Key takeaways

Invoice vs Bill vs Receipt: the short answer

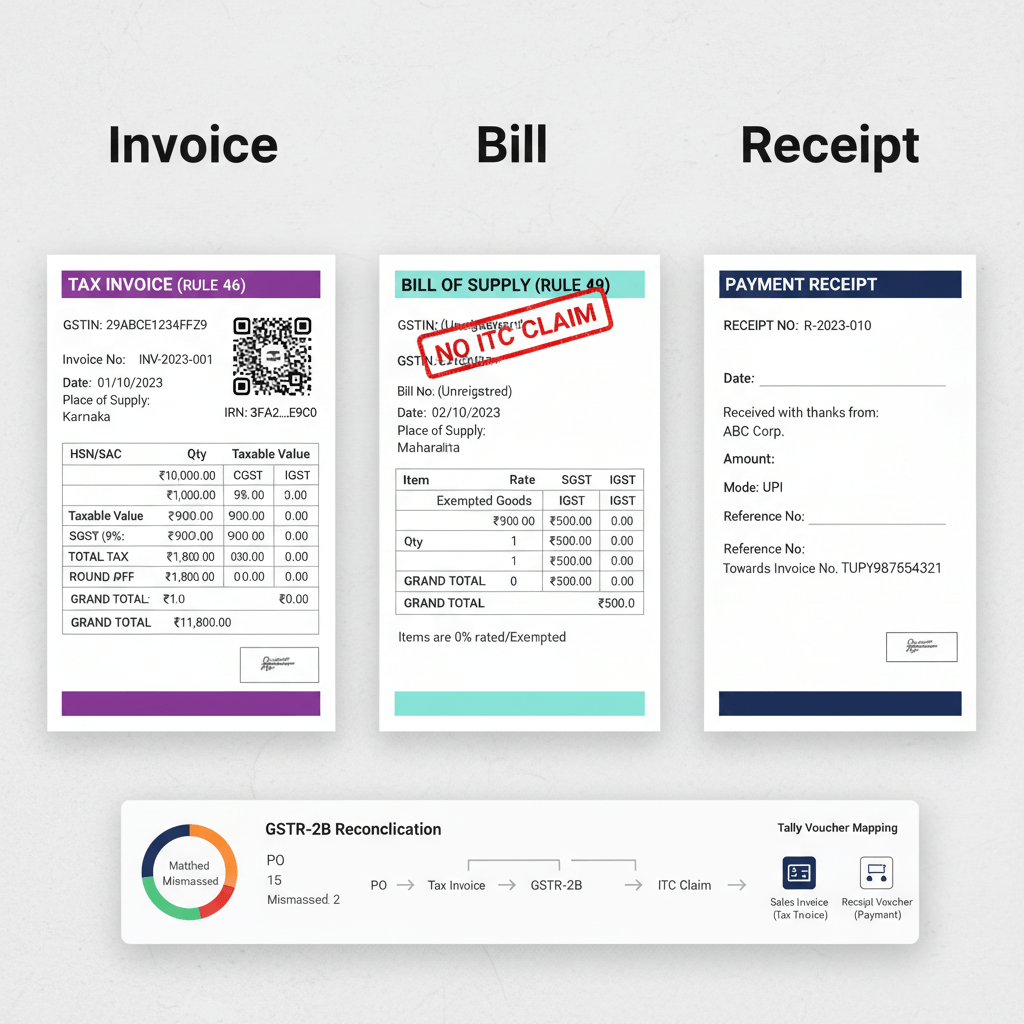

In GST compliance, the document type drives your ITC. A tax invoice issued under Section 31 read with Rule 46 enables the recipient to claim ITC. A bill of supply under Rule 49 covers exempt or non-GST supplies and does not permit ITC. A receipt merely acknowledges payment, while a receipt voucher under Rule 50 applies to service advances where GST becomes payable at the time of receipt.

