aggregate payments to a payee exceed ₹30,000 in a financial year, tracked per category, professional, technical, royalty, and non-compete, not combined. Once the threshold is crossed, deduct TDS on the entire amount including the crossing payment, see Section 194J guide and Bajaj Finserv overview.

Practical threshold tracking

- Track cumulative payments per vendor PAN, not branch-wise.

- Set alerts at 80% of the threshold in your accounting system.

- Update vendor masters when patterns change, especially for recurring services.

Who Must Deduct TDS Under 194J

Entities required to deduct

Companies, LLPs, partnerships, cooperative societies, trusts, and societies must deduct when conditions are met. Individuals and HUFs only deduct if they were liable for tax audit under Section 44AB in the preceding year, see the TDS tables and Bajaj Finserv guide.

Individual and HUF exceptions

Even audited individuals or HUFs need not deduct on exclusively personal payments. Bootstrapped founders operating as individuals typically do not have 194J obligations unless prior year audit limits were crossed.

When to Deduct: Timing Rules

Basic timing principle

Deduct at the earlier of credit or payment, including year-end provisions, and advance payments. A practical explanation of prepayments and operational timing is available in the prepayment management system discussion.

GST and TDS base

If GST appears separately on the invoice, compute TDS excluding GST. If GST is bundled, deduct on the gross amount. For reimbursements, pure agent flows with proper documentation may be excluded, while lumped reimbursements often attract TDS on the full amount.

Compliance note: Train your team to check whether GST is shown separately, a two-second check saves you from chronic over or under deduction.

194J vs 194C vs 194H: Classification Framework

Decision tree for service companies

- Is it commission or brokerage, apply 194H at 2% with threshold in the ₹15,000 to ₹20,000 range, per the TDS rate chart.

- Is it a contract to carry out work or supply labor, like printing, logistics, housekeeping, use 194C at 1% to 2%.

- Else, if resident professional, technical, royalty, or non-compete, use 194J.

Common classification examples

- Creative brand strategy or ad films, generally 194J at 10%.

- Printing based on your design, typically 194C.

- Software consulting architects, 194J technical consultancy.

- Hardware AMC, often 2% technical under 194J, some treat under 194C, document your rationale.

- Call centers on headcount processing, commonly 194C.

- Sports coaches and physiotherapists, 194J professional engagement.

Practical Examples with Calculations

Example 1: CA professional fees

Invoice: ₹1,00,000 plus 18% GST, total ₹1,18,000, PAN available, threshold crossed.

Rate 10%, TDS base ₹1,00,000 excluding GST, TDS ₹10,000, net payment ₹1,08,000.

Example 2: Technical services with complications

Invoice: ₹2,00,000 plus GST.

- Scenario A, normal case: 2%, TDS ₹4,000, net payment ₹2,32,000.

- Scenario B, no PAN under 206AA: 20%, TDS ₹40,000, net payment ₹1,96,000, see Section 194J overview.

- Scenario C, specified person under 206AB: higher of 4% or 5%, apply 5%, TDS ₹10,000, net payment ₹2,26,000, explained in TDSman chart.

Example 3: Crossing threshold mid-year

April payment ₹28,000, no TDS. September payment ₹7,000, cumulative ₹35,000, threshold crossed. Deduct 10% on the entire ₹35,000, TDS ₹3,500, deduct from the September payment, per the Section 194J guide.

Vendor Onboarding Best Practices

The right onboarding prevents costly cleanup later, and supports smooth monthly processing.

Essential onboarding steps

- Validate PAN on the Income-tax portal, capture service nature, map to the correct section.

- Verify GSTIN, and invoice format, document classification reasoning.

- Collect Form 13 or Section 197 certificates, run 206AB specified person checks, store screenshots.

- Automate with vendor onboarding automation for consistency and speed.

Ongoing monitoring

- Maintain vendor-wise ledgers with TDS components and running thresholds.

- Update masters quarterly for certificate or status changes.

- Review high-value vendors periodically, ensure contracts back your classification.

Monthly Compliance Calendar

TDS deposit deadlines

- April to February: deposit by the 7th of the following month.

- March: deposit by April 30, see TDSman deadlines, TDS rate chart, and APCCA chart.

Use Challan ITNS 281, double-check section and amounts before submission, corrections take time.

Quarterly filing requirements

- Form 26Q due dates: Q1 July 31, Q2 October 31, Q3 January 31, Q4 May 31.

- Issue Form 16A within 15 days of filing 26Q.

