Key takeaways

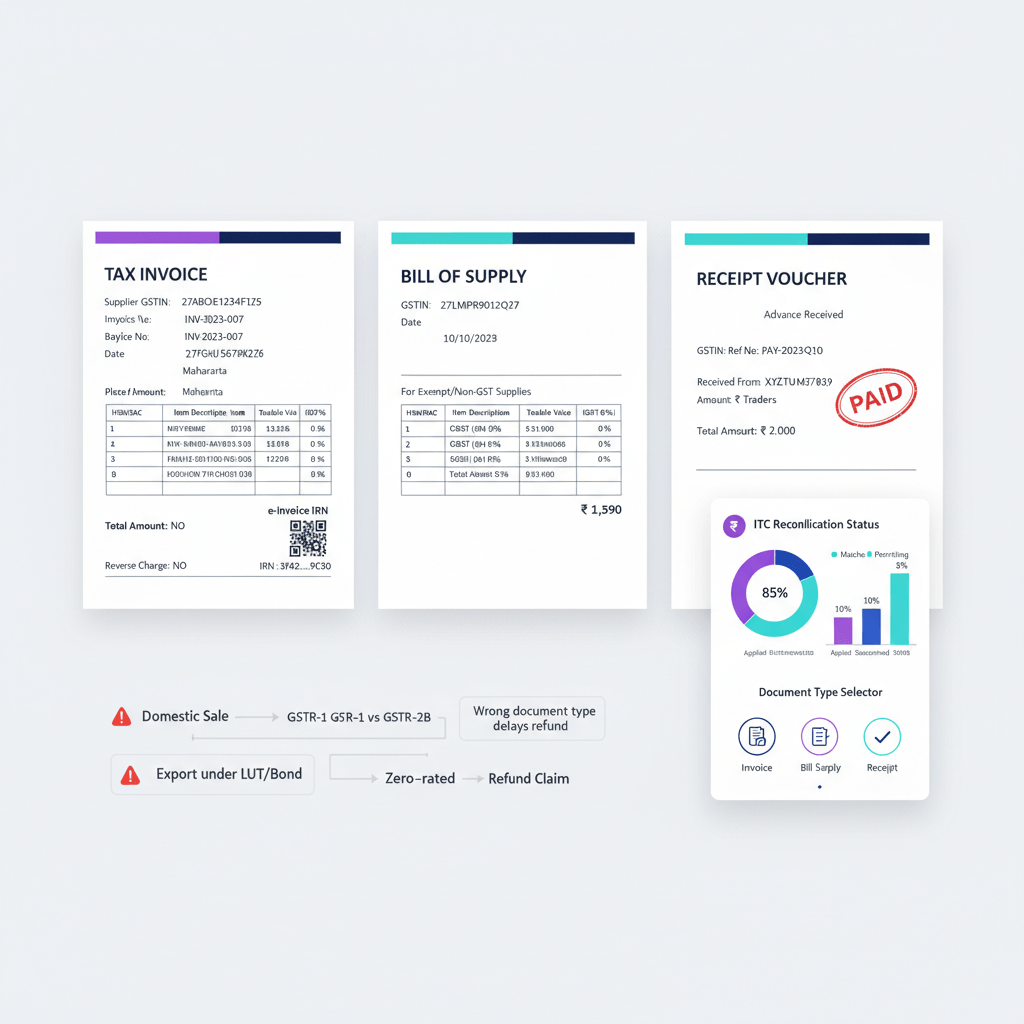

- Exports are zero-rated when issued under LUT/Bond. Under the CBIC LUT/Bond circular, exporters furnish either LUT or Bond to claim zero rating on exports. No IGST is charged, instead, exporters claim input tax credit on input costs. The alternative path requires paying IGST upfront and claiming refund later through the Shipping Bill. See the CBIC circular on LUT/Bond.

