Key Takeaways

- A ledger is the permanent home for balances, updated automatically by vouchers, while a journal is a controlled, manual path used only when no structured voucher fits.

- In Tally Prime, most day to day transactions should flow through Purchase, Sales, Receipt, Payment, and Contra vouchers, not through Journal vouchers.

- Posting purchases or bank items as journals breaks GST logic, disrupts registers, and makes GSTR-2B and bank reconciliation unreliable.

- Reserve journals for accruals, provisions, depreciation, prepayment amortisation, and reclassifications, and ensure every journal carries a clear narration.

- Wrong ITC via journal entries carries interest exposure and penalties, which often exceed any perceived time saved by bypassing the correct voucher.

- Restrict Journal voucher permissions to senior finance, turn on audit trail, and enforce a maker checker workflow to keep adjustments tight and auditable.

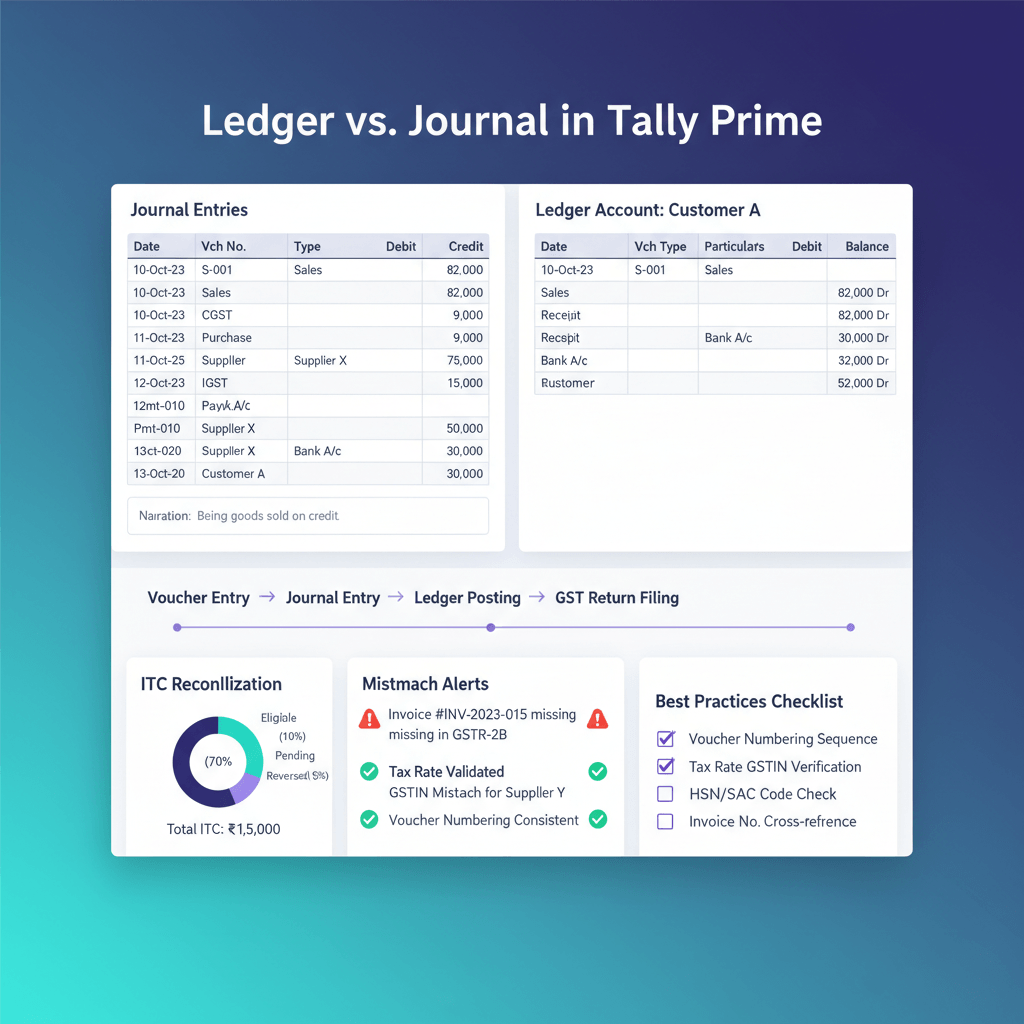

Ledger vs Journal in Tally Prime, the difference that saves money and time

A ledger holds the running balance for a specific account, for example Bank, Sundry Creditors, Input CGST. A journal is a manual, two sided entry that you use only when there is no structured voucher type for the transaction. In Tally Prime, vouchers post directly to ledgers, which means journals are the exception path, not the default.

| Dimension | Ledger | Journal |

|---|---|---|

| What it is | An account that accumulates debits and credits | A manual entry with at least one debit and one credit |

| Role | Book of final entry, holds running balances | Traditionally book of original entry, in Tally an exception path |

| When used | Updated by Purchase, Sales, Payment, Receipt, Contra | Accruals, provisions, depreciation, reclasses |

| Who posts | Any trained operator via source vouchers | Senior finance with narration and approval |

| GST treatment | Voucher type drives correct tax classification | No GST computation logic, no GSTR linkage |

| ITC impact | Purchase vouchers map to GSTR-2B | Journal debits to ITC ledgers have no GSTR-2B link |

| Audit trail | Inherits voucher and document details | Requires complete narration and approval |

| Source | Invoice, bank statement, receipt | Internal memo or schedule, no external document |

The quick rule: if there is a source document, there is a voucher, use it. If there is only an internal schedule, use a journal.