Why this matters: misclassifying a vendor document in Tally inflates ITC beyond what GSTR-2B permits, inviting reversals and interest. In Q3 2024, GSTR-2B reconciliation mismatches blocked ₹8.4 lakh average ITC per SMB, with 68% of errors traced to wrong document classification at purchase entry.

Rule of thumb: No tax breakup, no ITC. No supplier GSTIN, no ITC. Not in GSTR-2B, no ITC.

What is a GST tax invoice in India, and what does it unlock?

A GST tax invoice issued under Section 31 of the CGST Act read with Rule 46 is the primary document that unlocks ITC for the recipient. It must show supplier and recipient GSTINs, invoice number and date, HSN/SAC, description, quantities or values, taxable value, tax rate and amount, place of supply, and signature. ITC flows only when the supplier uploads it, and it appears in the recipient’s GSTR-2B.

Mandatory contents under Rule 46

Miss any core field, and the invoice risks scrutiny, GSTR-2B mismatches, and ITC blockage.

ITC linkage and GSTR-2B population

Supplier GSTR-1 feeds the buyer’s monthly GSTR-2B, a static statement generated between the 1st and 13th. CBIC Circular 193/05/2023-GST ended provisional ITC, so claims must mirror GSTR-2B. If a ₹1,00,000 purchase bears ₹18,000 GST on the invoice but the supplier files late, you must wait until it appears in a later GSTR-2B, still subject to Section 16(4).

E-invoicing and the IRN field

With AATO above ₹5 crore, you must generate an Invoice Reference Number (IRN) before issuing B2B invoices, credit notes, or debit notes. The IRN authenticates the invoice and auto-populates GSTR-1 and e-way bill. Missing IRN where applicable can lead to ITC denial for the recipient even if other fields are correct.

What exactly is a “bill” in accounting and Tally, and how is it different from an invoice?

In practice, “bill” is the buyer’s payable record, while the seller’s document is either a tax invoice with GST or a bill of supply under Rule 49 for exempt, non-GST, or composition-dealer supplies. The confusion comes from Tally’s bill-wise tracking in payables. The underlying GST document type still governs ITC.

Buyer’s “bill” vs seller’s invoice

From the seller side, you issue a tax invoice for taxable supplies, a bill of supply if the supply is exempt. From the buyer side, both are vendor bills in accounts payable. Record them differently to avoid phantom ITC.

Bill of supply: when and why

Bill of supply excludes tax fields by design, so no ITC is available.

Tally voucher mapping

What is a receipt under GST, and when does a receipt voucher apply?

A receipt is just a payment acknowledgment, it carries no tax implication, and cannot support ITC. A receipt voucher under Section 31(3)(d) read with Rule 50 applies to service advances, where GST becomes payable on receipt and is later adjusted against the final invoice.

Receipt vs receipt voucher

Payment receipts, bank slips, or UPI confirmations are proofs of payment only. A receipt voucher is a GST document for service advances, showing description, advance amount, tax rate, and tax amount. For a ₹1,00,000 service advance at 18% GST, tax payable on receipt is ₹15,254, computed as 1,00,000 × 18/118, later adjusted in the final invoice.

Advances: goods vs services

Goods advances are exempt from GST per Notification No. 66/2017-Central Tax, so no receipt voucher, and tax is due at invoice. Service advances require a receipt voucher and tax payment on receipt, then adjustment later.

What not to claim ITC on

Compliance tip: If it is not a Rule 46-compliant tax invoice and is not in GSTR-2B, it cannot support ITC.

