Key takeaways

- GSTR-9 preparation starts with reconciling your books against GSTR-1, GSTR-3B, and GSTR-2B month by month, accuracy depends on doing this throughout the year, not in a December rush.

- If your turnover exceeds ₹2 crore, GSTR-9 is mandatory; above ₹5 crore, you also need GSTR-9C certified by a chartered accountant.

- Strong controls on ITC eligibility, reversals under Section 17(5), and the 180 day supplier payment rule are essential since mistakes here are the top trigger for GST notices and audits.

- A structured reconciliation workbook with tabs for outward supplies, inward supplies, amendments, and DRC-03 payments cuts rework by making exceptions visible early.

- The September 30 amendment cutoff and December 31 filing deadline leave a narrow window, so start reconciliations by July to avoid last minute penalties.

- Automating GST reconciliation and 2B matching eliminates the manual grunt work that causes most GSTR-9 errors and delays.

GSTR-9 Filing for FY 2024-25: What's New in 2026

The GSTR-9 landscape for FY 2024-25 (filed in 2025-26) has shifted in ways that affect preparation timelines and data requirements. Here is what changed and what it means for your workflow.

Until FY 2023-24, the ₹2 crore turnover exemption for GSTR-9 filing remained stable. For FY 2024-25, this threshold continues, but the GST Council's push toward tighter return matching means the auto-populated data in GSTR-9 now pulls more granular detail from GSTR-1 and GSTR-3B. If your monthly returns have unexplained gaps, GSTR-9 will surface them more visibly than before. The GST portal now flags discrepancies between auto-populated tables and manually entered figures at the time of filing, not after.

E-invoicing thresholds dropped to ₹5 crore from August 2023, and businesses that crossed this line mid-year often have mixed data quality in their returns. If that describes your client, expect extra reconciliation work for the months before and after the switchover. Additionally, CBIC's recent circulars have tightened the interpretation of ITC eligibility on construction, employee welfare, and motor vehicles, meaning reversals that were borderline in prior years may now need explicit treatment in your GSTR-9.

Firms still running manual reconciliation across 12 months of GSTR-1, GSTR-3B, and GSTR-2B data face significantly longer cycle times. Platforms that support automated bookkeeping and transaction matching can compress this work from weeks to days, especially for multi-entity CA practices handling several annual returns in parallel.

What to do now:

- Download all 12 months of GSTR-2B and compare against your purchase register before August 2025.

- Verify e-invoicing compliance for any month where your turnover crossed or approached the ₹5 crore mark.

- Review ITC claims against the latest CBIC circulars on blocked credits and reverse where needed, with interest calculated from the original due date.

Understanding GSTR-9 Requirements

Who Must File GSTR-9

Entities with annual turnover above ₹2 crore must file GSTR-9. Taxpayers below ₹2 crore may file voluntarily for a cleaner audit trail and better credibility with lenders.

If your turnover crosses ₹5 crore, file GSTR-9C as well. This is the reconciliation statement certified by a chartered accountant, as specified under Rule 80 of the CGST Rules.

Key GSTR-9 Filing Deadlines

Mark December 31 for filing the annual return. Amendments to regular returns generally close by September 30 following year end. Complete your reconciliations before that date.

Missing the due date invites late fees of ₹200 per day (₹100 CGST plus ₹100 SGST), capped at 0.5% of turnover in the state or union territory. Note the possible follow-on risks like cancellation proceedings or disputes over input tax credit.

