-01%201.svg)

Key takeaways

- Most reconciliation gaps in India arise from timing differences, mixed-format statements, and suspense entries, solve them with weekly reviews, a strict month-end checklist, and clear GL mapping.

- Payment gateway net settlements, GST code mistakes, and TDS net vs. gross postings cause recurring AR, AP, and GSTR mismatches, reduce these with invoice-level matching and contra entries.

- Automate data ingestion and narration decoding, then approve postings via workflow, tools like AI Accountant minimize manual typing and duplicate entries.

- Lock prior-month reconciliations, verify opening equals prior closing, and track outstanding cheques, deposits in transit, and intercompany transfers to prevent carry-forward errors.

- Maintain entity-specific vendor masters, separate bank charges, interest, and FX, and consistently split EMI principal, interest, for clean financial reporting.

- Use UTR-based matching for UPI, IMPS, NEFT, apply rules for petty cash replenishments, and round-off variances, then clear suspense balances within five days of close.

- Adopt a 10-phase month-end checklist, document exceptions, and sign off with reviewer oversight, this protects audit readiness and cash flow clarity.

Why bank reconciliation matters in India

It is late at night, the spreadsheet is noisy, narrations are cryptic, and settlements do not align, this is the reality of bank reconciliation for small businesses in India. Reconciliation is not a compliance checkbox, it underpins cash flow visibility, audit readiness, and fraud prevention. In India’s complex ecosystem, GST and TDS cycles, fragmented payment channels, and varied statement formats quickly amplify small mistakes.

What is at stake?

Cash flow visibility: Uncategorized transactions obscure true operating cash.

GST compliance: Incorrect codes and missed credits invite GSTR mismatch and audit exposure.

TDS management: Net vs. gross posting mismatches distort AR and payables clarity.

Audit readiness: Unresolved gaps prolong close timelines.

Payment gateway complexity: Razorpay, Paytm, PhonePe settlements mask fees, refunds, and timing lags.

Bank narrations are sparse, statements arrive in mixed formats, and data lives across WhatsApp, photos, CSVs, and accounting systems, without process, errors cascade.

The most common bank reconciliation errors small businesses make in India

1. Timing differences, deposits in transit and outstanding cheques

The problem: Cheques take days to clear, deposits recorded at month end may not appear on the bank statement, this temporary mismatch is often confused with real errors.

India context: Cheque usage remains common in B2B payments, without an outstanding cheque register, items linger indefinitely.

Fix: Maintain an outstanding cheque log, verify clearance for items older than seven days, and flag for follow-up. Further reading: indinero’s bank reconciliation services for small businesses, FreshBooks on bank reconciliation.

2. Missing or duplicate entries from manual data entry and mixed-format statements

The problem: Bank shows a transaction that is missing in books, or the same payment is recorded twice due to retyping, system glitches, or parallel processes.

India context: PDF and JPEG statements, inconsistent CSVs, and manual retyping invite transposed amounts and duplicates.

Fix: Use reconciliation software that automatically detects duplicates across bank files and validates data entry. Consider AI Accountant, then require a second-layer review and standardize ingestion via CSV to one system. References: KMK Ventures on bank reconciliation errors, AFP Cash Management on common errors.

3. Uncategorized transactions in suspense due to unclear narrations

The problem: Cryptic narrations for UPI, IMPS, NEFT, and gateway settlements leave entries unclassified.

India context: UTRs and gateway references omit invoice numbers, variable vendor names complicate matching.

Fix: Build recurring mapping, maintain a vendor and customer master with aliases, bulk match reference IDs at month end, and apply a threshold rule for UPI micro spends. Learn more: smart narration parsing for Indian statements.

4. Misclassification of ledgers, income vs. transfers, loan principal vs. interest

The problem: Director loan repayments booked as expenses, refunds treated as negative revenue, EMI principal and interest lumped together.

