Key takeaways

- Separate expense recognition from GST ITC: book costs with solid proof like POs, GRNs, and delivery challans, but defer ITC until the valid tax invoice appears in your GSTR-2B.

- Run a monthly missing invoice cadence covering GRN versus invoice checks, bank and card statement mapping, GSTR-2B reconciliation, and a live tracker with chase due dates to close gaps before they compound.

- Create provisional accruals for material items, reverse them on invoice receipt, and only then post the GST split and claim ITC, keeping maker checker logs for every entry.

- Adopt preventive controls such as GSTIN validation at vendor onboarding, mandatory POs, a central invoice inbox, and automated reminders to stop invoices from going missing in the first place.

- Align record retention to 8 years (the longest across GST, Companies Act, and Income Tax) and maintain audit evidence packs linking each provisional entry to its final resolution.

- Automate the heavy lifting with AI Accountant's GST reconciliation to detect gaps, reconcile GSTR-2B, flag bank transactions without bills, and cut days off your month-end close.

Missing invoice compliance in India: what's new in 2026

Until March 2025, e-invoicing was mandatory only for businesses with turnover above ₹5 crore. From April 2025, this threshold dropped significantly, pulling a much larger pool of SMEs into mandatory IRN generation. If your vendors recently crossed the threshold and are still issuing non-electronic invoices, those documents may not qualify for ITC. The practical fallout: more invoices rejected at the portal, more gaps in your GSTR-2B, and more chasing for your AP team.

The Invoice Management System (IMS) on the GST portal has also changed how GSTR-2B works. Previously, GSTR-2B was largely system generated. Now, taxpayers must actively validate and accept invoices through IMS before they flow into 2B. If you take no action within the prescribed window, invoices are auto-accepted, but mismatches slip through silently. This means your monthly reconciliation workflow now has an extra step: review IMS, accept or reject invoices, and then reconcile against your purchase register. Ignoring this step risks claiming ITC on invoices you should have disputed, or missing ITC on invoices you never reviewed.

The cost of inaction is concrete. Claiming ITC without the invoice appearing in GSTR-2B attracts interest at 18% per annum under Section 50, plus potential penalties under Section 122. The 180 day payment rule under Section 16(2) still applies: if you don't pay the vendor within 180 days of the invoice date, ITC must be reversed.

What to do now:

- Verify all active vendors against the updated e-invoicing threshold and confirm they are generating valid IRNs as per the GST e-Invoice portal.

- Add IMS review to your monthly close checklist before downloading GSTR-2B.

- Reconcile the purchase register against 2B by the 15th of each month, and chase supplier GSTR-1 filings for any missing invoices.

Teams using automated bookkeeping workflows can flag IMS mismatches and unmatched bank transactions in real time, cutting the manual effort that otherwise bogs down month-end close.

Why invoices go missing in India and their impact

E-invoicing thresholds create friction when vendors cross the turnover limit. IRN generation fails, HSN or SAC omissions trigger rejections, and wrong GSTIN entries block invoice uploads on the GST e-Invoice portal.

Outside e-invoicing, the reasons are more mundane. Emails land in spam. POs are missing so vendors do not know where to bill. GRN is done but the invoice is stuck in approval. Employees pay via cards without collecting GST bills. SaaS renewals fire silently. Foreign vendors miss Indian GST nuances entirely.

The impact is immediate. Month-end close slips as teams chase paperwork. Your GST ITC is at risk because claims require a valid tax invoice visible in GSTR-2B as mandated under Section 16 of the CGST Act. Management reporting shows gaps if expenses are not recorded.

Over time, ITC losses mount when employees pay vendors without the company GSTIN. Interest accrues on ineligible claims. Your GRNI (Goods Received Not Invoiced) ledger grows from unreconciled receipts.

Missing invoices are not just an AP headache. They are a compliance and cash flow problem that compounds every month you let them linger.

