-01%201.svg)

Key takeaways

- Missing the March 15 advance tax deadline triggers 1% monthly interest under Section 234C, paying by March 31 minimizes damage but does not eliminate it

- TDS deducted in March must be deposited by April 7, not March 31, late payment attracts 1.5% monthly interest plus ₹200 per day penalty

- Section 43B(h) now disallows deductions for MSME payments beyond 45 days, clear these before year end or lose the tax benefit entirely

- Virtual Accounting by AI Accountant prevents most year end compliance fires through automated tracking and proactive CA alerts

What tax deadlines do Indian businesses face on March 31?

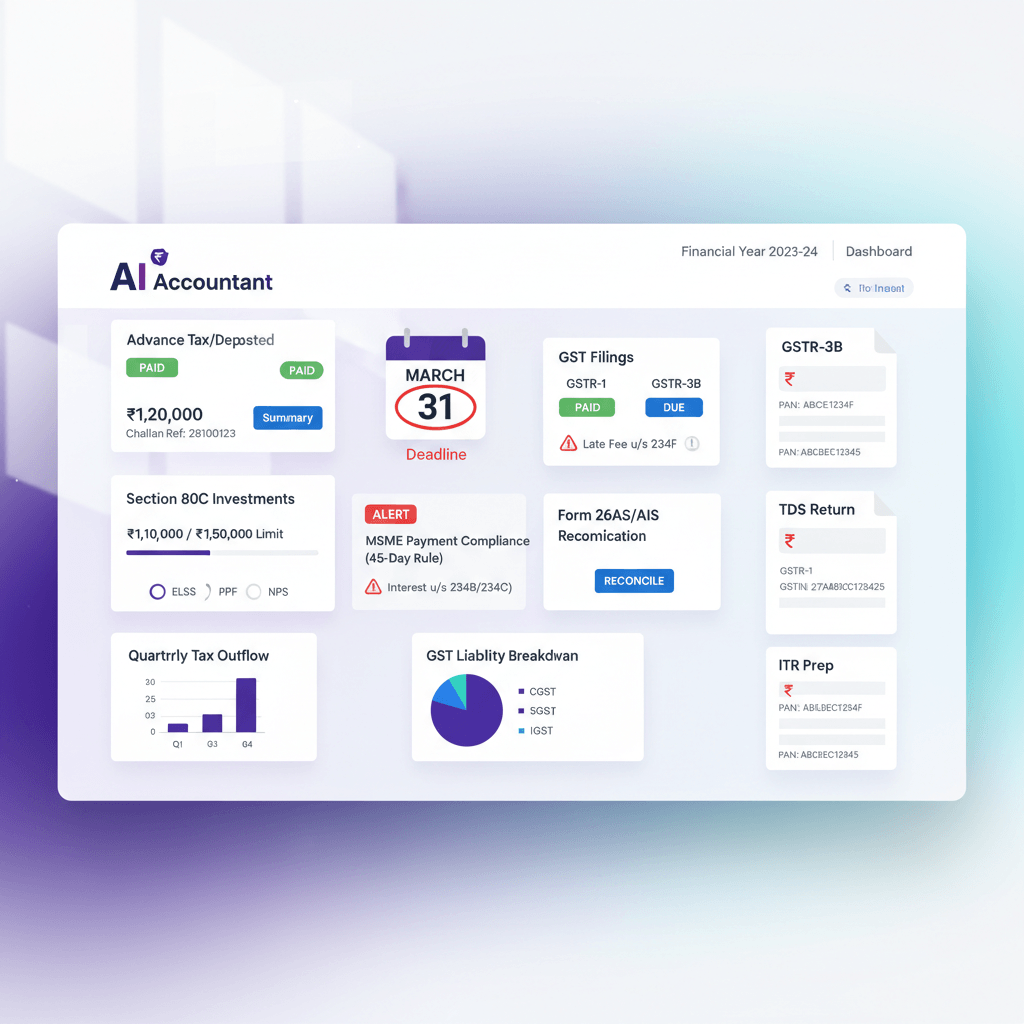

March 31 sits at the crossroads of multiple compliance workflows. You are wrapping up advance tax, preparing to deposit March TDS by April 7, closing GST books for annual return prep, and locking in tax saving investments under Section 80C by March 31. Miss any one of these, and you invite interest, penalties, and scrutiny that can snowball through the year. With Virtual Accounting by AI Accountant, you get automated deadline tracking and proactive CA support, so your team avoids costly last minute scrambles.