Fix: Freeze the chart of accounts, pre-validate EMI splits, tag related-party and loan transactions clearly, and enforce approvals for capital, loan, and related-party postings.

5. GST issues, wrong codes, missed input credits, refunds not matched

The problem: Incorrect GST codes and misposted refunds lead to GSTR mismatches and reduced credits.

Fix: Standardize GST capture at bill entry with HSN or SAC, match GSTR-2B monthly, record GST refunds as credits not income, and investigate variances above a clear threshold.

6. TDS mismatches, net payments vs. gross invoices

The problem: AP shows a gross invoice, bank reflects net after TDS, the TDS receivable is not recorded, creating phantom variance.

Fix: Use a standard TDS workflow, post gross to AP, post TDS receivable contra, clear receivable upon deposit, and reconcile monthly via a TDS register.

7. Bank charges, interest, and FX fees not recorded or lumped

The problem: Small charges and FX markups are missed, interest credits mix with expenses, uncategorized balances swell.

Fix: Review weekly, create separate GL codes for service charges, interest income, interest expense, and FX gain or loss, auto-map recurring fees, and resolve unidentified charges quickly.

8. Payment gateway settlements, fee netting, timing mismatches, refunds

The problem: Net deposits differ from invoice revenue, fees are not recorded, refunds and chargebacks are not linked to invoices.

Fix: Pull daily gateway reports and match invoice level, split net and fees, track refunds as contra entries, and set timing rules. Deep dive: settlement file parsing for gateways.

9. Reversals and refunds posted as revenue adjustments instead of contra entries

The problem: Negative revenue postings inflate turnover and break AR linkage.

Fix: Use a “refunds and reversals” contra GL, always link to the original invoice, monitor refund ratios, and match bank reversals to approvals.

10. Opening and closing balance carry-forward errors

The problem: Prior month incomplete reconciliation causes compounding variances.

Fix: Lock prior month, verify opening equals prior closing, document status, and use a checklist to sign off before posting.

11. Intercompany and related-party transfers misposted

The problem: Transfers booked as revenue or expense across entities inflate top-line and costs.

Fix: Maintain dedicated intercompany ledgers with entity codes, enforce approvals, and reconcile monthly between entities.

12. Petty cash and bank transfers double-counted or treated as income

The problem: Cash withdrawals posted as expenses, interbank transfers coded as revenue.

Fix: Treat internal transfers as balance sheet only, reconcile petty cash weekly, and flag withdrawals without supporting receipts.

13. Round-off differences and tax rounding issues

The problem: Minor rounding at invoice vs. bank leads to small but numerous variances.

Fix: Standardize rounding rules, match at net levels, and clear micro variances via a round-off adjustment GL monthly.

14. Multi-entity confusion, same vendor or customer across entities

The problem: Payments matched to the wrong entity ledger create phantom AP and AR.

Fix: Use entity-specific vendor and customer codes, enforce entity selection at bill entry, and validate entity tags during bank reconciliation.

How reconciliation errors emerge, India context

Bank narration variability and abbreviations

The challenge: Narrations like UTR and IMPS references lack invoice linkage, causing manual lookups.

Mitigation: Build a narration library and a UTR index mapped to invoices, reconcile weekly.

Fragmented data sources

The challenge: Bills on WhatsApp, invoices across systems, and statements in multiple formats, no single source of truth.

Mitigation: Establish a single bill repository, require upload within five days of receipt, then reconcile against a complete list.

Last-minute posting without reviews

The challenge: End-of-month rush introduces miscoding and missing GST checks.

Mitigation: Create a posting window that closes by the 25th, late bills are flagged or deferred.

No standardized chart of accounts or vendor and customer master upkeep

The challenge: Vague GLs and alias-heavy vendor lists make matching a guessing game.

Mitigation: Freeze the chart, appoint a GL owner, and normalize vendor naming with aliases and entity codes.

Practical, step-by-step month-end close checklist

Phase 1, pre-close preparation by the 25th

- Lock the posting window and collect all bank statements.