- Refund processing depends on accurate data matching. CBIC’s IGST refund FAQs specify that validation errors like SB002 and GSTIN mismatches delay refunds. Export General Manifest data must match Shipping Bills and GST returns exactly. Even bank account or IEC suspension stalls processing. Refunds below ₹1,000 are not processed at all. Reference: CBIC FAQs on IGST refund.

- Document classification drives compliance workflows. Treating a vendor’s tax invoice as a ‘bill’ in your books creates the buyer side payable. Misclassifying advances as simple receipts instead of receipt vouchers can affect ITC timing, particularly for services.

- Export invoice treatment differs from domestic invoices. Export invoices under LUT/Bond are zero-rated supplies, no IGST charged. Exporters choosing the IGST paid path issue standard invoices but claim refunds through Shipping Bills treated as refund claims. Cash flow impact differs significantly.

- Small errors cascade into major delays. Data integrity requirements mean that GSTIN mismatches, unvalidated bank accounts, or incorrect IEC details can block entire refund batches. The ₹1,000 minimum refund threshold means multiple small errors may accumulate into unrecoverable amounts.

Invoice vs bill vs receipt: the short answer

Invoice vs bill vs receipt fundamentally tracks who issues what document, and when GST obligations trigger.

Operational rule: sellers issue invoices to create tax liability, buyers record these as bills in their payables, receipts acknowledge payment but do not create tax positions unless they are receipt vouchers for advances.

DocumentIssued ByPurposeGST ImpactWhen UsedInvoiceSellerDemand for payment with tax calculationCreates GST liability for seller, enables ITC for buyerOn supply of goods or servicesBillBuyer, internalPayable entry mirroring vendor’s invoiceTracks purchase liability, must match vendor invoice for ITCRecording vendor invoicesReceiptPayer or PayeeProof of paymentNo GST impact unless it is a receipt voucherAfter payment settlementExport Invoice, LUTExporterZero-rated supply documentNo IGST charged, ITC on inputs claimedExports under LUT or BondExport Invoice, IGST paidExporterStandard invoice for exportsIGST paid, refund claimed via Shipping BillExports without LUT or BondReceipt VoucherSupplier receiving advanceGST on advance paymentCreates tax liability on service advancesWhen advance is received

Common mistake: using “invoice,” “bill,” and “receipt” interchangeably, inviting ITC mismatches and export refund delays.

What is an invoice in the Indian context?

An invoice is the seller’s tax document that creates GST liability and enables the buyer’s ITC claim. Export invoices under LUT or Bond are treated as zero-rated supplies, no IGST payable, while IGST paid export invoices use the Shipping Bill as the refund claim mechanism. See the CBIC circular on LUT/Bond which clarifies that exports are zero-rated, under LUT or Bond no IGST is charged, alternatively IGST may be paid and refunded later.

Why export invoices are different

- LUT or Bond route: zero-rated, invoice carries LUT or Bond endorsement, exporter claims ITC on inputs, no IGST collected from buyer.

- IGST paid route: standard invoice with IGST, Shipping Bill becomes the refund claim document, cash is blocked until refund is processed.

- Domestic vs export: domestic invoices apply CGST and SGST or IGST based on place of supply, export invoices either show zero tax under LUT or show IGST that will be refunded.

Cash flow tip: LUT or Bond preserves working capital, the IGST paid route suits cases where ITC accumulation is low or procedural certainty is preferred.

Data integrity on export invoices

CBIC’s validation relies on exact matching across the export invoice, Shipping Bill, and EGM data. Common blockers include:

- SB002 errors when Shipping Bill numbers do not match GST returns

- GSTIN mismatches between the invoice and exporter profile

- Port code or value discrepancies

- Missing or incorrect IGST payment details on non LUT exports

Per the CBIC FAQs on IGST refund, inaccurate filings delay refunds. Even small discrepancies can stall the entire refund batch, and refunds below ₹1,000 will not be processed.

Practice pointer: export invoice preparation deserves double checks, because errors directly hit cash flow through delayed refunds.

Frequently asked questions about invoices

What happens if I issue an export invoice without LUT or Bond and do not pay IGST?