March hits different when you are running a business. While competitors chase new deals, you are juggling spreadsheets, wondering if that TDS payment went through, whether your advance tax calculation is right, and what happens if you miss a GST deadline by one day. The cost is not just a late fee, it is the audit notice that shows up later, the working capital crunch that follows, and the hours lost to firefighting.

The real cost of missing March deadlines

Missed deadlines trigger a chain reaction. A single missed TDS deposit becomes 1.5% monthly interest under Section 201(1A), plus ₹200 daily late fee under Section 234E, plus potential prosecution if the amount is significant. Miss a GST return, and you pay per day late fees, plus 18% annual interest on unpaid tax. The real cost arrives later, when one late filing flags your account for deeper scrutiny.

What penalties hit immediately versus later?

Immediate penalties start at once. TDS late fees at ₹200 per day, GST late fees from the missed due date, automated and relentless. Delayed penalties land months later. Underpaid advance tax invites Section 234C interest, MSME payments delayed beyond 45 days get disallowed under Section 43B(h) during assessment, increasing your tax bill. These delayed hits are worse, since they usually arrive with reassessment notices.

Which deadlines can destroy your working capital?

GST interest at 18% annually drains cash quickly. On a ₹10 lakh GST liability, a three month delay costs about ₹45,000 in interest alone. Advance tax shortfalls also create a double hit, you pay 1% monthly interest on the shortfall, and your next quarter’s burden spikes. Many businesses end up borrowing just to service compliance mistakes.

Pro tip: Put compliance cash outflows on a predictable schedule, not ad hoc transfers. It saves both interest and reputation.

Critical March 15 to March 31 actions that save lakhs

Your advance tax final installment was due March 15. If you missed it, pay by March 31 to cap further interest under Section 234C. Every day you wait compounds the problem. For MSME vendors, Section 43B(h) can disallow deductions if payment exceeds 45 days, so clear aging MSME invoices before year end. For employees, ensure tax saving proofs and actual payments under Section 80C are in place by March 31, otherwise expect TDS corrections and audit queries later.

How much advance tax must you pay by March 31?

By March 31 you must reach 100% of your final tax liability for the financial year, including surcharge and cess. If your total tax is ₹10 lakh and you have paid only ₹7 lakh, you owe 1% monthly interest on the ₹3 lakh shortfall from April 1 until payment. When in doubt, a conservative approach is to pay 110% of last year’s tax if income is stable, or ask a CA to recompute on current year numbers if profits have spiked.

What if you have underpaid advance tax all year?

Quarter wise shortfalls attract stacked interest, since Section 234C applies quarter by quarter. If you repeatedly paid 50% of what was required each quarter, the March payment balloons to cover the entire backlog, and interest accumulates by quarter and by month.

| Quarter | Required | If paid 50% | Interest rule | Illustration on ₹10L tax |

|---|---|---|---|---|

| Q1 (Jun 15) | 15% | 7.5% | 3% for 9 months | ₹2,250 |

| Q2 (Sep 15) | 45% | 22.5% | 3% for 6 months | ₹4,050 |

| Q3 (Dec 15) | 75% | 37.5% | 3% for 3 months | ₹3,375 |

| Q4 (Mar 15) | 100% | 50% | 1% per month | ₹5,000 per month |

Action now, not comfort later. Pay the maximum possible by March 31, then prepare for the inevitable interest computation. Money paid sooner stops the meter.

TDS and compliance traps hidden in plain sight

TDS compliance looks easy until notices begin. March TDS is due April 7 for salary and most payments, not March 31. The common trap is missing February TDS, then paying February and March together in April, which triggers cascading interest, late fees, and mismatches in Q4 returns.