Risks and compliance stakes in India

GST Section 16 requires a valid tax invoice, supplier reporting in GSTR-1, and visibility in your GSTR-2B for ITC claims. Without the invoice, you must defer ITC to avoid interest at 18% per annum and penalties under Section 50 and Section 122 of the CGST Act.

TDS and TCS obligations continue on payment or credit. Documentation must back every deduction.

Retention rules span 72 months under GST, 8 years under the Companies Act, and 6 years under Income Tax. Align to the longest requirement, which is 8 years.

Auditors will flag unreconciled entries, expenses without GST compliant invoices, and weak documentation. The 180 day payment window under Section 16(2) adds another layer: if you have not paid the vendor within 180 days of the invoice date, ITC already claimed must be reversed and can only be reclaimed after payment.

What counts as acceptable proof of expense when the invoice is missing

When you lack the tax invoice, compile alternative documentation to substantiate the expense for P&L recognition.

Use POs, contracts, SOWs, delivery challans, GRNs, gate entries, vendor acknowledgement emails, and work completion certificates. Reinforce with payment evidence: bank statement entries, UPI confirmations, payment advice, vendor portal receipts, subscription renewal confirmations, and logistics LRNs.

Remember, this is valid for expense recognition and booking costs to your ledger. It is not valid for ITC, which must wait until the invoice hits GSTR-2B. No amount of alternative proof substitutes for the tax invoice when it comes to claiming input credit.

Month-end playbook: how to handle missing invoices during monthly accounting

Step 1: Identify the gaps systematically

Run unmatched transaction reports from your accounting system. Compare GRN registers against posted invoices. Scan bank and credit card statements for payments lacking bills. Review subscription renewals and recurring payments. Audit employee reimbursement claims for missing GST invoices.

Step 2: Collect and organize proof of expense

Attach available documents to each transaction. Maintain a Missing Invoice Tracker with these columns:

- Vendor name and GSTIN

- Invoice amount and tax split

- Transaction date

- Proof type available

- Chase due date

- Current status and resolution date

- Notes

This tracker becomes your single source of truth for chasing, accruing, and resolving gaps.

Step 3: Launch vendor follow up campaigns

Use standardized email and WhatsApp templates to request invoices. Ask explicitly for the e-invoice with IRN and QR code. Include your GSTIN. Confirm HSN or SAC codes. Set a clear deadline and mention that payment processing depends on receipt of the valid invoice.

Step 4: Create provisional entries

Post accrual entries via journal vouchers. Debit the expense and credit Accrued Liabilities or GRNI. Do not book GST at this stage.

When the invoice arrives, reverse the accrual, post the vendor bill with the GST split, and claim ITC only after verifying it in GSTR-2B.

For mechanics and examples, see AP accruals and reversals.

Step 5: Handle GST compliance carefully

Flag entries where ITC is deferred. Track them separately in an ITC deferral register. Only claim ITC after the invoice appears in 2B and you have validated it through IMS. Monitor amendments or credit notes that change prior period deferrals.

Step 6: Apply cut off and materiality thresholds

Define thresholds for petty transactions. Specify write off timelines, for example 3 months for amounts under ₹5,000. Require documented approvals for any write off. This keeps your tracker clean and prevents immaterial items from clogging reconciliation.

Step 7: Document everything for audit readiness

File all proof. Update the tracker weekly. Create evidence packs for each provisional entry. Keep version control. Draft reconciliations showing the path from provisional to final entries.