The ten second answer for a Tally led team

The ledger is where every transaction ends up, the journal is one of many input paths, and it is the riskiest one when misused.

What a ledger does in Tally Prime

When you save a Purchase voucher for a vendor bill with GST, Tally automatically splits the amount across Purchase, Input GST ledgers, and the party’s ledger. No journal is needed. These ledger updates are correctly classified and ready for ITC matching through ITC reconciliation.

What a Journal voucher does, and does not do

A Journal voucher is a manual debit and credit. It does not compute GST, it does not populate purchase or sales registers, and it does not trigger e invoicing. A proper journal example is a month end salary accrual, debit Salaries Expense, credit Salaries Payable. When you actually pay salaries, you clear it via a Payment voucher, not a journal.

Use vouchers to move source documents into ledgers, use journals only for adjustments without external documents.

The flow you want, source document to ledger, journals only for adjustments

Design your process so that every document maps to a voucher type at intake. The ledger is updated by those vouchers, and journals remain a controlled exception.

| Source document | Tally voucher type | Key ledgers updated |

|---|---|---|

| Vendor purchase invoice | Purchase | Purchase, Input GST, Sundry Creditors |

| Customer sales invoice | Sales | Sales, Output GST, Sundry Debtors |

| Bank payment to vendor | Payment | Bank, Sundry Creditors |

| Customer receipt | Receipt | Bank, Sundry Debtors |

| Bank to bank transfer | Contra | Bank to Bank |

| Petty cash expense | Payment | Cash, Expense |

| Month end accrual | Journal | Expense, Provision |

| Depreciation | Journal | Depreciation, Accumulated Depreciation |

| Advance tax payment | Payment | Advance Tax, Bank |

How to handle AP, from bill to ledger in three steps

Step one, verify the vendor invoice against the purchase order, use vendor bill matching to enforce checks and tolerances. Step two, post a Purchase voucher with invoice date and GST split, Tally handles ledgers automatically. Step three, save and move on, your Purchase register and ITC ledgers are now aligned for monthly reconciliation. If a bill is booked via a journal, reverse it and rebook as a Purchase voucher.

How to handle bank entries, statement first, not journal first

Import the bank statement into Tally’s bank reconciliation, match lines to the right ledgers, and let Tally post vouchers. Avoid using journals to nudge bank balances, it creates gaps that multiply each month. With bookkeeping automation, statement lines are classified by AI based on your posting history, then synced back to Tally as proper vouchers, not journals.

Legitimate journal entries, the short list

- Accruals for expenses incurred but unbilled

- Provisions for doubtful debts and specific reserves

- Depreciation charges

- Prepayment amortisation

- Reclassifications between ledger groups

Seven costly mistakes that come from mixing journals and ledgers

1. Claiming ITC via a journal

Debiting Input GST by journal without a matching Purchase voucher breaks the GSTR-2B link. This can trigger interest at 24 percent per annum on wrongly availed and utilised ITC, and penalties. See CBIC Circular 238/32/2024 for the treatment under Sections 50 and 122.

2. Replacing Purchase vouchers with journals to save time

Those invoices vanish from the Purchase register, reconciliation takes longer later, and your team spends hours tracing and reversing entries. A minute saved at entry becomes twenty minutes at month end.

3. Using Suspense as a dumping ground

Unidentified bank credits posted to Suspense by journal clog the balance sheet and delay close. Every bank credit needs proper identification and a Receipt voucher, or immediate escalation.

4. Booking depreciation as a Purchase voucher

That creates a fake purchase, inflates creditors, and contaminates GST reports. Depreciation belongs in a Journal entry only.

5. Skipping provisions to avoid journals

Delaying provisions understates expenses during the year and creates a March spike and advance tax shortfall. Journals exist precisely for these adjustments.

6. Posting reclassifications without narration

Unexplained reclasses fail audit tests. Every journal must carry a clear narration that explains the business reason.

7. Passing contra entries as journals

Cash to bank or bank to bank belongs in a Contra voucher. Journals here disrupt sequences and confuse audit trails.

What to configure in Tally Prime, convert policy into process

Ledger master configuration

- Set GST applicability and tax rates on purchase and sales ledgers so vouchers auto compute correct splits.

