Key takeaways

- Categorize every UPI transaction by business purpose (rent, supplies, utilities), not by payment method, this single habit fixes most reconciliation headaches and keeps your P&L accurate.

- Record gross amounts, fees, and settlements as separate line items: netting hides costs, breaks GST claims, and misleads cash flow reports.

- Set up dedicated ledgers (UPI clearing, wallet assets, gateway fees, Owner's Drawings) during Week 1, a clean chart of accounts makes daily categorization almost automatic.

- Capture UTR numbers, GSTINs, invoice details, and tax breakups for every transaction, this is non‑negotiable for audit defence and ITC eligibility.

- Daily five‑minute reconciliation prevents month‑end firefighting: match UPI debits to ledger entries and UTRs before they pile up.

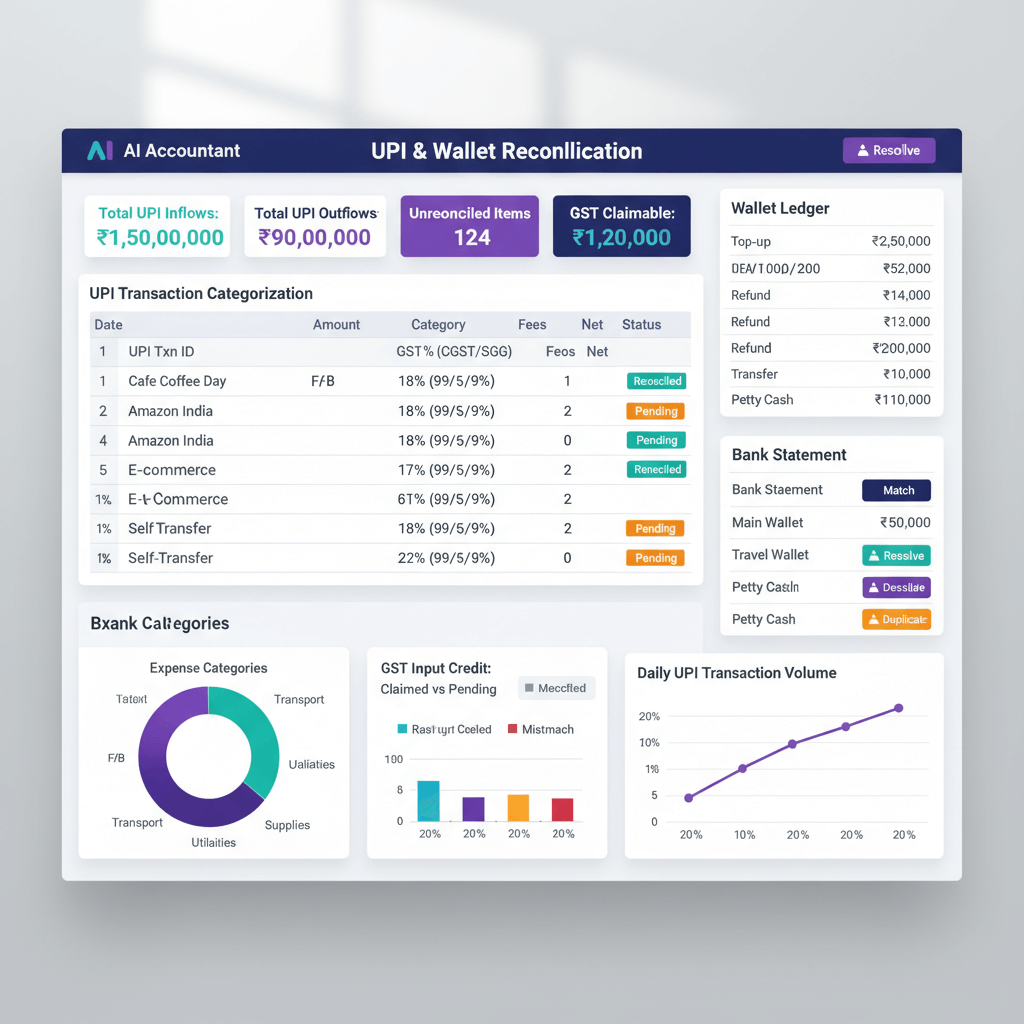

- High‑volume UPI and wallet entries are error‑prone when coded manually. AI Accountant's bookkeeping automation ingests statements, predicts categories, and auto‑matches settlements so your team focuses on exceptions, not data entry.