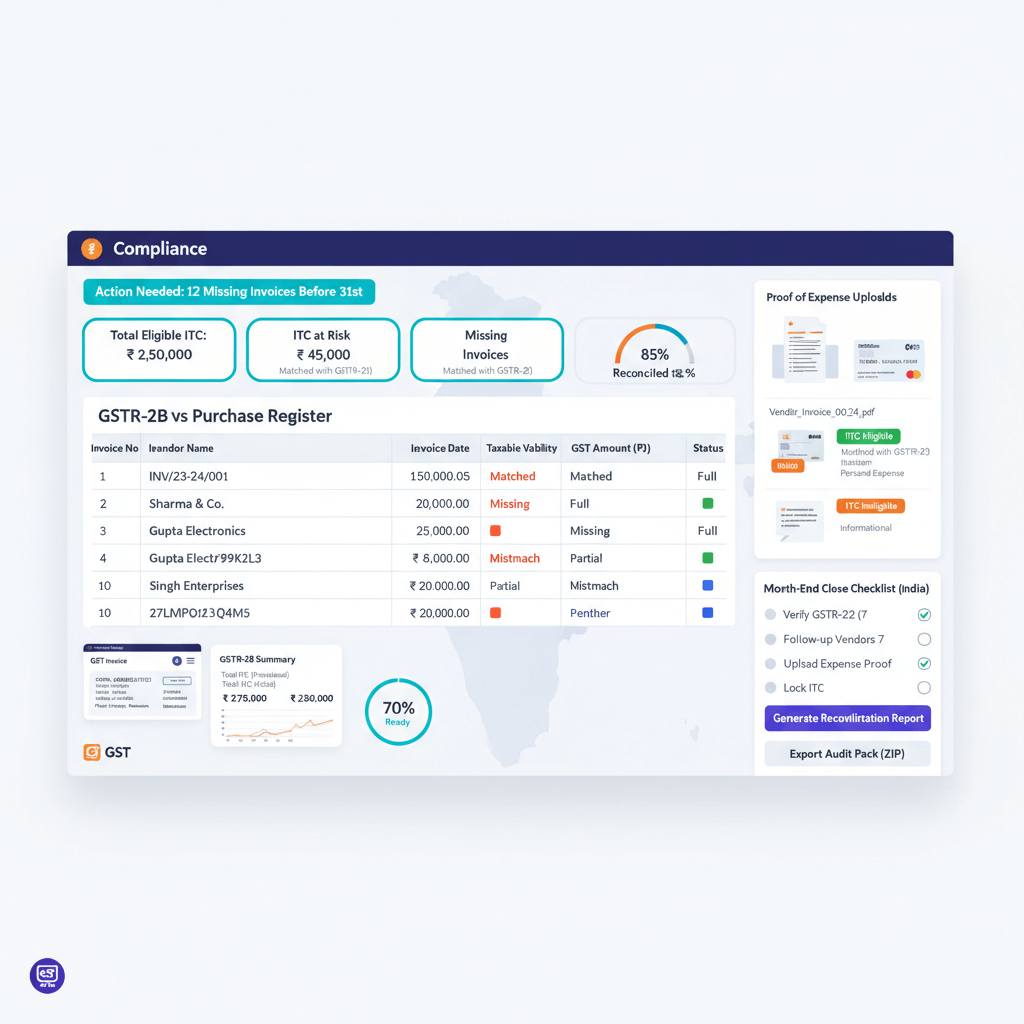

Reconciliation with GSTR-2B: solidifying ITC

Download GSTR-2B when it publishes, after reviewing and accepting invoices in IMS. Then perform a line by line match to your purchase register.

For methods and tooling, review this GSTR-2B reconciliation tools guide.

Compare GSTINs, invoice numbers and dates, taxable values, tax amounts, and POs where available. Classify results into these buckets:

- Matched

- Missing in 2B (supplier has not filed GSTR-1)

- Mismatches in value or tax amount

- Prior period amendments

Take action quickly. Chase vendors to file GSTR-1 for invoices missing in 2B. Defer ITC until visible. Process credit notes correctly. Prepare RCM self invoices where applicable. Handle imports via Bill of Entry.

Keep detailed reconciliation worksheets with comments, follow up actions, and aging on unreconciled items. As per CGST Rule 36(4), ITC claims must align with GSTR-2B data. Any excess claim invites scrutiny.