Different payments demand different TDS sections and rates, contractors, professionals, rent, and more. Pay a freelance designer without deducting TDS, and you risk disallowance of the expense and interest on top. You carry the liability, not the vendor.

Warning, Section 40(a)(ia) disallowance: Skip TDS on a ₹5 lakh professional payment, and you risk disallowance of the entire ₹5 lakh during assessment, increasing tax liability by ₹1.5 lakh at a 30% rate, plus interest.

Which TDS rates apply for year end bonuses?

Bonuses and incentives are taxed under Section 192 at slab rates. If a bonus pushes an employee into a higher slab, compute TDS accordingly, add surcharge and cess as applicable. Gifts and ex gratia above ₹5,000 are taxable perquisites, and need TDS at the employee’s marginal rate. Safer practice, estimate at the highest plausible bracket for each employee, then true up in Form 16.

What happens if you missed TDS on February payments?

February TDS was due March 7. If missed, you already owe 1.5% monthly interest under Section 201(1A). Pay immediately, since interest runs until deposit. The late fee of ₹200 per day caps at the TDS amount, but interest keeps ticking. Defaults reflected in your Q4 TDS return can invite wider scrutiny.

This is where Virtual Accounting by AI Accountant changes the game. You get proactive alerts before deadlines, a CA reviews every payment for TDS applicability, and automated mapping of transaction types to TDS sections. If you are comparing providers, use this buyer’s checklist to shortlist the right virtual accounting partner. Want to see it in action? Watch this short video.

Stop managing tax deadlines in Excel

Get a dedicated CA team plus smart automation. Never miss another deadline.

GST annual return and ITC reconciliation disasters

Your GST annual return for FY 2023 to 24 is not due until December 31, 2024, but reconciliation headaches start now. Mismatches between books and GSTR 2A or 2B, ITC without valid invoices, and missed reversals, they surface during annual filing, with interest if you claimed credit prematurely.

Invoices older than November 30 following the financial year cannot be claimed. If your vendor has not filed the return reflecting your invoice, credit is blocked. March 31 is your best chance to push vendors to file pending returns, otherwise you risk losing ITC or paying it back with interest later.

| Common ITC issue | Impact | Fix before March 31 |

|---|---|---|

| Vendor has not filed return | ITC blocked | Withhold payment, send legal notice |

| Invoice date versus booking date mismatch | ITC reversal with interest | Correct books now |

| Blocked credits under Rule 36(4) | ITC partly lost | Reconcile and follow up |

| Reverse charge unpaid | ITC blocked plus interest | Pay immediately |

How do mismatched invoices affect next year?

Mismatches ripple forward. A March purchase booked on an April dated invoice inflates current year ITC, then gets reversed with 18% interest from April 1. Credit notes not properly accounted for trigger flags in GSTR 9 and often lead to notices. The fix is tedious, review every credit note, reverse ITC where required, and match to vendor GSTR 1.

What is the real deadline for ITC claims?

The statute says November 30 of the following financial year, but the practical deadline depends on vendor compliance. If a vendor files March returns in October, you have only a narrow window to claim credit. Prioritize high value ITC gaps by March 15, escalate with suppliers who chronically file late, or renegotiate terms to compensate for lost ITC.

Documentation and audit preparation most businesses botch

March 31 is not only about payments, it is about evidence that stands up to scrutiny. If your turnover crossed ₹1 crore, you likely need a tax audit. Even smaller businesses get picked for review when GST and income tax numbers do not align. Physical inventory verification on March 31 is evidence, not formality. Discrepancies need explanations, adjustment entries, and sometimes revised returns.

Which documents do tax officers demand first?

Expect full bank statements for every account, party wise ledger reconciliations for top vendors and customers, stock statements, and fixed asset registers. Digital assets and software are under the microscope, if you claimed depreciation, keep purchase proofs and license documents handy.

How should you organize audit files?