- Fetch payment gateway reports at invoice level.

- Upload all bills and invoices to the repository.

- Verify opening equals prior closing, then review prior exceptions.

Phase 2, normalize statement data by the 27th

- Export CSVs, avoid retyping from PDF or JPEG.

- Check duplicates by sorting date and amount.

- Verify opening and closing balances, flag charges and FX items.

Phase 3, resolve uncategorized transactions by the 28th

- Pull suspense lists, match via UTR, amount, and date.

- Apply mapping for recurring payees, escalate unresolved items.

Phase 4, match bank entries to invoices and bills

- Confirm amount, counterparty, date, and GST treatment.

- Validate TDS receivable entries and net vs. gross clearing.

- Match deposits to invoices, reconcile gateway fees separately.

Phase 5, record bank charges, interest, FX

- Post service charges, interest income and expense, and FX to distinct GLs.

- Split EMI principal and interest, validate loan balances.

Phase 6, payment gateway net settlements

- Use dashboard reports, match invoices, record fees, and track refunds as contra entries.

- Reconcile UPI and IMPS via UTRs.

Phase 7, review exceptions

- Analyze refunds and reversals, link to source invoices, and verify interbank transfers are non-revenue.

Phase 8, validate AP and AR aging

- Align bank collections with AR, and bank payments with AP, then clear suspense accounts.

Phase 9, final cut-off checks

- Post accruals, verify dates, and rerun reconciliation, adjusting for outstanding cheques and deposits in transit.

Phase 10, document and close

- Prepare a reconciliation summary, maintain an exception log, sign off, and lock the month.

Automation and workflows that reduce errors

Structured data ingestion

Upload any bank statement format, convert to standardized data, and bulk-capture invoices with GST details. Benefit: Accountants focus on matching and approvals.

Automated ledger mapping

System learns narrations and payees, predicts GST codes, and auto-classifies UPI micro spends. Benefit: Most entries are pre-classified, reviewers approve instead of typing.

One-click sync with accounting software

After reconciliation, push matched entries to Tally or Zoho in one action, flag exceptions in system for ownership. Consider AI Accountant for India-focused OCR and mapping.

Dashboarding and trend visibility

Daily cash and recon health, highlighted charges and refunds, and uncategorized trends illuminate emerging issues before month end.

AP and AR automation and aging clarity

Link AR to deposits, and AP to payments, with DRO and DPO alerts that prompt collection and payment discipline.

India-focused roadmap benefits

- GSTN integration: Auto-fetch GSTR-2B, validate against bills, and align GSTR-1 post close.

- Bank feeds via account aggregator: Real-time feeds reduce timing differences.

- AI-powered reconciliation assistant: Learns exceptions and highlights anomalies such as unexpected vendor spikes.

Philosophy: Let your accountant think, software will type, humans keep control, automation removes grunt work.

India-specific tips and examples

UPI and QR, reliable matching via UTR

Extract UTR from bank, cross-check in UPI app, link UTR to invoice, and benefit from auto matching next time.

Payment gateway reconciliation, net vs. gross settlement

Record invoice revenue at gross, bank deposit at net, and fees to “payment processing fees,” this avoids understated GSTR-1 and muddled revenue.

TDS workflow example, gross invoice, receivable, net payment

Post gross to AP, record TDS receivable contra, clear AP for net on payment, and clear receivable upon government deposit, reconciliation stays clean.

GST rounding differences, handle minor variances

Match on rounded totals, clear micro differences to a round-off GL monthly, keep the balance at zero.

Multi-entity handling, entity tags and vendor normalization

Create entity-specific masters, select entity at bill entry, validate entity at bank reconciliation, avoid cross-entity orphan balances.

Quick diagnostic, red flags

- Large suspense balances indicate unmatched transactions that need immediate resolution.

- Recurring unidentified bank charges suggest a fee or subscription not mapped.

