-01%201.svg)

Key Takeaways

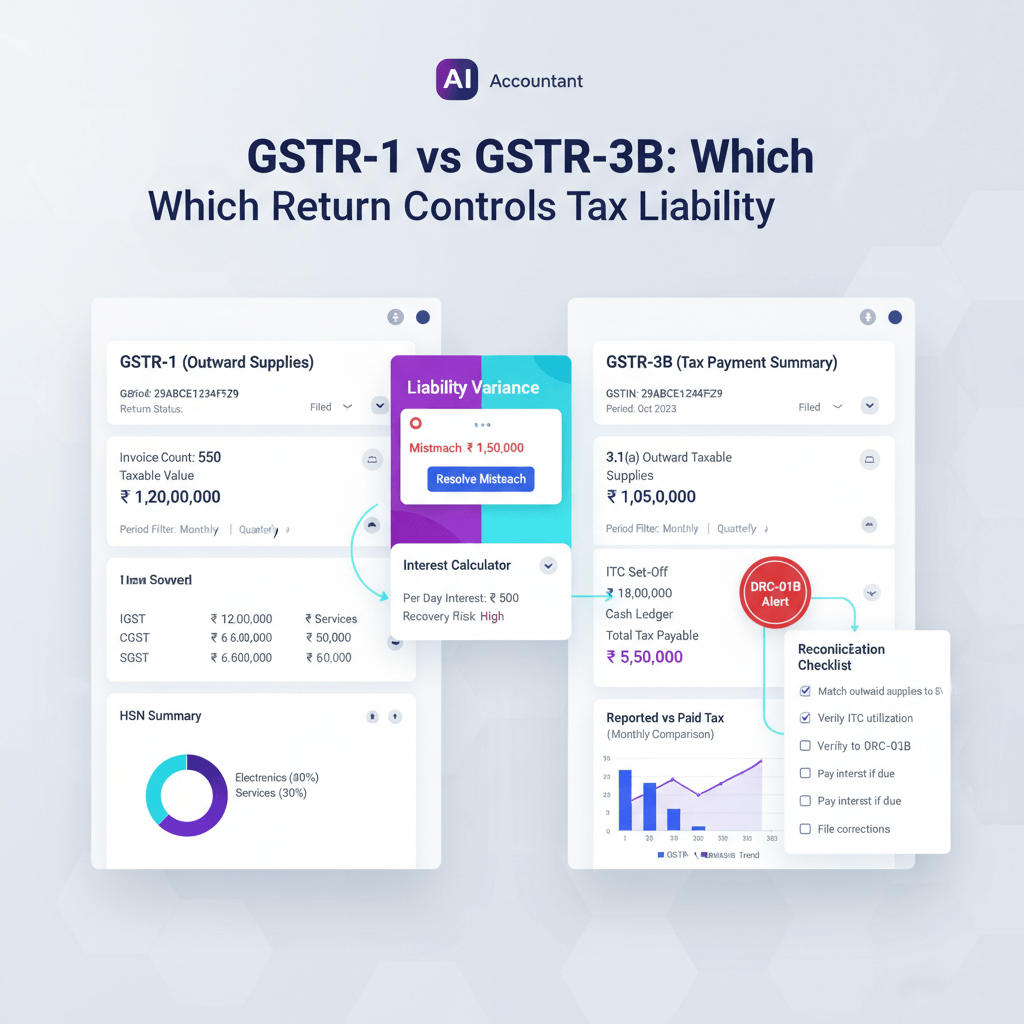

- GSTR-1 declares, GSTR-3B pays. GSTR-1 is the legal statement of outward supplies under Rule 59, while GSTR-3B is the summary return under Rule 61 through which tax is actually discharged. If GSTR-1 shows higher tax than paid via 3B, the shortfall is recoverable as self-assessed tax under Section 75(12) without separate adjudication.

- Mismatch risk is systemic. Finance teams often treat GSTR-3B as the authoritative number, but outward liability is anchored to GSTR-1. A lower figure in 3B than in GSTR-1 will trigger a DRC-01B intimation and a seven-day response clock.

- Late filing hurts twice. Late fees apply to both GSTR-1 and GSTR-3B, and any tax paid after the 3B due date attracts interest at 18% per annum from the day after the due date until payment.