UPI and wallet accounting rules: what's new in 2026

Until March 2025, most UPI settlements followed a T+1 cycle. From April 2025, NPCI's phased rollout of near‑real‑time settlement for merchant transactions means many businesses now see funds hit their bank account within minutes, not the next business day. This compresses the window your UPI clearing account carries a balance and demands tighter same‑day reconciliation routines. If your workflow still assumes overnight settlement, clearing account balances will look wrong by morning, and your dashboards will lag reality.

The RBI's Master Direction on Payment Aggregators and Payment Gateways now requires all PAs to maintain a net‑worth of ₹25 crore (up from ₹15 crore until March 2025). For finance teams, this means fewer fringe aggregators in the market and more standardised settlement file formats, but you still need to validate that your aggregator's reports match the new escrow and settlement norms.

On the GST front, the e‑invoicing threshold dropped to ₹5 crore aggregate turnover from August 2023, and GSTN's Invoice Management System (IMS) now lets buyers accept or reject invoices directly on the portal before GSTR‑2B is generated. This means your purchase register must reconcile to IMS actions monthly, not just to GSTR‑2B. Miss an acceptance window and your ITC for that period is blocked until the next cycle.

Who does this hit hardest? CA firms managing 20+ clients on Tally, and SME finance teams processing more than 500 UPI transactions a month. The operational shift is real: you need same‑day statement ingestion, automated UTR matching, and IMS‑aware GST reconciliation. Platforms built for automated GST reconciliation absorb these new steps without adding headcount.

What to do now:

- Switch your UPI clearing account reconciliation from next‑day to same‑day, or configure alerts for settlement delays beyond 30 minutes.

- Verify your payment aggregator's PA licence status and confirm settlement file formats align with current RBI norms.

- Start reconciling purchases against IMS actions on the GST portal monthly, not just GSTR‑2B, before your next filing deadline.

UPI categorization matters more than ever

UPI has become the default rail for Indian retail payments. Your customers pay via QR, your vendors accept UPI, and your team reimburses expenses digitally.

When categorization is sloppy, GST credits vanish, personal and business expenses mix, bank reconciliation derails, and your P&L turns into fiction.

The fix is straightforward: standardize your approach to UPI payments accounting, document rules, and reconcile consistently. According to NPCI's UPI product statistics, monthly UPI transaction volumes now exceed 16 billion, meaning even small businesses face hundreds of digital entries each month.

Pro tip: Categorize by business purpose, not by payment method. UPI is how you paid, not what you paid for.

Understanding UPI, wallets, and payment aggregators

UPI transactions

UPI moves money instantly between bank accounts, whether via UPI IDs or QR codes. There is no float with a middleman, so you record the expense or revenue directly with bank movement and the UTR reference.

Digital wallets

Wallets hold prepaid balances. A top‑up creates an asset transfer, not an expense. The expense is recognized when the wallet balance is spent. Always track both legs (top‑up and spend) with transaction IDs.

Payment aggregator settlements

Aggregators batch collections, deduct fees, and settle net to your bank. You must record gross sales, explicit fees, and settlement to the UPI clearing account, then reconcile to the bank on settlement day.

For deeper context, explore the RBI's framework for payment aggregators and Stripe's overview of Unified Payments Interface.

Setting up your chart of accounts for digital payment success

Your chart of accounts is the backbone of UPI payments accounting. Clarity here simplifies categorization and reconciliation.

- UPI Clearing Account: track aggregator collections until they settle to bank.

- Wallet Asset Accounts: one per wallet, treat balances like petty cash.

- Payment Gateway Fee Account: record MDR and taxes separately for visibility and GST claims.

- Cashback and Promotional Income: keep cashbacks as other income. Do not net against expenses unless policy demands.

- Owner's Drawings: route personal spends paid via business UPI here.

Add cost centers or tags for branches or projects. This yields better reporting without proliferating ledgers.

The complete rules for categorizing UPI transactions

Rule 1: vendor bill payments via UPI

Link the payment to the vendor bill or vendor invoice. Capture the UTR, post to the correct expense ledger with GST breakup, and tie supporting documents. Use payment matching of unreconciled bills to avoid loose ends.

Rule 2: customer collections via UPI QR

Record gross sales. Record gateway fees separately. Track net settlement to UPI clearing, then to bank on settlement.

Rule 3: inter‑bank transfers

Contra entries only. Transfers between your accounts are asset movements, not income or expense.

Rule 4: wallet top‑ups are not expenses

Debit wallet asset, credit bank. The expense is recognized when the wallet balance is spent.

Rule 5: wallet spends require documentation

Record the actual expense category. Attach bills. Capture GST where applicable. Wallet is a payment method, not a category.