It becomes a non compliant export. Rectify by furnishing LUT or Bond immediately or paying IGST with applicable interest, then align your returns and Shipping Bill to the corrected path.

Can I revise an export invoice after the goods have shipped?

Use a credit note or a debit note referencing the original invoice. If the Shipping Bill is filed, seek customs amendment so that invoice, Shipping Bill, and EGM remain in sync for refund.

Do service exports also require LUT or Bond for zero rating?

Yes. Service exports can also opt for LUT or Bond or pay IGST and claim refund, while ensuring place of supply and receipt of foreign exchange conditions are satisfied.

What is a bill in day-to-day accounting?

A bill represents the buyer’s payable entry that mirrors the vendor’s invoice. Field by field accuracy is essential to avoid mismatches with GSTR-2B and to prevent refund delays where export refunds depend on precise alignment of data across systems.

Buyer side view: bill equals vendor invoice in your books

When recording a purchase bill, verify:

- Supplier GSTIN matches exactly

- Invoice number and date match what will appear in GSTR-1

- HSN or SAC codes mirror the vendor’s classification

- Tax breakup into CGST, SGST, IGST aligns with place of supply

The purchase bill forms the basis of ITC that must later match GSTR-2B. Even a small mismatch can cause reconciliation effort out of proportion to the error.

Why tiny mismatches matter

- Invoice number typos: “INV-1234” vs “INV/1234” creates an orphan entry

- Date discrepancies: using email receipt date instead of invoice date affects Section 16(4) eligibility

- Rounding errors: sub rupee differences accumulate across volume

- GSTIN errors: a single character error breaks validation

In exports, ITC accuracy on purchases is crucial, because refund algorithms compare claimed credits with what is present in GSTR-2B and customs data.

Frequently asked questions about bills

Should I record a bill from the PDF invoice or wait for the vendor’s GSTR-1?

Record promptly from the PDF, then reconcile with GSTR-2B on the 14th of next month and seek corrections via credit or debit notes if needed.

What if my vendor calls it a “bill” but it is a proforma?

Proforma does not create tax liability. Do not book ITC against proforma. Wait for the tax invoice.

What if the vendor charged IGST but both of us are in the same state?

Seek a corrected invoice with CGST and SGST. Claiming ITC on the wrongly taxed document risks reversal.

What is a receipt, and how is it different from a receipt voucher?

A receipt acknowledges payment settlement and does not have GST implications by itself. A receipt voucher under GST is a formal document for advances that may trigger tax liability, especially for service advances where tax is payable on receipt.

Receipt vs receipt voucher

- Simple receipts: payment acknowledgments, bank confirmations, or gateway confirmations, no GST impact.

- Receipt vouchers: must be issued for service advances, require GST calculation, sequential numbering, and reporting in GSTR-3B. If cancelled, a refund voucher is needed.

For goods, advances are not taxed upfront due to Notification No. 66/2017 Central Tax. For exports, maintain documentation to support zero rating where applicable.

CBIC’s validation focus on accuracy extends to advances too, see CBIC FAQs on IGST refund for general principles around validation and refunds.

Frequently asked questions about receipts

If I receive partial payment from a customer, do I need a receipt voucher with GST?

For service advances received before invoicing, yes, compute GST on the advance. For goods, no GST on advances, but document the advance.

Can a bank statement alone work as a receipt for GST?

It proves payment, but for advances on services you still need a compliant receipt voucher with prescribed particulars.

What is a refund voucher?

It reverses the tax earlier paid on an advance when the advance is refunded, referencing the original receipt voucher.