Special Situations and FAQs

Payments to non-resident consultants

Use Section 195, examine DTAA, file Forms 15CA or 15CB as applicable. Plan extra time for compliance.

Hospital payments to doctors

Employee doctors on fixed salaries fall under Section 192, visiting consultants on fee-per-visit or revenue share typically attract 194J. Keep contracts clear to separate employment from professional engagement.

Composite contracts

Split materials and services clearly, materials do not attract 194J, services do. Without clear splits, authorities may treat the full invoice as services.

Credit notes and reversals

If services are reversed or refunded, adjust TDS in subsequent returns when permissible, and help vendors claim refunds. Keep credit notes, refund proofs, and correspondence ready for audit.

Technology Solutions for Compliance

How automation helps

Modern tools like AI Accountant, QuickBooks, Xero, FreshBooks, and Tally Prime, predict correct sections from invoice text, exclude GST when shown separately, check PAN and 206AB, monitor thresholds, and show filing and deposit alerts, see the TDS automation software guide 2025.

Key features to look for

- Automated PAN validation and clean vendor masters.

- Threshold tracking with warnings.

- ERP integrations, and compliance dashboards for upcoming deadlines.

Risk Management and Controls

Internal control framework

- Write a TDS policy with a one-page decision tree for 194J vs 194C vs 194H.

- Implement maker-checker for vendor setup and section selection.

- Run quarterly pre-filing reviews to catch misclassifications.

Documentation standards

- Include tax deduction clauses in all service contracts.

- Track Section 197 certificates and validity.

- Store 206AB checks, challans, 26Q acknowledgments, and Form 16A copies, reconcile with Form 26AS.

Common Pitfalls to Avoid

Classification errors

- Not all services are professional at 10%, technical services often qualify for 2%.

- Do not treat employment relationships as 194J, substance over form.

- Document your rationale for borderline 194J vs 194C calls.

Threshold mistakes

- Once crossed, apply TDS on the entire amount, not just excess.

- Track thresholds per category, not combined across all 194J types.

- Include advances in threshold calculations.

Compliance gaps

- Year-end provisions attract TDS immediately.

- Delays in deposit invite interest from the deduction date.

- Validate PANs before first payment, reversing 20% deduction later is difficult.

Consequences of Non-Compliance

Financial impact

Section 40(a)(ia) can disallow 30% of expenses for TDS failures, increasing tax liability. Interest under Section 201(1A) at 1% monthly for non-deduction until deposit, and 1.5% monthly for late deposit after deduction.

Additional penalties

Late filing attracts 234E fees, chronic delays compound costs. Section 271C allows penalties equal to the TDS amount for willful defaults, prosecution is possible in extreme cases.

Reputational issues

Defaults show up in vendor 26AS, vendors may demand gross-up clauses, increasing costs. Notices consume management time and professional fees.

Year-End Considerations

Provision management

Review all March accruals for TDS, including unbilled services. Adjust advance TDS against actual invoices accurately to avoid double deduction.

Threshold reviews

Scan vendors approaching thresholds by February, plan March payments considering cumulative positions. Split payments only for genuine business reasons.

Documentation push

Collect pending Section 197 certificates, chase missing PANs, run 206AB checks for all active vendors, and refresh vendor masters for the new year.

Integration with GST Compliance

Invoice requirements

Ensure GST is shown separately for correct TDS base, verify rates and service classification, check place of supply, exports may have GST relief yet still attract TDS if payee is resident.

Reconciliation practices

Reconcile GST via GSTR-2B and TDS via 26AS separately, do not assume one implies the other. Track input credit availability independently from TDS deductions.

Building a Compliance Culture

Team training

Train accounts teams on section selection logic, share a quick reference, set escalation protocols for complex cases, update guidance when clarifications emerge.

Vendor education

Explain documentation needs upfront, provide Form 16A promptly, help vendors understand credit availability in returns, maintain goodwill through predictable processes.

Future-Proofing Your Compliance

Regulatory updates

Monitor Finance Act changes, watch CBDT clarifications, track judicial precedents, and join professional forums to learn from peer responses.

System scalability

Select technology that scales with volumes, centralize compliance for multi-entity setups, automate wherever possible to cut manual effort.

Conclusion and Action Items

Managing professional services TDS under Section 194J is a discipline, not a guessing game. The professional fees TDS rate and rules for service companies are clear for FY 2025-26, execution quality makes the difference.

Action checklist:

- Audit vendor classifications against the TDS rate chart and official tables.

- Implement systematic onboarding with PAN validation and 206AB checks.

- Enable threshold tracking and alerts.

- Document section selection decisions for borderline cases.