Bank and card statement mapping to catch missing invoices

Ingest bank and credit card statements monthly. Flag every transaction without a matching bill or vendor invoice.

Usual suspects include SaaS subscriptions, utility payments, insurance premiums, and professional services. For each unmatched item:

- Determine the expense nature

- Request invoices or receipts from the vendor

- Confirm if it is personal spend on company cards

- Validate FEMA aspects for foreign currency payments

- Assess RCM on service imports

Create a follow up loop. Email vendors with payment details and invoice requests. Enable vendor portal auto download. Set mailbox rules to capture subscription invoices. Train employees to submit receipts immediately after any card based purchase.

Audit readiness India: what auditors expect

Auditors look for a defined SOP, a current tracker, and three way matching between PO, GRN, and invoice.

At period end, they expect:

- GRNI aging reports

- Vendor statement reconciliations

- Monthly 2B versus purchase register tie outs

- Bank to expense linkages

Documentation makes or breaks your review. Align retention to the longest rule (8 years). Maintain version control for provisional entries and reversals. Keep maker checker logs. Build evidence packs showing identification to closure for every missing invoice item.

The ICAI Standards on Auditing emphasize that sufficient appropriate audit evidence must exist for every material assertion. Provisional entries without supporting documentation will attract qualifications.

Preventive controls to reduce missing invoices

Improve vendor onboarding. Validate GSTINs against the GST portal's taxpayer search. Confirm e-invoice readiness for eligible vendors. Set TDS sections and rates. Maintain billing contacts with escalation matrices.

Enforce purchase discipline. Mandate POs for all purchases above a defined threshold. Use a central invoice inbox. Enforce required fields in your accounting system so incomplete entries cannot be saved.

For simple automation on bill capture from email, explore email to ledger capture.

Strengthen employee expense policies:

- Mandatory receipts for reimbursement

- Expense tools with receipt capture at point of purchase

- Corporate cards with spend controls

- Monthly submission deadlines

- Routine vendor reconciliations

Light touch tooling to streamline

Automation accelerates detection and resolution. Bulk ingestion processes hundreds of bills. GSTIN validation runs automatically. Bank reconciliation highlights missing invoices. Dashboards show missing invoice aging and deferred ITC at a glance.

- AI Accountant for Indian businesses: automates bill extraction, detects GSTIN mismatches, flags bank transactions without bills, performs PO matching, tags missing invoices, reconciles GSTR-2B with ITC deferral tracking, and provides audit ready dashboards syncing with Tally.

- QuickBooks: automated invoice tracking and reminders with vendor management features. GST workflows may require localization for India specific compliance.

- Xero: strong bank feeds and invoice capture. Limited native 2B reconciliation for India.

- FreshBooks: effective expense and receipt capture on mobile. Lacks e-invoicing and IRN features.

- Zoho Books: native Indian GST and GSTR filing. Manual effort may be needed for missing invoice chase and vendor follow up.

Practical artifacts

Missing Invoice Tracker template

Create columns: Vendor Name, GSTIN, Invoice Amount, Tax Amount, Transaction Date, Proof Type Available, Chase Due Date, Current Status, Resolution Date, Notes.

Vendor follow up email template

Subject: Urgent: Missing Invoice for [PO or GRN Reference]

Dear [Vendor Contact],

We are following up on the missing invoice for our transaction dated [Date] for ₹[Amount]. Our records show goods or services delivered, but we have not received the GST invoice.

Please share the e-invoice with IRN and QR code at the earliest. Our GSTIN is [Your GSTIN]. Ensure correct HSN or SAC codes.

This is critical for GST compliance and payment processing. Please send the invoice by [Deadline] to avoid payment delays.