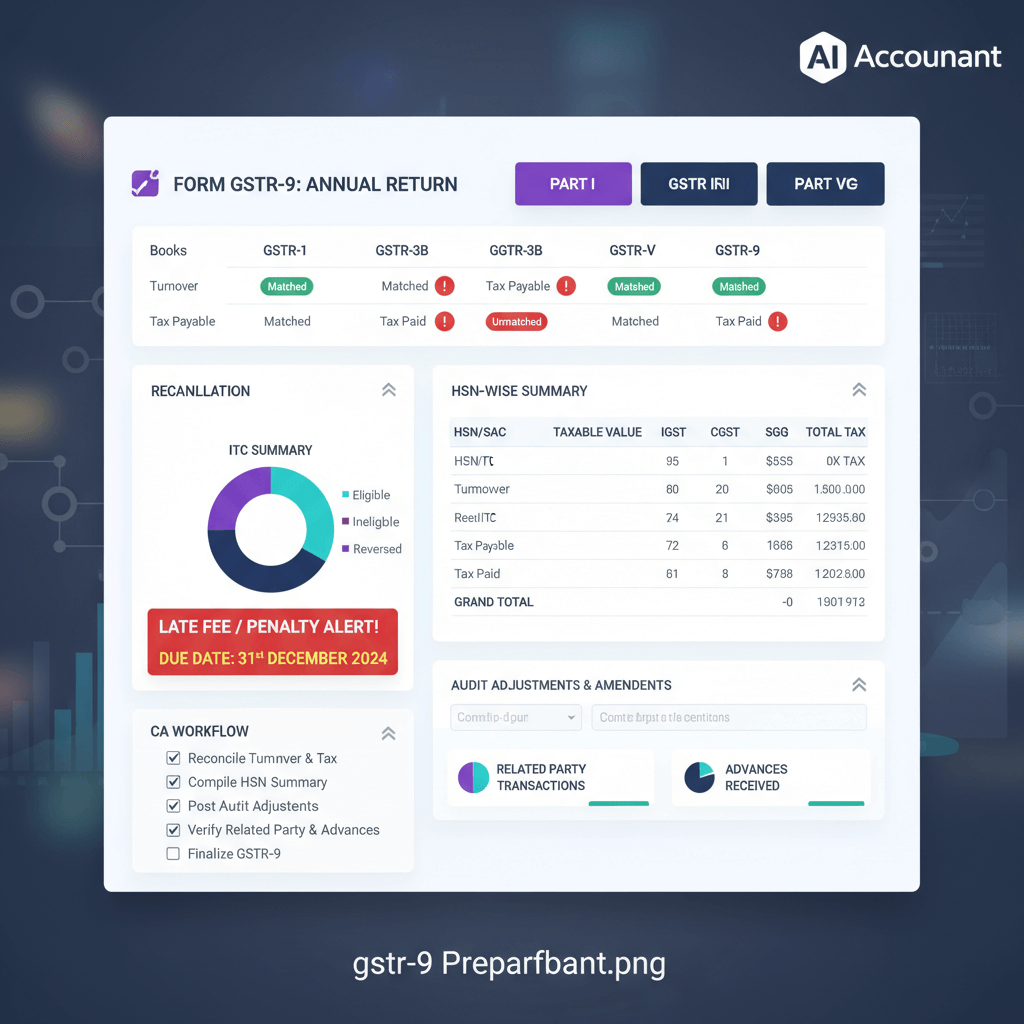

What Information Goes Into GSTR-9

Think of it as a year in review. It covers outward supplies broken down by tax rate, inward supplies and tax paid, input tax credit claimed and reversals, amendments, and tax payments with interest or late fees.

Each figure should be traceable to books, returns, and supporting documents.

If a number cannot be traced, it will not be trusted. Build a paper trail that connects books, returns, and payments.

Essential GSTR-9 Preparation Checklist

Gathering Required Documents

- All 12 GSTR-1 and GSTR-3B returns, arranged month wise.

- Audited financials: profit and loss statement, balance sheet, and cash flow statement.

- Complete sales and purchase registers (ledger entries), plus all tax invoices, credit notes, and debit notes.

- Bank challans for GST payments, mapped to returns.

- Records for exports, reverse charge mechanism (RCM), job work, and special transactions.

Pro tip: Keep a separate folder for amendments and another for DRC-03 payments. This reduces last mile stress.

Creating a GSTR-9 Reconciliation Framework

Build a master workbook with columns for books, returns, and differences. Reconcile outward supplies first, then inward supplies and ITC.

Split workstreams by B2B, B2C, exports, reverse charge, and adjustments. This structure makes exceptions visible faster.

Document timing differences clearly. For instance, March sales recorded in books but reported in April GSTR-1.

Step-by-Step GSTR-9 Filing Process

Monthly Return Reconciliation

Compile GSTR-1 taxable values by rate and month. Tie them to GSTR-3B, then match both with your books of accounts.

Investigate mismatches like advances, cancellations, sales returns, and rate changes. Prepare a reconciliation note that narrates each variance with evidence.

Input Tax Credit Verification

- Check eligibility under Sections 16 and 17 of the CGST Act. Identify blocked credits and reverse them.

- Apply the 180 day rule: reverse ITC with interest where supplier payment (vendor invoice settlement) is delayed beyond the threshold.

- Match claims with GSTR-2A or GSTR-2B data. Resolve supplier non-compliance or GSTIN mismatches.

- Compute common credit reversals for exempt supplies and personal use. Document the formula and basis clearly.

Reminder: Keep a separate log for ITC reversals with reasons, dates, and calculations. Attach proofs to the working paper file. The ICAI's guidance notes on GST audit provide useful frameworks for structuring this documentation.

Handling Amendments and Adjustments

List all amendments made during and after the year that impact the reporting period. Capture invoice level changes, cancellations, and rate corrections.

For additional liability, compute interest from the original due date and pay through DRC-03 before filing GSTR-9. Track credit notes that reduce liability. Ensure counterpart entries appear in counterparties' returns where applicable.

Common GSTR-9 Preparation Mistakes

Data Entry Errors to Avoid

- Wrong GSTINs causing ITC mismatches with GSTR-2B.

- Incorrect tax rate selection (for instance, 18% billed instead of 12%).

- HSN code discrepancies across invoices and returns.

- Duplicate invoices inflating tax liability.

- Rounding inconsistencies across months that compound over the year.

Missing Documents and Information

- Untraceable invoices or credit notes, which can sink ITC claims or reduce credibility of adjustments.

- Missing bank challans, which weakens payment reconciliation.

- Incomplete purchase registers (vendor bill records), which leave claims unsupported.

- Amendment registers not maintained, which produce unexplained gaps in your annual return.

If a document is missing, create a contemporaneous note, gather secondary proof, and mark the file for follow up.