- E-invoice auto-population can create gaps. For businesses above ₹5 crore turnover, IRP e-invoices auto-populate GSTR-1. If 3B is prepared from a different data source than the IRP feed, mismatches arise.

- HSN discipline matters. Report 6-digit HSNs if above ₹5 crore turnover, 4-digit if at or below ₹5 crore. Wrong or missing HSNs cause line-level validation issues and downstream 3B mismatches.

GSTR-1 Vs GSTR-3B: The Difference, Explained

GSTR-1 and GSTR-3B serve distinct legal functions under the CGST Act, 2017: one declares outward liability, the other settles it.

| Parameter | GSTR-1 | GSTR-3B |

|---|---|---|

| Legal character | Statement of outward supplies | Summary self-assessment return |

| Governing rule | Rule 59, CGST Rules 2017 | Rule 61, CGST Rules 2017 |

| What it captures | Invoice-level outward supply details | Summarised outward supplies, ITC, net tax payable |

| Tax payment | No tax paid here | Tax paid via this return |

| Filing frequency (monthly) | 11th of succeeding month | 20th of succeeding month |

| Filing frequency (QRMP) | 13th of month after quarter | 22nd/24th of month after quarter |

| Amendment vehicle | Tables 9A, 9C, 9D for prior-period corrections | Current-period 3B reflects revised liability |

| E-invoice link | Auto-populated from IRP for eligible taxpayers | No auto-population, manually entered or derived |

| Recovery risk | Declared liability recoverable under Sec 75(12) | Underpayment attracts 18% interest under Sec 50 |

| HSN requirement | 4-digit (≤₹5 cr) / 6-digit (>₹5 cr) | No HSN requirement |

The rule most teams get wrong: GSTR-3B is not the primary record of outward liability, GSTR-1 is. If your 3B shows ₹10 lakh in output tax but your GSTR-1 already declared ₹12 lakh, the ₹2 lakh gap is recoverable without a separate demand notice — it is already self-assessed tax per the proviso to Section 75(12) of the CGST Act, 2017, as clarified in CBIC Circular 238/32/2024.

GSTR-1 Vs GSTR-3B — What Is The Difference And Which One Sets Your Liability?

GSTR-1 is the legal trigger for outward tax liability, GSTR-3B is the mechanism through which that liability is extinguished. Both are mandatory, and both must tie to your books — but they do different jobs. Treating 3B as the “real” return and GSTR-1 as a downstream report is the single most expensive misread in GST compliance.

GSTR-1: The Declaration That Creates Legal Exposure

GSTR-1 records every outward supply — B2B invoices, B2C supplies, exports, credit notes, debit notes, and advances for services. Once filed, the liability declared in GSTR-1 is treated as self-assessed by the taxpayer. The proviso to Section 75(12) of the CGST Act, 2017 explicitly allows tax authorities to recover tax declared in GSTR-1 but unpaid via GSTR-3B through direct recovery proceedings — no show-cause notice, no adjudication under Section 73 or 74 required, as confirmed in CBIC Circular 238/32/2024.

Worked example: Your sales team issues a ₹50 lakh B2B invoice in March. It gets reported in GSTR-1 by the 11th of April. Your GSTR-3B for March, filed on the 20th, only captures ₹45 lakh because the last-minute invoice was missed. The ₹5 lakh gap is self-assessed tax. Recovery can start without notice.

GSTR-3B: The Cash-Payment Control

GSTR-3B captures summarised outward supplies, ITC claimed, and net tax payable after ITC set-off. It is where you actually pay GST — either by debiting your electronic cash ledger or applying ITC from the electronic credit ledger. The due date for monthly filers is the 20th of the succeeding month, for QRMP filers it is the 22nd or 24th depending on the state. Late payment attracts 18% per annum interest under Section 50 of the CGST Act, computed from the day after the due date to the date of actual payment.

The Five Operating Rules

- GSTR-1 declares, GSTR-3B pays. A declaration without payment is an open recovery risk.

- GSTR-1 should be filed before GSTR-3B for the same period, and sequencing is enforced for QRMP via IFF.

- Tax declared in GSTR-1 and not paid in 3B attracts interest from the GSTR-3B due date, not from the GSTR-1 due date.

- Late fees under Section 47 apply independently to each return — ₹50 per day per return, ₹20 per day for nil returns, subject to caps.

- E-way bill generation is blocked after two consecutive unfiled GSTR-3B returns under Rule 138E.