- Frequent GST rounding variances hint at rule mismatch between systems.

- High AP 90+ days may point to TDS workflow gaps.

- AR not aligned to deposits indicates payment gateway matching issues.

- Bank chargebacks without GL entries reveal missed refunds.

Review now: Prior-month reconciliation, opening balance equality, late bills after the 25th, top 10 suspense items, gateway reports for failed or pending transactions, and aged cheques or deposits in transit.

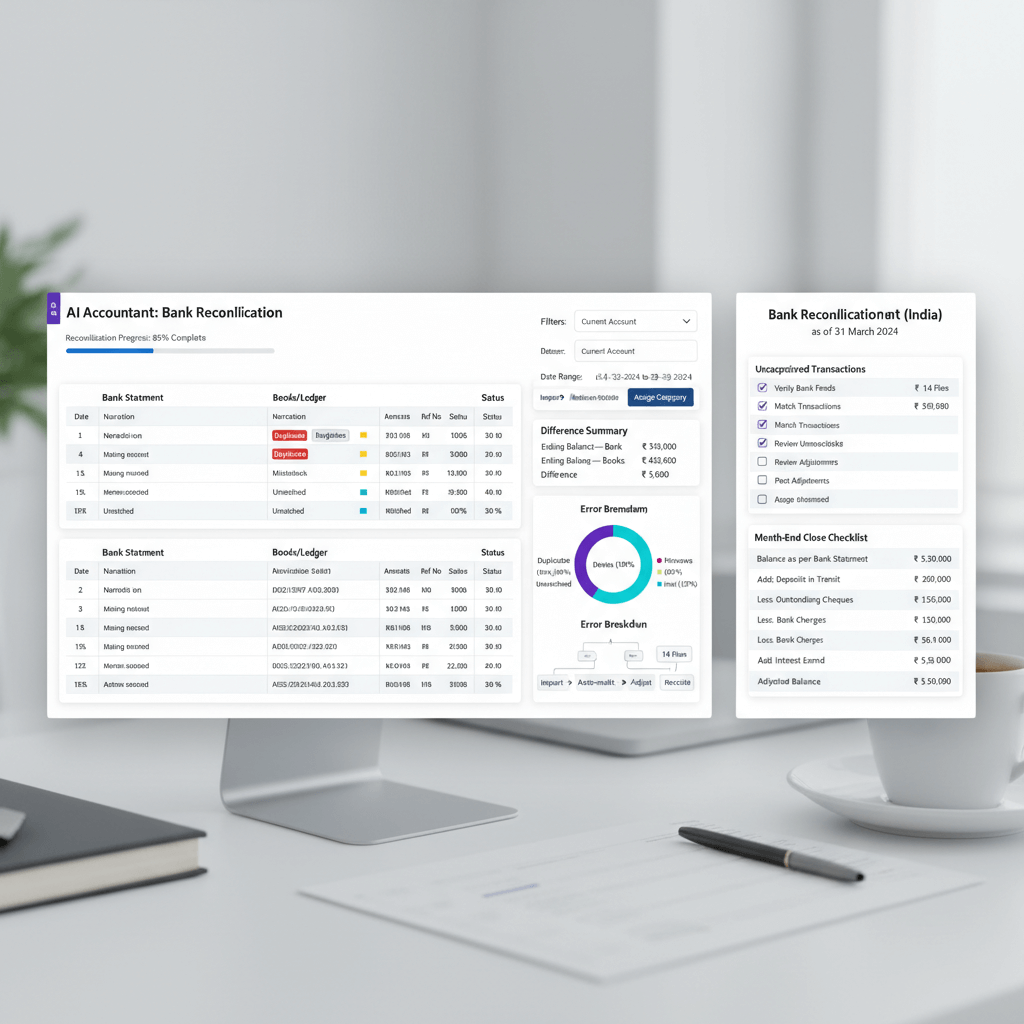

Mini case study, clearing three months of uncategorized chaos

Situation: A CA firm closed books for a mid-sized e-commerce company with three months deferred, suspense at ₹8,50,000.