Invoice vs bill vs receipt: a side-by-side comparison

AspectInvoiceBillReceiptIssued bySeller or service providerBuyer, internal documentPayer or payeePurposeDemand payment and establish tax liabilityRecord payable from vendor invoiceAcknowledge payment settlementGST or Tax effectCreates GST liability, enables buyer’s ITCCaptures ITC claim to match GSTR-2BNo tax effect unless a receipt voucherTypical voucherSales voucherPurchase voucherReceipt or payment voucherTimingOn supply or advance for servicesWhen vendor invoice is receivedAfter paymentExport scenarioZero rated under LUT or IGST paidMust match export invoice for ITCFIRC supports forex receiptCompliance risk if wrongPenalties, ITC denial to buyerGSTR-2B mismatch, ITC reversalMissed advance tax liability

Under LUT or Bond, exporters do not charge IGST, alternatively they may pay IGST and claim refund later, as clarified in the CBIC LUT/Bond circular. The choice of document classification therefore has direct cash flow consequences.

Data must match perfectly across Shipping Bill, EGM, and GST returns, otherwise refunds are delayed. Refer: CBIC FAQs on IGST refund.

Frequently asked questions about the comparison

Can a single document serve as both invoice and receipt?

You may mark an invoice as paid, but accounting still requires separate recording of the receipt or payment voucher. Compliance points remain distinct.

Why do some vendors title their document “Bill” when it is actually an invoice?

The legal nature depends on contents, not the label. If mandatory invoice fields exist, it functions as a tax invoice for ITC.

In exports, is the Shipping Bill an invoice or a receipt?

Neither, it is a customs document that, for IGST paid exports, doubles as the refund claim. The commercial invoice remains the tax document.

When should you use an invoice, a bill, or a receipt?

Decide based on your role in the transaction, the nature of supply, and timing, especially in exports where LUT or Bond versus IGST paid affects the refund path and working capital.

Sales and purchases

- When selling domestically: issue a tax invoice on supply. For e invoicing thresholds, generate IRN/QR codes where applicable.

- When purchasing: record the vendor’s invoice as a purchase bill in your books, then perform GSTR-2B reconciliation on the 14th of next month and resolve mismatches.

- For advances received: services require receipt vouchers with GST, goods do not, exports need proper zero rating endorsements.

Exports

- LUT or Bond route, zero rated: furnish LUT or Bond early, issue zero tax invoices with endorsements, claim ITC on inputs, avoid cash blockage.

- IGST paid route: issue standard invoice with IGST, pay tax via GSTR-3B, file Shipping Bill for refund claim, wait for validation and refund processing.

As the CBIC LUT/Bond circular reiterates, exports are zero rated, and the chosen route significantly affects working capital cycles.

Collections and advances

- Customer payments against invoices: issue simple receipts acknowledging settlement, no fresh GST impact.

- Vendor payments against bills: maintain clear payment trails to support ITC eligibility and audit.

- Customer advances for future supply: services require receipt vouchers with GST, goods require documentation without upfront GST, exports require zero rating support documents.

For teams processing hundreds of documents, manual classification invites error. An AI driven tool, such as AI Accountant, can read PDFs and spreadsheets, detect whether a document is a tax invoice, a purchase bill, or an advance, and post the correct voucher into Tally, reducing refund and ITC delays.

Common mistakes and misconceptions

Myth 1: A receipt is sufficient documentation for any advance payment.

Reality: service advances require receipt vouchers with GST computation and sequential numbering, creating immediate tax liability. Goods advances are not taxed upfront, but still need proper documentation.

Myth 2: Bill of supply works for exports since they are tax free.

Reality: exports need tax invoices showing zero rating under LUT or IGST payment for refunds. A bill of supply will not support customs clearance or ITC. See CBIC LUT/Bond circular.

Myth 3: Minor data mismatches do not affect compliance.

Reality: even small discrepancies can delay refunds, and refunds below ₹1,000 are not processed. Refer to CBIC FAQs on IGST refund.

Frequently asked questions about common mistakes

What if I issued simple receipts for service advances, not receipt vouchers?

Issue receipt vouchers retrospectively, pay GST with interest, and align returns. Maintain a corrective audit trail to mitigate penalties.

Can I claim ITC if the document is titled “Bill” but contains all invoice particulars?

Yes, content prevails over the label. Ensure your purchase entry and 2B matching reflect it as a tax invoice.

