Key takeaways

- Bookkeeping equals capture and coding, bills and bank and basic matching, while accounting equals controls and decisions, reconciliations, provisions, and compliance review.

- Manual bookkeeping creates avoidable waste, about 2.3% coding errors and 7 minutes per invoice, which becomes 58 hours monthly for 500 bills.

- Automate high volume, low judgment tasks first, AP ingestion, bank coding, GSTR-2B matching, keep human review for exceptions and adjustments.

- Redesign roles around automation, bookkeepers handle exceptions, accountants drive close quality, controllers sign off on MIS and compliance.

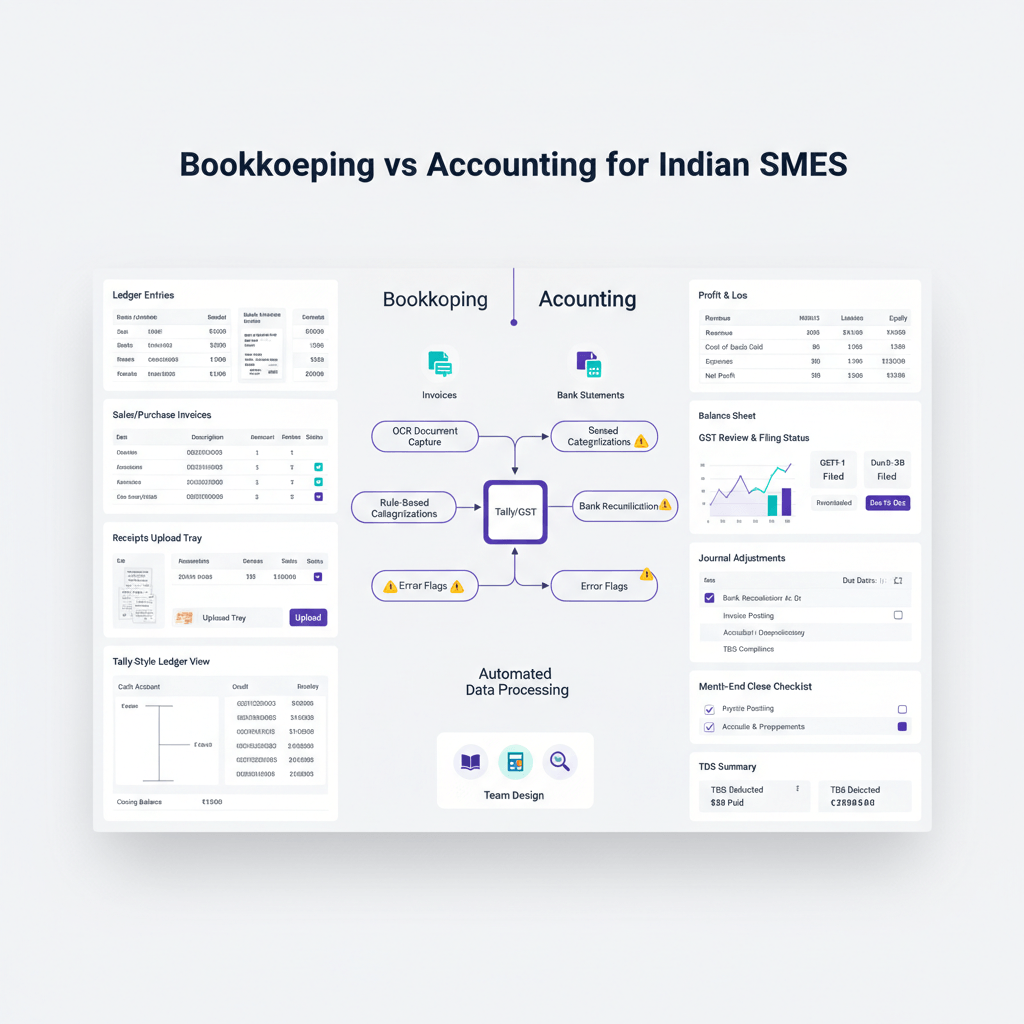

Bookkeeping vs accounting, the short answer for Indian SMEs

Bookkeeping vs accounting is not about job titles, it is about workflow design. Bookkeeping captures and codes transactions, accounting applies judgment for reconciliations, provisions, and compliance decisions. Automation now handles the mechanical parts better than people, so accountants should review exceptions, not type vouchers.

ICAI distinguishes the two clearly in the ICAI Intermediate Accounting Study Material, which frames bookkeeping as mechanical recording, and accounting as analysis and interpretation. Books must be retained for eight years per MCA Companies Act 2013, accuracy and accessibility matter more than who keyed the data.