Process: Categorize entries by type, build mapping rules, pull Razorpay and Paytm reports, resolve outliers, and re-reconcile.

Outcome: Suspense reduced to ₹2,300, three months cleared in four weeks, and future months close in two days with automation and weekly discipline.

Tools, templates, and takeaways

Month-end close reconciliation checklist

Use the 10-phase process above, assign owners and deadlines, and print or digitize for control.

Exception log template

| Date | Transaction type | Amount | Description | Owner | Status | Target resolution | Resolution date |

|---|---|---|---|---|---|---|---|

| May 28 | Unmatched NEFT | ₹25,000 | NEFT UTR123, vendor unknown | Arjun | Open | May 29 | — |

| May 28 | Late bill | ₹15,000 | Contractor invoice received May 28 | Priya | In progress | May 31 | — |

| May 29 | TDS mismatch | ₹8,000 | Invoice gross ₹80k, bank ₹72k, receivable missing | Ravi | Resolved | — | May 29 |

Common rules for recurring transactions

- SALARY TRANSFER, map to salary expense with expected range and date.

- RENT PAYMENT, map to rent expense, attach lease reference.

- GST PAYMENT, map to GST payable, link to GSTR filing.

- RAZORPAY SETTLEMENT, split bank settlement and fee, reconcile daily.

- EPFO CONTRIBUTION, map to employee benefits, link to payroll.

Chart of accounts best practices

Structure assets, liabilities and equity, revenue, cost of goods sold, operating expenses, compliance and tax, finance and admin, and intercompany ledgers. Rule: Every GL has a one sentence definition, if not, split it.

A gentle call to action

If your close involves late nights, suspense piles, and mismatches that spill into next month, combine structured ingestion, automated categorization, and India-specific rules for GST, TDS, and gateway handling. The aim is not to replace accountants, it is to free them from typing so they can focus on analysis, judgment, and audit readiness.

Fewer suspense entries, faster close, clearer cash flow, consider AI Accountant for OCR, mapping, and one-click sync to Tally and Zoho.

Further reading: IBN Tech on bookkeeping mistakes, KMK Ventures guide to reconciliation errors, AFP Cash Management, five common reconciliation errors, SAG Infotech on small business bookkeeping errors, FreshBooks on reconciliation basics, FinSmart Accounting on Indian accounting errors.

FAQs

How should a CA distinguish uncategorized bank entries from true reconciliation errors during month end?

Uncategorized entries exist in bank and books but lack GL coding, reconciliation errors indicate a mismatch between bank and ledger. A CA should first isolate suspense, then run a match by amount, counterparty, and date, resolve suspense with mapping rules, and treat true mismatches via adjustments or contra entries. AI Accountant can auto-suggest categories for recurring narrations and highlight entries missing a ledger match.

What weekly cadence minimizes India-specific timing differences without creating noise?

Adopt a Friday bank review, thirty minutes to flag deposits, payments, charges, and anomalies, then a full reconciliation by the 29th. Daily checks create noise due to cheque and gateway timing, weekly cadence balances speed and signal. AI Accountant dashboards surface outstanding cheques and deposits in transit so you do not chase false errors.

How can a CA control OCR errors when statements are mixed PDF and JPEG from multiple banks?

Use a parser built for Indian formats, validate high-value rows against original PDFs, set an accuracy threshold, and avoid any manual retyping once parsed. AI Accountant’s OCR reports confidence scores, a CA can auto-accept above threshold and batch-review any low-confidence lines.

What is the most reliable way to match UPI and IMPS using UTRs across AR ledgers?

Create a UTR index linked to invoice IDs, customer names, and dates, reconcile weekly, and let rules auto-match recurring UTR patterns. When the same payer’s UTR appears next month, matching is instant. AI Accountant can learn payer aliases and map UTRs to invoices for auto-matching.