Rule 6: cashbacks and rewards

Record cashbacks as other income for transparency and audit trails. Only net if your policy explicitly allows.

Rule 7: refunds and reversals

Link refunds to the original transaction. Reverse the ledger entry appropriately. Avoid orphaned credits.

Rule 8: split transactions

Split UPI payments that cover multiple items. Do not dump mixed purchases into a single bucket. For example, an Amazon order covering both office equipment and cleaning supplies should be split into two ledger entries.

Rule 9: personal expenses via business UPI

Route to Owner's Drawings. Keep business categories clean.

Rule 10: employee reimbursements

Record as employee advance first, then expense on submission. Claim GST if the invoice has company name and GSTIN.

Rule 11: payment aggregator batch settlements

Show gross collections. Show fees. Reconcile daily. Use settlement file parsing for gateways to speed matching.

Normalizing UPI and wallet feeds for consistent data

Every payment app, bank, and aggregator exports data in a different format. Column names differ, timestamps vary, and status labels are inconsistent. Before you can categorize or reconcile, you need a single, clean schema.

- Standardize status values: map every variant ("Success", "COMPLETED", "Paid") to one vocabulary: success, failure, pending.

- Harmonize PSP handles: treat @okicici, @ybl, @paytm, and similar suffixes as equivalent when matching payer identity.

- Normalize VPAs: lowercase everything, strip gateway suffixes, and handle bank‑specific quirks so the same vendor doesn't appear as three different entries.

- Use reliable identifiers first: match on UTR or RRN and exact VPA before layering fuzzy signals like amount plus date matching with confidence scoring.

- Account for settlement timing: T+1 for most UPI (moving toward real‑time in 2026), T+2 for some wallets, and instant for UPI Lite under ₹500.

Tag UPI Lite transactions at ingestion by instrument code or narration patterns provided by banks. Expect instant settlement with no T+1 lag, and isolate them into a separate reconciliation stream.

Capturing the right data for audit and GST compliance

Every UPI transaction has a UTR. Every wallet transaction has an ID. Every QR collection has a reference.

Store these along with vendor name, GSTIN, invoice number, and tax breakup. Attach screenshots, PDFs, settlement reports, and receipts without fail. This demonstrates business purpose and supports GST claims when scrutiny arises.

Under the GST portal's Invoice Management System, buyers now need to accept or reject invoices before GSTR‑2B generation. Ensure your purchase register aligns with IMS actions every month.

Building robust reconciliation workflows

Daily bank reconciliation is non‑negotiable. Match UPI debits and credits to ledger entries and UTRs.

Reconcile wallet statements monthly. Verify top‑ups, spends, and cashbacks to the wallet ledger.

For aggregators, match three data points:

- Collections on the aggregator dashboard (gross)

- Fees from the MDR and tax reports

- Net settlements in the bank statement

Clear exceptions promptly: duplicates, failed transactions, or pending entries. With near‑real‑time UPI settlement now rolling out, same‑day matching is becoming the new standard.

Daily rhythm beats month‑end firefighting. Five minutes of matching now prevents hours of cleanup later.

GST considerations for digital payments

Claim input tax credit only with valid tax invoices in the business name, with GSTIN and correct tax details. UPI payment confirmations are not tax invoices.

Payment gateway fees generally include GST. Capture and claim it. Small amounts add up: a business processing ₹10 lakh monthly through an aggregator at 2% MDR pays ₹20,000 in fees, and the GST on that fee (₹3,600 at 18%) is recoverable ITC.

Watch RCM (reverse charge mechanism) services and self‑assess GST where applicable. Reconcile purchases to GSTR‑2B monthly, and now also verify IMS acceptance status on the GST portal to ensure credits are not blocked.

Automation tools and technologies

Manual coding for hundreds of UPI and wallet entries is error‑prone. Automation ingests statements, predicts categories, applies GST treatments, and auto‑matches settlements.

- AI Accountant: ingests bank, wallet, and aggregator data in PDFs, CSVs, or scans. Predicts categories with confidence scoring (above 90% auto‑post, 60 to 90% queue for review, below 60% manual). Links payments to bills with audit‑ready references and syncs to Tally.

- QuickBooks: strong bank feeds and rules for recurring transactions.

- Xero: machine learning suggestions for coding and reconciliation.

- Zoho Books: banking automation with India‑friendly workflows.

- FreshBooks: receipt scanning and smart categorization.

- Tally Prime: bank statement imports and semi‑automated reconciliation for Indian banks.

Bulk operations and learned patterns reduce effort. Categorize recurring vendors quickly, split mixed purchases, and auto‑link payments to bills to shrink close times.