Remember: a lower 3B than your GSTR-1 invites a DRC-01B intimation, and the seven-day clock starts the day the intimation is issued.

Frequently Asked Questions About GSTR-1 And GSTR-3B Liability

If I file GSTR-1 on time but GSTR-3B late, what interest do I owe?

Interest under Section 50 of the CGST Act, 2017 is charged at 18% per annum on the tax paid late. It runs from the day after the GSTR-3B due date — not from the GSTR-1 filing date — to the date of actual tax payment. For a ₹10 lakh liability paid 30 days late, interest is approximately ₹10,00,000 × 18% ÷ 365 × 30 ≈ ₹14,795. See CBIC Circular 238/32/2024.

Can GSTR-3B be filed without filing GSTR-1 first?

For monthly filers, GSTR-3B can technically be filed before GSTR-1 in a period. For QRMP scheme filers, invoice details flow via IFF before the quarterly GSTR-1. The system compares GSTR-1 and 3B after both are filed, and any positive difference triggers a DRC-01B intimation. Filing 3B first does not prevent mismatch detection.

3B Vs GSTR-1 — Which One To Trust For Revenue, MIS, And Cash Planning?

For internal MIS and cash planning, MIS reporting dashboards need accurate inputs from both returns: GSTR-1 is the more granular, legally determinative record of outward revenue, while GSTR-3B governs what cash actually left your bank for tax. Your books should be the master, with both returns derived from them.

What Each Return Tells Your MIS

GSTR-1 gives invoice-level revenue by GSTIN, HSN, tax rate, and supply type — the closest GST-native approximation of your revenue ledger. GSTR-3B gives net tax payable after ITC — the cash number treasury needs. For businesses above ₹5 crore turnover, IRP e-invoices auto-populate GSTR-1, which means your GSTR-1 can reflect invoices that your accounting system has not yet posted.

Decision Criteria: Which Number To Use

| Decision | Use This | Why |

|---|---|---|

| Revenue for MIS / P&L | Books (sales register) | GSTR-1 excludes non-GST revenue; 3B is summarised |

| Output tax liability | GSTR-1 | Invoice-level declaration, legally determinative |

| Net GST cash outflow | GSTR-3B | Actual payment after ITC |

| ITC reconciliation | GSTR-2B + books | 3B ITC claim must match GSTR-2B auto-draft |

| Creditor / receivable ageing | Books | Returns do not carry party-wise aging |

| HSN-wise revenue analysis | GSTR-1 (Table 12) | 4/6-digit HSN mandatory; most granular GST view |

If you are unsure about the monthly input credit side while finalising outward liability, get clear with 2A vs 2B ITC rules.

E-Invoice Auto-Population: The Hidden Alignment Risk

When an IRN is generated on the IRP, the invoice details push automatically to the supplier's GSTR-1. The risk: if you maintain a separate billing system or cancel and re-issue invoices on IRP without updating your books, a 3B prepared from the books will understate liability compared to GSTR-1. Reconcile IRP data before 3B preparation.

HSN Accuracy Is A Revenue-Level Problem

Wrong HSN codes in GSTR-1 create rate-band mismatches with 3B. If a line is coded at 18% HSN in GSTR-1 but the 3B includes it at 12%, the system flags a rate mismatch. Clean stock item HSN masters before month-end. Taxpayers above ₹5 crore must report 6-digit codes, at or below ₹5 crore must report 4-digit codes, per CBIC notifications accessible on cbic-gst.gov.in.

Frequently Asked Questions About MIS And Return Alignment

Should I use GSTR-1 or 3B to report revenue in my MCA annual return?

Neither. MCA filings use audited book figures, not GST return data. However, GST returns must reconcile with financials — GSTR-9 requires differences to be disclosed. If GSTR-1 and books diverge materially, GSTR-9 preparation becomes complex and risks scrutiny.

My GSTR-1 shows higher revenue than books because of a cancelled e-invoice that was re-raised. How do I fix it?

Report the cancellation via a credit note in Table 9B of GSTR-1 in the period of cancellation. Ensure the original invoice and credit note both appear in GSTR-1, and adjust 3B in the same period. Do not leave a cancelled IRN unreported — IRP pushes the original invoice to GSTR-1 automatically, only the credit note will net it out.