Invoice vs bill vs receipt: a quick mapping to avoid ITC mistakes

DocumentPurpose & IssuerGST/ITC treatmentTally posting (buyer)Common mistakesTax invoiceTaxable supply by registered dealerGST charged, ITC available if Rule 46 compliantPurchase Voucher, Invoice Mode with tax ledgersMissing HSN, wrong place of supply, no bill-wise referenceBill of supplyExempt or non-GST supplyNo GST, no ITCPurchase Voucher, Voucher Mode without tax ledgersRecording with GST ledgers, creating phantom ITCReceiptPayment acknowledgmentNo ITC relevancePayment or Contra VoucherAttempting ITC from payment proofReceipt voucherService advanceGST payable on receipt, adjustableSupplier issues voucher, buyer books as advanceUsing for goods advances where not requiredCredit noteReduces original invoice valueReduces recipient’s ITCCredit Note Voucher linked to originalPosting via Journal, breaking GSTR-2B trailDebit noteIncreases invoice valueIncreases recipient’s ITC if acceptedDebit Note Voucher linked to originalNot linking to original invoice referenceSelf-invoice (RCM)Recipient under RCMITC on payment basisPurchase + Payment VoucherClaiming ITC before tax payment

Credit and debit note linkage requirements

Credit and debit notes under Section 34 must reference the original invoice and be reported by the annual return due date, or September following the year, whichever is earlier. In Tally, use dedicated Credit/Debit Note Vouchers with bill-wise adjustment, never a Journal Voucher for these documents.

RCM self-invoice mechanics

For notified supplies under Reverse Charge Mechanism, the recipient issues a self-invoice and pays tax via GSTR-3B. ITC is eligible only upon payment, then availed in the same month.

When should you use invoice, bill, or receipt in FY 2025-26?

Compliance has shifted to a GSTR-2B-first world. Get the document type right, track e-invoicing thresholds, and work backward from the Section 16(4) deadline to protect ITC.

GSTR-2B-first ITC

GSTR-2B is generated monthly and is static. Claims in GSTR-3B must align with GSTR-2B entries. Missed invoices must wait for a future GSTR-2B, so monthly reconciliation is non-negotiable. Tools like an “AI Accountant” can help, for example automated pulls of GSTR-2B and matching to your purchase register, to keep claims accurate.

The 30 November cutoff

For FY 2025-26, the last date to claim ITC is 30 November 2026, or the annual return filing date if earlier. Use April to November to chase suppliers, correct HSN, fix place of supply, and ensure e-invoicing compliance where applicable.

Capture IRN when applicable

With AATO over ₹5 crore, enable e-invoicing in your ERP, capture the 64-character IRN and QR code, and ensure the same appears on the tax invoice. Missing IRN where mandated can block the recipient’s ITC even if everything else is correct.

Time saver: If your team spends days on exceptions, consider an “AI Accountant” workflow that auto-tags IRN errors, credit/debit note linkages, and supplier filing delays.

Common mistakes and misconceptions

Myth 1: Payment receipts can support ITC claims.

Reality: Only Rule 46-compliant tax invoices support ITC. Receipts or bank statements cannot substitute a tax invoice, and claiming on their basis attracts reversal plus 18% interest.

Myth 2: Credit notes can be posted through Journal Entry.

Reality: Use Tally’s Credit Note Voucher with original invoice linkage. Journals break the GSTR-2B trail and complicate ITC reversals.

Myth 3: ITC can be claimed immediately upon invoice receipt.

Reality: Claim only when the invoice appears in GSTR-2B. Posting early creates mismatches and interest exposure.

Related reading

FAQ

How do I explain invoice vs bill vs receipt to non-accounting staff so they do not book wrong ITC?

Train teams that only a Rule 46-compliant tax invoice with supplier GSTIN and tax breakup unlocks ITC, a bill of supply is for exempt or non-GST items with no ITC, and a receipt is only payment proof. Share sample screenshots in Tally: Purchase Voucher Invoice Mode for tax invoices, Voucher Mode for bills of supply, and Payment/Contra for receipts. Reinforce that ITC is claimed only when the invoice appears in GSTR-2B.

What checklist should a CA insist on before booking a vendor invoice with ITC in Tally?

Confirm supplier GSTIN, unique invoice number and date, HSN/SAC, place of supply, tax rate and split, and for eligible entities, a valid IRN. Verify the vendor’s GSTR-1 filing status, and match the invoice in the next GSTR-2B. Post in Purchase Voucher Invoice Mode with correct tax ledgers and bill-wise reference. If any field is missing, return the invoice for correction before booking.