Tools and Software for GSTR-9 Preparation

Accounting Software Integration

AI Accountant automates reconciliation at scale. It connects to your accounting system, syncs transactions, and matches purchase data with GSTR-2B quickly. It flags mismatches, tracks reversals, and prepares filing ready reports with an audit trail.

Other tools that support GST workflows include QuickBooks, Tally Prime, Zoho Books, FreshBooks, and Xero. Evaluate their reconciliation depth against your complexity before choosing.

GSTR-9 Specific Utilities

- GST portal offline utility for preparation and upload.

- Excel pivot based reconciliation templates for large data sets.

- Automated GSTR-2A or 2B download tools to structure vendor data.

- JSON validators to pre-check errors before submission.

- Third party matchers to align books, GSTR-1/3B, and GSTR-2B in one view.

Best Practices for GSTR-9 Compliance

Maintaining Year-Round GST Records

- Reconcile each month after filing. Do not roll forward issues.

- Maintain month wise folders for returns, challans, and registers.

- Run a compliance calendar for due dates, payment windows, and amendment cutoffs.

- Review ITC eligibility monthly. Reverse promptly where required.

- Maintain a live amendment register, plus a DRC-03 log.

- Conduct quarterly internal audits to reduce year end risk.

Internal Audit and Review Process

Adopt sampling for invoice tracing. Verify rate logic, monitor vendor filing status, and test reconciliation throughput quarterly.

Record findings, assign owners, and close actions before the annual crunch. The ICAI's technical guides on internal audit offer useful checklists for structuring this review.

Working with GST Professionals

Engage a professional early. Share complete data and align on a clear scope.

Ask for their reconciliation methodology, timelines, and deliverables. This should include a post-filing compliance note or certificate.

Post-Filing Considerations

Handling GSTR-9 Notices

Notices often seek clarifications rather than penalties. Read carefully, assemble evidence, respond point wise, and consider professional help for complex issues.

If an error is genuine, disclose and correct. Voluntary clarity often reduces exposure. You can refer to the GST Council's published recommendations on dispute resolution for guidance on how departments typically handle voluntary disclosures.

Maintaining GSTR-9 Audit Trail

Create a master file with working papers, reconciliations, challans, DRC-03 proofs, and correspondence. Back up digitally and store physically for at least six years.

Keep a lessons learned memo to streamline next year's filing process.

Conclusion

GSTR-9 is manageable when treated as a year long process, not a December rush. With disciplined reconciliation, tight documentation, and selective automation, you can file confidently and avoid notices.

Start early, track exceptions, and keep your audit trail airtight. Your future self will thank you.

FAQ

How should a CA design an end to end GSTR-9 reconciliation workbook for FY 2024-25?

Start with a control sheet that tracks every GSTR-9 schedule, then create separate tabs for books versus GSTR-1, books versus GSTR-3B, and ITC versus GSTR-2B. Segment data into B2B, B2C, exports, RCM, and amendments. Include a variance log with narrated reasons and evidence, a DRC-03 tracker, and a closing certification checklist.

What is the practical cutoff for amendments in returns versus reporting the difference in GSTR-9?

Amend regular returns by the statutory September 30 window following the financial year. After that window closes, differences flow through GSTR-9 with proper narration and, where needed, DRC-03 payment for additional liability. Maintain an amendment register with invoice wise details to support the audit trail.

How do I validate ITC under Section 16 and reversals under Section 17(5) during GSTR-9 preparation?

Map each purchase to its purpose of use, remove blocked credits listed under Section 17(5), and compute common credit reversals for exempt or personal use. Match all claims against GSTR-2B to confirm supplier compliance. Where credits are ineligible or unmatched, reverse them with interest as applicable. (2026 update) Review claims against the latest CBIC circulars that have tightened interpretations on construction, employee welfare, and motor vehicle credits.

How do I operationalize the 180 day supplier payment rule while compiling GSTR-9?

Run an ageing analysis from the invoice date and flag items exceeding 180 days. Compute the ITC reversal amount with interest and post entries with a clear memo. When payment is made later, re-avail the eligible credit with a reference to the original reversal entry.

What cross checks ensure parity among GSTR-1, GSTR-3B, and books before I finalize GSTR-9?

Perform rate wise reconciliation of outward supplies, tie taxable value and tax head amounts across all three sources, and confirm that advances, cancellations, and sales returns are treated consistently. Reconcile e-way bill data where relevant. Prepare a sign-off note for management capturing any residual immaterial differences.

When should I advise management to proceed with GSTR-9C, and what documents are essential?

GSTR-9C is mandatory when turnover exceeds ₹5 crore. Provide audited financials, trial balance, ledgers for GST output and input, reconciliation statements, fixed asset register for ITC on capital goods, and proof of corrective actions on prior audit observations. Keep a management representation letter on file.

Is GSTR-9 mandatory for taxpayers with turnover below ₹2 crore?

No, GSTR-9 is optional if your aggregate annual turnover is below ₹2 crore. However, filing voluntarily creates a cleaner audit trail, strengthens your position during assessments, and improves credibility with banks and lenders evaluating your GST compliance history.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.