The Usual Culprits: GSTR-1 Vs 3B Mismatches That Trigger DRC-01B — And How To Fix Them

A DRC-01B intimation is auto-generated by GSTN when the tax liability in GSTR-1 exceeds the tax paid in GSTR-3B for the same period. You have seven days from the date of the intimation to either pay the differential tax with interest or furnish a valid explanation on the portal. Ignoring it converts the gap into a recoverable demand under Section 75(12).

How DRC-01B Works

The system compares the outward tax liability declared in GSTR-1 against the outward tax declared in Table 3.1 of GSTR-3B. When GSTR-1 exceeds GSTR-3B by a meaningful amount, DRC-01B is issued. The taxpayer must log in to the portal and either accept and pay, or contest with a written explanation. No published tolerance threshold has been specified — any positive difference may generate the intimation.

Six Mismatch Patterns And Their Fixes

1. Invoice filed in GSTR-1 in a prior period, missed in that period's 3B

Cause: Invoice entered after 3B filing, captured in prior-period GSTR-1 via amendment.

Fix: Pay differential tax for the prior period in the current 3B, with interest at 18% under Section 50 from the day after the original due date.

2. Credit note in GSTR-1 not reflected in 3B

Cause: Credit note reported in Table 9B but 3B shows gross liability without netting.

Fix: Deduct credit notes in 3B Table 3.1 in the same period they appear in GSTR-1.

3. Advances for services reported in GSTR-1 but omitted from 3B

Cause: Advances posted to liability accounts without GST recognition until invoicing.

Fix: Capture advance-received GST in 3B in the period of receipt; reverse in GSTR-1 Table 11B when invoiced.

4. Inter-branch or inter-GSTIN supplies missed in 3B

Cause: Distinct person supplies treated as internal transfers in books.

Fix: Ensure every GSTIN-to-GSTIN supply appears in 3B Table 3.1 of the supplier.

5. E-invoice auto-populated in GSTR-1 but books show a different figure

Cause: IRP auto-population not reconciled with accounting data.

Fix: Reconcile IRP vs books before preparing 3B; correct mismatches.

6. RCM outward supply wrongly included in 3B outward tax

Cause: RCM-liable supplies included in 3.1(a) by mistake or mis-netted across tables.

Fix: Match GSTR-1 Table 4B with 3B Table 3.1(c)/(d). Supplier's 3B should carry zero output tax for RCM supplies. For a full compliance workflow, see reverse charge accounting under GST.

AiA’s master-data sync with Tally Prime standardises GST rates, HSN codes, and party supply types at the transaction level before GSTR-1 or 3B is extracted — eliminating “wrong rate in wrong section” mismatches at source rather than at reconciliation.

Consequences If You Miss The DRC-01B Window

If no response is filed within seven days, the differential liability stands as recoverable self-assessed tax. Interest at 18% per annum under Section 50 continues to accrue. Non-filing of GSTR-3B for two consecutive periods also triggers e-way bill blocking under Rule 138E — this can halt logistics entirely, per the e-waybill portal.

Frequently Asked Questions About DRC-01B And Mismatch Resolution

What happens if I disagree with the DRC-01B amount?

Respond within seven days on the portal with a detailed explanation and working. If accepted, no further action is taken; if rejected, the matter can escalate to a formal demand under Section 73 or 74. Keep your reconciliation workbook ready — portal responses are permanent records.

Does GSTN generate DRC-01B for every small difference?

No threshold has been formally published. Any positive difference can trigger the intimation. In practice, departments focus on material differences, but the system itself does not filter by size.

Can I amend GSTR-3B after filing to avoid a DRC-01B?

No. GSTR-3B cannot be revised. Declare the shortfall in the next period’s 3B and pay interest at 18% for the shortfall period.

Month-End Close Workflow: Books ↔ GSTR-1 ↔ 3B (And What To Lock Before Filing)

The structural fix for GSTR-1 vs 3B mismatches is a locked, sequenced month-end workflow — not a post-filing scramble. The workflow below assumes a ₹2 crore monthly revenue business using Tally Prime, with credit notes, RCM, and advance receipts in play.

AiA’s AP and bills automation pulls invoices, advances, and credit notes directly into Tally, maps them to the correct GST ledgers, and runs a pre-filing reconciliation of outward supplies — so the GSTR-1 data extracted from Tally already matches the 3B working before either return is filed.

The Ten-Step Monthly Close Checklist

Step 1 — Lock the sales register by the 8th.