- Activate cost centres and make allocation mandatory for expense ledgers so department tagging happens at voucher entry, not by month end journals.

Voucher type permissions, restrict Journal to senior finance

Create separate user roles, give operators access to Purchase, Sales, Payment, Receipt, and Contra, and exclude Journal. For multi user setups, enable voucher approval so every journal requires a checker. On the AP side, AiA ingests invoices and posts Purchase vouchers directly into Tally, journals are created only for true adjustments and carry a complete audit trail.

Audit trail and narration, non negotiable

- Turn on Audit Trail so every creation and change is logged.

- Make narration mandatory for Journal vouchers, block saving without it.

Month end checklist for journal control

- Review the journal day book for entries not on the approved adjustment list.

- Confirm narrations explain the business reason for each journal.

- Reconcile Suspense to zero before period close.

- Match total adjustments to an approved schedule signed by the finance head.

When to automate, the ROI of taking statements and bills straight to ledgers

The volume trigger

Once you process more than a hundred bank lines or fifty vendor invoices in a month, manual classification turns into the bottleneck. If you already receive e invoices with IRN, you are generating structured data, then typing it again into Tally.

The error cost equation

One wrong ITC entry of two lakh rupees utilised for a quarter can cost interest at twenty four percent per annum, plus the operational churn of reversals and amended filings. Preventing a single such error can pay for automation.

A simple ROI frame

| Input | Manual | Automated |

|---|---|---|

| Bank posting time per month | 10 hours | 1 hour |

| AP entry time per month | 15 hours | 2 hours |

| Month end journal review | 5 hours | 2 hours |

| Estimated wrong ITC per year | High exposure | Near zero |

| Close cycle | 12 to 15 days | 5 to 7 days |

Readiness signals

- A stable chart of accounts and clear posting rules

- More than 100 bank lines or 50 vendor bills per month

- Recurring journals that should have been vouchers, for example bank, AP, AR

Frequently Asked Questions

Do I need a journal entry first before a ledger updates in Tally Prime?

No. Purchase, Sales, Payment, Receipt, and Contra vouchers update ledgers directly when you save them. Journals are not prerequisites, they are used only when no structured voucher fits the transaction, for example provisions and reclasses.

Can I claim ITC through a journal entry by debiting Input CGST or Input IGST?

No. ITC eligibility flows from invoices that appear in GSTR-2B and are booked through Purchase vouchers. A journal entry does not create a valid GSTR-2B linkage. Using journals to inflate ITC exposes you to interest at twenty four percent per annum on wrongly availed and utilised ITC and potential penalties, see CBIC Circular 238/32/2024.

How do I fix a vendor bill that was posted as a journal instead of a Purchase voucher?

Cancel or delete the journal, then create a Purchase voucher with the correct invoice date, party, amount, and GST split. Ensure the voucher date aligns with the correct GST period. If the period is closed, consult your CA for the right adjustment approach before rebooking.

What is the correct treatment for bank receipts, journal or Receipt voucher?

Always use a Receipt voucher. Journals break the receipt register and can leave party balances uncleared. For unidentified credits, hold for investigation rather than parking in Suspense. With AI Accountant, statement lines are auto classified and posted as Receipt or Payment vouchers for faster, cleaner reconciliation.

When is it appropriate to use a journal for TDS related entries?

Use journals for TDS provisions at period end, for example debit Expense, credit TDS Payable, when you need to accrue tax without a cash movement yet. Actual TDS deductions on vendor payments flow through Payment vouchers. Remember, a journal to TDS Recoverable does not create a legal credit by itself, the deductor’s filing must reflect it in Form 26AS.

Can I restrict Journal voucher access to a few users in Tally Prime?

Yes. Set up user roles that include or exclude specific voucher types. Give operators access to operational vouchers and restrict Journal to senior finance. In multi user, add voucher approval so journals require maker checker sign off.

What is the best way to ensure journal entries pass audit scrutiny?

Enable Audit Trail, enforce mandatory narration on journals, and keep a pre approved month end adjustment schedule. Narrations should explain the business reason clearly, for example reclassifying capex, reversing an accrual, or recognising depreciation.

Should advances to vendors be posted as journals or payments?

Use a Payment voucher, debit the vendor or an Advances to Suppliers ledger, credit Bank. This ensures the advance appears in the party ledger and clears correctly against the subsequent Purchase voucher.

How do cost centres affect the journal versus ledger decision?

Cost centres are captured at voucher entry. Make allocation mandatory for expense ledgers so every Payment, Purchase, and where necessary Journal, prompts for a department tag. This removes the need for later reclass journals for MIS.

Does automation change which entries go to journals versus ledgers?

No. Automation captures documents and predicts ledgers for vouchers, it does not change the rule. Journals remain for adjustments without external documents. Automation simply ensures that the majority of entries land in the correct voucher type on day one.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.