What belongs to bookkeeping, and what stays with accounting

Bookkeeping tasks, capture and classify

- Bill and invoice data extraction from PDFs or images

- Vendor and ledger coding for purchases and expenses

- Bank and credit card transaction categorisation

- GSTR-2B download and basic invoice matching

- Recurring journals and routine allocations

- Document storage and indexing

Accounting tasks, control and decide

- GSTR-2B versus purchase register reconciliation with ITC adjustments

- Journal vouchers for provisions and accruals

- TDS and TCS applicability review and tracking

- Financial statement preparation and sign off

- MIS, ratio analysis, variance commentary

- Statutory audit coordination and schedules

Bottom line: bookkeeping is process, accounting is judgment. Design your month end around this split.

Timing matters. GSTR-2B is generated on the 14th based on supplier activity till the 12th per the GSTN Portal Guide. Complete AP coding by the 15th so accountants have five days for reconciliation before GSTR-3B filing on the 20th. If you cross the e‑invoicing threshold per CBIC Notification 10/2023-CT, treat IRN validation as a bookkeeping checkpoint, and compliance interpretation as an accounting decision.

What bookkeeping includes in India, and what accounting should keep

Bookkeeping owns, automate these

- AP processing: extract bill data, detect vendors, map to ledgers, check duplicates

- Bank coding: ingest statements, auto categorise, suggest GST treatment

- Credit card reconciliation: match receipts to statements, allocate to cost centres

- GSTR-2B ingestion: download, parse line items, prepare for matching

- Master maintenance: update vendor details, GSTIN and PAN verification

- Document management: store bills, link vouchers, maintain audit trail

Accounting keeps, human judgment required

- 2B reconciliation: review mismatches, adjust ITC, handle blocked credits

- Month end provisions: accruals, depreciation, bad debts

- TDS compliance: applicability, computation, certificates and reporting

- Financial review: margin checks, unusual transactions, approvals

- MIS preparation: dashboards, variances, cash flow outlook

- Statutory coordination: audit schedules, queries, returns

Plan the handoff around statutory dates. Your AP and bill automation should push draft vouchers into Tally by mid month, then accountants complete GSTR-2B reconciliation and month end close.

The cost of getting the boundary wrong

Time drain on skilled resources

Manual invoice entry takes 7 minutes per document per the ICAI SMP Practice Guide. For 500 invoices, that is about 58 hours. Bank coding typically takes 3 minutes per line, see NASSCOM FinTech Report 2023, which adds another 50 hours for 1,000 transactions. That is more than a hundred hours of skilled time used for typing, not analysis.

Error rates that cascade

Manual data entry has a 2.3% coding error rate per the ICAI DAAB Technical Guide. A dozen wrong ledgers each month can break GSTR-2B matching, HSN reporting, and MIS integrity. Each error costs additional time during reconciliation.

Compliance penalties from delays

Late GSTR-3B filing costs add up per CBIC Notification 13/2022, and wrong ITC claims attract 18% annual interest under Section 50 of the CGST Act. Scrutiny can trigger penalties from ₹10,000 up to the tax amount. RBI data shows typical SMEs process 500 to 2,000 invoices and 1,000 to 5,000 bank transactions monthly, see RBI MSME Pulse 2024, which makes manual handling impractical.

What to automate first, a Tally first framework

Phase 1, high volume capture

- AP and bills automation: OCR for PDFs, vendor detection, ledger prediction

- Bank statement ingestion: portal fetch or upload, rule based categorisation

- Credit card reconciliation: receipt matching, cost centre allocation

Start here because rules are clear and volumes are high. Once documents flow into Tally with high accuracy, your team moves from data entry to exceptions.

Phase 2, compliance matching

- GSTR-2B reconciliation: auto match invoices, flag mismatches for review

- TDS applicability checks: vendor thresholds, section wise rules

- E‑invoice status tracking: IRN validation and cancellations

GSTR-2B reconciliation at scale needs automation for matching and a human for adjustments. The handoff is critical, automation identifies, accounting decides.

Phase 3, multi entity scale

- Inter company reconciliation: auto match across entities

- Consolidated reporting: roll up MIS without rekeying

- Entity specific learning: improve predictions from history

For CA firms and groups, multi org support keeps books separate while allowing shared oversight.

Design the handoff carefully. Automated capture pushes draft vouchers in Tally, see automate vendor bill entry in Tally. Accountants review exceptions such as new vendors, unusual amounts, or tax code changes. Set thresholds, for example auto post transactions under ₹10,000 and flag anything above for review. Track the review queue daily.

AI Accountant runs this workflow for hundreds of Indian companies. Bills and bank statements are ingested, vendors and ledgers are predicted from history, and clean data syncs back to Tally Prime. Controllers see exceptions, make adjustments, and post with confidence, no parallel books, no data silos.

Team design and KPIs, staff for throughput not typing

Redefined roles

- Bookkeeping ops, about one per ten thousand transactions, handle exceptions, vendor masters, and documents

- Accountant, about one per three to five entities, owns reconciliations, provisions, compliance, and MIS

- Controller, about one per hundred crore revenue, signs off close, reviews variances, coordinates audit

KPIs that matter

- Time from document to draft voucher: under two hours

- Auto classification accuracy: above eighty five percent

- GSTR-2B match rate: above ninety five percent

- Days to close books: five to seven days

- Exceptions per thousand transactions: under fifty

- Rework rate after posting: under one percent

For CA portfolios, add entity level on time close and exceptions per client. Receivables and Payables dashboards should update in real time as transactions post. Measure improvement monthly and adjust review rules if metrics stall.