FAQ

Are exports zero rated under GST, and should I charge IGST on export invoices?

Exports are zero rated. Either issue zero tax invoices under LUT or Bond, or charge IGST and claim refund via the Shipping Bill. Many CAs advise LUT or Bond to protect working capital, while monitoring ITC accumulation. AI Accountant can flag export invoices lacking LUT or Bond endorsements before filing.

My client’s IGST refund shows SB002, how do I fix it quickly?

SB002 indicates Shipping Bill mismatch with GSTR data. Verify invoice number, date, GSTIN, and value across GSTR-1, GSTR-3B, Shipping Bill, and EGM. Correct the source error, file amendments, and revalidate. AI Accountant can reconcile invoice fields against customs extracts to pinpoint the variance within minutes.

Is a receipt the same as a receipt voucher for services advances?

No. A simple receipt acknowledges payment, a receipt voucher is a GST document that triggers tax liability for service advances. For example, when a professional services retainer is received before invoicing, issue a receipt voucher and report the tax in that month’s GSTR-3B. AI Accountant can auto detect advances from bank entries and draft compliant receipt vouchers.

Can I use a bill of supply for exports under LUT or Bond?

No. Use a tax invoice that states zero rated supply with LUT or Bond reference. A bill of supply cannot support customs clearance or ITC claims. AI Accountant’s document validator can alert if an export document is incorrectly prepared as a bill of supply.

What is the minimum refund threshold under GST, and does it affect small exporters?

Refunds below ₹1,000 are not processed. Small exporters should consolidate and ensure accuracy to avoid permanent losses from multiple sub threshold errors. AI Accountant can aggregate and simulate refund eligibility to prevent such leakages.

How do I correct an already filed invoice in GSTR-1 for a valuation mistake?

Issue a credit note to nullify or reduce the original, or a debit note to increase the value, and then file the corrected document in GSTR-1. Ensure the buyer books the adjustment for 2B alignment. For exports, amend the Shipping Bill if already filed. AI Accountant can generate the appropriate note referencing the original invoice and update ledgers.

Vendor invoice not appearing in GSTR-2B, can my client still claim ITC this month?

Best practice is to claim ITC only when the invoice appears in 2B. Engage the vendor for immediate GSTR-1 correction. If business urgency demands provisional booking, maintain a tracker and reverse if not reflected later. AI Accountant automates vendor nudges and 2B watchlists so finance teams do not miss reversals.

Do B2C cash sales below ₹200 need individual invoices?

Not if the buyer does not request one. Issue a consolidated day end invoice covering all such sales. Maintain cash and POS trails. AI Accountant can bulk generate consolidated documents and map them to POS data for audit readiness.

When are HSN or SAC codes mandatory on invoices, and how granular should they be?

Digit requirements depend on turnover based notifications, with more digits required as turnover grows, and exports generally require full HSN. Use SAC for services. Incorrect classification risks rate disputes. AI Accountant maintains a master of items with HSN or SAC and auto validates rate mappings to reduce misclassification.

How long should invoices, bills, and receipts be preserved for GST audits?

Follow Section 36 document retention timelines, and keep export documentation until refunds close plus the statutory period. Digital preservation is acceptable if records are producible. AI Accountant stores invoice images and audit trails, easing retrieval during scrutiny.

For a service contract, should I issue separate invoices for services and reimbursable expenses?

Often yes, separate invoicing or clear line item segregation helps. Reimbursements without markup may still be taxable unless they qualify as pure agent. Split lines with distinct SAC codes and narratives. AI Accountant templates can pre tag reimbursables and apply correct SAC and tax logic.

How should foreign currency invoices be handled for GST reporting and refunds?

Show FCY values on the invoice, convert to INR using the applicable reference rate on invoice date for GST reporting. For exports, ensure the INR value matches what flows into GSTR-1 and Shipping Bill. Forex gains or losses on receipt are accounting adjustments, not GST events. AI Accountant can capture the conversion rate and maintain both FCY and INR ledgers for accurate reporting.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.