We recorded a bill of supply with GST ledgers by mistake, how do we fix ITC already claimed?

Reverse the ITC in the next GSTR-3B through Table 4B with interest at 18% from the original claim date. In Tally, cancel or modify the voucher to Voucher Mode without GST ledgers, and pass a journal to reverse the credit against CGST/SGST/IGST ledgers. Keep a note explaining the error and correction for audit trail.

Is an e-invoice without IRN valid for ITC if the vendor’s turnover is above ₹5 crore?

No. If e-invoicing applies, a valid IRN is mandatory. Absence of IRN risks ITC denial during audit. Ask the vendor to cancel and reissue with IRN within the allowed timelines, or issue credit/debit notes as applicable. Use an “AI Accountant” check to flag invoices missing IRN automatically.

Can a CA recommend provisional booking of ITC pending GSTR-2B, then reverse if not appearing?

Post-CBIC Circular 193/05/2023-GST, ITC should not be claimed provisionally. Best practice is to book the expense in accounts but defer the ITC claim until the invoice appears in GSTR-2B. Automate a monthly hold-and-release workflow using an AI Accountant ruleset to minimize manual follow-ups.

How should advances be accounted when we receive consulting fees upfront?

Issue a receipt voucher under Rule 50 at the time of receipt, compute tax on the advance using the tax-inclusive method, pay GST in the corresponding GSTR-3B, and later adjust the advance and tax against the final invoice. Do not issue a tax invoice on day one unless the service is also supplied.

What is the CA’s approach when supplier GSTR-1 shows a lower value than the physical invoice?

Claim ITC only up to the amount visible in GSTR-2B, then coordinate with the supplier to file an amendment or a debit note to correct the short reporting. Keep email trails, revised documents, and the final GSTR-2B reflection before enhancing the ITC claim. Avoid over-claiming and subsequent reversal with interest.

How do we handle imports for ITC without GSTR-2B linkage?

Use the Bill of Entry as the tax document for imports, along with IGST payment proof. Post the Bill of Entry number and date in Tally, and claim ITC in the month of filing. The IGST on imports is not dependent on supplier GSTR-1, so GSTR-2B is not the basis here.

What controls prevent staff from posting credit notes via Journal in Tally?

Disable generic journal posting for purchase returns in your SOP, enable bill-wise details and enforce use of Credit Note Voucher with mandatory original invoice reference. Run a monthly review for vouchers that reduce purchase values without using Credit Note Voucher, and retrain users. An AI Accountant audit rule can auto-flag non-linked adjustments.

When is a self-invoice under RCM mandatory, and how does ITC flow?

For notified RCM supplies such as GTA or legal services, the recipient issues a self-invoice under Section 31(3)(f). Record the purchase, pay the tax via Payment Voucher, and avail ITC in the same period after payment. Do not claim ITC before paying the RCM liability.

Can we claim ITC on telecom and utility bills issued without our company’s GSTIN?

Technically no, the recipient GSTIN should appear on the invoice for ITC. Ask the provider to reissue bills with your GSTIN. If that is not feasible, keep reimbursement and usage documentation, but recognize that ITC may be denied during audit. Policy-level vendor onboarding should require GSTIN mapping to avoid this.

For March year-end invoices received in April, should we backdate ITC to March?

No. Post the expense as per accrual needs, but claim ITC only in the period when the invoice appears in GSTR-2B. Ensure the claim is before the Section 16(4) deadline. Maintain a tracker for March invoices appearing in April or May GSTR-2B to avoid missing the cutoff.

Does a POS retail receipt saying “GST included” allow ITC if it lacks supplier GSTIN and tax breakup?

No. Without supplier GSTIN, invoice serial number, HSN/SAC, and tax breakup, the document is not a valid tax invoice. Ask for a proper B2B tax invoice. Treat the POS slip as payment proof only, not a basis for ITC.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.