Create seven folders, Income Proof, Expense Support, Statutory Filings, Bank Reconciliations, Party Confirmations, Stock Records, and Legal Documents. Each invoice should have three proofs, invoice, payment evidence, and delivery or service proof. Keep digital copies searchable, consistently named, and indexed. For a step by step prep guide, see How to Prepare Your Books for a Statutory Audit India.

- All 12 months of bank statements, certified

- Physical stock verification report with variance notes

- Fixed asset verification certificate

- Party confirmations for large balances

- Related party transaction documents

- Director or partner personal account statements when relevant

- Cash book with daily balances

- Pending litigation and provisions

- Loan agreements with interest workings

- Board resolutions for major transactions

Lesser known rules that trigger surprise penalties

Section 269ST is unforgiving. Accept more than ₹2 lakh cash from a single person in a day, even across invoices, and the penalty equals the amount received. Under the Section 40A(3) limit of ₹10,000 cash payment per day, splitting payments in a day does not help. Transport businesses have a higher threshold with proper documentation.

Depreciation also has traps. Buy an asset on March 30 and you usually get 50% depreciation if used less than 180 days. If you sell next year, the department can claw back benefits during block adjustments. Prefer acquisitions before September 30 for full depreciation, or wait until April 1.

What about MSME payment rules nobody talks about?

The 45 day MSME payment rule under Section 43B(h) has teeth. Payments to Udyam registered MSMEs beyond 45 days, or 15 days without a written agreement, become non deductible this year and only allowable in the year of actual payment. Vendors can update Udyam status anytime, so review vendor status monthly.

Which cash transactions will haunt you later?

Festival gifts in cash can become disallowed expenses and taxable perquisites if you skipped TDS. Petty cash settlements on March 31 invite questions when balances look artificially low. Document everything, deposit excess cash before month end, and avoid last minute cash purchases that look like income suppression.

Your finance team without the overhead

Automated compliance tracking plus dedicated CA support from ₹4,000 per month. Fewer fires, more focus, better sleep.

Systems that prevent March madness all year

Chaos happens when compliance lives in fragments, GST in one sheet, TDS in another, advance tax on chat threads. High performing teams run a single workflow, a compliance calendar with due dates, preparation windows, reviews, and confirmed proofs saved in a central repository.

What tools actually work for small businesses?

For turnover under ₹5 crore, three connected tools are enough, a cloud accounting system, a simple compliance tracker, and a document manager. Integration matters more than features, ensure accounting data feeds the tracker automatically. If you prefer to outsource, consider online bookkeeping services that bring accounting, compliance, and documentation together.

How do you build compliance into daily operations?

Make compliance part of each transaction. Every purchase entry should check TDS applicability, GST classification, and vendor MSME status. Every sales entry should update advance tax projections. Weekly reviews beat monthly scrambles, a 30 minute Monday review prevents a 30 hour month end crisis.

| Date | Action | Why it matters |

|---|---|---|

| March 1 to 5 | Calculate advance tax, review vendor payments | Arrange funds in time |

| March 6 to 10 | Collect employee investment proofs | Process TDS corrections cleanly |

| March 11 to 15 | Pay advance tax, clear MSME dues | Avoid interest and disallowance |

| March 16 to 20 | Reconcile GST and ITC | Fix mismatches before year end |

| March 21 to 25 | Complete documentation and physical verification | Be audit ready |

| March 26 to 31 | Final payments and system cleanup | Enter the new year clean |

Conclusion

March 31 is not about a single day, it is about the systems you run all year. Every April penalty was preventable in February. Businesses that thrive do not rely on heroics, they build workflows that make compliance automatic. Whether you do it in house or with Virtual Accounting by AI Accountant, consistency beats last minute chaos, every single time.

FAQs

What happens if I miss the March 15 advance tax deadline by just one day?

Missing March 15 triggers Section 234C interest at 1% per month on the shortfall. If you owed ₹10 lakh and pay on March 16, expect ₹10,000 as interest for that period. The notice comes later, but the clock starts right away. Pay by March 31 to stop further accrual. To avoid repeats, consider Virtual Accounting by AI Accountant for proactive reminders and CA oversight.