No new invoices or credit notes for the closed month after the 8th. Late postings create next-month liability risk.

Step 2 — Reconcile IRP data against Tally.

Download the IRP report and match every IRN against your sales register. Any IRN missing in books is a GSTR-1 auto-population gap and a future 3B mismatch.

Step 3 — Post credit notes and debit notes to the correct period.

Credit notes reduce current-period GSTR-1 liability; ensure books reflect the correct period. Do not defer to beautify MIS.

Step 4 — Validate HSN codes.

Run an HSN summary, fix missing or short codes in the master. Wrong HSNs create rate-band conflicts.

Step 5 — Capture advance receipts for services.

Identify all advances in the bank statement; recognise GST in the period of receipt and reflect in 3B.

Step 6 — Identify and segregate RCM supplies.

Confirm supplier-side Table 4B shows zero output tax and recipient-side 3B carries the RCM in Table 3.1(d).

Step 7 — Extract the GSTR-1 draft and cross-check totals.

Match taxable value and tax by rate band to the output tax ledger totals.

Step 8 — Prepare the 3B working from the same data.

Build Table 3.1 from the same extract. Any difference here is a data error — fix before filing either return.

Step 9 — File GSTR-1 by the 11th.

For QRMP, file IFF by the 13th for B2B invoices. Lock GSTR-1 filing as the trigger for 3B preparation.

Step 10 — File GSTR-3B by the 20th/22nd/24th.

Re-check: GSTR-1 outward tax total equals 3B Table 3.1 total. If not, investigate before filing. Post-filing fixes incur interest.

Worked example: ₹2 crore month. Taxable supplies ₹1.8 crore, zero-rated exports ₹20 lakh, credit notes ₹5 lakh, advances ₹10 lakh, RCM purchases ₹3 lakh. GSTR-1 outward tax: (₹1.8 crore – ₹5 lakh) at blended 18% = ₹31.5 lakh. 3B Table 3.1(a): ₹31.5 lakh + ₹1.8 lakh (on advances) = ₹33.3 lakh. 3.1(d) RCM: ₹54,000. 3.1(b): ₹20 lakh at 0%. ITC reduces cash payable. All figures must flow from one extract.

Frequently Asked Questions About Month-End Reconciliation

Should I reconcile GSTR-1 with 3B before or after filing GSTR-1?

Before. Once GSTR-1 is filed, your liability is locked. Align 3B to the filed GSTR-1 to avoid DRC-01B and interest.

How do I handle a credit note that spans two financial years?

Credit notes for a prior FY must be issued by 30 November of the following FY or before filing the annual return, whichever is earlier. Report in GSTR-1 Table 9B in the period issued and net in the same period’s 3B.

Benchmarks And Tools: Time Taken, Error Rates — And When To Automate

The GSTR-1 vs 3B reconciliation problem is operational. It is solved by removing manual steps where errors accumulate — not just by knowing the rules.

What The Benchmarks Show

- Monthly GST prep for ₹2–20 crore businesses typically consumes 2–4 person-days when done manually from Tally exports.

- At least three data pulls are involved: sales register, purchase register, IRP dashboard, each with cross-checks.

- Manual errors compound across periods: a missed October credit note cascades into November and December, with daily interest on unpaid tax.

- DRC-01B is now issued at scale when 1 exceeds 3B; the seven-day response window is enforced.

The Interest And Penalty Math

| Scenario | Period | Liability | Interest @ 18% p.a. | Late Fee |

|---|---|---|---|---|

| GSTR-3B filed 10 days late | Monthly | ₹10 lakh | ≈ ₹4,932 | ≈ ₹500 |

| GSTR-3B filed 30 days late | Monthly | ₹10 lakh | ≈ ₹14,795 | ≈ ₹1,500 |

| GSTR-1 filed 15 days late | Monthly | Nil tax | N/A | ≈ ₹750 |

| DRC-01B unresponded (30 days) | Monthly | ₹5 lakh gap | ≈ ₹7,397 | Plus recovery |

The Operational Case For Automation

Error classes that cause mismatches are predictable: wrong GST rate in stock master, advances not posted as taxable, credit notes parked in suspense, RCM vendors not flagged. These are master-data or posting failures, not filing failures.