Set confidence thresholds so your automation tool handles the routine volume while your team reviews only the exceptions. This keeps models robust and reduces manual effort without overfitting rules.

Decision making improves when dashboards reflect reality, not netted or miscategorized numbers.

Implementation checklist for small businesses

Week 1: foundation setup

Create UPI clearing, wallet asset, and fee ledgers. Set vendor and customer masters with UPI IDs and GSTINs.

Week 2: process definition

Document categorization rules, cashback handling, and personal expense adjustments. Build templates for frequent payments like rent, SaaS subscriptions, and utility bills.

Week 3: reconciliation rhythm

Establish daily bank reconciliation, weekly wallet checks, and monthly aggregator matching. Consistency beats complexity.

Week 4: compliance and controls

Define GST document standards, storage, and responsibilities. Add approvals for large UPI spends (for example, anything above ₹10,000 requires senior sign‑off). Set escalation for exceptions.

Common mistakes and how to fix them

- Recording wallet top‑ups as expenses: fix with asset transfer entries and expense on spend.

- Netting away payment gateway fees: fix by recording gross revenue and explicit fee expense for visibility and GST claims.

- Missing GST invoices for UPI payments: fix by insisting on proper tax invoices. UPI confirmations are not invoices.

- Treating intra‑bank transfers as income: fix with contra entries only.

- Unlinked refunds: fix by reversing original entries and tying credits to source transactions.

- Dumping all UPI spends into one bucket: fix by categorizing by business purpose: rent, supplies, utilities, and more.

- Mixing personal and business spends: fix by routing to Owner's Drawings and keeping categories clean.

- Ignoring UPI Lite transactions: these settle instantly with no T+1 lag. Tag them at ingestion and reconcile separately to avoid mismatches.

Moving forward with confidence

When you master categorizing UPI transactions, month‑end is faster, GST filings are calmer, and cash flow reports become reliable.

Start with chart of accounts, rules, and reconciliation. Then layer in automation. The result is cleaner books and better decisions.

Your digital payments volume will grow. Build the right foundation now. Avoid painful cleanups later.

FAQ

How should a CA record PhonePe and Google Pay customer collections to ensure gross revenue and fee visibility?

Record the full collection as sales, post MDR or gateway fees to a dedicated expense ledger, and use a UPI clearing account to hold collections until the net settlement hits bank. For example, on a collection of ₹50,000 with fees of ₹150, post sales at ₹50,000, fees at ₹150, and clear ₹49,850 to bank on settlement day.

What is the correct treatment for wallet top‑ups and subsequent spends in Tally?

Treat top‑ups as asset transfers: debit Wallet Asset, credit Bank. The expense is recognized only when the wallet balance is spent. Record the actual expense category at spend time, attach the invoice, and capture GST details. Maintain transaction IDs for both legs to ease reconciliation and audits.

How do I reconcile UPI QR settlements when aggregator reports show daily batches but the bank settles net amounts?

Match three data points: aggregator dashboard for gross collections, fee report for MDR and taxes, and bank statement for net settlements. Use a UPI clearing account to bridge timing differences. With near‑real‑time UPI settlement rolling out in 2026, check whether your aggregator has shifted from T+1 to same‑day cycles and adjust your reconciliation window accordingly (2026 update).

What documentation should I capture for GST input tax credit when paying vendors via UPI?

Collect a valid tax invoice in the business name with GSTIN, supplier GSTIN, invoice number, and tax breakup. Store UTR references, payment confirmations, and invoice PDFs together. From 2026, also verify that the invoice has been accepted in GSTN's Invoice Management System before your GSTR‑2B is generated, otherwise ITC may be blocked for that period (2026 update).

How can an SME finance team automate categorization for high‑volume UPI transactions without overfitting rules?

Combine base rules for common vendors and amounts with machine learning predictions that learn patterns over time. Use confidence thresholds: auto‑post above 90%, queue for review between 60 and 90%, and classify manually below 60%. This keeps models robust while reducing manual effort as transaction volume grows.

Should cashbacks from UPI wallets and aggregators be netted against expenses or shown as other income?

Show cashbacks as other income for transparency, unless your documented accounting policy explicitly mandates netting. This approach clarifies profitability analysis, preserves audit trails, and ensures small amounts that compound over time remain visible in your books.

What is the recommended approach to refunds and reversals for UPI purchases, including partial returns?

Link every refund to the original transaction and reverse the expense entry appropriately. For partial returns, split the original transaction into components, reverse only the relevant part, and adjust GST input where necessary. Attach supporting documents and references to maintain full audit traceability.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.