How should a CA post payment gateway fees and refunds to avoid distorted GSTR-1?

Book invoice revenue at gross, bank deposits at net, and gateway fees to a dedicated expense GL, always record refunds as contra entries linked to original invoices, never as negative revenue. This preserves turnover reporting and AR integrity. AI Accountant ingests settlement files, splits net and fees, and links refunds to the source invoice automatically.

What is the clean TDS workflow to prevent AP phantom balances for vendors?

Post vendor invoices at gross to AP, record TDS receivable contra to AP, pay net to vendor, deposit TDS to government and clear the receivable, reconcile the TDS register monthly to AP and bank. This ensures AP aging and bank outflows align. AI Accountant can template this workflow and flag any invoice where receivable is missing or aged beyond ninety days.

How should intercompany transfers be structured in GL to simplify consolidation for a CA?

Maintain entity-specific intercompany ledgers, book transfers symmetrically, and reconcile monthly so Parent and Subsidiary balances offset perfectly. Require approvals for all intercompany journals. AI Accountant’s entity tags ensure payments clear the correct entity AP or AR, reducing cross-entity confusion during consolidation.

What controls prevent petty cash replenishments from being misposted as expenses?

Treat replenishment as a balance sheet transfer, maintain a petty cash log with weekly reconciliation and receipt capture, post net spend to relevant expense GLs, and flag withdrawals without documentation. AI Accountant can prompt receipt uploads and restrict posting of cash withdrawals to “interbank or cash transfer” until receipts are attached.

How should a CA handle systematic round-off differences at invoice vs. bank?

Standardize invoice rounding rules, reconcile at rounded totals, and clear micro variances via a round-off adjustment GL monthly, keeping the account at zero by close. AI Accountant can auto-detect sub-one-rupee variances and propose a consolidated adjustment entry.

What exception log structure gives auditors confidence and speeds close for a CA firm?

Track date, type, amount, description, owner, status, target resolution, and resolution date, review daily during close, and require sign-off. Pair this with a reconciliation summary of outstanding cheques, deposits in transit, and adjusting entries. AI Accountant maintains a live exception log, assigns owners, and reminds reviewers before lock.

Which India-focused automations most reduce bank reconciliation defects in practice?

Indian OCR for bank statements, UTR-based matching, GST code prediction at bill entry, TDS receivable templating, and settlement file parsing for gateways. AI Accountant combines these, reducing manual classification and duplicate detection workload, while keeping approvals with the CA.

How can a CA prove opening equals prior closing before allowing current-month postings?

Run a lock check on prior-month reconciliation, verify opening equals closing, and block current postings until alignment is confirmed, document status as reconciled or pending. AI Accountant enforces this lock, preventing drift that leads to carry-forward errors.

What reporting helps a CA spot reconciliation trouble early without waiting for month end?

Daily cash flow with recon health, a highlight feed for bank charges, refunds, FX adjustments, and large transfers, plus an uncategorized trend chart. AI Accountant’s dashboard surfaces these signals, prompting fixes before they snowball.

How should a CA deal with mixed-format gateway narrations that hide invoice references?

Always pull invoice-level gateway reports, match to billing system IDs, record fee splits, and treat refunds as contra, never negative revenue. Where narrations are opaque, rely on settlement files instead of bank narrations. AI Accountant’s settlement file parsing for gateways automates this matching.

What documentation trail satisfies audit review for GST refunds and chargebacks?

Maintain refund entries linked to invoices, attach gateway confirmation, and record GST refund credits distinctly from revenue. Keep a monthly reconciliation pack with lists of refunds, dates, amounts, and links. AI Accountant stores attachments at the transaction level, easing auditor sampling and verification.

A results-driven finance and sales professional with hands-on experience through finance internships and a fast-paced sales role. With a strong interest in accounting and business finance, Harsh focuses on turning complex topics into clear, practical takeaways for founders and finance teams.