Bookkeeping automation inside Tally eliminates these errors at source. AiA ingests bank feeds and bills, maps transactions to correct GST ledgers using AI, and keeps a live reconciliation between books, GSTR-1 extract, and the 3B working. On the ITC side, automated GST reconciliation ensures the 3B claim matches 2B before filing. In practice, both returns derive from one data source — not reconciled after the fact.

The cost of one DRC-01B cycle, including interest and CA time, typically exceeds several months of automation cost for a ₹5–10 crore business.

Related Reading

- How GSTR-2B Reconciliation Works and Why Unmatched Credits Get Disallowed

- Tally Prime and GST Returns: What the Software Does and What It Doesn't

- Month-End Close Checklist for Indian SMBs on Tally

References

- CBIC Circular 238/32/2024 – GST

- CBIC Circular 246/03/2025 – GST

- GST Portal – gst.gov.in

- E-Way Bill Portal – e-waybill.nic.in

- CBIC Tax Information Portal – Rule 59 and Rule 61

FAQ

What is the difference between GSTR-1 and GSTR-3B in simple terms?

GSTR-1 is a detailed statement of all outward supplies made in a period, filed under Rule 59. It declares invoice-level liability but does not involve any tax payment. GSTR-3B is a summary self-declaration under Rule 61 through which you pay net GST after ITC. Think of GSTR-1 as the invoice manifest and GSTR-3B as the cheque. If GSTR-1 exceeds 3B, the gap is recoverable as self-assessed tax under Section 75(12).

Can GSTR-1 be amended after it is filed?

Yes. Prior-period invoices can be amended via GSTR-1 Tables 9A, 9C, and 9D in the current period. Reflect any change in the current period’s GSTR-3B. For e-invoices, amend on the IRP first so the corrected data auto-populates GSTR-1.

What if my GSTR-3B shows more tax paid than what GSTR-1 declared?

That is an excess payment for the period. It sits in your electronic cash ledger for set-off against future liabilities, or you may apply for a refund under Section 54. Overpayment does not attract interest or penalty, but refunds require documentation matching GSTR-1 and books.

Does GSTR-1 need to be filed even if there are no outward supplies?

Yes. File a nil GSTR-1 to avoid late fees and to ensure your customers’ GSTR-2A/2B reflect their inward supplies accurately. Non-filing risks late fees and damages customer ITC eligibility.

What is the QRMP scheme and how does it change GSTR-1 and 3B timelines?

QRMP applies to taxpayers with turnover up to ₹5 crore. Under QRMP, both GSTR-1 and GSTR-3B are filed quarterly, but you still pay monthly via fixed-sum or self-assessment challans. IFF enables monthly B2B invoice reporting so buyers get timely ITC.

What happens if I do not respond to a DRC-01B intimation within seven days?

The differential tax declared in GSTR-1 but unpaid in 3B is treated as confirmed self-assessed tax under Section 75(12). Recovery can begin without adjudication, and interest at 18% per annum continues from the day after the original 3B due date.

How does RCM affect the GSTR-1 vs 3B comparison for the supplier?

RCM supplies are reported by the supplier in GSTR-1 Table 4B with zero output tax. The recipient reports and pays the RCM in 3B Table 3.1(d) and may claim ITC. Properly classified RCM supplies do not create a GSTR-1 vs 3B mismatch for the supplier.

Can I rely on Tally Prime alone to prevent GSTR-1 vs 3B mismatches?

Tally Prime produces both returns from transaction data and validates basic fields, but it does not automatically reconcile IRP e-invoice data or flag rate-band mismatches across returns. Many CAs add a layer like AiA to run pre-filing checks inside Tally, standardise HSN/rates, and reconcile 1 vs 3B before filing.

How should I reconcile when I use both e-invoicing and manual invoices?

Maintain sub-registers for e-invoiced B2B and for non-e-invoice transactions. At month-end, download the IRP report and match every IRN with your sales register, then add manual invoices. The combined totals must match your output tax ledger and flow into both GSTR-1 and 3B. Tools such as AiA can automate this match within Tally and surface gaps before filing.

If my GSTR-1 is higher due to a late credit note not posted in books, what is the fix?

Post the credit note to the correct period in books and ensure it appears in GSTR-1 Table 9B. Reduce the GSTR-3B outward tax in the same period. If the 3B was already filed, adjust in the next 3B and pay or reverse interest as applicable, with clear working papers for audit and any DRC-01B response.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.