- Use automation tools like AI Accountant to streamline deduction, deposit, and filings.

Disclaimer: This guide summarizes public information for FY 2025-26, tax laws change frequently, consult your advisor for decisions affecting your business.

FAQ

How should a CA classify a vendor’s services between 194J and 194C when the scope mentions consulting and on-site manpower together

Split the contract into service components, consulting and professional expertise generally falls under 194J at 10%, manpower or routine work delivery often fits 194C at 1% to 2%. If the invoice lacks a clear split, document your rationale, obtain a revised SOW if feasible, and deduct conservatively under 194J for the professional portion. AI Accountant can help by parsing descriptions and suggesting a split based on past patterns.

For FY 2025-26, what rate should we apply on creative agency retainers that include strategy, design, and ad film production

Strategy and creative direction are professional services under 194J at 10%, ad film production typically remains within 194J, printing or fabrication done by third parties may be 194C. Use a contract and invoice split to avoid over-deduction, AI Accountant flags mixed scopes and proposes correct sections.

Do we compute TDS excluding GST if the invoice shows GST separately, what if the fee is quoted as a lump-sum inclusive of GST

Exclude GST from the TDS base when shown separately, if fees are lump-sum inclusive, deduct on the gross amount. Train AP teams to check invoice structure, AI Accountant can auto-detect GST segregation and compute the correct base.

When exactly does 206AA at 20% override the normal 10% or 2% rates, and how do we handle vendors sharing PAN post deduction

When PAN is not furnished at the time of deduction, apply 20% or the prescribed rate, whichever is higher. If PAN is shared later, you cannot retroactively reduce the rate for the paid transaction, adjust only prospectively. Maintain a PAN validation workflow, AI Accountant performs PAN checks before payment runs.

How should we apply 206AB for specified persons, do we need to check status every quarter or at each payment

Check 206AB status before the first payment in a quarter, re-check when there is a status change or at quarter end. Deduct at higher of twice the rate or 5%. Store screenshots as evidence. AI Accountant schedules periodic 206AB checks and attaches proof to vendor records.

We crossed the ₹30,000 threshold mid-year for a consultant, do we deduct on the full cumulative amount or only on the amount exceeding ₹30,000

Deduct on the entire cumulative amount, including the payment that crosses the threshold. Update your ledger and ensure the September or subsequent payment carries the catch-up deduction. AI Accountant maintains running thresholds and prompts catch-up entries automatically.

How do we handle year-end provisions on March 31 for unbilled professional fees, should we deduct TDS before receiving the final invoice

Yes, deduct at the earlier of credit or payment, provisions on March 31 trigger TDS immediately. When the invoice arrives, reconcile the provision, adjust any differences, and ensure the vendor’s Form 16A aligns with books. AI Accountant supports accrual-based TDS and maps final invoices to provisions for clean reconciliation.

What is the correct treatment for reimbursements, can we exclude them from TDS if they are pure agent expenses

If reimbursements qualify as pure agent expenses with documentation and are shown separately, you may exclude them from the TDS base. Lumped reimbursements without segregation should be included. Design your invoice template to separate reimbursements, AI Accountant checks invoice lines and flags non-qualifying reimbursements.

We pay a non-resident expert for technical advice, do we apply 194J or 195, and what filings are typically required

Apply Section 195 for non-residents, review the DTAA for rates, and complete Forms 15CA or 15CB as applicable. Plan for timelines, as bank remittance may require documentation checks. AI Accountant can generate the payment checklist and track 15CA or 15CB status.

How should we treat AMCs for servers and network gear, is it 194J technical at 2% or 194C

Many hardware AMCs qualify as technical services under 194J at 2% when they involve technical expertise, routine maintenance without specialized input may be argued as 194C. Review the contract language, document your decision, and keep consistency. AI Accountant compares similar past contracts and suggests the dominant classification.

What deadlines apply for deposits and Form 26Q filing across quarters, and how can we avoid interest and late fees

Deposit by the 7th for April to February, by April 30 for March, file Form 26Q by July 31, October 31, January 31, and May 31 respectively. Use calendar alerts, reconcile before filing, and issue Form 16A within 15 days post filing. AI Accountant’s compliance calendar pushes reminders and monitors pending challans.

How do we correct TDS if a credit note is issued for services not rendered, can vendors still claim refunds

Adjust TDS in the subsequent return where permissible, or the vendor can claim credit as available and seek refund through their return. Keep credit notes, communications, and ledger adjustments well documented. AI Accountant records reversal workflows and ties them to filings for audit trails.