Regards,

[Your Name]

Sample journal entries

Provisional accrual entry:

Dr. Computer Expenses ₹1,00,000

Cr. Accrued Liabilities ₹1,00,000

(Being expense accrued for services received from ABC Vendor, invoice pending)

Reversal and actual bill posting:

Dr. Accrued Liabilities ₹1,00,000

Cr. Computer Expenses ₹1,00,000

(Being reversal of accrual on receipt of invoice)

Dr. Computer Purchases ₹90,000

Dr. CGST Input ₹5,000

Dr. SGST Input ₹5,000

Cr. ABC Vendor ₹1,00,000

(Being bill posted with GST on tax invoice INV-2024-1234)

Month end checklist for missing invoices

- Run unmatched transactions report

- Generate GRN versus invoice reconciliation

- Review bank and card statements for unbilled payments

- Update the Missing Invoice Tracker

- Attach proof of expense for each missing invoice

- Send vendor follow ups with IRN and QR requirements

- Post provisional entries for material items

- Review and accept invoices in IMS before downloading GSTR-2B

- Complete GSTR-2B reconciliation by the 15th

- Update the ITC deferral tracker

- Review and approve any write offs per policy

- Archive documentation into evidence packs

Moving forward with confidence

Missing invoices need not derail your close. Recognize expenses with robust proof. Defer ITC until invoices appear in GSTR-2B. Maintain airtight documentation.

Implement the tracker today. Deploy vendor templates. Define provisional entry policies. Train your team. Consider automation such as AI Accountant to cut manual work and accelerate resolution.

Resolve a gap today, avoid a compliance issue tomorrow.

FAQ

Can we recognize an expense without an invoice, and how should we document it for audit?

Yes, you can recognize expenses with strong alternative proof such as POs, GRNs, delivery challans, vendor email confirmations, and bank proof. Keep an evidence pack combining proof, approvals, and reconciliation notes. GST ITC must be deferred until the valid tax invoice appears in GSTR-2B, as no provisional ITC is allowed without 2B visibility (2026 update).

Can we claim GST ITC without an invoice if we have proof of expense and payment?

No. ITC requires a valid tax invoice reported by the supplier in GSTR-1 and visible in your GSTR-2B after validation through the Invoice Management System. Use alternative proof to book the expense in your P&L, but wait to claim ITC until the invoice surfaces in 2B. Claiming without 2B visibility attracts 18% interest under Section 50.

What is a sensible write off timeline for small missing invoices in an SME environment?

CA firms often propose materiality based cut offs: write off after 3 months for amounts under ₹5,000, and 6 months for larger amounts, subject to management approval. Keep your tracker updated and document follow ups before writing off.

How should we handle unregistered vendors and RCM cases during month end?

Unregistered vendors cannot issue GST invoices, so standard ITC is not available. For RCM eligible services, issue a self invoice, pay GST under reverse charge, and claim ITC subject to eligibility. Maintain self invoices and payment challans in your evidence pack.

What is the recommended cadence for GSTR-2B reconciliation to protect ITC?

Download 2B on the 14th after reviewing invoices in IMS, complete reconciliation by the 15th, chase supplier GSTR-1 filing for missing items, and defer ITC on anything not yet visible. Maintain an ITC deferral register with aging and resolution notes. The IMS now requires active validation before invoices flow into 2B, so add that review step to your monthly cadence (2026 update).

How do we deal with foreign SaaS invoices, RCM, and FEMA aspects?

Foreign SaaS typically falls under import of services. Raise a self invoice, pay IGST under RCM, and claim ITC if eligible. Ensure correct SAC, maintain bank remittance documents, and comply with FEMA paperwork for cross border payments. The 180 day payment rule under Section 16(2) applies here too: ITC must be reversed if payment is not made within the window.

What is the 180 day payment rule and how does it affect missing invoices?

Under Section 16(2) of the CGST Act, if you do not pay the vendor within 180 days of the invoice date, any ITC already claimed must be reversed. It can only be reclaimed after actual payment. For missing invoice situations, this means even after you receive and book the invoice, the clock on the 180 day window started on the original invoice date, not the date you received it. Track payment timelines alongside your missing invoice tracker to avoid surprise reversals.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.