Can I still claim Section 80C deductions if I invest on April 1?

No, Section 80C investments must be made by March 31 to count for that year. Payments on April 1 shift the deduction to the next year. If March 31 is a bank holiday and you have banking channel proof, your CA can advise if an exception is reasonable.

What if my vendor refuses to file GST returns affecting my ITC?

Send a legal notice, withhold future payments, and document on the GST portal via DRC 01B. This does not guarantee ITC, but it builds your defense. Consider switching vendors who chronically default, since every blocked ₹1 lakh of ITC costs ₹18,000 in cash outflow. Automated vendor compliance checks in Virtual Accounting by AI Accountant help you act early.

My TDS payment failed on the due date, what should I do?

Repay immediately through the portal and keep failure proofs. You will still owe 1.5% monthly interest under Section 201(1A) from the original due date. File the TDS return with the actual deposit date. Late fee of ₹200 per day still applies.

How do I know if my vendor is MSME registered?

Verify on the Udyam portal using PAN or Aadhaar, and ask for the Udyam Registration Certificate. Update vendor status monthly, since registrations change. Virtual Accounting by AI Accountant automates MSME status checks and flags invoices approaching the 45 day limit under Section 43B(h).

Is cash payment to employees on March 31 problematic?

Cash salary is not barred, but it complicates audits. Large cash payouts invite questions, reduce deduction credibility, and can create perquisite tax issues. Best practice is bank transfer by March 30, and use March 31 only for minor true ups with documentation.

What is the penalty if I accept ₹2.5 lakh cash from a customer?

Under Section 269ST, the penalty equals the amount received, here ₹2.5 lakh. Exceptions are narrow, so always use bank channels for high value receipts. Configure alerts in your billing process to block large cash receipts automatically.

Can I claim GST ITC for March 2024 purchases in April 2025?

No, the hard stop for FY 2023 to 24 ITC is November 30, 2024. After that date, you cannot claim, even with valid invoices. Reconcile by March, push vendors to file, and lock your claims early.

Do I need physical stock verification if I maintain digital inventory?

Yes, auditors expect a physical verification on March 31 with variance explanations. Without this, closing stock values are open to challenge, often leading to higher assessed income. Create signed count sheets, variance logs, and adjustment entries with supporting notes.

What interest applies if I delay MSME payments beyond 45 days?

The tax impact is disallowance under Section 43B(h), so you lose the deduction this year and only get it on actual payment. Separately, MSME vendors can charge interest under the MSMED Act. Automated payables aging in Virtual Accounting by AI Accountant helps you stay compliant.

How quickly must I deposit March TDS to avoid penalties?

Deposit by April 7 for non government deductors. From April 8, interest at 1.5% per month begins, and the late fee of ₹200 per day applies. Even a one day delay counts as a full month for interest.

Can advance tax be revised after March 31?

You cannot revise advance tax after year end, but you can pay self assessment tax before filing. Shortfalls trigger 234B and 234C interest, while self assessment tax primarily triggers 234A from the return due date. If you find underreported income in April, pay immediately to minimize interest.

What if I discover fake invoices in my purchases during March review?

Report via DRC 01B, reverse ITC with interest from the claim date, and file a police complaint if fraud is suspected. Voluntary disclosure usually avoids penalties, but not interest. Three way matching in Virtual Accounting by AI Accountant prevents such invoices from entering your books.

Should I defer March revenue to April for tax planning?

No, if goods were delivered or services completed by March 31, recognize revenue. The GST system matches e way bills with filings, deferrals are caught easily. Focus on legitimate deductions and timing of real expenses, not manipulation.

How do I handle year end employee tax declarations?

Collect Form 12BB with proofs by March 25, adjust TDS in March payroll, and keep copies for seven years. If proofs are missing, deduct higher TDS now, and let employees claim refunds in their returns. Virtual Accounting by AI Accountant digitizes declarations, automates TDS recalculation, and flags missing proofs before payroll cut off.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.