Tool selection criteria, Tally first and compliance grade

Tally Prime integration

- Two way sync, masters from Tally and transactions back to Tally

- No parallel ledgers, Tally remains the source of truth

- Voucher types, cost centres, and tracking preserved

Your Tally Prime sync should be real time, not import export cycles.

India compliance depth

- Native GSTR-2B parsing, supplier GSTIN and tax rate understanding

- ITC eligibility logic, Section 16 and blocked credit rules

- TDS tracking, Section 194Q and certificate management

- E‑invoice awareness, IRN validation and changes

Scale architecture

- Multi entity by design with combined reporting

- Entity specific learning for vendor patterns

- Bulk processing without slowdown

- Smart review queues by value, due date, and exception type

Security and compliance

- ISO 27001 and SOC 2 Type II

- India data residency

- Complete audit logs

Never compromise on security. Verify certifications independently and review audit logs regularly.

Conclusion

The bookkeeping and accounting split is practical, not academic. Get the boundary right and you unlock faster closes and cleaner compliance.

Focus on three moves: automate capture and coding, invest human time in controls and decisions, and track metrics that reflect cycle time and quality. Do this and month end becomes a routine, not a fire drill.

FAQ

What is the practical difference between bookkeeping and accounting for Indian SMEs, in one line?

Bookkeeping captures and codes transactions, while accounting applies judgment for reconciliations, provisions, and compliance. ICAI’s framing in the ICAI Intermediate Accounting Study Material reinforces this separation.

For a ₹10 crore trading company on Tally, do I hire a bookkeeper or an accountant?

Hire an accountant and automate bookkeeping. Manual entry for 500 invoices and 1,000 bank lines consumes about 108 hours monthly per ICAI SMP Practice Guide and NASSCOM. Use an AI tool like AI Accountant for capture and coding, and let the accountant focus on GSTR-2B reconciliation, provisions, and compliance.

How should a CA firm split tasks between junior staff and seniors across 20 SME clients?

Put juniors on exception handling from automation, vendor master upkeep, and document control. Seniors should own reconciliations, TDS reviews, and MIS sign off. AI Accountant can route exceptions by value and due date, which helps seniors focus on material items.

Which bookkeeping tasks in Tally Prime give the fastest ROI if automated first?

AP bill capture, bank statement ingestion, and credit card reconciliation. Once these flow to draft vouchers, move to GSTR-2B matching. Tally supports import and reconciliation workflows, see Tally documentation. AI Accountant plugs in for two way sync and review queues.

How do I handle GSTR-2B reconciliation, can AI really manage the nuances?

AI can auto match invoices, flag mismatches, and identify blocked credits under Section 16, but a human should clear exceptions and make ITC decisions. Refer to the CGST Act for eligibility rules. AI Accountant’s GSTR-2B module highlights supplier filing gaps and RCM cases for quick review.

What compliance dates should drive the bookkeeping to accounting handoff each month?

Use the 14th GSTR-2B generation per the GSTN Portal Guide as your AP coding deadline, then give accountants five days for reconciliation before GSTR-3B on the 20th. With AI Accountant, AP drafts should be ready by the 15th.

For a ₹50 crore manufacturing client with e‑invoicing, where does IRN validation sit?

Bookkeeping validates uploads and captures IRN and QR data, accounting ensures compliance treatment for cancellations and amendments. Follow CBIC notifications for thresholds. AI Accountant surfaces missing or cancelled IRNs before posting.

How much can we realistically cut the month end close with automation on Tally?

SMEs moving AP and bank coding to AI typically compress closes to five to seven days. With 85% plus auto classification and a shrinking exception queue, AI Accountant users see faster MIS without sacrificing control.

What KPIs should a controller track to prove quality and speed improvements?

Document to draft voucher time, auto classification accuracy, GSTR-2B match rate, days to close, exceptions per thousand transactions, and rework rate post posting. AI Accountant dashboards track these across entities.

Is it safe to keep financial data in an AI tool, what certifications should we look for?

Look for ISO 27001, SOC 2 Type II, India data residency, and complete audit logs. Never bypass Tally as the system of record. AI Accountant maintains Tally as the source of truth with traceable sync and logs.

Can we auto post small value transactions and only review large or unusual entries?

Yes. Set thresholds, for example auto post under ₹10,000 with matching vendor and tax logic, and route exceptions to review. AI Accountant supports value based rules and anomaly detection.

What is the cleanest way to explain bookkeeping vs accounting to promoters who conflate both?

Say this, bookkeeping captures data quickly and accurately so accounting can ensure compliance and insight. Use a simple example, AI Accountant posts bills and bank in hours, your accountant then reconciles GSTR-2B and signs off MIS, which avoids interest and penalties.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.